Quick Answer

Assign named owners first, then lock the minimum controls by day 30: vendor onboarding segregation, approval limits, verified bank-detail changes, and payment-release checks. Build one trace from request to settlement to General Ledger posting, and require the artifact at each step before calling the process controlled. Route ambiguous exceptions to human review, not automation. Expand volume only after your team can retrieve approval logs, tie-out support, and exception decisions without rebuilding evidence from email or chat.

Stabilize AP approvals, evidence, and exceptions first#

AP usually starts failing at scale in ordinary places, not exotic ones: unclear approvals, weak evidence, and exceptions that sit too long. This roadmap gives a Corporate Controller a practical 90-day path to stabilize those points while payout volume, entities, and compliance demands keep rising.

The goal is execution, not theory. In the first stretch, you need clear answers to three questions, backed by names and evidence rather than assumptions: who owns each control, what proves the control worked, and which failures must be escalated immediately. That is what turns AP from a busy queue into a controlled process that can hold up under close pressure, audit review, and cross-functional scrutiny.

A policy is not enough if nobody can produce the approval record, vendor onboarding file, payment log, or General Ledger support behind it. A simple checkpoint works well here: pick a recent payment, trace it from request through approval to posting, and confirm the proof is complete and retrievable. If the team can describe the process but cannot show the artifacts, assume the control is weaker than it looks.

The 90-day horizon is a management window, not a legal rule. It is useful because early controller priorities are usually framed around balancing growth with governance, and that is the real tension in AP. You are trying to stabilize quickly enough that month end does not depend on manual heroics. You also need enough discipline that the next entity, payout lane, or audit request does not expose the same gap again.

The biggest scope caveat is compliance design. KYC, KYB, AML, and tax handling vary by jurisdiction and by program, so you should not expect one checklist to work unchanged across all markets. The FATF Recommendations set a common AML and counter-terrorist financing framework, but countries implement that framework through different legal and operating measures. In the US, 31 CFR 1010.230 requires covered financial institutions to maintain written procedures to identify and verify beneficial owners, and Form W-8 BEN is submitted when requested by a payer or withholding agent. In the UK, the FCA is explicit that firms need a risk assessment, appropriate systems and controls, and due diligence. Tax outcomes can vary too, since treaty relief may reduce statutory withholding rates.

That means your AP design needs a documented place to collect, validate, and retain the right compliance and tax artifacts for the entity, corridor, and payment program involved. A simple day one red flag is this: if cross-border payouts are active and nobody can tell you which documents are required, who reviews them, or what blocks release when they are missing, escalate that before you scale volume. From there, lock the operating model so ownership is explicit before tooling starts hiding control gaps.

If you want a deeper dive, read How to Scale a Marketplace from 100 to 100000 Users: Payment Infrastructure Roadmap.

Set the operating model before you touch tooling#

Lock the AP governance operating model before you buy or expand tooling, because software can route approvals and store logs but cannot repair unclear ownership or weak evidence standards.

| Role | Focus |

|---|---|

| Policy owner | Control design |

| Execution owner | Day-to-day AP processing |

| Exception approver | Out-of-policy releases or overrides |

| Audit response owner | Evidence retrieval and walkthrough support |

Here, AP governance is the decision rights, internal controls, and evidence trails that keep outcomes consistent as volume grows. Internal control is a process carried out by management and staff, not just a policy file. If the team cannot name who decides, who executes, and what record proves completion, the control is not reliable yet.

Define the control chain before you debate org chart details. A practical chain runs from AP request through matching and approvals, then payment, then General Ledger posting, then AP sub-ledger-to-GL sign-off. AP posting profiles determine how vendor balances hit the General Ledger, and reconciliation checks whether AP sub-ledger totals match the AP control account in the GL. When that handoff breaks without clear ownership, close quality drifts quickly.

Set single-threaded ownership for four roles:

- policy owner for control design

- execution owner for day-to-day AP processing

- exception approver for out-of-policy releases or overrides

- audit response owner for evidence retrieval and walkthrough support

Run one end-to-end trace on a recent payment and put one name next to each control step, then pull the artifact for each step: approval record, posting record, and tie-out support. If ownership is shared or vague, treat that as a missing control until it is assigned. This is an operating rule, not a universal legal test, and it is especially relevant if your company has ICFR responsibilities under SOX Section 404. Related: A Guide to DAOs for Freelance Contributors.

Baseline the current state and find control breaks#

Once owners are named, baseline the live workflow before you optimize anything. Map the real path of money and evidence, then rank breaks by financial-reporting and audit exposure before you fix convenience issues.

Start with an end-to-end process map plus a clear ownership matrix. A RACI-style view makes handoffs and gaps visible quickly, especially when scaling introduces fragmented approval and invoice flows before controls are fully standardized. Treat the documented process as a draft until you confirm the live process.

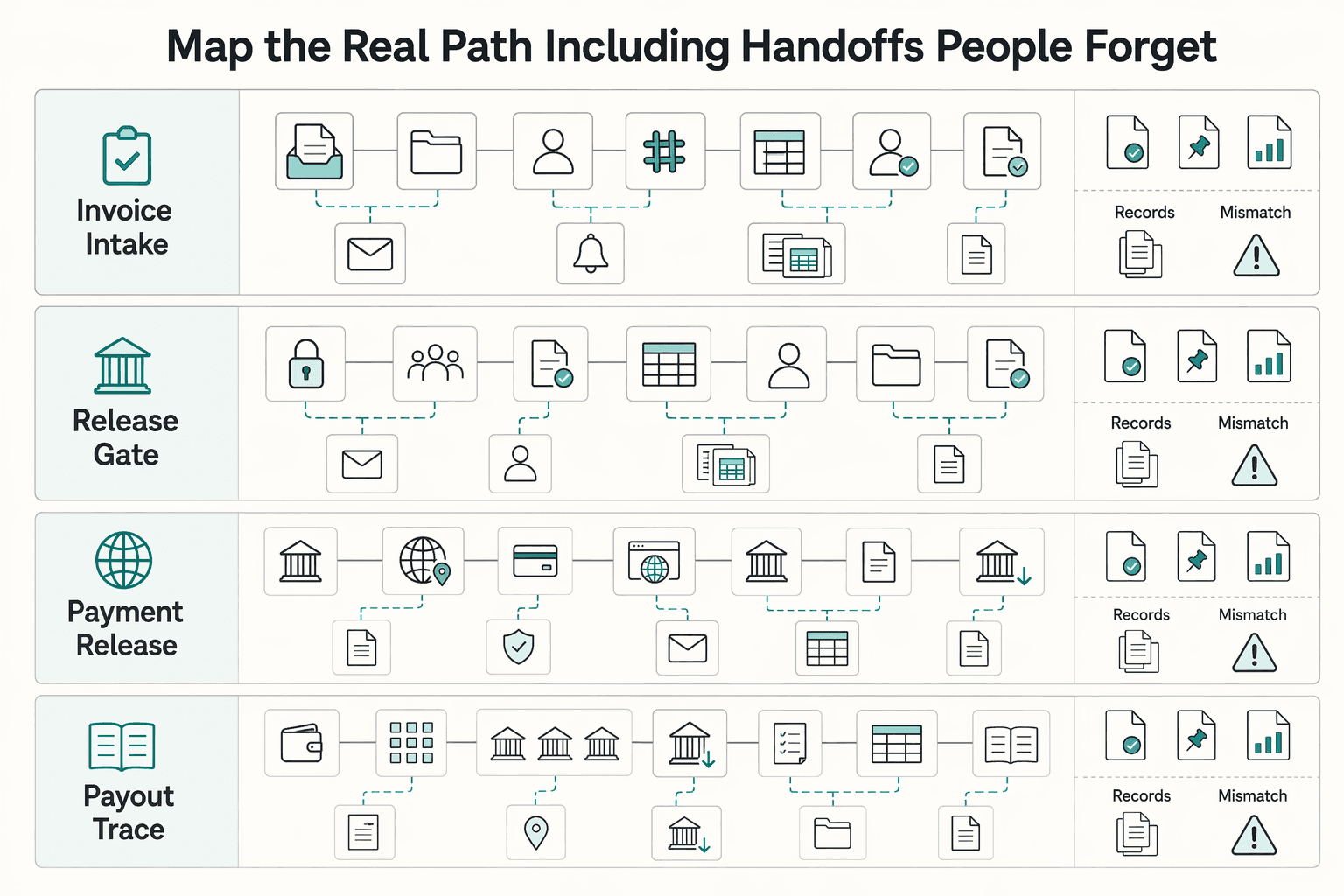

Map the real path, including handoffs people forget#

Build the map across four lanes: invoice intake and approval, payment execution, Settlements, and General Ledger posting and close tie-out. Include every system handoff and manual touchpoint, including shared inboxes, spreadsheet trackers, provider portals, Slack approvals, bank uploads, and manual status updates. If a step changes transaction status or evidence quality, it belongs on the map.

Validate with live transactions, not just a workshop diagram: one routine invoice, one cross-border payment case, and one payout batch. Cross-border paths usually need extra detail because they tend to be slower, less transparent, and more costly than domestic flows, which increases status hops and reconciliation risk.

Trace one transaction from invoice receipt to close sign-off and request the artifact at each step: invoice, approval record, payment submission record, settlement proof, General Ledger posting, and tie-out support. If the trail stops at a screen view or note with no retained export, treat that as a control break.

Define status states explicitly for each rail: "paid," "settled," and "final." If your team cannot say what event counts as settled and final for each path, cash reporting and close support drift.

| Process step | Owner | Control type | Failure mode | Current evidence artifact |

|---|---|---|---|---|

| Invoice intake | AP operations | Preventive | Decentralized intake, stale status updates, missing invoice trail | Intake mailbox record, AP system receipt log |

| Approval routing | Budget owner and AP approver | Preventive | Duplicate approvals, missing segregation of duties, out-of-policy release | Approval log, dated approver record |

| Payment release / Payout Batches | Treasury or AP payments lead | Preventive | Batch edited outside approved path, wrong payment status, unauthorized release | Payment batch submission record, bank or provider confirmation |

| Settlements | Treasury or finance ops | Detective | Unmatched deposits, unclear settled state, missing provider-to-bank tie-out | Provider settlement report, bank statement |

| General Ledger posting | Accounting | Detective | Late GL posting, wrong cutoff period, incomplete subledger-to-GL tie | Posting report, journal entry support |

| Sub-ledger / GL tie-out and exception review | Controller delegate | Detective | Open reconciling items, unresolved exceptions, aging not monitored | Completed tie-out, exception tracker |

Build a failure inventory you can actually rank#

After mapping, build a ranked failure inventory tied to repeat issues and financial impact. Prioritize duplicate approvals, unmatched deposits, stale status updates, late General Ledger postings, and unresolved exceptions. For each item, log date found, entity, amount, payment type, whether cash moved, detection method, and missing or weak evidence.

Prioritize exposure, not annoyance. UI friction can wait; breaks that obscure cash position, weaken reconciliation evidence, or block sub-ledger-to-GL support cannot. Documented reconciliation work is itself a control artifact, so unresolved exceptions without documented follow-up are both operating and audit risks.

Use a practical ranking rule: issues that can distort cash visibility, delay close, or prevent proof that a control occurred go first. Exceptions still open after a 30 to 60 day resolution window should be treated as a red flag that needs management ownership.

Lock day 30 non-negotiable controls#

By day 30, lock the minimum controls that stop bad transactions from moving and leave an auditable trail. Focus on vendor setup, approval thresholds, bank-detail changes, payment release, and close discipline.

Set this as a hard operating rule: if a payment path cannot prove who did what, when, where, from what source, and with what outcome, it does not go live.

| Control area | Minimum day-30 rule | Evidence to retain | Red flag |

|---|---|---|---|

| Vendor onboarding | Separate preparer, reviewer, and approver responsibilities | Vendor record, supporting onboarding documents, dated approvals | Same person creates and approves vendor |

| Approval thresholds | Publish an authority matrix tied to roles and monetary limits | Current matrix version, approval log by transaction | Amount bands exist informally in email or Slack only |

| Bank detail changes | Require callback verification or another out-of-band check before funds release | Callback note, contact used, date/time, approver | Change accepted from inbound email alone |

| Payment release | Enforce segregation of duties between payment preparation, approval, and review | Batch submission record, release approval, confirmation | One user can build, approve, and release the batch |

What minimum controls actually means#

Minimum controls should cover the core control activities: authorizations and approvals, verifications, reconciliations, and segregation of duties. For approvals, publish an authority matrix now and refine it later; do not wait for a perfect version.

Treat bank detail changes as a high-risk path with direct cash impact. Require callback verification through a known contact route independent of the change request, and require that artifact before release.

Tie Accounting Policies to the General Ledger close#

By day 30, your Accounting Policies should explicitly cover cutoffs, accrual handling, and exception aging. Cutoff discipline is simple: transactions and events should be recorded in the correct accounting period.

If AP marks a payment as complete but the General Ledger posts in a different period without documented rationale, treat it as a close-control break. Open exceptions that roll across close cycles without documented follow-up should escalate to controller visibility.

Make auditability and daily review hard gates#

Do not move a payment path to production unless it can produce auditable event records. At minimum, retain records showing what happened, when, where, source, outcome, and identity.

For high-risk queues, run daily exception review, especially where items can affect Liquidity Management or vendor-critical payouts. A daily exceptions report only works if review, disposition, and retained evidence have a clear owner.

Design approval and exception routing rules that survive volume#

At scale, approval and exception routing need explicit rules or volume will outpace your controls. Once day-30 controls are in place, make routing decisions system-readable so two reviewers reach the same outcome on the same transaction.

Start with one AP approval matrix teams can apply consistently. Use risk tier, approval amount limit, Vendor Management class, and payment type as the core inputs. Approval routing is meant to enforce hierarchy and limits before processing, so define the maximum each approver can authorize. In some setups, approvals above $500 are shown as an example; the threshold itself is not the takeaway. The takeaway is to set clear caps and tie them to vendor and payout context.

Build the matrix around real payment risk#

The most useful split is cash-risk exposure, not just transaction size. Keep amount bands, Vendor Management class, and payment type in the same rule set so routine, well-evidenced payments route differently from higher-risk requests.

Before rollout, sample five recent transactions across different vendor classes and confirm two reviewers would route each one the same way. If they would not, the matrix is still ambiguous and likely to be bypassed under pressure.

Write escalation as clear if-then logic#

Escalation works when it is time-bound and owner-bound. Define what happens when an item stays unresolved past a set age, and assign each step to a named role in your policy.

If-then routing should be explicit:

- If a payout is blocked by compliance or missing artifacts, route it to finance ops within your defined SLA.

- If it remains unresolved past that threshold, escalate to the next owner defined in your Accounting Policies (for example, the controller where policy assigns that role).

Separate exception handling into two lanes:

Can auto-resolve: deterministic condition, complete evidence, no new cash risk.Must be human-reviewed: compliance blocks, missing documents, approval-limit breaches, bank-detail changes, or repeated payout failure.

Retain routing evidence: blocking reason, timestamp, assigned owner, resolution note, and any artifact that cleared the hold.

Watch queue health across Payout Batches#

Track aging, reopen rate, and repeat-failure patterns across Payout Batches. Aging shows unresolved-item delay, reopen rate shows whether "resolved" stayed resolved, and repeat failures reveal recurring routing or data-quality issues in payout states such as paid, failed, or canceled.

| Signal | What it shows | Action if it rises |

|---|---|---|

| Aging | Unresolved-item delay | Check ownership and handoffs |

| Reopen rate | Whether resolved stayed resolved | Tighten auto-resolve rules |

| Repeat failures | Recurring routing or data-quality issues in payout states such as paid, failed, or canceled | Fix the root condition instead of handling each case as one-off noise |

Use those signals to act: if aging rises while volume is stable, check ownership and handoffs; if reopen rate rises, tighten auto-resolve rules; if the same vendor class or payment type keeps failing across batches, fix the root condition instead of handling each case as one-off noise.

For a step-by-step walkthrough, see Build a Public Roadmap in Notion That Keeps Client Scope Under Control.

Build the reconciliation and evidence pack auditors will ask for#

Your pack is audit-ready only when another reviewer can trace each payout from approval to provider reference to bank movement to General Ledger entry, or to a documented exception with an owner and dated rationale.

Keep the daily pack lean but complete: transaction log, approval records, provider payout references, payout reconciliation report, and a bank-facing settlement view. A provider export alone is not enough; you still need the approval trail, bank-side confirmation, and ledger impact in the same evidence chain.

Use one daily trace test: pick a bank credit, trace it back to the provider batch and transaction records, then forward to the posted ledger entry. If your provider settlement files include batch number, date, or unique IDs in filenames, mirror those IDs in your own naming convention so the trail is reproducible without handoffs.

Timing discipline matters. Stripe notes reconciliation data is computed daily beginning at 12:00 am, so align treasury and accounting pull times to avoid false deltas caused by refresh timing.

Daily and month-end pack design#

Month-end evidence should answer a different question: not just whether cash moved, but whether close is supportable and differences are understood. Add a close summary of differences, General Ledger tie-out, open exception list, and a shared cash movement view treasury and accounting both use.

Include Settlements and Cash Flow checkpoints in that month-end pack so payout-to-bank ties and period-close posting status are reviewed together. A difference is not a failure by itself, but it is a control failure if it is unexplained.

Artifact reference table#

| Artifact | Source system | Owner | Refresh cadence | Retention window | Audit use case |

|---|---|---|---|---|---|

| Transaction log | AP or payments platform | AP operations | Daily | Per policy | Shows transaction population and status |

| Approval records | AP tool or approval system | AP manager or controllership | Daily | Per policy | Shows authorization path |

| Provider payout reconciliation report | Payment provider reporting | Treasury or finance ops | Daily | Per policy | Matches bank payouts to payout batches |

| Settlement details report | Payment provider reporting | Finance ops | Daily or per settlement cycle | Per policy | Reconciles settlements at transaction level |

| Bank activity or payout-to-bank summary | Bank portal and provider reconciliation | Treasury | Daily and month end | Per policy | Confirms cash receipt and cash-flow position |

| General Ledger tie-out | ERP or General Ledger | Accounting | Month end | Per policy | Verifies posting completeness and explains differences |

Set retention by policy, not habit. If records are audit documentation in a PCAOB issuer-audit context, the retention baseline is 7 years, but do not assume one window fits every AP artifact.

Set the close gate#

Close is not ready until unreconciled deltas are resolved or documented with a controller-approved rationale under your accounting policy. For each documented delta, capture amount, batch or provider reference, cause, expected clearing date, and why it does not change the close conclusion.

If evidence shows a timing item that will clear next period, document it and proceed. If cause is unknown, support is missing, or results cannot be reproduced from the file set, keep the close open.

Decide what to automate now and what to defer#

Use your evidence pack to decide this, not instinct: automate high-volume, low-ambiguity steps first, and defer judgment-heavy exceptions until failure patterns are stable.

A practical rule is straightforward. Automate work that is repetitive, rules-based, and already reconciles cleanly. Keep anything that still depends on interpretation, missing documents, counterparty follow-up, or judgment calls in a controlled manual queue with a named owner and clear evidence requirements.

Prove retry safety before you widen the pipe#

Before expanding to new payout corridors, confirm your integration handles retries and duplicate webhook deliveries without duplicate side effects.

- Retry the same instruction with the same idempotency key and confirm one business outcome, one provider object, and one ledger impact.

- Replay the same webhook event and confirm your consumer deduplicates it using a persistent event identifier.

If either check fails, defer automation that releases funds or posts ledger entries until controls are fixed.

Virtual Accounts and MoR are different control choices#

Virtual Accounts and Merchant of Record (MoR) solve different problems, so compare them against your control goals before expanding automation.

| Path | What it changes | Control and reconciliation impact | Onboarding friction |

|---|---|---|---|

| Virtual Accounts | Uses non-real accounts tied to a real account for payments | Can improve cash-flow tracking and attribution, which can improve reconciliation transparency | Validate per provider and operating model |

| Merchant of Record (MoR) | Shifts legal payment-processing responsibility to the MoR entity | Centralizes financial, legal, compliance, and indirect-tax ownership; changes where close evidence is produced and what files you must obtain | Validate per provider scope, reporting, and support model |

Choose based on the bottleneck: if attribution and cash visibility are the problem, evaluate Virtual Accounts first; if legal, compliance, and indirect-tax operations are the bigger constraint, evaluate MoR first.

Do not leave items as a vague future phase. For each deferred automation item, record the owner, review date, and trigger condition for revisit.

Add compliance and tax gates without stalling payouts#

Set compliance and tax gates in onboarding, with a narrow exception path, so you catch issues before payment release instead of turning AP into a last-minute hold queue.

| Checkpoint | When to apply | Purpose or handling |

|---|---|---|

| KYC | Before account opening | Required customer identification data should be in place |

| KYB and beneficial-owner identification | At legal-entity onboarding | Include beneficial-owner identification at that same stage |

| AML manual review | For legitimate but incomplete cases | Route to manual review with a defined evidence pack and recorded decision |

| Form W-9 | When information-return reporting may apply in U.S. payer flows | Vendor record has the correct TIN |

| Form W-8BEN-E | For foreign entities | Document status for U.S. withholding and reporting |

| Form 2555 | If expatriate support is enabled | Run in a separate FEIE workflow |

| FBAR handling | If FBAR support is enabled and aggregate foreign financial accounts exceed $10,000 during the calendar year | Flag for separate handling |

| 1099 readiness | When reporting may be triggered | No missing tax form in the vendor record |

| VAT Validation | During onboarding and again if invoice entity details change for EU cross-border counterparties | Use VIES to confirm cross-border VAT registration status and store the validation result with a timestamp |

Use KYC and KYB as onboarding gates: required customer identification data should be in place before account opening, and legal-entity onboarding should include beneficial-owner identification at that same stage. Keep AML handling risk-based, and route legitimate but incomplete cases to manual review with a defined evidence pack and recorded decision.

Apply the same structure to tax checkpoints:

- In U.S. payer flows, collect Form W-9 when information-return reporting may apply, so the vendor record has the correct TIN.

- For foreign entities, collect Form W-8BEN-E to document status for U.S. withholding and reporting.

- If expatriate support is enabled, run Form 2555 in a separate FEIE workflow instead of mixing it into standard AP onboarding.

- If FBAR support is enabled, flag cases where aggregate foreign financial accounts exceed $10,000 during the calendar year for separate handling.

- For 1099 readiness, enforce a simple control: no missing tax form in the vendor record when reporting may be triggered.

For EU cross-border counterparties, run VAT Validation during onboarding and again if invoice entity details change. Use VIES to confirm cross-border VAT registration status, and store the validation result with a timestamp in your evidence set.

Do not treat this as one global rulebook. Coverage, tax handling, and legal obligations vary by country and by program, so assign a jurisdiction owner to confirm final legal and tax interpretation. Related reading: A 90-Day Leaving America Blueprint for US Expat Freelancers.

Conclusion#

A scalable AP governance plan is mostly a sequencing decision. Get ownership clear first, lock the non-negotiable controls second, and only then widen automation where you can prove the evidence trail holds up.

That order matters because growth and governance are not opposing goals. Internal controls are not just compliance paperwork. Used well, they support operations, reporting, and compliance at the same time, which is what a Corporate Controller needs as transaction volume rises faster than process maturity. Teams that treat AP as a control center, not a back-office queue, have clearer visibility into release timing, close risk, and exception priority because the facts are visible in one place.

The first test is role clarity. If nobody can name the owner for vendor onboarding policy, exception approval, payment release, General Ledger tie-out, and audit response, you do not have a mature process yet. You have activity without accountability. A practical rule is the one this article kept returning to: if ownership is unclear, treat the control as missing until it is assigned. That helps prevent stale exceptions, duplicate approvals, and last-minute controller overrides from becoming normal.

The second test is whether automation improved control quality or just buried weak judgment inside faster processing. Automated AP still needs clear approvals, separation of duties, audit trails, exception handling, and data controls. If a payment path cannot produce approval records, transaction logs, and a clean General Ledger tie-out, do not expand it yet. Keep the higher-ambiguity cases in human review until exception patterns stabilize. A common risk is automating around missing policy, then discovering the queue is faster but less trustworthy.

The third test is evidence. Audit readiness is not a presentation deck made at quarter end. It is the habit of keeping current artifacts that support what happened, who approved it, what cleared the payment, and how it landed in the books. Your checkpoint is simple: can you pull the daily or month-end pack without recreating it from email and chat history? If not, your documentation process is still fragile.

That becomes especially painful when compliance documentation is collected late or inconsistently. Keep it concrete: each item should name the owner, target date, control objective, evidence artifact, and escalation path if it slips. That is how AP governance can protect growth, cash flow decisions, and close quality in a way leadership can trust.

Frequently Asked Questions

What should a controller complete in the first 30, 60, and 90 days to stabilize AP governance?

In the first 30 days, learn the actual process, not just the documented one: map handoffs, find manual touchpoints, and baseline current performance. By 60 days, prioritize streamlining and efficiency improvements, starting with the most visible control and workflow gaps. By 90 days, evaluate what changed and present findings to leadership with evidence, not anecdotes: queue aging, reopen patterns, close delays, and unresolved deltas.

Which AP controls are non-negotiable before scaling payout volume?

You need hard stops for vendor onboarding, approval thresholds, bank detail changes, payment release, and tax or compliance gaps that would block legal payment. If a payment path cannot produce auditable logs, approval records, and a clear General Ledger tie-back, do not scale it. Those are internal controls in the basic sense: processes that give reasonable assurance over operations, reporting, and compliance.

What usually breaks first in AP when transaction volume increases?

Exception queues often strain before the payment rail does. Common signs include duplicate approvals, unmatched deposits, stale statuses, late General Ledger postings, and cases that keep reopening because nobody fixed the root cause. If you see backlog growth with weak ownership, close pressure and payment-release risk often follow.

How should teams measure whether AP governance is actually improving?

Start with a baseline and keep it stable long enough to compare. APQC points to cost per invoice as a useful benchmark, along with related process quality and speed metrics. Add control-oriented metrics such as exception aging, reopen rate, percentage of transactions with complete evidence, and unreconciled items at close. A simple checkpoint is whether fewer payments need last-minute intervention and whether close sign-off happens with fewer controller-approved exceptions.

When should AP exceptions be auto-resolved versus escalated to human review?

Auto-resolve only where the rule is bounded and the evidence is clear. Good candidates include duplicate detection, small price or quantity variances within tolerance, recurring non-PO spend with standardized coding, and supplier status updates that carry clear proof. Escalate when ownership is unclear, required artifacts are missing, or the issue touches compliance, tax status, bank detail changes, or unusual value or counterparty risk.

How do cross-border compliance checks affect payout speed and failure rates?

They tend to slow payouts most when controls are inconsistent or delayed. FATF has warned that a lack of risk-based, consistent AML/CFT implementation increases cost, reduces speed, limits access, and reduces transparency. In practice, teams can reduce disruption by collecting required compliance data earlier so payments are less likely to pause later for missing information.

What evidence should be ready at all times for audit and board-level oversight?

Keep a current evidence pack with transaction logs, approval records, reconciliation outputs, and General Ledger tie-outs, plus supporting compliance artifacts where relevant. The standard is not "some documentation." It is sufficient appropriate audit evidence that is relevant, reliable, and ready to support the conclusion.

Try a related tool

Harper reviews tools with a buyer’s mindset: feature tradeoffs, security basics, pricing gotchas, and what actually matters for solo operators.

Sources

- bis.org/publ/bppdf/bispap167.pdftrusted

- controller.berkeley.edu/accounting-and-controls/internal-controlstrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- europa.eu/youreurope/business/taxation/vat/check-vat-n...trusted

- finance.cornell.edu/controller/internalcontrols/unitlevelactivit...trusted

- gao.gov/products/gao-25-107721trusted

- guides.gaoinnovations.gov/greenbook/2025trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Scaling Marketplace Payments from 100 to 100,000 Users

Treat marketplace payments as an operating model decision, not a checkout widget decision. In a two-sided marketplace, customers pay the marketplace and the marketplace pays sellers. How well you scale depends on everything around that flow: monetization, merchant risk, payout operations, disputes, compliance, support, reporting, and fund recording.

DAO for Freelancers Who Need Payment Certainty

Treat any **dao for freelancers** opportunity as unconfirmed income until you verify who releases funds and how that release happens. A passed vote, active Discord, or busy forum thread may look encouraging, but none of it guarantees payment.

How Delaware Court of Chancery Clauses Change Freelancer Contract Risk

If your contract points disputes to the **Delaware Court of Chancery**, treat that as a business decision before you sign, not boilerplate buried at the end. Forum language can change remedy strategy and cost when a project slips.