Quick Answer

Start by treating vendor fraud red flags duplicate ghost vendors billing schemes as a sequence problem: verify vendor legitimacy, match invoice to a real obligation, then confirm payout destination integrity. In practice, align the vendor master record, invoice record, payment event, and any Purchase order (PO) link for the same transaction, and preserve approval and edit history before anyone changes records. Escalate when duplicate activity or account changes cannot be explained with documented evidence.

How duplicate and ghost vendor billing usually shows up#

Treat this as a pattern hunt, not a single-invoice review. In Accounts Payable (AP), losses can surface across vendor setup, invoice handling, and the payment rail together, especially when a fake vendor, supplier impersonation, or unauthorized bank payout is made to look routine.

That matters because AP fraud can come from inside or outside the company, and it can blend into normal operations. A ghost vendor scheme is not just a bad invoice. It is a fictitious vendor added to AP so money can move without real goods or services. A billing scheme may look different on the surface, but control gaps can still become a repeatable path to payment. A small control lapse gets treated as admin noise until it becomes a repeatable path to payment.

You can get better results if you check in the right order. Start with whether the vendor should exist at all, then whether the invoice matches a real obligation, then whether the payout destination changed or was redirected. If you reverse that order and jump straight to payment exceptions, you can miss the setup issue that explains the whole case.

A useful early verification point is simple. Line up the vendor master record, invoice record, payment event, and any Purchase order (PO) link for the same transaction. If the names are close but not exact, the bank details changed recently, or the invoice cannot be tied back to a valid service or PO, do not let AP close it as a clerical oddity without notes. The red flag is rarely one mismatch on its own. It is the cluster.

One control weakness deserves early attention: segregation of duties. When vendor onboarding and invoice approval sit with the same person or a very small team, ghost vendor risk rises because creation and approval can reinforce each other without an independent check. That does not prove fraud, but it should change your posture from routine review to documented validation.

This guide is built for that first pass. It focuses on three scheme types that can create confusion in payout operations: ghost vendors, duplicate invoice payment cases, and broader billing schemes. The goal is not to freeze every questionable payment. It is to help you contain the cases that deserve it, collect enough evidence to separate process error from intent, and know when AP should stop owning the decision alone.

Keep your evidence standard high from the start. Preserve approval history, vendor edit history, invoice images, and payment timestamps before anyone "fixes" the record. Detection is often delayed, so preserving the trail early matters.

What to prepare before you start#

Preparation should make a suspicious invoice a contained case, not another AP exception.

| Step | Focus | Key items |

|---|---|---|

| 1 | Assign named owners | AP, compliance, and legal; document who can pause a payment, who approves that pause, and who must be informed the same day |

| 2 | Build one working dataset | Vendor master data (with Tax ID), invoice records, payment events, Purchase order (PO) links, and bank account change history |

| 3 | Confirm control baseline | Use current invoice matching rules, actual segregation of duties, and any known internal controls exceptions or temporary workarounds |

| 4 | Set escalation channel | Route fake vendor or account information, or signs of unauthorized electronic transfer activity, to the named compliance or legal owner; preserve notes, timestamps, and export versions at handoff |

Step 1: Assign named owners in AP, compliance, and legal before review starts. Document who can pause a payment for suspected invoice fraud, who approves that pause, and who must be informed the same day. If authority is unclear, high-risk items can sit in queue until they are paid or edited.

Step 2: Build one working dataset that can be matched across records. Include vendor master data (with Tax ID), invoice records, payment events, Purchase order (PO) links, and bank account change history. GAO frames data analytics as a fraud-control activity and data matching as a way to verify key information, so your first checkpoint is whether one vendor record can be tied to the invoice, approval trail, and payout trail without guesswork.

Step 3: Confirm your control baseline before interpreting exceptions. Use your current invoice matching rules, actual segregation of duties, and any known internal controls exceptions or temporary workarounds. A suspicious mismatch means something different when it bypasses an existing control versus when no control was set for that case.

Step 4: Set the escalation channel in advance. If AP finds fake vendor or account information, or signs of unauthorized electronic transfer activity, route the case directly to the named compliance or legal owner instead of routine ticket triage. Preserve notes, timestamps, and export versions at handoff so later review can distinguish processing error, control failure, and intent.

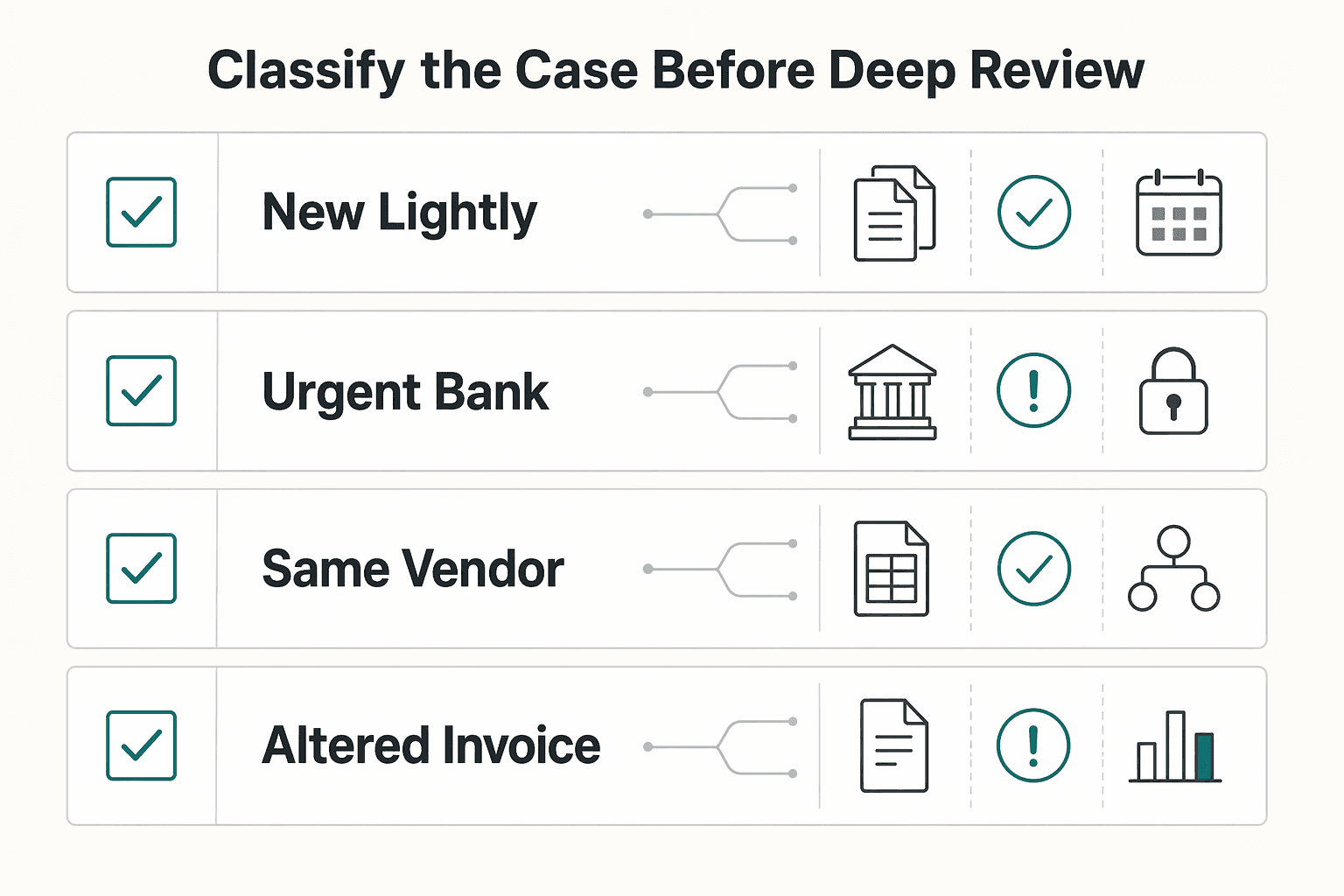

Classify the case before deep review#

Classify the alert before detailed review so you can choose containment and evidence steps early, instead of treating every exception the same way.

Step 1 Assign a working risk class: internal, external, or collusive. Use these as triage labels, not a formal standard. If ownership is still unclear after a first pass through vendor master data, invoice history, approval trail, and bank-account change history, treat the case as higher risk and require compliance sign-off before releasing queued payouts.

Step 2 Map the alert to the most likely scheme type: ghost vendor, supplier impersonation, ACH payment fraud, or duplicate processing. Common AP fraud schemes include billing schemes, ghost vendors, invoice duplication, and unauthorized ACH transactions. At this stage, classify for proportionate containment; do not try to prove intent yet.

| Signal | Likely actor and scheme | Immediate containment action | Evidence required to move from suspicion to incident |

|---|---|---|---|

| New or lightly used vendor with invoices but weak PO or service trail | Internal or collusive; ghost vendor | Pause pending payouts and lock vendor-profile edits | Vendor master record, Tax ID match result, PO link, receiving/service evidence, approval history |

| Urgent bank-change or remittance-update request from a new contact | External or collusive; supplier impersonation or ACH payment fraud | Hold release, verify through known contacts already on file, review recent bank-change events | Change log, original vendor contact record, email/domain comparison, callback notes, payment timing |

| Same vendor, amount, or invoice number appears twice | Internal error or fraud; duplicate processing | Stop the second payout and check for an existing reversal or credit | Invoice image, payment-event trail, duplicate-check result, reversal/adjustment record |

| Altered invoice fields, rush request, unusual vendor activity, or financial inconsistencies | Internal, external, or collusive; billing scheme or duplicate scheme | Escalate for same-day review and preserve current export versions | Invoice versions, approval timestamps, exception notes, matching-rule outcome |

Step 3 Confirm one containment checkpoint before marking the case as contained: the suspect vendor cannot still be paid through an already approved batch.

Step 4 Build the evidence pack to match the classification. For ghost vendor concerns, focus on vendor profile integrity, Tax ID consistency, PO links, and proof of service/receipt. For impersonation or ACH concerns, prioritize bank-change history, known-contact verification notes, and the payment-event timeline.

This early split helps reduce avoidable escalation and keeps review effort targeted. Related: A Guide to Dunning Management for Failed Payments.

Build a red-flag matrix your team can execute#

Build this matrix before alerts move through AP. A red flag should never stand alone; each one needs a defined check, a clear escalation trigger, and a record of what is still unknown.

Start with five working columns#

Use five columns: signal, likely scheme, validation step, escalation threshold, and unknowns. The unknowns column keeps reviewers from treating early patterns as proof of intent.

Keep it practical. This is a fraud risk assessment tool for execution, so it should direct attention to higher-risk work in procurement and payment activity instead of treating every exception the same way.

Tie each signal to one concrete check#

Build rows from the red flags and control inconsistencies you already see, then tie each to one repeatable check.

| Signal | Likely scheme | Validation step | Escalation threshold | Unknowns |

|---|---|---|---|---|

| Duplicate-looking payment activity tied to the same vendor record | Duplicate processing or billing scheme | Run a transaction history review across invoice, payment, and reversal/credit records | Escalate if the event trail does not clearly explain the duplicate pattern | Whether behavior reflects process error or intentional resubmission |

| Supplier activity that is inconsistent with normal operating patterns | Billing scheme, impersonation, or collusive activity | Perform a vendor-bank detail comparison against prior approved instructions and recent change history | Escalate if reviewer cannot verify the change path through approved records | Whether the change came from a legitimate vendor request |

| Invoice and internal records do not align on key fields | Billing scheme or processing error | Record the invoice matching outcome (pass/fail/exception) and supporting review notes | Escalate if mismatch remains after document-level validation | Whether mismatch is clerical, timing-related, or intentional |

| Open red flag with incomplete supporting records | Undetermined | Identify the missing record and assign owner/date for follow-up validation | Escalate if required evidence is still unavailable at review deadline | Whether available data is sufficient to close safely |

The validation step should be specific enough that two reviewers would perform the same action and reach the same documented result.

Set a closure rule before alerts start closing#

Set one rule and enforce it: do not close alerts as error only without documented validation evidence. Closed files should show the check performed, the outcome, and what remained unknown at closure.

That separation between suspicion, validation, and escalation is what keeps avoidable losses from becoming harder and more costly to investigate later. For a step-by-step walkthrough, see 10 Freelance Contract Red Flags That Scream 'Run Away'.

Run the first 24 hours in fixed order#

Use a fixed internal triage order for day one: contain, validate, scope, escalate, then document. This is an operating sequence, not proof of intent or a legal standard.

| Order | Action | Details |

|---|---|---|

| 1 | Contain exposure | Pause suspect payouts and isolate the vendor records and invoices tied to duplicate-payment or fictitious-vendor signals so records are not changed mid-review |

| 2 | Validate the record chain | Run a transaction history review and trace creation, edits, approvals, payments, reversals, credits, and re-entry; compare Tax ID consistency and confirm PO, invoice, and service-delivery records align if your file includes them |

| 3 | Scope the pattern | Check whether patterns touch one vendor, one employee, or multiple entities; repeated exceptions tied to the same internal actor, shared vendor details, complaints about pressure to pay kickbacks, or recurring favored-supplier arrangements are escalation clues |

| 4 | Escalate | Move to compliance or legal when evidence suggests intentional billing schemes, supplier impersonation, or attempted ACH payment fraud |

| 5 | Document | Preserve logs, reviewer notes, and decision timestamps for each hold, release, and escalation, including what remains unknown |

Separate duplicate processing errors from fraud signals#

A "duplicate" should start a review, not end it. In Accounts Payable (AP), duplicates can come from processing mistakes, but duplicate invoices are also a known fraud pattern where the same invoice is submitted repeatedly to obtain multiple payments.

Reconstruct the event history before labeling the case#

Treat an apparent duplicate as a hypothesis to test. Confirm the full sequence with timestamps: original entry, exception or duplicate handling, approvals, and final payment or reversal outcome.

If the file only says "duplicate" without a clear payment outcome and review trail, keep the case open. When the issue is a real processing miss, close the control gap and document exactly what failed so the same pattern is visible next time.

Verify the duplicate still ties to a real obligation#

Shift toward probable fraud when the record no longer fits a normal processing explanation. AP fraud is manipulation of the payment process for personal gain, and known patterns include fake invoices, vendor collusion, ghost employees, business/vendor email compromise, duplicate invoices, and phantom vendors.

Test whether the duplicate still ties to a real supplier and a real obligation. A familiar vendor label is not enough without support from the underlying records.

Escalate repeat patterns into formal case handling#

Repeated "errors" linked to the same vendor or internal review path should move out of routine cleanup and into formal case handling. You do not need certainty of intent to escalate; you need a repeat pattern with documented evidence.

That control matters because AP fraud can remain undetected for long periods, and isolated closures can hide broader schemes. Your verification point is simple: someone outside the case should be able to reconstruct the repeat behavior from the file alone.

Tighten controls without breaking payout operations#

When a duplicate starts to look intentional, add targeted controls instead of blanket friction so you catch billing fraud patterns without stalling clean payouts.

| Control area | What to tighten | Checkpoint |

|---|---|---|

| Invoice matching | Compare the vendor record, amount, date, purchase order (if one exists), and whether the goods or services were actually expected | For any released invoice, a reviewer should be able to trace the match result and see what exception, if any, was approved |

| Segregation of duties | Put separation around vendor setup or edits, invoice approval, and payment release; use risk-based approval tiers where exposure is higher | The audit trail should show who changed the vendor, who approved the invoice, who released the payment, and whether any one user handled more than one of those actions |

| Exception paths | Define one urgent-payment path before teams improvise around controls; require a business owner, a second approver outside the request chain, and a documented reason | Complete a post-release review; the red flag is when urgent payouts skip evidence collection and no one follows up |

Strengthen invoice matching before adding broader friction#

Start with stronger invoice matching, because it usually adds less operational drag and catches common billing schemes early. In AP, matching should compare the vendor record, amount, date, purchase order (if one exists), and whether the goods or services were actually expected, not just a raw invoice number. That matters because documented billing-fraud patterns include duplicate invoice submissions, inflated invoices, and charges for goods or services never provided.

Your verification point is simple: for any released invoice, a reviewer should be able to trace the match result and see what exception, if any, was approved. A common failure mode is duplicate logic that only catches exact string matches, so punctuation, spacing, or date edits still pass.

Put separation around vendor edits, approval, and release#

Enforce segregation of duties at the highest-risk steps: vendor setup or edits, invoice approval, and payment release. If one person can do all three, you are over-trusting a single account and a single explanation.

Use risk-based approval tiers so extra review is applied where exposure is higher, not on every routine payout. Vendor due diligence and multi-step authentication are specifically cited as measures that reduce financial-loss risk, so use them where your data shows elevated risk.

A practical checkpoint is the audit trail: you should be able to show who changed the vendor, who approved the invoice, who released the payment, and whether any one user handled more than one of those actions.

Define exception paths before adding more holds#

Extra holds can reduce fraud risk, but they also increase payout latency, so define one urgent-payment path before teams improvise around controls. Require a business owner, a second approver outside the request chain, and a documented reason, then complete a post-release review.

The red flag is not that an exception exists. The red flag is when urgent payouts skip evidence collection and no one follows up.

Build the escalation packet auditors and counsel need#

Once a case may be intentional, lock it into one packet so a new reviewer can reconstruct what happened, what failed, and why you escalated without chasing side threads.

- Build one standard evidence pack. Include a short case summary, affected invoices, a payment timeline with timestamps, vendor profile history, and control-failure notes. For duplicate, ghost-vendor, or billing-scheme indicators, tie each conclusion to visible facts (for example, vendor edits, invoice mismatches, missing PO support, or release overrides).

- Add cross-functional records, not just AP exports. Include AP review logs, compliance decisions, and legal escalation rationale tied to specific indicators. Make roles and timing explicit: who reviewed, who edited the vendor record, who approved or paused payment, and when.

- Attach tax and jurisdiction context only when your file already supports it. If the file includes 1099, W-8, or W-9 records, attach the document or status note, collection date, and any mismatch or staleness issue. For foreign-account context, label FBAR explicitly as the FinCEN Report of Foreign Bank and Financial Accounts.

If maximum account value is relevant, record each account separately and convert to U.S. dollars rounded up to the next whole dollar (for example, $15,265.25 becomes $15,266). State scope limits clearly, such as "FBAR timing noted for counsel review only," because the cited April 15, 2027 extension applies to certain individuals with signature authority and no financial interest, while other FBAR obligations in that notice remain due April 15, 2026. Related reading: Building Subscription Revenue on a Marketplace Without Billing Gaps.

Conclusion#

The thread through every alert is order and proof. Move fast, but use a clear sequence: classify the case, validate red flags against records, contain money movement early, and escalate after you can show what happened and what still remains unknown.

That discipline matters because Accounts Payable fraud is, at root, manipulation of the payment process for personal gain. It can show up as fake invoices, vendor collusion, ghost vendors or ghost employees, duplicate invoices, or business and vendor email compromise. The excerpts supporting this draft indicate these schemes can sit undetected for long periods while draining cash and straining operations. The practical mistake is not missing one odd invoice. It is treating a pattern as a one-off processing issue before checking the basics.

Your best verification point is simple: can you tie the vendor, invoice, and payment activity to a credible business purpose with normal support and a believable event sequence? If the answer is no, do not close the case as "error only." One failure mode is seeing a duplicate payment and stopping there instead of checking for additional red flags in the same records.

Containment also needs judgment. You do not need final proof of intent before pausing a suspect payout or isolating a vendor record for review. You do need enough documented fact to explain why the payment should not keep moving while AP sorts it out. If the matter includes signs of collusion or complaints that someone was pressured to pay kickbacks, treat that as more than an AP cleanup issue. In government contract settings, that type of pressure complaint is described as a fraud indicator.

Use this as an internal closeout checklist template:

- Pull vendor, invoice, payment, and related support records

- Classify the likely case pattern

- Check records for additional red flags

- Contain suspect payouts while review continues

- Document what is known vs still unknown

- Escalate with documented facts when risk remains

If you want one operating rule to keep, make it this: no alert is resolved until the records support the explanation. That standard will not eliminate every false positive, but it can reduce the chance of releasing money on weak facts and leave compliance or legal with something usable when a billing scheme turns out to be real.

Frequently Asked Questions

What is a ghost vendor in AP operations?

In the AP fraud material here, ghost vendor is listed as a scheme category, not a single fixed legal definition. In practice, treat a vendor record as high risk when invoice or payment activity cannot be supported by normal documentation and a legitimate business purpose. If the file is thin, exception-heavy, or built around missing support, treat it as a fraud-risk signal rather than a routine cleanup task.

What is the difference between a duplicate invoice payment error and duplicate invoice fraud?

A duplicate payment error can have an ordinary processing explanation with a documented correction trail. Fraud risk rises when the duplicate sits next to altered invoice details, unusual vendor activity, rush payment pressure, missing documentation, or other financial inconsistencies. If you cannot document a clean processing mistake, do not close it as error only.

Which red flags should teams check first when time is limited?

Start with the signals you can verify quickly and that can travel together: duplicate payments, altered invoices, unusual vendor activity, rush payment requests, and missing documentation. If you have only minutes, also scan for exception-heavy activity tied to the same people and any complaint suggesting kickback pressure from a vendor or subcontractor. Your first pass should answer one question: does this look like routine AP noise, or does it show coordinated behavior worth pausing?

When should AP escalate a case to compliance or legal?

Escalate when the facts suggest more than a processing mistake, especially possible ghost vendors, billing schemes, invoice duplication with suspicious context, unauthorized ACH activity, or kickback-related pressure. There is no fixed universal threshold in the material here, so use an evidence rule instead: if AP cannot explain the pattern with normal records and controls, move it up. A repeated “error” pattern involving the same people or vendor is a strong red flag.

Can invoice matching alone prevent billing schemes?

No. Invoice matching helps, but it is only one control. You still need segregation of duties, reconciliations, and independent approvals because consistent internal controls make fraud harder and help anomalies stand out earlier. A match result should not end review when vendor setup or supporting documentation looks questionable.

What can red flags show, and what do they still leave unknown?

Red flags can show patterns such as duplicate activity, altered records, unusual payment urgency, missing support, and exception-heavy dealings around the same people. They do not prove intent by themselves, and they usually do not tell you whether you are looking at carelessness, collusion, or a deliberate invoice fraud attempt. That is why your escalation packet needs additional records, including payment events, vendor history, and evidence of where controls failed.

Try a related tool

Asha writes about tax residency, double-taxation basics, and compliance checklists for globally mobile freelancers, with a focus on decision trees and risk mitigation.

With a Ph.D. in Economics and over 15 years of experience in cross-border tax advisory, Alistair specializes in demystifying cross-border tax law for independent professionals. He focuses on risk mitigation and long-term financial planning.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- clame.nyu.edu/default.aspx/E17608/315589/Fraud%20Risk%20As...trusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- fincen.gov/reporting-maximum-account-valuetrusted

- gao.gov/assets/870/866764.pdftrusted

- grants.az.gov/sites/default/files/fraud%20paper.pdftrusted

- theiia.org/globalassets/site/chapters/united-states/geo...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

SaaS Usage-Based Pricing for Predictable Cashflow and Fewer Disputes

If you are considering **saas usage-based pricing**, treat it as an operations and collections decision first. Pricing works best when the usage unit can be measured, shown on the invoice, and explained by someone outside your product team.

A Guide to Dunning Management for Failed Payments

If you run recurring invoices, failed payments are not back-office noise. They create cashflow gaps, force extra follow-up work, and increase **Involuntary Churn** when good clients lose access after payment friction.

Credit Invoices Explained: How to Issue Reversals and Adjustments in a Subscription Billing Platform

Once volume grows, credit invoices, invoice reversals, and invoice adjustments stop being simple billing edits. They become order-to-cash events that affect customer balances, accounts receivable, accounting records, payment matching, and sometimes fund finalization on a different timeline. The practical mistake is treating them like one back-office task when they are really several linked records that have to stay in sync.