Quick Answer

Yes. Automate commission payouts only when the request matches principal-authorized escrow documents, and hold anything that does not. In the California example, the June 30, 2025 DFPI/DRE Joint Bulletin says escrow trust funds follow written instructions from principals, while brokers are not principals to the escrow transaction. For operations, that means auto-release is limited to document-matched payees and approved split outcomes, while reroutes, late payee edits, and unresolved recipient status move to manual legal or compliance review.

How commission and closing payouts work#

At closing, the controlling question is who can lawfully instruct the escrow holder to release trust funds. In California, the June 30, 2025 guidance from the Department of Financial Protection and Innovation and the Department of Real Estate makes the boundary clear. An escrow agent disburses trust funds based on the written escrow instructions of the principals to the transaction, not solely on a broker's request at closing.

That sounds narrow until you try to productize commission payouts. California regulators warned about a specific pattern involving a Commission Disbursement Authorization, or CDA: independent escrow companies issuing checks from the escrow trust account to pay third parties for a broker's personal or business expenses. The bulletin says those practices may violate California Real Estate Law and Escrow Law. It also states something founders should treat as a product boundary, not a footnote. The principals are the buyer and seller, or the borrower and lender. Brokers are not principals to an escrow transaction.

Before you start

- Treat California as a concrete example, not a rule you can export automatically to every state or country. - Ask for the written escrow instructions and identify the transaction principal before you design payout logic.

For operators, that changes the shape of the work. The question is not just whether your platform can calculate a split or schedule a closing disbursement. It is who is legally allowed to instruct the escrow holder, and whether the payee and payment purpose match what the principals actually authorized. In the California fact pattern this guide starts from, a broker-entered payout form by itself may not be enough.

Use a simple rule. Automate only what you can tie back to principal-authorized instructions, and policy-gate everything else. Make instruction provenance your first verification checkpoint. Can you show the source document and the link to the buyer, seller, borrower, or lender? If not, you likely do not have a clean basis for release.

The failure mode is just as clear. When a commission request starts rerouting funds to personal expenses, business expenses, or a potentially unlicensed entity, you are no longer dealing with a normal split problem. You are in exception territory, and launch speed should give way to legal review.

This guide uses that California control point to separate product work from policy work. The goal is to avoid California-style CDA mistakes while building a closing model you can test market by market, with explicit limits on what can be automated and what must stay under human approval.

For a step-by-step walkthrough, see How Platform Operators Pay Creators Globally Across YouTube, Twitch, and Substack.

Define the legal control point at closing#

Treat disbursement authority as the control point, not a broker's payout preference. In California, the June 30, 2025 Joint Bulletin from the Department of Financial Protection and Innovation (DFPI) and the Department of Real Estate (DRE) warns that certain Commission Disbursement Authorization (CDA) patterns are legal risk, not just an operations edge case.

Start with the California warning, not broker preference#

The bulletin flags patterns where a broker uses a CDA to direct settlement or escrow funds toward the broker's personal or business expenses, or to a potentially unlicensed entity or individual. It says some of these practices may violate California Real Estate Law and California Escrow Law.

For closing design, that means a broker-entered payout request is not inherently valid because it matches a commission amount or appears at closing. The governing question is whether the escrow holder is authorized to disburse trust funds on that instruction.

Anchor authority to the transaction principal and written escrow instructions#

In this advisory context, principals are the buyer and seller or the borrower and lender, and brokers are not principals to an escrow transaction. Your approval logic should trace to principal-authorized written instructions.

Before approving a disbursement, verify:

- the written escrow instruction or written commission authorization

- the principal tied to that instruction

- the payee and payment purpose in the payout request

If that chain is missing, hold the payout.

Treat reroutes and unresolved payee status as legal exceptions#

Use California Escrow Law and California Real Estate Law as operating constraints. If commission proceeds are rerouted to unrelated personal expenses, business expenses, or a potentially unlicensed recipient, move the request out of automation and into legal review.

If payee or purpose no longer matches principal-authorized instructions, treat it as an exception. Also avoid declaring a recipient unlicensed without independent verification; mark the status unresolved, stop auto-disbursement, and require documented review.

Prepare the evidence pack before onboarding a market#

Treat the evidence pack as a launch gate, not documentation cleanup. If you cannot show who controls disbursement instructions, which document grants that authority, and how a commission split is treated locally, the market is not ready.

Collect the minimum artifact set#

For each market or corridor, require these three artifacts before onboarding:

| Artifact | Covers |

|---|---|

| Local law summary | Who may authorize escrow disbursements |

| Written commission authorization format | The format you will accept |

| Escrow instruction sequence | From principal instruction to final payee |

California makes the control point explicit. The June 30, 2025 DRE advisory states that escrow agents disburse trust funds only under the principals' written escrow instructions, and that brokers are not principals to an escrow transaction. A Commission Disbursement Authorization (CDA) can instruct escrow disbursement, including broker commission payment, but do not assume that format or label carries across markets.

Before launch review, make sure each artifact identifies the transaction principal, the authorizing document, and the destination payee.

Map roles before you design APIs or ops#

Do the role mapping before you design product or ops. Explicitly map settlement agent, escrow agent, real estate broker, and transaction principal so authority is assigned by role definition, not inferred from job title.

In the California bulletin context, settlement agent is also known as an escrow agent. Keep that equivalence explicit in policy and product records so broker, settlement, and principal actions do not collapse into one generic requester flow.

Label unresolved commission split rules honestly#

If local treatment of a commission split is unverified, mark the market as research incomplete. Do not treat common practice as an approved path, especially where instruction changes may need to come from a principal.

Use a hard rule: unknown authority means no automation, no ready status, and no launch date. Related: The Best CRM for a Real Estate Agent.

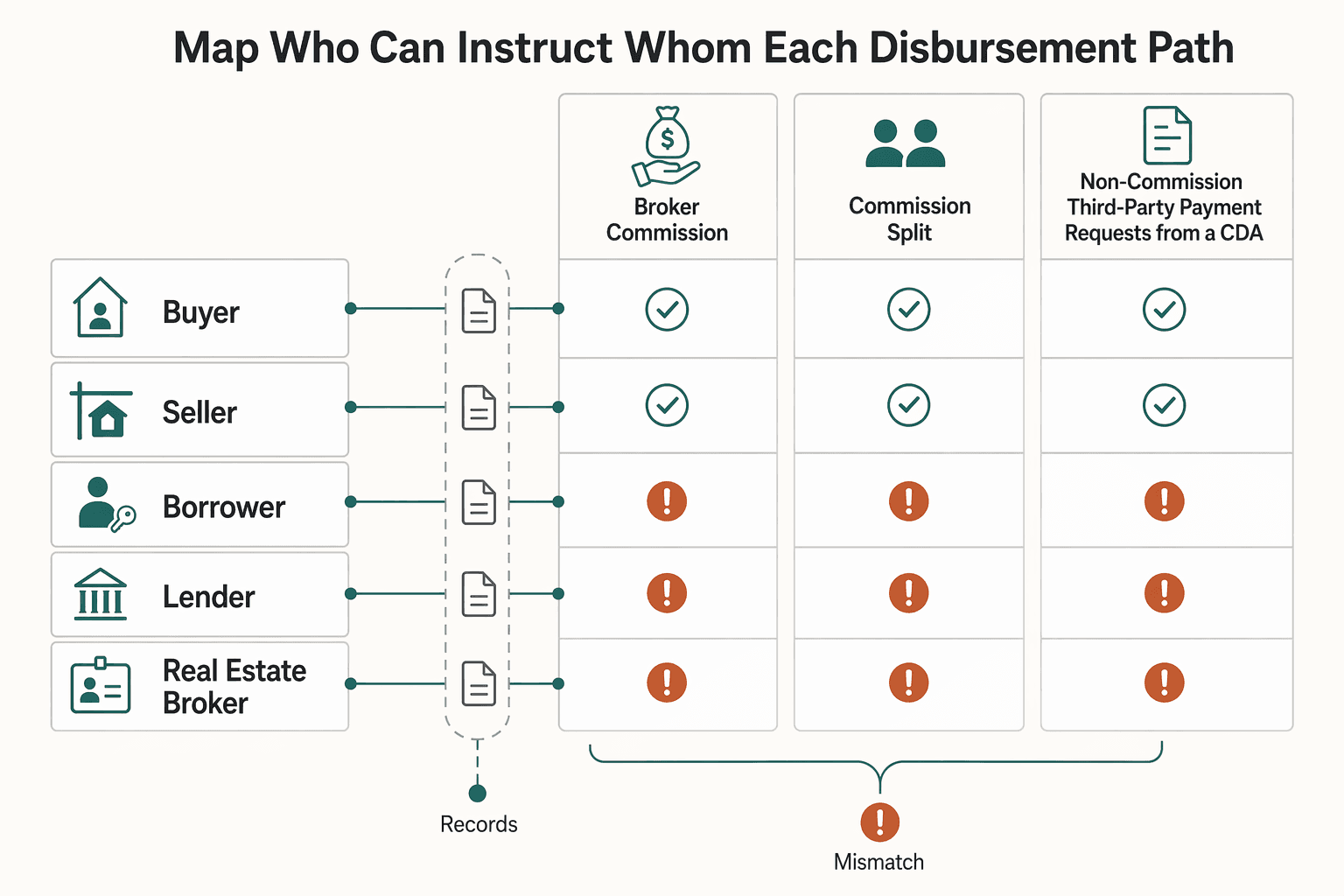

Map who can instruct whom in each disbursement path#

Build an authority matrix before you automate any closing disbursement path. In California, principals control escrow instructions, and a real estate broker does not hold principal instruction authority.

Use these actor rows: buyer, seller, borrower, lender, real estate broker, independent escrow company. Use these disbursement columns: broker commission, commission split, non-commission third-party payment requests from a CDA.

For each cell, record:

- the document basis: written commission authorization or signed instruction/amendment

- the control basis: initial instruction, amendment, or payee-only role

| Actor | Broker commission | Commission split | Non-commission third-party request from a CDA | Operator note |

|---|---|---|---|---|

| buyer | allowed with written commission authorization | allowed only with principal amendment | blocked as potential unlicensed entity risk | Principal to the transaction |

| seller | allowed with written commission authorization | allowed only with principal amendment | blocked as potential unlicensed entity risk | Principal to the transaction |

| borrower | allowed only with principal amendment | allowed only with principal amendment | blocked as potential unlicensed entity risk | Principal status is clear; specific commission path needs document confirmation |

| lender | allowed only with principal amendment | allowed only with principal amendment | blocked as potential unlicensed entity risk | Principal status is clear; specific commission path needs document confirmation |

| real estate broker | blocked, non-principal instruction source | blocked, non-principal instruction source | blocked as potential unlicensed entity risk | May be payee, not escrow-instruction owner |

| independent escrow company | blocked, executor not authorizer | blocked, executor not authorizer | blocked as potential unlicensed entity risk | Executes authorized instructions, does not self-authorize |

Keep these California cells conservative. If a commission split changes prior instructions, treat it as an amendment path and require signatures or initials from all prior signers.

If authority is ambiguous, do not automate. Route it to manual approval and add audit notes to the closing disbursement record with instruction source, signer set, payee request, and hold or approval rationale.

Hard stop: if a CDA-type request routes proceeds to broker personal or business expenses, or to an unlicensed entity or individual, block and escalate for legal review.

Before release, test one sample per matrix cell against real documents. Related: How to Invest in Real Estate as a Digital Nomad.

Decide what to automate and what to gate with human approval#

Set the line this way: automate only what is provable from signed documents, and send anything interpretive to human review. In California, that keeps the flow tied to transaction-principal authority instead of assumptions about intent.

Automate only deterministic checks#

Automate checks that can pass or fail without legal interpretation:

- Presence of principal-signed escrow instructions.

- Presence of written commission authorization where required.

- Exact match between the payout payload and the approved instruction package: payee, amount or split outcome, and transaction reference.

- Duplicate prevention with idempotency keys so retries do not create a second disbursement.

For broker commission and commission split payouts, release only when your system can name the supporting signed instruction set and approved payee path. If the payload differs from the signed record, fail closed and route to review.

Keep interpretive exceptions in a human lane#

Require human approval for exception classes such as late instruction changes, non-standard CDA language, and requests that resemble personal or business expense routing or payment to potentially unlicensed recipients. If an instruction change is requested, treat signer control strictly: changes need sign-off from all original instruction signers before release.

Apply one hold rule and preserve traceability#

Use one hold rule across the whole lane: if payer or payee intent cannot be traced to a transaction principal, hold the payout and require legal or ops sign-off.

Run compliance gates before release, keep provider retries idempotent, and preserve an audit trail from request to provider response to ledger posting. For a deeper look at the operational cost of delays, read Payout Support Ticket Cost Calculator: What Delayed Disbursements Really Cost Your Platform.

Implement the payout sequence with verification checkpoints#

Use a fixed sequence and fail closed on any mismatch: ingest the instruction package, verify authority, lock the approved commission split, execute the closing disbursement, then reconcile provider references to ledger and approval records.

| Step | When | Required check |

|---|---|---|

| Ingest instruction package | Pre-execution | Confirm the instruction source is complete and the signature chain is intact from the original instruction through any amendment |

| Lock approved commission split | Before handoff | Freeze the approved beneficiary list, amount, split outcome, and transaction reference |

| Execute closing disbursement | In flight | Re-compare provider payload routing to the approved escrow instruction objects before money moves |

| Reconcile provider references | Post-execution | Link disbursement reference, beneficiary, total paid, approval record, instruction source, and final ledger event |

Ingest the instruction package and verify authority#

Treat the signed escrow instruction as the controlling record, with any written commission authorization or CDA attached to the same file. Checkpoint 1 is pre-execution: confirm the instruction source is complete and the signature chain is intact from the original instruction through any amendment.

In California, disbursement must follow the principals' written escrow instructions, and instruction changes must be signed or initialed by all prior signers. If you cannot show the approved payee path, signer set, and amendment trail together, do not queue release.

Lock the approved commission split before handoff#

After authority verification, freeze the approved beneficiary list, amount, split outcome, and transaction reference that will drive execution. Allow updates only through a new principal-signed amendment that replaces the approved record; do not let release-tool edits change destination details after approval.

If the execution payload diverges from the approved record on beneficiary, amount, or split outcome, fail closed.

Execute the closing disbursement and re-check routing in flight#

Checkpoint 2 is in flight: re-compare provider payload routing to the approved escrow instruction objects before money moves. For timing, disburse at closing or as specifically agreed to in writing; if that condition is not met, hold the payment.

If ownership or destination becomes disputed, move to hold until principal parties resolve it in writing.

Reconcile provider references to ledger events after execution#

Checkpoint 3 is post-execution reconciliation: produce an export linking disbursement reference, beneficiary, total paid, approval record, instruction source, and final ledger event. Settlement records should show who in the end received payment and how much.

Retain this record set so you are audit-ready. In California, escrow records must be preserved for at least five years from close of escrow. If you cannot quickly pull the disbursement event, beneficiary, and approval chain together, the payout sequence is incomplete.

Handle failure modes and recovery without breaking escrow instructions#

Recovery should follow the same control standard as release: replay the exact approved instruction state, or stop and require a new principal-authorized instruction. That is the practical guardrail against duplicate payouts and disbursements that drift from escrow instructions.

| Scenario | Required action | Keep with the case |

|---|---|---|

| Rejected or timed-out payout after approval | Retry the original request with the same idempotency key and locked payload | Approval record ID, beneficiary, amount, transaction reference, and any disbursement reference for that idempotency key |

| Post-cutoff payee change request | Freeze the payout and open an amendment case | Current escrow instruction, any CDA on file, proposed payee path, and the new principal-authorized amendment |

| Suspected personal/business expense or unlicensed destination | Remove it from auto-disbursement, place the file on hold, and escalate | Requested payee, requester, related escrow instruction or CDA, flag reason, and escalation owner |

Replay rejected payouts with the same idempotent record#

When a payout is rejected or times out after approval, retry the original request with the same idempotency key and locked payload, not a new payout request. Payment APIs support this retry pattern so you can re-attempt execution without performing the action twice.

Before replay, confirm the approval record ID, beneficiary, amount, and transaction reference still match the frozen commission split record. Then verify whether a disbursement reference already exists for that idempotency key. The common failure mode is a manual "send again" action that later settles twice.

Route payee changes through a formal amendment#

A post-cutoff payee change is an amendment workflow, not a support edit. In California, trust funds are disbursed only under written escrow instructions from transaction principals, and the June 30, 2025 DFPI/DRE bulletin states brokers are not principals to the escrow transaction.

If a broker, team admin, or ops user requests a reroute, freeze the payout and open an amendment case. Keep the current escrow instruction, any CDA on file, the proposed payee path, and the new principal-authorized amendment together in the case file. Replace the locked payout record only after that amended instruction is approved. If the change affects borrower-facing closing terms, route it to settlement or legal review instead of assuming timing is unchanged.

Hold and escalate suspected unlicensed or non-commission destinations#

If a destination appears tied to personal or business expenses, or to an unlicensed entity, remove it from auto-disbursement immediately and place the file on hold. California regulators specifically warned about CDA use in those patterns.

Do not treat "broker approved" as sufficient. Record the requested payee, requester, related escrow instruction or CDA, flag reason, and escalation owner. Keep the file on documented hold until compliance or legal clears the destination in writing or the principals issue a clean amended instruction with the flagged payee removed.

Related reading: Opportunity Zone Real Estate: Verify Gain, Timing, and Tract Status Before You Invest.

Compare market expansion candidates before committing build#

Do not pick your next market on volume alone. Prioritize legal authority first: when binding instruction authority is unclear and commission-split exceptions are common, automation usually turns into manual case handling.

Score authority clarity before demand#

Start with one question: who can issue the binding instruction for closing disbursements? Score higher when authority is explicit, written, and tied to transaction principals. Oregon is a useful clarity benchmark: escrow agents must act only on dated written instructions of the principals.

Use a strict evidence check before you build. For each market, confirm the governing rule or guidance, the named closing actors, and how written commission authorization is handled in local practice. If controlling authority is still ambiguous, defer full automation.

Penalize fragmented closing-role models#

Treat role fragmentation as operational risk for standardization. U.S. closing models vary by region: many western states use title or escrow companies, while some eastern states use closing attorneys, and some states require attorney involvement for title transfer and exchange of funds.

Include non-U.S. role models in the same scoring logic. In the UK, legal transfer work is handled through conveyancing by legal professionals. In Western Australia, operating as a real estate settlement agent requires licensing, and settlement pathways are structured through two operating routes.

Use manual controls when exception risk exceeds legal certainty#

Use California as a clarity benchmark, not a universal template. DFPI/DRE guidance ties commission handling to principal authorization and warns that deviating from that instruction framework can violate Escrow Law.

If a candidate market does not offer comparable clarity, or local escrow-company practices vary too much for predictable handling, start with manual controls and postpone full productization until exception patterns are stable.

Final rollout checklist for founders and ops#

Use this as a go/no-go release gate: launch only the paths where instruction authority, documentation, and reconciliation are clear.

- Confirm the market evidence pack is complete, and unresolved legal questions are logged as open items, not handled ad hoc at close.

- Confirm the authority model is documented and approved for each payout path: who is the transaction principal, who is the escrow agent, and what role the broker has.

- Confirm California logic is implemented correctly where applicable: written instructions from principals control escrow disbursement; brokers are not principals; CDA requests that look like personal or business expense routing are routed to manual review.

- Confirm CDA handling is split into two lanes with explicit rules: auto-approve only when the request matches principal-authorized written instructions; send exceptions to review.

- Confirm reconciliation outputs tie each closing disbursement and commission split to instruction source, release decision, and ledger or journal record.

- Confirm escrow-account controls are operationally aligned for California-facing flows: books posted daily, reconciled at least weekly, month-end reconciliation completed by the 15th day after month-end, with monthly three-way reconciliation support.

- Confirm launch scope reflects current support: enable only corridors with clear authority or compliance mapping, and pause markets with unresolved instruction or role definitions.

Frequently Asked Questions

Can escrow pay agent commissions directly?

Yes. In the California fact pattern discussed here, an escrow agent can pay a broker commission when a seller or buyer authorizes that payment on a written commission authorization. The June 30, 2025 California DRE advisory is clear on the boundary: escrow trust funds must be disbursed only according to the written escrow instructions of the transaction principals. If a payout departs from those written instructions, the advisory says doing otherwise is a violation of Escrow Law.

Who counts as a transaction principal in escrow?

In the California advisory, the principals are the buyer and seller, or the borrower and lender. That distinction matters because instruction authority sits with those parties, not with everyone involved in the deal. If your ops team cannot point to which principal authorized the disbursement, treat the file as not ready for automation.

Are brokers principals in escrow instructions?

No. The advisory states that brokers are not principals to an escrow transaction. A broker may appear in the commission disbursement path through a Commission Disbursement Authorization, but that does not give the broker authority to unilaterally change escrow instructions or redirect funds outside principal-authorized instructions.

When is a CDA request high risk?

Treat a CDA as high risk when it routes earned commission to a broker's personal expense, business expense, or to someone who may have engaged in unlicensed activity. The advisory notes that independent escrow companies made these kinds of payments after a broker's CDA request, which is the failure mode you want to block. If a request looks like third-party expense routing instead of a clean commission payment, hold it for legal or compliance review.

What should a platform verify before scheduling a closing disbursement?

Check four things before release: instruction provenance, principal authorization, payee-role consistency, and audit-trace completeness. In practice, that means you should have the written commission authorization, the escrow instruction source, a clear signature chain, and any change signed or initialed by all persons who originally signed or initialed the instruction. If the payee in the payout payload does not match the approved instruction object, do not push the funds.

Can we apply the same flow globally?

No. Before you reuse the same flow elsewhere, validate the local legal model, the closing actors, and whether the same principal-authorized instruction standard actually applies.

Try a related tool

Sarah focuses on making content systems work: consistent structure, human tone, and practical checklists that keep quality high at scale.

Sources

- app.leg.wa.gov/WAC/default.aspxtrusted

- consumerfinance.gov/ask-cfpb/im-about-to-close-on-a-real-estate-...trusted

- consumerfinance.gov/ask-cfpb/who-should-i-expect-to-see-at-my-mo...trusted

- dfpi.ca.gov/regulated-industries/escrow-law/escrow-law-a...trusted

- dfpi.ca.gov/regulated-industries/escrow-law/general-defi...trusted

- docs.stripe.com/api/idempotent_requeststrusted

- dre.ca.gov/Licensees/Advisories/Advisory_2025_06_30_RE_...trusted

- dre.ca.gov/files/pdf/refbook/ref08.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Payout Support Ticket Cost Calculator for Delayed Disbursements

Delayed disbursement tickets are not always just a queue problem. In many teams, one customer contact triggers additional internal follow-up, so visible ticket counts can understate total operating effort.

The Best CRM for a Real Estate Agent

If you start with "what is the **best crm for real estate agents**," you will probably compare demos, feature grids, and pricing pages before you define what your business actually needs. That is backwards. A CRM is not just a contact database. It is where your leads, follow-ups, campaigns, client communication, and day-to-day visibility either stay organized or start slipping.

Home Office Deduction for Real Estate Agents: Qualify, Choose a Method, and Keep Records

If you file Schedule C, the key question is not whether this deduction looks aggressive. It is whether you can prove you qualify, choose the right method for that tax year, and support the claim with clean records.