Quick Answer

Start with alignment: contractor agreement dol audit survival depends on whether your signed terms, payment records, and owner responses match under review. Prioritize scope, payment, recordkeeping, and audit-cooperation clauses, then tighten Termination, Limitation of Liability, Indemnification, Governing Law, Jurisdiction, and Dispute Resolution. Build one response packet tied to the financial questionnaire, document owners, and a mock pull test before any live request.

Contractor Agreement Consistency Is What DOL Audits Actually Test#

If you want your contractor agreement to hold up in a DOL review, start with consistency, not length. Risk rises when the agreement says one thing, the payment records suggest another, and your internal team cannot explain the gap the same way twice.

That matters because the U.S. Department of Labor has revisited how independent contractor status is interpreted under the Fair Labor Standards Act. In its 2020 notice of proposed rulemaking, the agency said it was revising its interpretation of independent contractor status under the FLSA. A cautious takeaway is simple: the facts of the relationship may matter at least as much as the labels in the contract.

Get your materials together#

Have these four items ready before you touch clause language:

- your current contractor agreement templates, including any country or business-line variants

- a clean record of how contractors are onboarded, approved, and paid in practice

- named owners in legal, compliance, finance, and operations for regulator-facing questions

- one source of truth for legal text, one source of truth for payment data, and a written way to reconcile conflicts between them

A useful checkpoint here is boring but important. Pick one live contractor file and test whether you can tie the signed agreement to actual invoices, approvals, and payout records without manual guesswork. If that trail breaks, the first problem is operational evidence, not drafting style.

This guide is built for that real-world gap. It walks through which clauses need the most precision, what evidence each clause needs behind it, and when to escalate internally. The goal is not to imitate government contract forms or paste public clause libraries into a private platform contract. For example, FAR Part 52 is the federal acquisition part for solicitation provisions and contract clauses, not a default rulebook for private contractor arrangements.

One source-quality point also matters here. FederalRegister.gov itself notes that its Web 2.0 display is not an official legal edition. If you are making a judgment call on wording, timing, or legal effect, verify against the official agency or regulatory text, not a summary page or a circulated screenshot.

A common failure mode is trying to paper over messy operations with stronger legal language. If your team pays contractors across markets, the durable approach is tighter alignment between the agreement, the records, and the people who will respond when questions come in. The sections that follow focus on that alignment, with clause priorities, evidence packs, escalation checkpoints, and a closeout checklist you can actually use.

What a DOL audit actually asks you to prove#

You are proving that the real working relationship matches the classification, not just that the agreement uses the right label. In the DOL materials, the core issue is employee-versus-independent-contractor analysis under the FLSA, and the framing has changed across proposals rather than staying fixed.

Anchor your response to the current classification test#

Start with the current test, then map your facts to it. The 2020 WHD NPRM (RIN 1235-AA34) said DOL was revising its interpretation to promote certainty and reduce litigation, while the 2026 proposal (RIN 1235-AA46) says DOL would rescind the current 29 CFR part 795 analysis and replace it with the January 7, 2021 approach with modifications. Before you prioritize evidence, confirm the current finalized rule text.

Build the evidence file around real operations#

Build your file around how work actually happens, then check whether the contract and records tell the same story. Possible touchpoints can include notice, a financial questionnaire, records review, interviews, and an exit interview tied to a draft audit report, but the cited rulemaking materials do not establish that as a standard DOL audit sequence. Prioritize the signed agreement, onboarding records, invoice and payout trail, and manager-side records of day-to-day direction.

Separate the trigger from the core issue#

Triage the trigger, but keep it separate from the core classification question. These materials do not provide first-day triage rules for reporting discrepancies, member complaints, or election complaints, so treat those as internal response design choices. If facts and contract drift apart, fix operations first and contract second.

For a step-by-step walkthrough, see How to Conduct a Personal Security Audit as a Freelancer.

What to prepare before you redline any contractor agreement#

Prepare the evidence and ownership model before you edit language. If facts and versions are scattered, redlining can hide the underlying control gap and make version risk worse.

Gather the full contract set#

Collect every live agreement variant and every document incorporated by reference. That includes the base independent contractor agreement, any commission-based independent contractor agreement variant, all amendments, and each country or business-line addendum still in use. Confirm the attachment list in each active template against what teams actually send, because attachments such as a statement of work or compliance guidelines are part of the contract package, not background files.

| Document set | What to verify |

|---|---|

| Live agreement variants | Every active template and local version is accounted for |

| Incorporated documents | Each referenced document is pulled with the base agreement |

| Base and commission-based forms | Both are included if still in use |

| Amendments and addenda | Each one is matched to the current effective version |

| Attachment list | The template matches what teams actually send |

Before you edit text, verify the current effective version and what it replaced. Sample agreement language can state the agreement is the complete and final understanding replacing prior agreements, so version drift across old addenda or exhibits can undermine your redline.

Build a source packet first#

Build one source packet that shows how the relationship operated in practice. Include onboarding records, payment approvals, tax artifacts, and the current audit trail from payout and ledger systems. Use a simple check: can finance trace one contractor payment from approval to payout to ledger entry without rebuilding the timeline manually?

If not, pause drafting until the packet is clean.

Name response owners early#

Assign named owners across legal, compliance, and finance before any regulator contact. Document who receives outreach, who approves document production, and who is authorized to respond. Keep the ownership model explicit, with a designated contract manager role and a clear handoff path.

Build the contract clauses that hold up under DOL review#

Use a proof-first drafting sequence: scope and document hierarchy, then payment and recordkeeping, then enforcement and risk terms. Treat this as a practical drafting order, not a legal requirement. If a clause cannot be supported by records you already hold, narrow it or remove it.

Lock scope and document hierarchy first#

Start by treating scope and incorporated documents as one package. In the sample materials, that package includes Attachment A, Statement of Work, Attachment B, Subsidy Funding, and Attachment C, Compliance Guidelines.

Then make document priority explicit inside the agreement. The Georgia draft's Inclusion and Priority of Documents section is a useful structure, and FAR 52.102 Incorporating provisions and clauses is a reminder that incorporation works only when the referenced documents are clearly identified.

Before finalizing scope language, verify the exact attachment names and versions your team actually issues. This avoids the common mismatch where the master agreement, current work attachment, and older addenda do not align.

| Clause | Legal intent | Operational evidence required | Owner | Common failure mode | Escalation trigger |

|---|---|---|---|---|---|

| Scope of work clause | Define services and engagement boundaries | Current Statement of Work, onboarding records, active addenda | Legal with business owner | Current work differs from signed attachment set | Work performed does not match active attachments |

| Payment terms clause | Define approval, calculation, and payment flow | Payment approvals, payout export, ledger entry, tax artifacts | Finance | Contract flow and actual payout flow diverge | Finance cannot trace one payment end to end |

| Recordkeeping clause | Define retention and production expectations | Signed agreement set, amendments, audit trail, retention location | Compliance or contract manager | Records are promised but not retrievable as one package | No clear retention path or owner |

| Audit cooperation clause | Define a consistent response process | Owner map, response procedure, agreed document formats | Legal with compliance | Teams respond inconsistently across functions | Regulator outreach produces conflicting submissions |

Draft payment and recordkeeping around proof#

Write payment and recordkeeping clauses to match how your systems actually operate. A practical test is whether finance can trace one contractor payment from approval to payout to ledger entry without rebuilding the record manually.

Apply the same test to recordkeeping: one owner should be able to produce the base agreement, current attachments, amendments, and related payment history in one package. For audit cooperation language, keep it specific enough to drive consistent responses, but do not promise more than your team can actually execute.

Tighten risk terms after core clauses are stable#

After core clauses are stable, tighten Termination, Limitation of Liability, Indemnification, Governing Law, Jurisdiction, and Dispute Resolution so they do not conflict with how the relationship is documented and run.

Termination should align with your term section. The source materials show explicit Contract Term and Renewal language and stated end dates such as June 30, 2023 and up to 3 years. If any obligations continue after term end, state that directly instead of leaving it implicit.

If clause strength exceeds evidence strength, narrow the clause until every line is supportable in operations. Related: How to Handle Termination of an International Contractor.

Set Governing Law, Jurisdiction, and Dispute Resolution for multi-market teams#

Set these terms to the operating reality of each market variant, not to a single default template. If contractor location, payer entity, and payout corridor diverge, your governing law, Jurisdiction, and dispute resolution language should diverge too.

Map the real enforcement facts first#

Treat governing law, Jurisdiction, and dispute resolution as one decision. Before you choose language, map for each agreement variant:

- where services are performed

- which entity signs

- which entity pays

- where contract and payment records are stored

If those facts point to different places, escalate the template instead of forcing one forum. A quick verification check is to ask one contract owner and one finance owner, separately, where a claim would be filed and who can produce the signed agreement, current attachments, and payment history for that venue.

Pick the forum only after testing evidence mechanics#

Choose arbitration or court only after testing how evidence will actually be produced for that forum. Keep the decision tied to record access, document trail integrity, and who can support production, rather than assumptions about which route is always faster or easier.

If you incorporate outside rules, identify them precisely and lock the version. FAR Part 52, including Subpart 52.1 ("Instructions for Using Provisions and Clauses"), is a useful reminder that incorporation works only when the reader can tell exactly what is incorporated. Use the same caution with regulatory references: FederalRegister.gov states its prototype edition is unofficial and does not provide legal or judicial notice, so verify legal research against an official Federal Register edition.

State survival terms plainly#

If you want duties to continue after Termination, say so explicitly and align that language across termination and dispute sections. That can include ongoing record retention, payment true-up support, confidentiality, or cooperation with lawful information requests.

Run an operational check: if the relationship ended today, could your team still retrieve the base agreement, current SOW, amendments, and payout history without rebuilding access from scratch? If not, tighten process ownership before relying on stronger enforcement language.

Map every clause to internal controls and evidence owners#

Once venue and survival terms are settled, make each clause executable by assigning a control and an evidence owner. A clause is only useful in review if someone can produce the supporting record quickly and consistently.

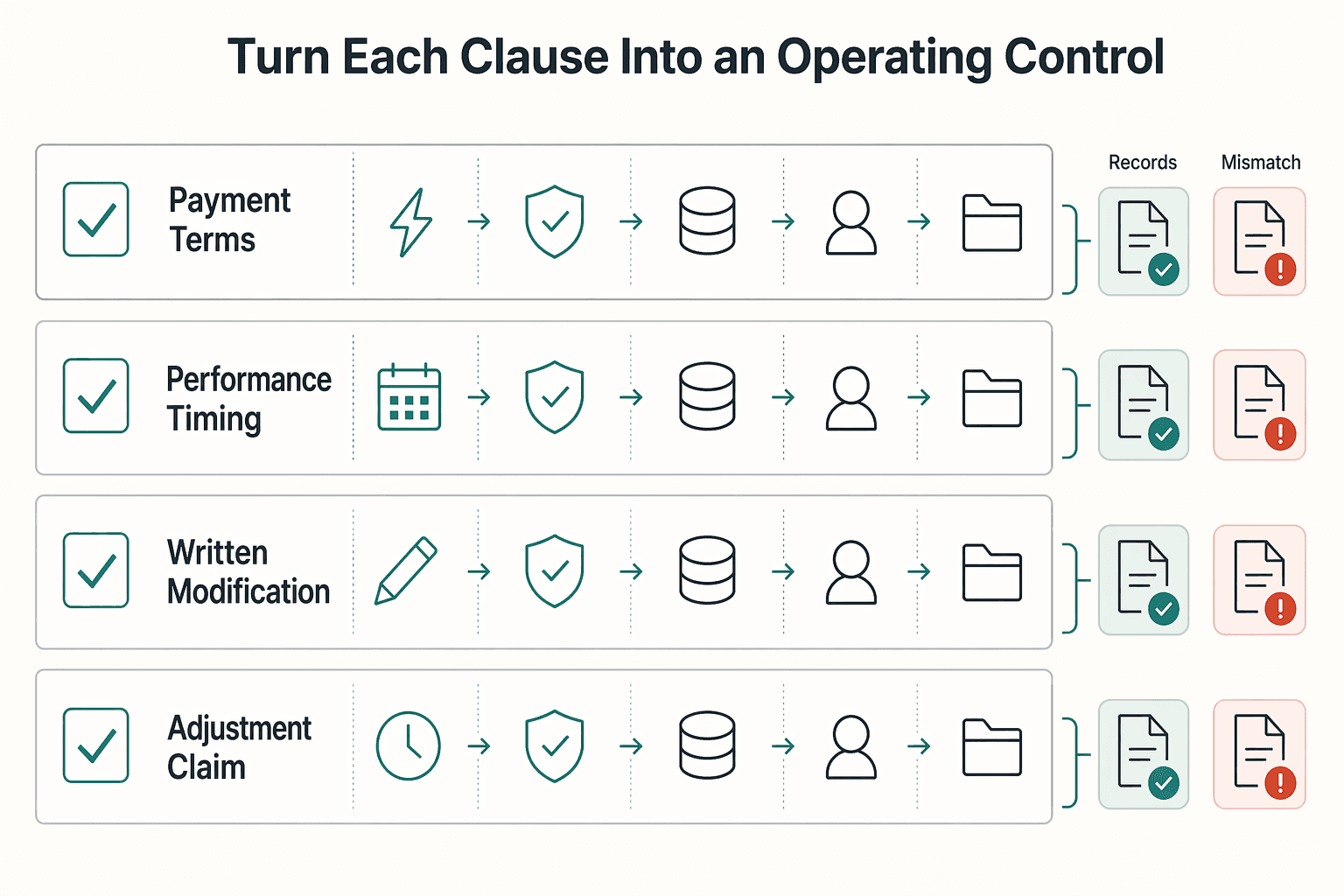

Turn each clause into an operating control#

Convert each high-risk clause into five fields: trigger, control action, system of record, reviewer, and retention path. If any field is missing, the clause is still legal text, not an operating control.

Be exact where the agreement already names a document or deadline. If payment is tied to Exhibit B, the control should require billings in the manner specified in Exhibit B and checks against the time and amount set there. Apply the same precision to Exhibit A timing, written modifications, and the thirty (30) day claim window.

| Clause | Internal control | Evidence artifact | Storage location | Owner | Backup owner | Response target |

|---|---|---|---|---|---|---|

| Payment terms tied to Exhibit B | Verify billing method, timing, and amount against signed Exhibit B before release | Signed agreement, Exhibit B, billing submission, approval record, payment record | Contract repository and finance record system | Finance owner | Compliance owner | Included in first response pack |

| Performance timing tied to Exhibit A | Check delivery timing against Exhibit A before acceptance; log exceptions | Exhibit A, completion record, exception log, approval record | Project file and contract repository | Service owner | Compliance owner | Included with timing response |

| Written modification requirement | Do not apply scope, price, or billing changes unless ordered in writing and reflected in current contract record | Written order, amendment record, approval chain, updated SOW | Contract repository | Contract owner | Legal ops | Included in contract packet |

| Adjustment claim within thirty (30) days | Date-stamp notice receipt, track the 30-day assertion window, and record continued performance status | Notice receipt, claim correspondence, timeline log, modified SOW evidence | Legal matter file | Legal owner | Operations owner | Included in exceptions file |

Assemble the evidence pack now#

Prepare the response pack before any request arrives. At minimum, keep the contract packet, payment history, exceptions log, and control attestations ready in one place.

The contract packet should include the base agreement, current SOW, Exhibit A, Exhibit B, and each signed written modification. If your contract sets a cap or date, make sure finance can show that limit and cumulative paid amount in the same pack (for example, a not-to-exceed amount of $3,617,600 through October of 2026).

Run a timed mock request#

Run a timed mock records request and assign handoffs in advance across legal, finance, ops, and compliance. Include one payment question, one modification question, and one timing question.

The test is simple: can one reviewer trace each answer to a signed contract document and a stored business record without version confusion? If not, fix the control map before the next audit request.

Set escalation rules for complaints, discrepancies, and regulator contact#

Set this up as an internal control: route reporting discrepancies, worker complaints, and regulator contact through separate intake lanes instead of one shared queue.

Create three intake lanes#

Use three lanes from day one: reporting discrepancy, worker complaint, and regulator contact. Capture the same core fields each time so handoffs stay clear: date received, source, issue summary, linked contract or contractor ID, current owner, and whether a government agency is named.

| Field | What to capture |

|---|---|

| Date received | When the issue came in |

| Source | Who raised it |

| Issue summary | A short description of the issue |

| Linked contract or contractor ID | The related contract or worker record |

| Current owner | Who is handling it |

| Government agency named | Whether a government agency is mentioned |

A quick check is whether a neutral reviewer can identify the lane, owner, and legal-notification status in under a minute. If everything is labeled as a generic "compliance issue," triage quality usually drops.

Set written escalation points#

Write escalation points as company rules before a live issue: what requires legal review, what triggers executive notice, and when outside counsel leads. Keep the matrix, contact roster, counsel list, and approval chain versioned and easy to retrieve.

When you reference regulations during triage, treat source status correctly. The eCFR page says its content is "authoritative but unofficial," and the excerpted Title 48 page shows "up to date as of 3/27/2026" and "last amended 3/13/2026." It also says OFR staff cannot answer questions about document content, so route interpretation questions to counsel, not website feedback.

Rehearse an interview protocol#

Define your protocol in advance for investigator contact: primary speaker, document coordinator, note-taker, and what can be answered immediately versus only in written follow-up after legal review.

If records conflict with the contractor agreement, pause discretionary cleanup, preserve the conflicting records, and use a legal-approved correction plan so your remediation trail stays controlled.

Recover from common audit findings without overbuilding process#

When the draft audit report arrives, do not rebuild your entire program. Close findings one by one with targeted control fixes and proof that those fixes work.

Fix evidence failures first#

Start with evidence gaps you can verify quickly: missing disclosures, incomplete records, inconsistent dates, or weak retention. Separate those from harder judgment calls so you can show concrete progress on retest.

If a finding involves reporting or disclosure, confirm the requirement before rewriting policy from memory. The DOL's Reporting and Disclosure Guide for Employee Benefit Plans (dated December 2022) describes itself as a quick reference for basic ERISA reporting and disclosure requirements and says it was prepared by EBSA with assistance from PBGC. Use it to confirm whether your disclosure fix is real, not just reworded.

Checkpoint: for each finding, a neutral reviewer should be able to identify the cited obligation, the affected record set, and the missing artifact in minutes.

Write the corrective plan against each finding#

Build the corrective action plan directly from the draft audit report, not a generic memo. For each finding, assign the following:

| Plan item | What to assign |

|---|---|

| Accountable owner | One accountable owner |

| Due date | One due date |

| Root cause | One root cause |

| Control change | One control change |

| Proof item | One proof item showing the fix is live |

Keep proof concrete: a revised contract template, a retention rule, a completed backfill log, a reconciled register, or a system-of-record export/screenshot. If a finding is a contract mismatch, fix the operating control first, then align contract language to actual practice.

Keep scope bounded. If someone tries to treat one finding as a full classification rewrite because of Federal Register RIN 1235-AA46, label that as separate policy monitoring. The document for 29 CFR Parts 500, 795, and 825 is a notice of proposed rule; request for comments, not a final effective rule.

Retest before closing#

Do a second mock request cycle before marking anything closed. Request the updated records, contract packet, and exact evidence you would provide if the U.S. Department of Labor asks again.

Use a higher bar than "policy updated": the team should be able to produce the corrected document set, with named owners and current versions, within your expected response timeline. If it fails that pull, the finding stays open.

Conclusion#

Getting through this is not about writing a longer contractor agreement. It is about making your contract terms, internal controls, and evidence outputs say the same thing if the U.S. Department of Labor selects your organization for audit and asks for a financial questionnaire, selected records, and interviews with the managers who actually own the work.

- Confirm your key contract clauses are backed by evidence.

Review your core clauses one by one and ask a blunt question: what record proves we operate this way? If you cannot point to the current agreement packet, amendments, approval history, and the operational records that support the clause, narrow the language or flag it for legal review instead of assuming the paper alone will carry you.

The checkpoint is simple: for each clause, you should be able to name one owner, one source record, and one storage location. A common failure mode is polished legal text with no matching evidence trail from finance or operations.

- Validate the owner map before the next notice arrives.

You need named owners for record collection, interview preparation, and approval of outbound responses to auditors. That map should show who works with counsel, who works with your CPA, who can explain payments and reconciliations, and who gives the final signoff before anything leaves the company.

Verify this by testing a real request path: if a DOL letter arrived today, could your team identify who completes the questionnaire, who attends the first meeting, and who approves written responses? If those answers live in someone's head, you do not have a reliable response structure yet.

- Run one mock request cycle and one exit interview prep cycle.

Do not wait for a live audit to learn where records are fragmented. Use a sample request built around records your team expects may be requested first, such as the contract packet, payment history, selected approvals, and the records behind your explanation of how the relationship is managed.

Then rehearse the exit interview stage as well. The point is not to script arguments. The point is to practice tying each management comment to a document pack that could support or correct a draft finding before it is finalized.

- Document what is still uncertain and escalate it cleanly.

Some gaps are operational and fixable now. Others are legal interpretation questions. Write those uncertainties down, attach the conflicting records or missing documents, and route the unresolved points to specialist counsel.

That last step matters because unresolved interpretation issues should not be settled by ad hoc business judgment during an audit response. The stronger closeout habit is to separate what you can prove today from what needs legal resolution before the next contract refresh. Related reading: How to Respond to an IRS Mail Audit Notice.

Frequently Asked Questions

What usually triggers a DOL compliance audit for contractor-heavy organizations?

The U.S. Department of Labor can select organizations for many reasons, and the examples in available guidance are not exhaustive. Available audit guidance names issues like failure to file, late filings, and obvious discrepancies in reports, along with election complaints or member complaints. Selection can also be random, with factors like size and location influencing who gets picked.

What should we do in the first day after a DOL notice arrives?

Contact your attorney and CPA first. Save the notice, confirm whether it requests a financial questionnaire or an initial conference, and set one response lead so answers and records stay consistent. A useful first-day checkpoint is knowing who owns the outbound response, who will attend the first meeting, and where the requested records are located.

Which records are typically requested before or during auditor interviews?

The grounded minimum is a request to complete a financial questionnaire and provide auditors access to selected records. Beyond that, use the notice and early conference to confirm exactly what is requested, who owns each item, and how you will deliver one consistent record set.

Who should be involved immediately: legal, finance, compliance, or operations?

At minimum, involve legal counsel and your CPA/finance team immediately. Also identify the company representative(s) who will attend the initial conference and coordinate responses. Depending on your operating model, compliance and operations may support document collection and factual explanations.

What are the most common findings tied to contracts vs recordkeeping?

This grounding pack does not provide a definitive contract-versus-recordkeeping ranking of findings. What it does support is that report discrepancies can trigger audit attention and that auditors may request selected records, so inconsistencies between reported information and underlying records are a clear risk area to address.

How should we handle an exit interview if we disagree with preliminary findings?

Treat the exit interview, or later final conference, as your chance to correct the record before findings are finalized. Ask which documents or facts support each draft point, and tie any disagreement to the exact records you can provide for auditor review before the report is finalized.

Try a related tool

Tomás breaks down Portugal-specific workflows for global professionals—what to do first, what to avoid, and how to keep your move compliant without losing momentum.

With a Ph.D. in Economics and over 15 years of experience in cross-border tax advisory, Alistair specializes in demystifying cross-border tax law for independent professionals. He focuses on risk mitigation and long-term financial planning.

Sources

- acquisition.gov/sites/default/files/page_file_uploads/Part-5...trusted

- acquisition.gov/far/part-52trusted

- capitol.tn.gov/Archives/Joint/committees/fiscal-review/cont...trusted

- dol.gov/agencies/owcp/energy/regs/compliance/Policya...trusted

- dol.gov/sites/dolgov/files/WHD/flsa/IC_NPRM_092220.pdftrusted

- dol.ny.gov/osh-attachment-a-1-a-2-and-a-3trusted

- dol.wa.gov/media/pdf/4907/sample-contracted-plate-searc...trusted

- dol.wa.gov/media/pdf/1278/mc-final-samplepdf/downloadtrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Structure a Commission-Based Independent Contractor Agreement

Commission agreements usually fail when key terms stay ambiguous. In practice, disputes start when the contract blurs contractor classification, leaves payout timing unclear, or leaves room for competing interpretations.

How to Handle Termination of an International Contractor

When you terminate an international contractor, treat it as a controlled legal and operational event, not a one-off conversation. A messy exit can trigger five risks at once:

How to Write a Contract for an Australian Client

**Use a one-sitting contract setup that secures scope, Payment Terms, and ownership before you debate price.**