Quick Answer

Start by confirming DORA scope and obligations from primary legal text and authority guidance, not VAT materials. For platform payment systems, the article's practical baseline is six control lanes: governance, ICT risk management, incident response, testing, third-party oversight, and evidence retention, supported by clear owners, early escalation triggers, and a 90-day plan that closes the highest-risk gaps first.

How DORA Applies to Platform Payment Systems#

DORA is now an active operational resilience requirement for payment-relevant operations, not a future planning topic. It entered into application on 17 Jan 2025, and it covers ICT risk management, major ICT-related incident reporting to competent authorities, and ICT third-party risk management.

If you run payouts across markets, this is as much an operations issue as a legal one. Unmanaged ICT risk can disrupt cross-border financial services, and a local incident can spread beyond a single system.

This article gives you a right-sized 90-day path for DORA-aligned work in payments: minimum controls, a reporting checklist, and clear escalation points. The goal is to reduce regulator-facing surprises without adding process that does not materially reduce risk.

What DORA requires from platform payment systems#

Confirm DORA requirements for your platform payment system against primary DORA texts and competent-authority guidance rather than materials scoped to VAT obligations.

That gap matters. If a team drafts incident handling, resilience testing, or vendor oversight requirements from these VAT sources, the controls can rest on the wrong legal base. The audit trail can be weak from the start.

What you can say with confidence#

The current evidence set is not enough to specify DORA obligations for platform payments. It does not support concrete claims about ICT risk frameworks, major ICT-related incident reporting, resilience testing, or ICT third-party risk management.

What to verify next#

Before writing requirements, use a short checkpoint:

- Tie each claimed obligation to DORA legal text or competent-authority guidance, not VAT OSS or CBR materials.

- Keep an evidence log with source document, section, owner, and review date.

- Mark unsupported items as open questions instead of filling gaps with assumptions.

VAT artifacts — including dated OSS and CBR materials — do not establish DORA obligations for payment systems. Fix that evidence boundary before you assign owners or deadlines.

For a step-by-step walkthrough, see Gruv Platform Payments for Global B2B Payouts and Compliance.

Decide whether your platform sits inside direct DORA scope or third-party obligations#

Confirm every DORA classification against the relevant legal texts and current authority guidance rather than VAT materials. Structure your review around those primary sources, not indirect references.

The boundary is clear. These are official EU europa.eu pages, but they cover VAT OSS and CBR, not DORA scope. If you blur that line, you can misclassify a service as directly regulated when it is only contract support. You can also miss direct obligations where they do apply.

Build a provisional scope map first#

Put each service into one working bucket before you assign controls:

| Bucket | Working question | Immediate action | Common mistake |

|---|---|---|---|

| Directly regulated entity | Are you the legal entity providing the regulated payment or financial activity? | Mark as provisional until legal text confirms scope | Treating operational importance as proof of direct scope |

| Outsourced function | Are you performing part of a regulated firm's service under contract? | Map client, delegated activity, dependencies, and notice duties | Assuming the client's duty automatically defines your duty |

| Supporting vendor | Are you providing ICT or operations that support the payment path without owning the regulated service? | Rank outage impact and verify incident-cooperation terms | Labeling vendors non-critical by default |

For each row, record the legal entity, jurisdiction, function touched, relying partner or client, contract owner, source, open question, and review date. If no source is attached, keep the row unverified.

Keep legal duties and contract duties separate#

If legal review confirms direct regulation, define incident-reporting obligations from DORA sources, not from this VAT pack. The current pack does not support DORA triggers, timelines, formats, or thresholds.

If direct regulation is not confirmed, center your controls on contractual obligations. Focus on notification paths, escalation contacts, minimum incident facts, evidence retention, and the log access your regulated partners need.

Treat criticality as an internal risk call until legal status is confirmed#

Do not assume formal critical ICT third-party providers (CTPPs) status without confirming against the relevant legal texts. Internally, still treat any service that could disrupt payment execution or safeguarding at scale as business-critical for escalation, testing, and executive visibility.

Where classification depends on country interpretation, group structure, or partner licensing, log it as an open question for legal and authority review channels. Track the owner, missing source, interim assumption, and next review date. For a related operating example, see Healthcare Staffing Platform Payments Compliance for Safer Rollouts.

Build your minimum control set before adding extra process#

Start with a baseline that helps you detect, classify, report, and recover from ICT-related incidents in payment flows. Add process later. The goal is operational resilience you can prove with evidence, not a larger policy set.

Use six control lanes as an operating structure: governance, ICT risk management framework, incident response, testing, third-party oversight, and evidence retention. Treat this as an operating model, not a claim that DORA prescribes this exact structure.

Start with six lanes and make each one visible#

Make each lane produce one concrete, reviewable output. If a lane has no artifact, it is not operating.

| Control lane | Minimum output | Single accountable owner | Verification checkpoint |

|---|---|---|---|

| Governance | Inventory of ICT-supported business functions, roles, and responsibilities tied to payment activities | Compliance or risk | Dated version, approver, review date, linked legal entities |

| ICT risk management framework | Monitoring coverage for infrastructure health, application performance, and dependency mapping for payment journeys | Risk | Critical payment steps can be traced to supporting systems and providers |

| Incident response | Severity criteria, escalation path, and decision log for ICT-related incidents | Payments ops | Record shows who set severity, when, and based on which facts |

| Testing | Disruption and recovery scenarios with remediation owners | Risk or payments ops | Findings, owners, due dates, and retest status are tracked |

| Third-party oversight | Critical vendor list, contacts, notification duties, and recovery cooperation terms | Legal or risk | High-impact vendors are ranked and contract gaps are logged |

| Evidence retention | Evidence index for logs, tickets, vendor notices, approvals, and recovery actions | Compliance | Incident timeline can be reconstructed from retained records |

A useful early checkpoint is a documented inventory of ICT-supported business functions, roles, and responsibilities. If ownership, decision rights, and system support for payouts are unclear, the baseline is not stable yet.

Give each lane one owner, even if many teams contribute#

As an operating choice, assign one accountable owner per lane so decisions do not stall during incidents. Cross-functional input still matters, but one person should make the final call when facts are incomplete.

This matters most in incident response. Legal, compliance, and payments ops can all contribute. But one final decision owner should be clearly named for ICT-related incidents, with a deputy and an after-hours path.

Keep the owner register operational: owner, deputy, scope, decision rights, source systems, evidence location, and next review date. A missing deputy or evidence location is a control gap, not an admin detail.

Prioritize controls that reduce outage impact first#

Fund controls that reduce outage impact first, then improve documentation depth. The practical test is whether you can show real capability with evidence, including monitoring, incident reporting, testing, and third-party oversight.

| Priority control | What it covers or improves |

|---|---|

| Monitoring | infrastructure health, application performance, and dependencies across the payment path |

| Dependency mapping | shows which business processes rely on which technical components |

| Incident decision path | severity logging and evidence capture from the start |

| Third-party escalation contacts | notification duties for high-impact dependencies |

A common failure mode is underestimating dependencies. One availability issue can cascade into wider unavailability across interconnected financial services. Use a simple tradeoff rule: if a control does not improve containment, recovery, or incident decision quality, defer it.

Set incident triggers and reporting handoffs before your next outage#

At incident start, make one choice easy: escalate quickly when a payment event could be reportable, even before the final label is clear. If severity is uncertain, treat it internally as potentially reportable, involve legal early, and reassess as facts stabilize.

This is where the owner model has to work. The incident owner should not spend the first hour debating labels while impact grows and evidence fragments. The operational test is whether you can withstand, respond to, and recover from ICT disruptions with defensible records.

Use trigger labels that force action#

Use a short internal taxonomy to route incidents fast. Treat these as operating triggers, not formal legal categories.

| Trigger | Evidence or question |

|---|---|

| customer impact | affected journeys; impact start time; impact scope |

| payment delay | queue depth; settlement timing; whether movement is blocked or slowed |

| data integrity risk | reconciliation checks; whether records are complete, duplicated, stale, or corrupted |

| third-party outage | catch failures across payment dependencies, not only in your core app |

| recovery uncertainty | whether the recovery path, replay needs, or post-restart reconciliation are unclear |

Each trigger should map to specific evidence needs. For example:

- customer impact: affected journeys, impact start time, and impact scope

- payment delay: queue depth, settlement timing, and whether movement is blocked or slowed

- data integrity risk: reconciliation checks and whether records are complete, duplicated, stale, or corrupted

Include third-party outage explicitly. DORA-related standards are not limited to cloud-only events and cover ICT assets or services from ICT third-party service providers more broadly. Your triggers should catch failures across payment dependencies, not only in your core app.

Treat recovery uncertainty as a trigger in its own right. If the recovery path, replay needs, or post-restart reconciliation are unclear, escalate.

Make the handoffs explicit#

Define first hour, first day, and closure as internal operating stages so responsibilities and evidence are clear.

| Stage | Main objective | Required handoff | Minimum artifacts |

|---|---|---|---|

| First hour | Contain impact, preserve evidence, start escalation | Incident owner notifies payments ops, engineering, compliance, and legal when potentially reportable | Start time, suspected trigger, affected payment flows, current customer impact, systems or providers involved |

| First day | Stabilize facts and assess reporting tracks | Legal and compliance review facts for potential major ICT-related incident reporting and other applicable reporting tracks | Decision log, impact summary, dependency notes, draft timeline, vendor statements, recovery hypothesis |

| Closure | Finalize record, remediation, and authority-ready package | Compliance and legal confirm completeness before any external submission or closure memo | Reconstructed timeline, final classification, remediation owners, evidence index, sign-offs |

Use these as internal timing gates, not legal deadline claims. Their value is simple: each stage creates a handoff artifact that does not depend on memory.

Escalate uncertainty, not only confirmed severity#

A common miss is late escalation while teams argue about whether an incident is reportable. Secondary implementation commentary has flagged runbooks that did not match DORA Article 17 to Article 23 timelines, which led to delivery stress and rework. You do not need exact clock math to act on that risk.

Set a clear internal rule: if multiple triggers fire, or one trigger is severe and recovery confidence is low, escalate immediately to legal and compliance as potentially reportable. That does not force external filing on incomplete facts. It protects response quality while evidence is still available.

Do not close until reconstruction is complete#

Before final submission or internal closure, verify three points:

- timeline reconstruction is possible from retained evidence, not memory

- the decision log shows who made each severity or reporting call, when, and based on what facts

- the evidence pack is complete for supervisory follow-up, including incident reports, relevant testing records, and ICT third-party service records

Closure is often time-constrained. DORA closure work should show results, remediation, and supervisory cooperation. If you cannot reconstruct the event cleanly, keep it open, assign evidence gaps, and close only when the record is complete.

Fix ICT third-party contracts where payment risk actually concentrates#

Do not review every vendor the same way. Prioritize ICT third-party work where service failure could disrupt critical financial operations, including payment flows, or make recovery and reconciliation unreliable.

Start from an ICT third-party service provider register, then rank providers by payment-path criticality, not spend. Focus first on dependencies tied to payment execution and control points, such as processing, core cloud, fraud, identity, and messaging, before lower-impact back-office tools.

Rank by payment-path criticality#

Use one practical test: if this provider fails, can you still accept, route, release, confirm, or reconcile payouts without heavy manual work? If not, treat it as high criticality for ICT third-party risk management.

For each high-criticality provider, keep the register operational, not descriptive. Record:

- service used

- payment flow affected

- internal owner

- known subcontracting dependencies

- location of signed contract and amendments

This keeps oversight tied to real payment exposure instead of memory. Under DORA, ICT third-party risk management includes contractual provisions as well as monitoring.

Review contracts for resilience, not only commercials#

For high-criticality vendors, legal and service owners should check whether the live contract gives you enough leverage to manage an outage and reconstruct events.

In practice, review whether the contract supports:

- practical assurance or challenge mechanisms

- usable incident communication

- visibility into material subcontracting

- cooperation for containment, recovery, and evidence reconstruction

Do not assume one mandatory clause template or one fixed notification timeline. In practice, the standard is simpler: if the contract leaves you unable to verify impact or reconstruct what happened, it is weak for payment resilience.

Watch CTPP developments against your dependency map#

Keep a standing comparison between your high-criticality register and official supervisory developments on critical ICT third-party providers. If a provider you rely on appears in that context, recheck ownership, concentration risk, and contract currency.

Do not overstate this step. The oversight framework exists, but that does not mean every major vendor you use is officially designated.

Escalate refusals, do not bury them#

If a critical provider refuses core resilience terms, route it to executive risk acceptance with legal sign-off, not a silent exception.

At minimum, document:

- unresolved contract point

- payment flows exposed

- why replacement, redesign, or compensating controls are not immediate

- exception owner and expiry date

Undocumented exceptions tend to become permanent gaps. Treat materially weak contracts for critical providers as explicit leadership risk decisions.

Test resilience with payment-path scenarios, not generic IT drills#

Test resilience on payment journeys, not uptime alone. A useful drill asks whether a user can still complete a critical payment journey safely.

Start from the journey, not the asset#

Build resilience tests around the journeys that matter most to payouts and settlement. Keep the scope tight: start with three to five critical journeys, run one drill at a time for one journey, and keep outputs consistent so results are comparable.

Before each drill, map dependencies across the journey so teams agree on what is connected to what. If payments ops, engineering, and compliance do not share the same dependency map, align on it before the scenario starts.

Use payment failure modes that create real ambiguity#

Generic outage drills are not enough for payment-path risk. Include scenarios that create uncertainty in money movement and status, such as:

- degraded dependencies that block payment approval

- other journey-level failures that leave payment status unclear

These scenarios test whether you can control risk when the failure is ambiguous, not just whether systems stay up.

Keep your baseline controls, then add the DORA layer#

If you already run structured control testing, keep it. But do not assume existing compliance work automatically covers DORA.

Add a DORA-focused layer. Test how teams judge potential reportability under uncertainty and how quickly operations, engineering, and compliance coordinate once payment impact is suspected. Close each drill by recording outcomes in a consistent format so follow-up work is clear.

Create an evidence pack competent authorities can review quickly#

Build the evidence pack before incidents happen. Keep one indexed record set so a reviewer can move from event to decision to remediation without hunting across teams.

Include drill outputs alongside live incident records, vendor assessments, and reporting records. If those artifacts sit in separate systems with inconsistent naming, review and replay slow down for both competent authorities and internal audit.

Build one index, not five folders#

Use a single evidence index mapped to the obligation areas you apply under Regulation (EU) 2022/2554. This does not provide a DORA-specific required artifact list, so keep the structure disciplined and explicit rather than claiming a fixed template.

| Index field | Included detail |

|---|---|

| Obligation area | obligation area under Regulation (EU) 2022/2554 |

| Artifact | artifact name and purpose |

| Owner | owner |

| Version/date | version or effective date |

| Repository | repository location |

| Related ID | related incident, test, or vendor review ID |

| Last review | last review date |

| Legal/compliance note | legal or compliance note where interpretation is still open |

Keep artifact categories broad but clear: policy documents, incident logs, test outputs, vendor assessments, reporting records, and remediation evidence.

Preserve traceability from event to remediation#

Your pack should let someone outside the response team reconstruct the sequence quickly. Start from an alert or incident ticket, then show the timeline, decision owners, remediation tasks, and retest results.

Store links between records, not just the records themselves. Split custody across ops, legal, security, and vendor teams can create fragments instead of evidence.

Make reporting judgments auditable#

For potentially reportable events, record the decision path at the time facts are known, including later changes. Keep a short record of event ID, known facts, reviewers, rule set used, conclusion, and any upgrade or downgrade with the reason.

A useful parallel from EU reporting operations is process discipline. OSS materials explicitly cover record keeping and audits, and OSS VAT returns follow defined filing checkpoints (quarterly in the non-Union and Union schemes, monthly in the import scheme), with submitted returns and payments transmitted through a secure communications network. The point is not that DORA copies OSS; it is that review moves faster when the filing record, support file, and transmission trail are easy to follow.

If you make one change this quarter, require every incident and resilience test to produce a pack-ready record on day one.

Use a 90-day sequencing plan with owners and escalation points#

Use the 90 days as an internal execution cadence, not as a legal timeline. Treat the day ranges below as an example sequence you can adjust to your institution.

Start with proportionality. Tie your information security planning to business objectives, operations, risk, and compliance requirements, and scale it to your institution's nature and size. In practice, named owners, formal reporting lines, and emergency procedures for non-standard situations should come before lower-priority documentation.

| Period | Primary outcome | What to complete | Owner checkpoint |

|---|---|---|---|

| Days 1 to 30 (example) | Scope and accountability | Confirm scope for critical operations; assign first-, second-, and third-line responsibilities; baseline current controls and gaps against your information security plan | Each control area has one accountable owner and defined reporting/escalation lines |

| Days 31 to 60 (example) | Reporting and operational readiness | Review emergency procedures for non-standard situations, confirm reporting lines during escalation, and prepare standard reporting records | Decisions, actions, and outputs are captured in auditable records |

| Days 61 to 90 (example) | Gap closure and escalation readiness | Close highest-risk control gaps and verify oversight records are complete | Leadership can see who decides, who reports, and what records support each step |

In days 1 to 30, solve ownership first. If first-, second-, and third-line duties are unclear, formal reporting lines are missing, or escalation is implicit, response quality can break under pressure.

In days 31 to 60, pressure-test decisions, not just communication. Retain a clear record of decisions, actions, and remediation owners so the trail is auditable.

In days 61 to 90, focus limited capacity where it reduces incident risk fastest: reporting readiness and high-risk control gaps first, broader document polish second. Before you close the cycle, verify emergency procedures are current and check whether employees follow classification policy in practice, not only on paper.

Before locking your 90-day plan, pressure-test your incident, payout, and retry flows against implementation patterns in the Gruv docs.

Avoid overbuilding by using explicit stop rules#

Once ownership and evidence paths are in place, use a clear stop rule. Do not add a control unless it improves your ability to withstand, respond to, or recover from ICT disruption.

Use proportionality as the anchor. In the RTS process under Regulation (EU) 2022/2554, the European Supervisory Authorities (ESAs) introduced further proportionality and removed one governance article from the general regime requirements after consultation. Treat that as a practical signal to prioritize operational effect over control volume.

For in-scope payment operations, make the stop rule explicit in your control inventory. Before you approve a new control, record:

- the requirement it addresses

- the existing control coverage already in place

- the expected effect on prevention, detection, containment, or recovery for a payment path

If the expected result is only more documentation or oversight, defer it until there is a clear resilience gain. Keep a decision log with the source obligation, linked control, owner, and review date. That helps document why you relied on existing controls instead of adding duplicates.

Apply the same discipline to third-party oversight. DORA and the RTS cover ICT assets or services provided by ICT third-party service providers in general, but not every gap needs a permanent custom fix. Where temporary measures are used, assign an owner, record business impact, and set a remediation target so they do not become default controls.

If entity classification or cross-border supervisory interpretation is unclear, involve legal or compliance specialists early and pause assumption-based buildout. In this RTS, implementation deadlines were not changed because they are set at DORA Level 1.

Related reading: Building a Virtual Assistant Platform Around Payments Compliance and Payout Design.

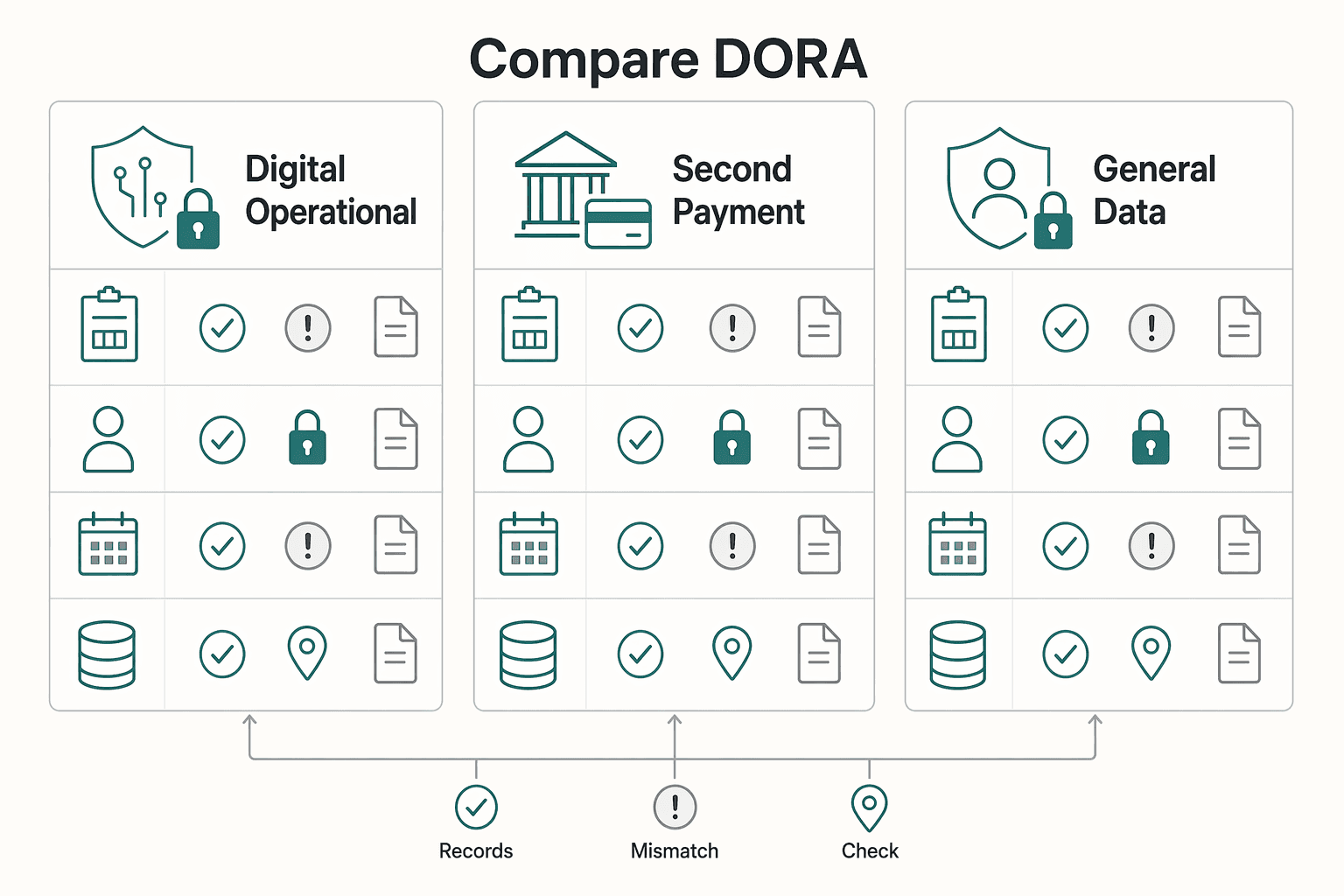

Compare DORA, PSD2, and GDPR so teams stop duplicating controls#

Use one cross-regulation event map and classify obligations by lifecycle and requirement category before creating new policy or evidence steps. That is a practical way to reduce manual, fragmented execution that can break down under pressure.

| Regime | Main purpose in your map | Practical trigger to review | Single source of truth | Primary evidence artifact | Open point for legal and competent authorities |

|---|---|---|---|---|---|

| Digital Operational Resilience Act (DORA) under Regulation (EU) 2022/2554 | ICT operational resilience and major ICT-incident reporting governance | ICT incidents or reportability decisions | Named resilience or compliance owner and the DORA incident policy | Master event record, reportability decision log, and governance artifacts (for example CA stock-taking inputs or stakeholder questionnaires) | Cross-border handling expectations and how to operate while Article 21 centralization remains exploratory |

| Second Payment Services Directive (PSD2) | Payment-related security or incident obligations that may overlap with the same event | The same event appears to affect payment-service operations | One named owner in the shared map, with legal-confirmed policy scope | Reused master event record plus PSD2 classification and decision notes | Whether the event needs a distinct PSD2 path or can reuse DORA evidence without conflicting labels |

| General Data Protection Regulation (GDPR) | Privacy and personal-data obligations that may be triggered by the same event | The same event appears to include personal-data impact | One named privacy or legal owner in the shared map, with legal-confirmed policy scope | Reused master event record plus privacy assessment and decision notes | Whether separate privacy handling is required and what evidence can be reused |

Keep overlap controls unified: intake, ownership, chronology, and evidence retention should start in one record. Branch only where regime-specific analysis is required. Do not assume a single EU reporting hub is already live. ESA centralization work under Article 21 is feasibility-focused and would still need further technical implementation steps and DORA amendments.

Related: How to Write a Payments and Compliance Policy for Your Gig Platform.

Conclusion#

DORA readiness for payment operations is an execution and evidence problem, not only a policy-writing exercise. Under Regulation (EU) 2022/2554, you need to show that your team can withstand, respond to, and recover from ICT-related disruptions and threats. You also need clear ownership and reviewable records.

Because DORA sets uniform requirements for network and information system security across the EU, the practical standard is defensibility. The technical standards process has also clarified expectations in areas such as network security, encryption, access control, and business continuity. Measure progress by controlled operations and evidence, not document volume.

A right-sized 90-day plan can be an internal sequencing tool, but it is not a regulator-endorsed finish line. Use it to confirm scope and owners first, then implement core controls, then verify each control with records.

Two outputs should stay in scope:

- the register of information alongside policy and process alignment

- an evidence trail that shows what happened, who decided, and what remediation was completed

Before you close the program, verify:

- each in-scope control has an accountable owner

- incident handling and escalation paths are documented and reconstructable

- ICT third-party dependencies are explicitly covered in your control set

- your evidence package is complete and review-ready, including the register of information

Timing and interpretation still matter. DORA came into force on 16 January 2023 and is cited as applicable from 17 January 2025, and requests to change level-1 deadlines were not accepted. The standards process also emphasized technology neutrality, so cloud-only thinking is too narrow for resilience.

Final step: confirm jurisdiction-specific interpretation with counsel and your supervisory context, lock owners and dates, and set verification checkpoints for open items. If scope, reportability, or third-party obligations are still disputed, escalate now with the exact provision, competing interpretations, and the business decision waiting on the answer.

If you want a market-by-market read on rollout constraints and compliance gating for your payout setup, contact Gruv.

Frequently Asked Questions

Is DORA already in force for payment firms?

The article states DORA is now active and cites application from 17 Jan 2025. It also says to confirm the date and your entity's applicability in primary legal text and official EU materials, then record who signed off internally.

Does DORA apply only to banks?

DORA scope by entity type isn't settled, so there is no basis for a banks-only answer. Document scope by entity, role, and owner of the conclusion, and do not use brand labels as a proxy for legal status.

What are the minimum workstreams to launch first?

Do not treat a generic checklist as mandatory unless you can trace it to source text. Start with a short obligations register that names owners, cites the exact rule text, and defines required evidence. The article's operating baseline then uses governance, ICT risk management, incident response, testing, third-party oversight, and evidence retention.

What should we do first if we are behind?

Confirm scope, timing, and evidence requirements before expanding policy drafts. Then split your gap list into confirmed legal requirements and optional good practice so effort stays targeted and rework is reduced.

How does DORA relate to PSD2 and GDPR?

Use one shared event record and one ownership map for shared facts. Keep intake, ownership, chronology, and evidence retention unified, then branch only where DORA, PSD2, or GDPR need regime-specific analysis. Get legal confirmation on what evidence can be reused and what needs separate handling.

What details are still uncertain from public summaries?

Treat any public summary as uncertain if it does not cite exact provisions, in-scope entities, or supervisory context. The article uses OSS guidance as a specificity benchmark because it states one Member State of identification, quarterly returns for Union and non-Union schemes, monthly returns for the import scheme, and a lock-in period for the current year plus two following years. If a DORA summary is less specific than that, treat it as incomplete.

When should we escalate to external counsel?

Escalate when unresolved interpretation could change legal exposure, reporting posture, or contract position. This is especially important when multiple entities or countries are involved. Bring an evidence pack with the open question, competing interpretations, and the pending business decision.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- content.leg.colorado.gov/sites/default/files/FY2026-27_humhrg.pdftrusted

- ec.europa.eu/finance/docs/level-2-measures/dora-regulatio...trusted

- eiopa.europa.eu/digital-operational-resilience-act-dora_entrusted

- esma.europa.eu/sites/default/files/2025-01/JC_2024_108_Repo...trusted

- esma.europa.eu/sites/default/files/2024-07/JC_2024-29_-_Fin...trusted

- eur-lex.europa.eu/legal-content/EN/TXT/PDFtrusted

- federalregister.gov/documents/2023/04/14/2023-05775/regulation-s...trusted

- hcpf.colorado.gov/sites/hcpf/files/FY26-27%20HCPF%20JBC%20Hear...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: