Quick Answer

To handle an IRS mail audit, respond to the exact notice on time with organized copies of only the documents requested. Confirm the notice number, issue, contact, submission method, and due date before collecting records. Keep a full copy of your packet and proof of mailing, faxing, or upload. If anything is unclear or you cannot meet the deadline, call the number on the letter and ask for clarification or more time.

A mail audit is stressful, but you can still control the outcome#

An IRS mail audit is a document review, not an automatic claim that you did something wrong. Your job is simple: send a complete, on-time response that follows the notice and is easy for the reviewer to verify.

Start by treating it as a correspondence case#

Treat this as a correspondence case unless your letter says otherwise. IRS audits can happen by mail or in person, and a mail audit is handled through documents.

Build your response around the notice#

Start with the notice, then build your response around it. The letter tells you what is under review, what to provide, where to send it, and who to contact.

Before you collect records, use one checkpoint: can you clearly identify the issue, submission instructions, contact, and due date from the letter? If not, call the number on the notice and clarify that first.

Keep the scope tight#

Keep the scope tight. Send what was requested, organized so the reviewer can match each document to the item under review. Send copies, not originals.

Prioritize proof and traceability#

Make proof and traceability the priority. Keep a full copy of what you submit, along with your mailing or fax confirmation. If you fax, include your name and Social Security number on each page.

Escalate before you miss a deadline#

Use escalation early, not after a missed deadline. If you can document the requested items and respond on time, this can stay self-managed. If you cannot meet the deadline, call the number on the letter and ask for more time instead of missing it.

Once the IRS reviews your packet, it may accept your return as filed, ask for more information, or propose changes. That is why a complete, notice-aligned response is your best low-drama control point from day one. If you are weighing broader resolution options, see A Guide to the IRS Offer in Compromise (OIC) Program.

Know what arrived before you do anything else#

Before you gather records, identify the exact notice. Mistakes can start when people answer the wrong issue or miss a notice-specific deadline.

Find the exact notice number#

Find the CP or LTR number in the right corner of the IRS letter and copy it exactly. Do not assume it is CP2000, CP06, CP75, or CP75A unless that exact code appears on your notice. Confirm what the letter says is under review before you draft anything.

Confirm whether it is correspondence or in-person#

Confirm whether this is a correspondence audit or an in-person audit. The notice should say which process applies, and your next steps depend on that. If it is correspondence, treat it as a document review by mail. If it is in person, do not run a mail-only response plan.

Calendar the notice deadline#

Pull the response due date from the notice and treat that as the controlling deadline. Put it on your calendar first. Some IRS materials mention 30 days for mailed documents, but your notice controls, and replying by that date helps protect appeal rights if you disagree.

Compare the letter to your return before building the packet#

Compare the letter against your return and records before you build the packet. The notice should explain why your return is being examined, what documents are requested, and how to proceed. If your paperwork does not match what the IRS is asking for, contact the IRS employee named on the notice before you send anything.

Do a 20-minute triage before collecting documents#

Do a quick triage before you start hunting for documents. Get the case clear on one page, confirm where it sits in the process, and decide whether you can handle it yourself or need help.

Build a one-page case brief#

Create a short control sheet for your own use. A practical format is: tax year or years, items under review, the due date shown on the notice, and any notice identifier you use to track the case.

This is not an IRS form. It is your working brief. If key details are still unclear after a careful read, stop and clarify the notice before collecting documents.

Map the case to the process#

Use a simple checklist as a visual aid if that helps. The key question is whether you are still in the document-request stage of an audit by mail or already at a proposed-changes stage.

If you are still in the document-request stage, send the requested documents by the due date to the address in the letter. If you already received proposed changes, treat the case as beyond basic document gathering. Not every letter works the same way, and IRS audits can be by mail or in person.

Decide whether to self-manage or escalate#

If the instructions are unclear, call the number on the letter first. The notice should tell you what to provide, where to send it, and who to contact with questions.

If you still cannot match the requested items to records you actually have, move out of DIY mode and consider writing to the listed address, visiting a TAC, or getting help from a qualified tax professional. A self-managed case should have a clear record match for each requested item.

Write your call questions before you call#

Go into any call with written questions so you come away with useful answers, such as:

- What exact documents do you need for each item in the notice?

- What submission channel or address should I use for this case?

- What counts as a complete response at this stage?

If your records differ from what the IRS is asking for, ask the employee named on the notice how to handle that gap. Only move into document collection once the due date, requested documents, and submission path are all clear.

For a step-by-step walkthrough, see How to Keep Records for IRS Audits. If your records are split across countries, use the tax residency tracker to build a clean timeline before you assemble your packet.

Build your evidence packet in the same order the IRS reviews it#

A good packet is not just complete. It is easy to verify. A practical approach is to map each notice item to the exact support behind it and keep everything in that same sequence.

Build a response index keyed to the notice#

Consider starting with a one-page index that mirrors the items under review on your notice. Use a simple structure like: notice item, tax year, return line or schedule, supporting records, and where those records appear in the packet.

Behind each index entry, place the records in the same order. Organize them by year and by income or expense type, and add a short transaction summary when that helps the reviewer follow the trail and avoid misunderstandings.

Lead with return-matching support for income items#

For income issues, show a straight path from the notice item to the filed return amount to the underlying records. Use the same records you relied on to prepare the return, since the IRS request should not require you to create new ones. If the issue touches self-employment tax, include the support tied to Schedule SE so the calculation path is clear.

Organize credit items by the eligibility point in dispute#

When a notice questions a credit, group documents by the specific point you are trying to prove, not by broad document type. For each page, you should be able to say what it proves and why it matters to that item. Keep enough context with each document so it can be understood on review, and avoid sending a large, unmapped document dump.

Send copies and follow the notice logistics#

Send copies, not originals. Use the notice for submission instructions, including how and when to respond and where to send records.

Send the response through the channel the notice actually allows#

In a mail audit, the notice controls how you respond. Follow the method, destination, and due date in your letter first, then use the allowed channel.

| Channel | When allowed | Detail |

|---|---|---|

| Digital upload | Only if your notice explicitly allows it | Use the upload method listed in your notice and keep a copy of what you uploaded and any confirmation details |

| If your notice requires mail | Send the packet to the address in the letter; if documents do not fit in the provided envelope, use the address shown on that envelope | |

| Fax | If allowed on your letter | Include your name and Social Security number on every page and keep the final packet and any transmission records |

| TAC appointment | If you need in-person clarification | Use it for clarification, not as a substitute for notice instructions |

Read the notice like a delivery instruction sheet#

Your letter tells you what issue is under review, what to send, where to send it, and when it is due. Treat that due date and destination as the live instructions for your case.

IRS audits happen by mail or in person, but your correspondence case still runs on your specific notice. Some IRS materials mention sending documents within 30 days, but if your letter gives a different deadline, follow your letter.

Use digital upload only if your notice offers it#

If your notice offers digital submission, use the upload method listed in your notice. Use it only when your notice explicitly allows it, then keep a copy of exactly what you uploaded and any confirmation details you receive.

Build a paper or fax trail if digital is not available#

If your notice requires mail, send your packet to the address in the letter. If your documents do not fit in the provided envelope, send them to the address shown on that envelope.

Send copies, not originals, and keep a full copy set of everything you submit. If fax is allowed on your letter, include your name and Social Security number on every page. For mail or fax, keep a copy of the final packet and any transmission records you receive.

Use TAC appointments for clarification, not as a substitute for notice instructions#

If instructions are unclear, call the number on your letter first. If you need in-person clarification, make a Taxpayer Assistance Center appointment.

Read IRS Publication 3498-A before that conversation so you understand your responsibilities and rights during and after a mail audit. If you cannot meet the deadline, call the notice number to discuss your situation and request more time.

Handle refundable credit notices differently from income mismatch notices#

Refundable credit notices can require a different approach from income mismatch cases. Treat them as eligibility proof, not bulk document collection. Your goal is to match each IRS request to specific proof, then send only what answers that request.

| Notice or issue | Action | Detail |

|---|---|---|

| CP75 or CP75A | Start with Form 886-H-EIC | It is built for EITC audit document verification tied to listed letters |

| Not one of the listed EITC letters | Call the number on your notice | Get direction before sending documents |

| Amount-reconciliation issue | Answer the amount issue the notice raises | Do not default to an EITC packet |

| Math error notice | Check whether a 60-day abatement window applies | You generally have 60 days from the notice date to request abatement; after that, the assessment generally becomes final |

Identify the notice type before you build the packet#

If your letter is CP75 or CP75A, start with the Form 886-H-EIC toolkit. It is built for EITC audit document verification tied to listed letters.

If you did not receive one of the listed EITC letters, call the number on your notice for direction before sending documents. For amount-reconciliation issues, answer the amount issue the notice raises instead of defaulting to an EITC packet.

Organize proof by eligibility element, not by file category#

For EITC reviews, organize records by eligibility element, for example age, relationship, or residency, then attach the documents that prove that one element. This matches how the IRS toolkit structures the review and makes your packet easier to validate.

For dependent-related substantiation, Form 886-H-DEP shows concrete record types the IRS may request, including school, medical, daycare, or social service records. If your notice involves more than one credit, use the same discipline: map documents to the exact element under review, and do not assume one credit's checklist proves another credit.

Remove irrelevant records and escalate early when one element is weak#

More pages do not fix a missing eligibility element. If one required element is weak, stop padding the packet and call the number on your notice to confirm what records are acceptable for that item.

If you need support, check whether you qualify for help from TAS or a Low Income Taxpayer Clinic. If EITC was denied after an audit, the IRS may require Form 8862 when you claim EITC again.

Confirm whether a 60-day math-error window applies#

If your issue came through a math error notice, timing can control your options. You generally have 60 days from the notice date to request abatement. After that, the assessment generally becomes final.

Before you submit, verify the notice type, the exact item in dispute, and whether your packet directly proves that item. Related: How to Handle an IRS CP2000 Notice (Underreported Income).

What happens after you submit and how to decide your next move#

After you submit, IRS mail-audit guidance describes three possible responses: the IRS may accept your return as filed, ask for more information, or propose changes that can affect tax owed or your refund. Your next move should follow the letter you receive, not the stress of waiting.

Treat each new notice as a decision point#

Use the next notice to identify your branch and act on that branch.

| IRS response | What it means | Your next move |

|---|---|---|

| Accepted as filed | Your original return was accepted | No further action is needed; archive your file |

| More information requested | The IRS asked for additional information | Provide the requested information by the due date on the letter |

| Proposed changes | The IRS proposed changes to return figures | Compare the proposed changes to your return, then decide what you agree or disagree with |

Before you respond, confirm the notice matches the same tax year and issue you addressed.

If accepted as filed, close the case cleanly#

If your return is accepted as filed, you are done. Keep your audit records together for that tax year, including the notice and your response packet.

If more information is requested, fill only the named gaps#

A follow-up request means the IRS is asking for more information. Respond to the specific items named in the new letter and send your response by the due date shown on that notice.

If proposed changes arrive, decide based on the evidence#

If the IRS proposes changes, compare those figures to your original return first. Then decide whether you agree or disagree with some or all of them based on what your documents can support. If the basis for the proposed figures is unclear, stop and get help before responding.

Know your escalation triggers before you miss a deadline#

Escalate as soon as the case stops being a straightforward document check. The main triggers are unclear scope, procedural dead ends, and address or delivery risk that can put deadlines at risk.

Escalate when the case is no longer clear enough to answer cleanly#

If a notice appears to cover multiple years, multiple issue types, or proposed changes you cannot clearly trace, treat that as a practical escalation point. This is not a formal IRS rule. It is a risk-control cutoff for when interpretation starts to outweigh simple verification.

Use a quick checkpoint: can you summarize the tax year, issues, and support documents in one page after one careful read and one clarification attempt? If not, escalate before another deadline passes.

Contact TAS when process friction blocks a fair response#

If you are stuck procedurally, cannot get clarity through normal channels, or have notice or delivery problems that block a clean response, consider contacting the Taxpayer Advocate Service (TAS). TAS accepts direct contacts by phone or walk-in, and also by mail or fax.

When you contact TAS, bring a tight packet: notice, tax year, due date, short timeline, and proof of prior submissions or calls. TAS intake tracks the date your assistance request is received, and it includes an emergency escalation path for urgent cases.

Verify your address status before assuming you were never notified#

For globally mobile taxpayers, address issues are a real escalation trigger. The IRS generally uses the address from your last return. A notice sent to your last known address can be legally effective even if you did not receive it. IRS policy also expects clear notice of an address change.

Check your latest filed-return address against where you can reliably receive mail now. If there is a mismatch, document it right away and escalate. This matters operationally because the IRS sends over 200 million pieces of correspondence each year, and cited studies found high UAA rates, including for international mail.

Get targeted help early if cost or complexity is the blocker#

If cost or cross-border complexity is the bottleneck, escalate early so deadlines do not stack up. If process friction or notice-delivery problems are part of the issue, TAS is one intake channel you can use.

Cross-border records that can quietly weaken your response#

Cross-border responses can weaken when traceability is unclear, even if paperwork exists. Your best move is a clean, year-specific record trail that maps source documents to the filed return.

Rebuild one timeline for the tax year in question#

Start with one timeline for that year: where you were, which accounts were active, and which records fed the return. Keep it tight enough that someone else can follow each questioned item from a dated source document to the exact line of the filed return.

If you cannot do that yet, do not add more documents. Fix the timeline first so country, account, and date ranges do not conflict.

Keep Form 8938 and FBAR duties separate#

Treat Form 8938 and FBAR as separate filing tracks. Form 8938 is attached to your annual return and filed by that return due date, including extensions, while FBAR, FinCEN Form 114, is filed separately with FinCEN.

Do not treat one filing as a substitute for the other. Depending on your facts, you may need Form 8938, FBAR, or both. The IRS comparison page notes the FBAR $10,000 aggregate threshold at any time during the year. IRS Form 8938 materials note a $50,000 baseline threshold for certain U.S. taxpayers. Confirm your actual Form 8938 threshold based on your filing context before assuming either way.

If you spot a possible foreign-account reporting issue while answering a notice, separate the tracks. Respond to the notice as written, then evaluate Form 8938 and FBAR obligations on their own.

Keep only records that prove the chain#

Use records that prove ownership, period, and return linkage. Large attachments that do not support that chain can make your response harder to review.

This filter matters for Form 8938 because not every foreign-adjacent account is reportable there, including some accounts maintained by a U.S. payer. Also, if no income tax return was required for that year, Form 8938 is not required for that year.

Preserve one audit folder with dated proof#

Keep one case folder as your source of truth. Include the notice, filed return, any filed Form 8938, dated records relied on, submission proof, and call or follow-up notes. That folder protects you later because it preserves what you knew, what you sent, and when you sent it.

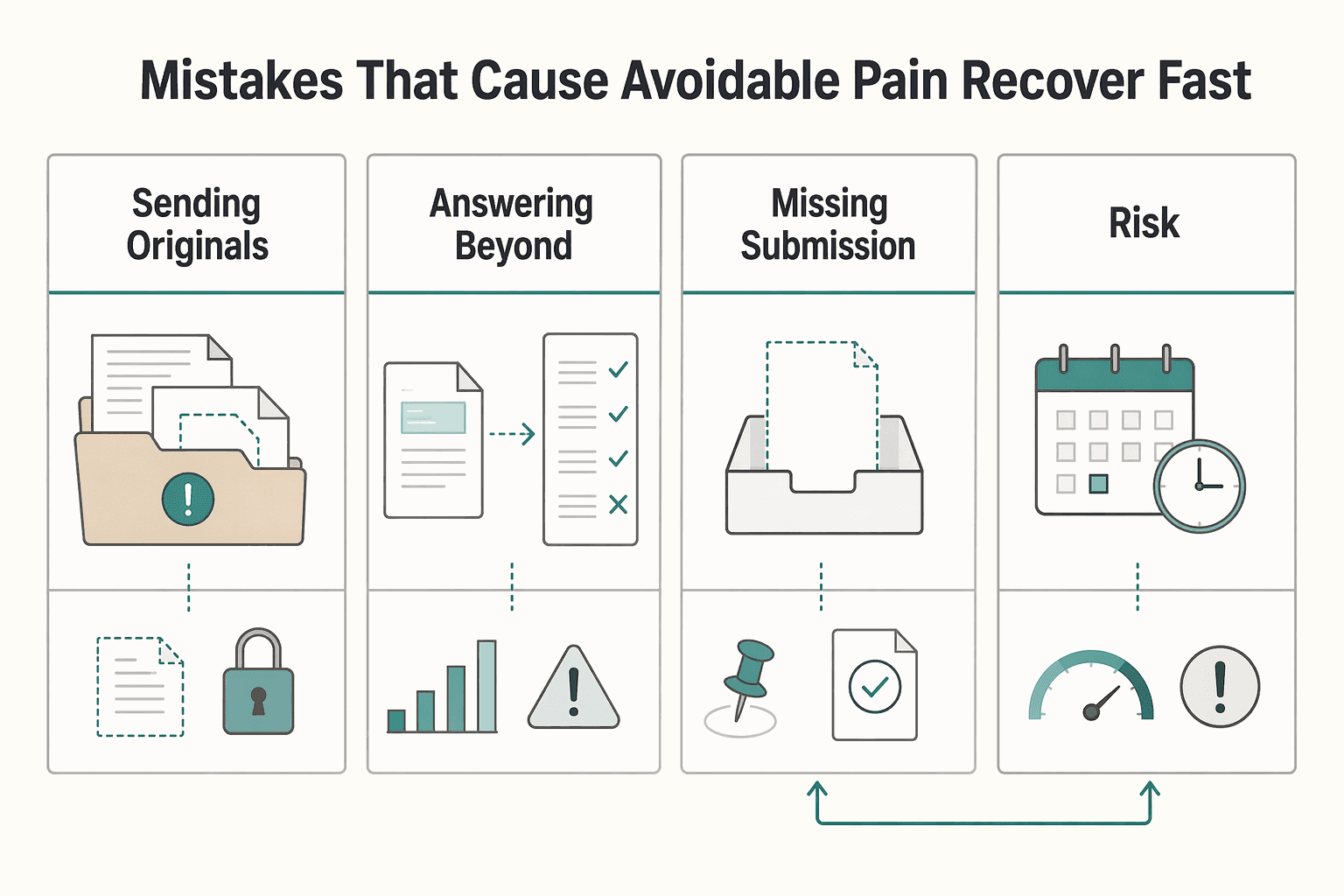

Mistakes that cause avoidable pain and how to recover fast#

Avoidable pain in a mail audit often comes from process mistakes: sending originals, answering beyond the notice, losing submission proof, and waiting too long to escalate.

| Issue | Do instead | Detail |

|---|---|---|

| Sending originals | Send copies, not originals | Keep a complete duplicate set in the same order; if faxing, include your name and Social Security number on each page |

| Answering beyond the notice | Let the notice define scope | Map each item you send to a specific request and send what was requested by the due date to the address listed in the letter |

| Missing submission proof | Create a send log | Record the date sent, channel used, address from the notice, and what was included; attach any upload confirmation, fax record, or delivery receipt you still have |

| Unclear instructions or deadline risk | Call the number on the letter | Request more time if needed, or ask for a TAC appointment, check whether you qualify for a Low Income Taxpayer Clinic, or involve a tax professional early |

Send copies only and label them#

If the IRS asks for documents, send copies, not originals. Keep a complete duplicate set of everything you submit in the same order so you can reproduce the packet if needed. If you fax documents, include your name and Social Security number on each page so they stay tied to your case file.

Answer the letter you got, not every issue you can imagine#

Let the notice define scope. Read the letter carefully, follow its instructions, compare any proposed changes to your filed return, and map each item you send to a specific request in that notice. Send what was requested by the due date to the address listed in the letter. If a document does not support a listed item under review, leave it out.

Rebuild proof of submission immediately if it is missing#

If your proof trail is weak, rebuild it now. Create a send log with the date sent, channel used, address from the notice, and what was included. Attach any confirmation you still have, such as an Exam DUT upload confirmation (if you used that channel), a fax record, or a delivery receipt. Submission proof does not prove the merits, but it protects your timeline and process record.

Ask for help as soon as clarity or deadline risk appears#

Escalate early when instructions are unclear or timing is tight. Call the number on the letter if you do not understand what to provide, and call that same number to request more time if you cannot meet the deadline. If you need more support, ask for a TAC appointment, check whether you qualify for a Low Income Taxpayer Clinic, or involve a tax professional early.

Final checklist before you send anything#

Before you send your mail-audit response, make sure it is complete, relevant, and aligned to your notice.

- I identified the key notice details, including the tax year, items under review, and the due date from the letter.

- I used the notice as my instructions for what to send, how to send it, and where to send it.

- I organized my supporting copies by year and by income or expense type, and included a short summary of transactions where helpful.

- I included relevant copies, not originals. If faxing, I put my name and Social Security number on every page.

- I used the submission instructions listed on the notice and kept a complete duplicate of everything I sent.

- I documented next checkpoints based on likely outcomes: accepted as filed, request for more information, or proposed changes, which may include Form 4549.

- If anything was unclear, or I could not meet the deadline, I called the number on the letter. If I needed extra support, I checked whether I qualify for LITC help.

Before your next filing cycle, review Gruv's tools hub to keep your documentation workflow consistent and audit-ready.

Frequently Asked Questions

What should I do first after receiving an IRS mail audit notice?

Start by pulling the key details from the letter, especially the items under review and the due date. Your specific notice controls the deadline and submission instructions. Then build a simple response index that maps each IRS request to the document you plan to send.

Does a mail audit mean I did something wrong?

No. A mail audit is a document review, not an automatic claim that you did something wrong. The IRS may accept your return as filed after reviewing your response.

Should I send original documents to the IRS?

No, send copies rather than originals. Keep a complete duplicate set of everything you submit. If you fax documents, include your name and Social Security number on each page.

Can I upload documents instead of mailing them?

Use the method listed in your letter first. Upload documents only if your notice explicitly allows digital submission. Keep a copy of what you uploaded and any confirmation details, and contact the person listed on the notice if you are unsure.

What happens after I submit my response?

The IRS may accept your return as filed, ask for more information, or propose changes. Follow the next letter you receive, not assumptions based on waiting. If the basis for the proposed figures is unclear, get help before responding.

When should I hire a tax professional for a mail audit?

Consider getting help if the notice is still unclear after you contact the person listed in the letter. You should also escalate if you cannot match the requested items to records you actually have or if you disagree with proposed changes. A qualified tax professional can help when the case is no longer a simple document check.

Can my refund be held during a credit-related audit?

This article does not give a blanket rule for when a refund will be held during a credit-related audit. Treat the timing as uncertain and follow the notice instructions exactly. A focused, complete response tied to the items under review gives the IRS what it needs to move the case forward.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

How to Handle an IRS CP2000 Notice (Underreported Income)

**Treat a [CP2000 notice](https://www.irs.gov/individuals/understanding-your-cp2000-series-notice) as a proposed change you must verify and answer on time, not as a final bill or final determination.** If you searched for **irs cp2000 notice freelancer**, you are not "in trouble" by default. You are looking at a records mismatch under time pressure, and you can manage it. You are the CEO of a business-of-one, and this notice is an operations problem to resolve, not a personal crisis.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.