Quick Answer

Start with a bounded pilot on a single paid endpoint in a single corridor, plus an alternate checkout path if the `HTTP 402 Payment Required` flow fails. In the machine payments protocol context, the safe approach is to treat the HTTP handshake as additive, then verify concrete checkpoints: challenge captured, authorization retry accepted, receipt checked, and final payment state reconciled. Scale only when fee assumptions, refund handling, and ops evidence hold up in live runs.

MPP matters because payment moves into the request flow#

The core shift is simple: payment can happen inside the same interaction that requests access. Instead of sending a user to a separate checkout, an agent, API client, or automated workflow can request a paid resource. The server responds with HTTP 402 Payment Required, the client authorizes payment, retries with payment proof in a header, and receives the resource plus a receipt in the same interaction cycle.

That changes where payment friction shows up. Older micropayment models often broke at human checkout. In agent flows, payment becomes a programmatic prerequisite for task completion. That is why MPP is an operator decision, not just a technical novelty.

What actually changed#

The 2026 material is more concrete: payment challenge, authorization, retry with proof, then resource and receipt. For founders, the practical implication is straightforward: payment moves into the request-response loop instead of sitting beside it as a separate user journey.

That opens new product paths, but it does not guarantee commercial viability. Autonomous transactions still operate within predefined controls, so launch readiness depends on what can be bought automatically and where human approval may still be required.

The operator question is narrower than the hype#

Before you commit roadmap or GTM spend, the useful question is not whether MPP exists. It is where your team can support it without creating more operational drag than value across your target verticals, countries, and payment setups.

What this article will help you decide#

This article stays focused on decisions teams can actually use, including:

- what the protocol is, and what it is not

- how one paid request cycle works in practice

- how to evaluate launch conditions by market and payment method

- which rollout gates finance, ops, and product should clear before expanding

The 2026 reality#

As of 2026, the core protocol behavior is no longer vague. March 18, 2026 is cited as a launch date. There are also secondary media claims that businesses are already live on MPP-style flows.

What remains unsettled is what operators are judged on in practice: adoption depth, benchmarked economics, and market-by-market constraints. Those still need direct validation in your own implementation and operating context.

The Machine Payments Protocol is an HTTP payment handshake, not a new rail#

The right way to read MPP is as an HTTP payment interaction pattern, not a payment network. The grounded core is the revival of HTTP 402 Payment Required as a machine-readable challenge-response flow for paid access over HTTP. That distinction helps separate what the protocol appears to cover from what your payments and finance operations still need to handle.

At a high level, the flow is simple. A client requests a resource, the server indicates payment is required, the client satisfies that requirement, and the request continues without a separate human checkout step.

What is actually standardized#

The strongest supported claim is the role of 402. Sources describe MPP as an open standard for machine-to-machine payments over HTTP. Secondary coverage ties the current network narrative to Stripe and Tempo or Tempo Labs, including the March 18, 2026 co-release date cited in the material.

Do not overread that into a fixed universal wire format. A required set of handshake headers or payload fields across implementations is not established here. If you are evaluating a vendor or planning a pilot, ask for the actual request and response trace.

What it is not#

MPP is not presented here as a card network, a bank transfer scheme, or a settlement rail. It is described as standardizing a paid HTTP challenge-response pattern. It is also not established here that MPP alone defines fund collection, settlement destination, refunds, or finance reporting outputs.

That is the operator risk. An open standard does not mean the hard operational layers are bundled. Merchant onboarding, payouts, refunds, settlement timing, tax treatment, reconciliation, and support workflows still depend on the payment method and provider stack underneath. One source frames Tempo as the execution layer for its implementation, but verify whether that applies to your specific deployment before treating it as mandatory.

A useful checkpoint is this: if a demo cannot show both the HTTP challenge flow and an underlying payment reference finance can reconcile, it is not yet a production-ready payments answer.

Keep protocol facts separate from vendor packaging#

The current network discussion is closely associated with Stripe, Tempo, Tempo Labs, and adjacent x402 coverage. That context is useful, but keep the core handshake separate from any single SDK, chain choice, or branding layer.

x402 is described as a separate open standard that embeds payment functionality into the web and is chain-agnostic. That does not make it automatically identical to MPP, and compatibility should be verified directly. For build-vs-buy decisions, request at least:

- one end-to-end paid request trace showing the

402challenge and successful retry - one underlying transaction or settlement reference your finance team can verify

- one explicit boundary between protocol behavior and provider-specific implementation

Keep one rule from this section: standardizing the request handshake may reduce agent checkout friction, but it does not remove the back-office work that makes payments operable.

For a closer look at how autonomous agents can initiate and settle transactions, see Machine-to-Machine Payments: How Platforms Will Process Autonomous Agent Transactions.

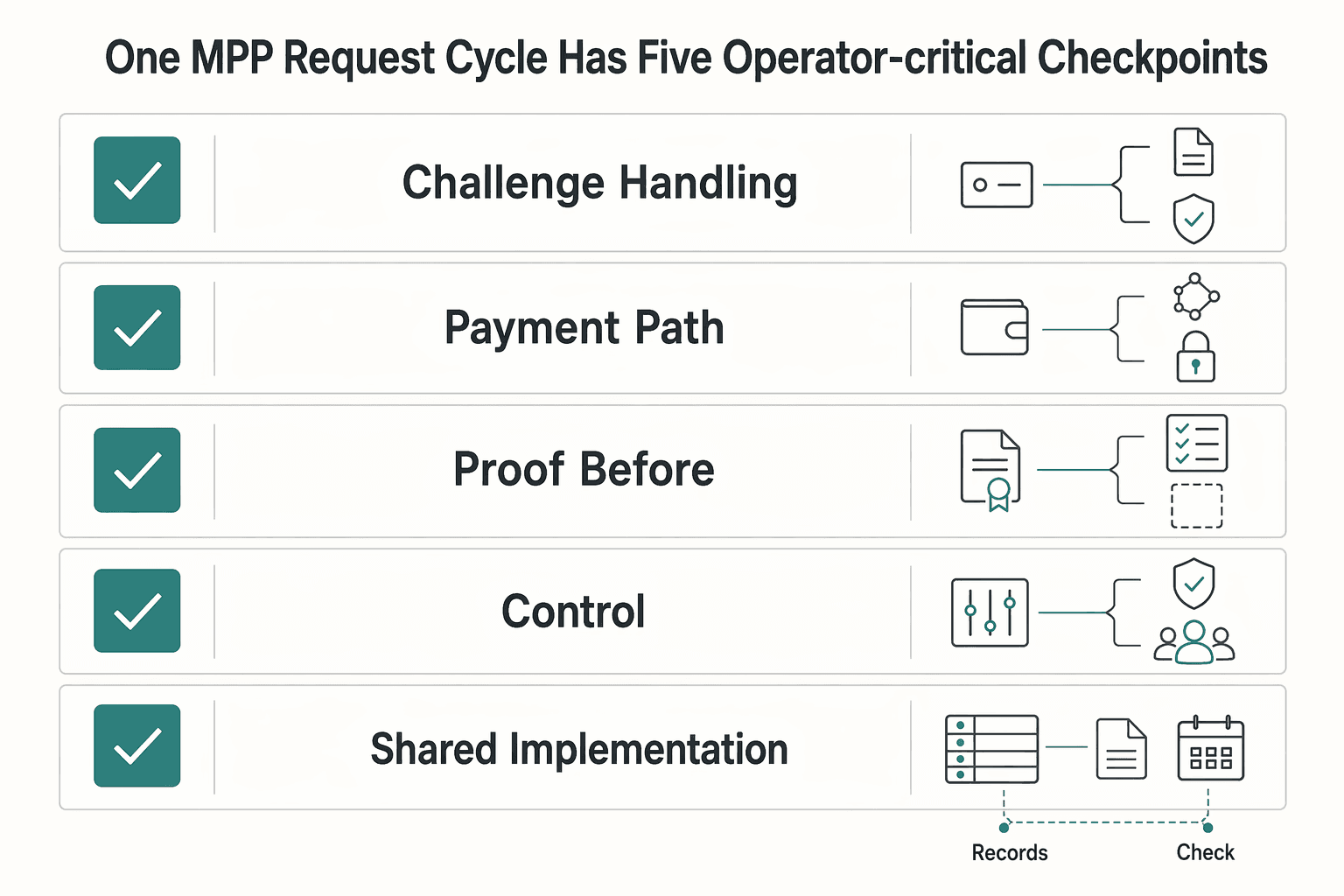

One MPP request cycle has five operator-critical checkpoints#

Treat the request cycle as an implementation checklist, not as a guaranteed universal wire sequence. In a payment-gated HTTP flow, HTTP 402 Payment Required can trigger the payment step, but the exact request and response artifacts depend on your stack.

| Checkpoint | What to define |

|---|---|

| Challenge handling | Capture the HTTP 402 Payment Required challenge data your system relies on and make it debuggable |

| Payment path selection | Define how the client pays for the gated resource in your environment and which provider path is allowed |

| Proof before fulfillment | Decide what payment evidence your system accepts before access is granted, and record it consistently |

| Replay and timeout control | Make retry behavior explicit so timeout-driven replays do not create ambiguous payment or delivery outcomes |

| Shared implementation ownership | Publish one validation and logging contract for all integrators so behavior stays consistent across clients |

In practice, make those five checkpoints explicit from the start and assign an owner to each one. That makes paid access easier to operate and easier to debug when client behavior diverges. In blockchain-linked payment contexts, failure impact can be severe because exploits may have immediate and substantial consequences.

For a deeper implementation template, see Machine Payments Protocol Implementation Guide for Platforms.

For a step-by-step walkthrough, see How Platform Operators Triage Late B2B Payments Before Market Entry.

The best first markets are the ones with clear usage metering and low human review#

Start where you can define the unit of value in software and model payment economics before launch. Gateway and program fees shape both user experience and margin, and their impact grows with volume.

| Launch criterion | What to look for first | Why it matters |

|---|---|---|

| Machine-detectable unit of value | A clear unit you can count consistently per transaction or payout cycle | Predictable metering makes pricing and margin modeling more reliable |

| Average ticket size and frequency | A realistic volume and ticket profile you can test against current fee schedules | Fee effects compound as transaction volume grows, so early economics can change quickly at scale |

| Stacked-fee exposure | Whether base processing fees and added program fees both apply | Some programs add fees on top of standard processing, for example Managed Payments adds 3.5% per successful transaction |

| Country and method variance | The exact country and method pricing pages you will operate under | Listed table fees can be superseded by local pricing pages, so assumptions can break by market |

| Payout model clarity | Clear expectations for when payouts are sent and how often | In Connect, payout events and monthly active account rules determine key billing moments |

A practical decision rule follows from the table. If you cannot define metering, fee stack, and payout behavior clearly enough to price and operate predictably, treat this as a second-phase monetization layer and validate with a smaller pilot first. Re-check current pricing before launch decisions because fee tables can change.

Country and payment-method fit will decide whether a pilot stays cheap#

If you need reach quickly, start with the payment method your team already knows how to reconcile, refund, and report on. Add a new rail only when it clearly improves demand or unit economics.

Keep the decision grounded in country and method specifics, not in a generic protocol narrative. Stripe can support 100+ payment methods, but effective availability and pricing still depend on method, buyer geography, program, and business country. In Managed Payments, supported buyer geos are listed per method, and country-specific payment-method pricing can supersede generic tables.

Build the market-entry sheet before you build the pilot#

Before you build anything, create a corridor table for the exact country pair and method you plan to launch first, and fill it with verifiable inputs from provider docs and live tests.

| Corridor and primary method | Payment-method availability | Settlement timing | Refund and dispute behavior | Tax/compliance gating | FX exposure | Payout coverage | Entity requirements |

|---|---|---|---|---|---|---|---|

| Home market, domestic cards | Confirm on your country pricing page and program docs | Verify with live test transactions | Verify your operational flow in production-like tests | Confirm required onboarding and documentation in provider docs | Confirm whether currency conversion is required for this corridor | Confirm where payouts are supported | Confirm account and entity setup requirements |

| Cross-border, international cards | Confirm buyer-country support | Verify with end-to-end tests | Verify dispute and refund handling before exposure | Confirm launch requirements in the target corridor | Model added FX and international-card cost | Confirm payout support for the destination | Confirm whether your current setup is eligible |

| Cross-border, local methods via Managed Payments | Use method-level supported buyer geos | Verify in live tests for the exact method | Verify method-specific handling in your workflow | Confirm program requirements before launch | Model conversion path and related fees | Confirm payout behavior under the program | Confirm program-level account requirements |

The cost risk is usually in stacked fees and corridor assumptions#

The biggest surprise usually comes from stacked fees and corridor assumptions. A domestic card transaction can start at 2.9% + 30¢, but cross-border exposure can add +1.5% for international cards and +1% when currency conversion is required. If you use Managed Payments, it adds 3.5% per successful transaction on top of standard Stripe processing fees.

| Fee layer | Amount | When noted |

|---|---|---|

| Domestic card transaction | 2.9% + 30¢ | Starting point mentioned for a domestic card transaction |

| International card exposure | +1.5% | Added for international cards |

| Currency conversion | +1% | Added when currency conversion is required |

| Managed Payments | 3.5% | Added per successful transaction on top of standard Stripe processing fees |

Model those layers before launch, because fee impact compounds with volume and pricing can change over time. The checkpoint is simple: validate the exact country and program pricing pages you will operate under, confirm any overrides, and run live corridor tests before treating a pilot budget as real.

New rail or new geography, not both#

For the first pilot, choose one corridor, one primary method, and one fallback path. Avoid combining a new geography and new payment mechanics in the same initial launch unless you are explicitly running a small discovery test.

That keeps support, finance, and launch decisions testable. Build approval on concrete evidence: exact fee inputs, method-level buyer-geo eligibility, and successful live transactions on the method and corridor you plan to ship. See The Future of Contractor Payments: AI Automation and Instant Settlement for related reading.

Charge and session solve different monetization problems#

Once you have one corridor and one method, the next decision is monetization shape. Use charge as one-off successful-transaction billing for a bounded unit of value, and use session for usage that runs across a time window or metered activity.

| Attribute | Charge | Session |

|---|---|---|

| Best fit | One-off successful-transaction billing for a bounded unit of value | Usage that runs across a time window or metered activity |

| When to use | When the deliverable is clear before payment | When usage is naturally continuous and reauthorizing each increment can add friction |

| Examples or description | One browser action, one dataset pull, one generated asset, one completed export, or one defined API bundle | One authorization followed by programmatic payments within defined limits |

| Rollout rule | Start with charge when the user can name the deliverable before payment | Move to session when usage is truly continuous and your limit enforcement is reliable |

| Auditability note | If early priorities are predictable billing and clear operational review, start with charge | Shift only after usage controls and transaction economics are proven end to end |

Use charge when the value is already bounded#

Use charge when the deliverable is clear before payment: one browser action, one dataset pull, one generated asset, one completed export, or one defined API bundle. The billing shape is straightforward because the fulfillment event is straightforward.

Session fits ongoing usage when limits are explicit#

Use session when usage is naturally continuous and reauthorizing each increment can add friction. A third-party MPP explainer describes session as one authorization followed by programmatic payments within defined limits.

Use this rollout rule:

- Start with charge when the user can name the deliverable before payment.

- Move to session when usage is truly continuous and your limit enforcement is reliable.

- Shift only after you verify that repeated one-off payments are the real friction.

Smooth UX can hide margin math#

A smoother UX is not always a better business choice. Monetization shape changes transaction shape, and transaction shape drives fee exposure. Confirm whether your implementation creates one successful transaction or many.

On standard Stripe pricing, domestic cards start at 2.9% + 30¢ per successful transaction, with +1.5% for international cards and +1% if currency conversion is required. If you use Managed Payments, the 3.5% fee is added on top of standard Stripe processing fees, and country-specific pricing pages can override generic tables. Stripe also notes that gateway fees can materially affect profitability, and that impact grows with volume.

Treat auditability as part of the choice#

Choose the model your team can verify consistently in production, not just the one that looks best in a demo. If your early priorities are predictable billing and clear operational review, start with charge and move to session after your usage controls and transaction economics are proven end to end.

MPP is additive to your existing merchant, settlement, and payout stack#

Treat MPP as a request-layer experiment until your downstream operations are verifiably reliable. Verify protocol-specific mechanics before treating it as a replacement for collections, settlement reporting, tax handling, treasury, or payouts.

The operational risk is familiar: if the request flow and back office are handled separately, you get disconnected experiences, inefficient operations, and harder support. That is why the safer approach is an integrated operating model, not a protocol-only rollout.

Before launch, set a hard verification checkpoint: each paid request should have a durable reference your ops and finance teams can match later.

That is also the careful way to position Gruv. Where supported and when enabled, Gruv can support teams running cross-border collections, conversions, and compliance-gated payouts with audit-ready records. The practical question is not whether MPP replaces your stack, but what infrastructure has to stay behind it so production operations remain supportable.

Failure modes appear in retries, receipts, refunds, and reconciliation#

Production failures often show up at the handoff between payment status and downstream actions, not only in the happy path. Treat retries, validation failures, refunds, and reconciliation as one control surface so a timeout or retry does not become a duplicate transaction.

Retries are normal behavior, not exceptions#

Retries are normal. Processor or gateway issues can surface as timeouts or declines, even when the root issue is provider-side. That means a repeated payment request may not reflect new purchase intent. You need an internal reference that ties each payment result to the related downstream action, and you should avoid blind retry loops when statuses do not agree.

After incidents or major changes, run end-to-end test transactions. This is a concrete checkpoint to verify that checkout and payment handling are functioning properly.

Validate payment artifacts before fulfillment#

Do not fulfill until your server can match payment artifacts to the active request context. When validation is unclear, give support and finance a visible review path that uses the same status language: approved, declined, or failed.

Refunds and post-payment adjustments can get expensive. Define how those cases are handled before rollout so provider status, internal records, and customer-facing outcomes stay aligned.

Reconciliation needs evidence, not just a dashboard status#

Dashboards help, but reconciliation needs evidence. Keep a compact reconciliation pack for each paid request so teams can rebuild what happened without raw-log forensics. At minimum, retain the payment result and transaction details used for tracking and reconciliation, plus related internal records and later adjustments such as refunds. This matters most after outages, where inaccurate refunds and duplicate transactions are more likely during cleanup.

Separate confirmed protocol facts from ecosystem claims before funding a launch#

Before you approve budget, separate what you have verified directly from what the network is claiming. That line is what keeps a credible demo from turning into a weak launch case.

| Bucket | What belongs there | What to do with it |

|---|---|---|

| Confirmed | Provider pricing pages and fee terms you reviewed yourself, including country-specific pages | Use in the go or no-go memo with links, date-checked assumptions, and known limits |

| Unproven | Claimed production volume, benchmarked success rates, dispute loss, support burden, cross-border settlement performance, or deployment depth | Keep out of revenue and margin assumptions until you run your own pilot |

| Internal proof | A fee model tied to your expected transaction mix and volume, with assumptions reviewed by finance and operations | Treat as the minimum package for launch approval |

Use a simple standard: if someone says a fee assumption is real, ask for the exact artifact that proves it. A current provider pricing page counts. A marketing claim does not.

Include current economics in the same evidence pack. Fee schedules are time-sensitive, and pricing pages can change. Recheck country-specific pricing before signoff, because those terms can supersede generic tables. Model the full fee stack you expect to carry in separate lines: 2.9% + 30¢ for domestic cards, +1.5% for international cards, +1% for currency conversion, 0.8% ACH Direct Debit with a $5.00 cap, 1.5% for stablecoin payments, and a 3.5% Managed Payments fee added on top of standard processing fees. If subscriptions are in scope, account for additional subscription charges as well.

If your memo does not include verified pricing artifacts and a volume-aware fee model, you still have a market claim, not a launch case.

A low-risk rollout starts with one corridor, one method, and a fallback path#

If you want pilot data you can interpret, start narrow: one paid surface, one buyer segment, one country or corridor, and one payment method, instrumented end to end before you expand. This is an operating choice, not a protocol requirement, and it makes it much easier to separate product issues from payment-method limits and market effects. That separation matters because cross-border compliance remains fragmented in 2026, and country-level AML, KYC, data residency, and reporting differences can raise cost and uncertainty.

Instrument the path before you widen it#

Treat the request lifecycle as the test surface. In an MPP-style flow, track the 402 challenge, the retry with Authorization: Payment ..., and the Payment-Receipt response. If you support pre-payment validation, use POST /api/machine/mpp/orders/validate to get quote and validation hints without payment side effects.

Track at least these checkpoints:

- challenge issued and parsed

- payment attempt created

- retry received with

Authorization Payment-Receiptverified and stored- fulfillment completed

- final payment status reconciled

One guardrail matters early: 202 plus Payment-Receipt does not always mean final completion. The flow can return 202 with a receipt while webhook finalization is still pending, so treat receipt and finalization as separate states.

Keep a real fallback path#

A pilot needs a real fallback. If a client cannot satisfy Authorization, or the paid retry fails after HTTP 402 Payment Required, route to an alternate payment path you already operate instead of ending the journey. The goal is to learn where the machine-native path works without stranding demand.

Capability constraints make this practical, not optional. One documented path supports Stripe Shared Payment Tokens (spt_...) for card and Link-capable clients, and does not accept raw card data, so some traffic may not be compatible with the machine path yet.

Define success like an operator, not a demo#

Define success in operational terms up front:

- paid-request success rate

- retry recovery rate

- gross margin after fees

- refund or dispute rate

Payment-Receiptverification success- support ticket volume

- reconciliation completion time

After the pilot, change one dimension at a time: add a new market or a new payment method, not both. That keeps failures diagnosable across compliance variation, SDK behavior, client capability, and economics.

Use this launch checklist for pilot scope:

- legal signoff for the selected country or corridor

- refund policy and support escalation path

- tax handling for the paid surface

- idempotency tests for retries and timeouts

- finance export mapping for provider and receipt references

- webhook alerts and exception handling ownership

- named owner for failed authorizations and receipt mismatches

- fixed post-launch review cadence, weekly to start

If you want deeper lifecycle implementation detail, read the Machine Payments Protocol Implementation Guide for Platforms.

Before expanding beyond the first corridor, use this operator checklist to pressure-test idempotency, fallback behavior, and reconciliation instrumentation in your stack: Gruv Docs.

Treat MPP as a gated expansion test, not a blanket roadmap bet#

Treat it as a gated expansion test, not a category bet. Approve spend only if one product surface, one market, and one payment path can show repeatable trust verification and operational evidence in a bounded pilot.

The decision is practical: can your team verify identity, reputation, and capabilities before money moves, and can it explain outcomes in a way finance and support will accept?

Start with a short scorecard#

Before approving product or GTM budget, score your top 2 to 3 verticals against hard checks. If a vertical fails these checks in a bounded pilot, keep it in discovery instead of turning it into roadmap commitment.

- Can the value unit be priced and fulfilled automatically? If it still depends on negotiation or manual completion, it is likely not the first pilot.

- Can trust be enforced before transactions? Define explicit trust thresholds so agents only transact when those thresholds are met.

- Can you produce auditable artifacts, not just a demo? Require verifiable records for what happened and why.

Pick one country and one method on purpose#

Run one country-and-method pilot tied to one product surface. Expanding geography and payment mechanics at the same time can make root-cause analysis harder when issues appear.

For agent-driven flows in this material, require the identity and verification model up front. Agents register an ERC-8004 identity linked to an operator wallet, transactions are real onchain transactions, and each transaction is independently viewable on a blockchain explorer. Define who handles human escalation before launch, since agent systems may still need operator coordination.

Demand an evidence pack before budget approval#

Require an evidence pack that can survive product, finance, and legal review. At minimum, include:

- one end-to-end trace from request to fulfillment

- the trust rule or threshold that allowed the transaction

- proof of real onchain transactions, with explorer visibility where relevant

- the agent-to-operator wallet mapping

agent.jsonandagent_log.jsonwhen compatibility checks require them- a written human escalation path for failures and edge cases

If a pilot can show a one-off success but not repeatable verification, clear exception handling, and concrete artifacts, treat that as a stop signal.

If you need the technical build details next, start with the Machine Payments Protocol Implementation Guide for Platforms. For broader context, read the machine-to-machine payments primer. If FX could shape your margins, pull in the multi-currency pricing guide before setting pricing. If you need to confirm whether collections, FX, or payouts can support your exact flow, talk to sales or request access before committing spend.

Related: How to Handle Multi-Currency Pricing for Your SaaS Product.

If your pilot is close to go or no-go, align product, finance, and compliance on real market constraints first. Then validate collections, FX, and payout coverage for your exact corridor and program: Talk to Gruv.

Frequently Asked Questions

What is the Machine Payments Protocol?

The Machine Payments Protocol, or MPP, is described as an open, internet-native standard for agent payments over HTTP. In practice, it defines a payment handshake for paid requests. Cited material also says MPP was co-authored by Tempo and Stripe.

How does MPP work in a single request cycle?

A client requests a resource, and the server responds with HTTP 402 Payment Required and a WWW-Authenticate: Payment challenge. The client completes the challenge and retries with Authorization: Payment. If verification succeeds, the server returns the resource and may include a Payment-Receipt header.

What payment methods can MPP support today?

The grounded examples are stablecoins and fiat methods like cards and buy now, pay later via Shared Payment Tokens, or SPTs. That supports more than one funding path in the cited implementation. You should not assume broader coverage without validating the methods you plan to launch.

What is the difference between `charge` and `session`?

The sources here describe session as an authorize-once primitive that allows programmatic payments within defined limits. They do not provide a full authoritative side-by-side definition of charge versus session. Treat that distinction as implementation-specific and verify semantics in the docs for your chosen stack.

Is MPP replacing existing payment stacks or sitting alongside them?

MPP is framed as additive to existing payment operations. It standardizes how paid HTTP requests are challenged and retried. There is no indication that MPP replaces settlement, tax, refunds, disputes, or payouts. Stripe’s framing is that existing human-payment infrastructure can also support agent payments.

Does MPP require Stripe, or can platforms support other methods too?

MPP is presented as an open standard, so the protocol concept is not limited to one provider. The concrete implementation details available so far are mostly Stripe-specific, including PaymentIntents API and SPT references. Evaluate provider choice based on what is proven in the stack you would actually ship.

What is still unknown before a platform should commit roadmap budget?

The key unknowns are operational: production success rates, dispute and refund behavior, support load, and country-by-country compliance outcomes are not established by these sources alone. Standards maturity is also early, with references to an IETF draft (draft-httpauth-payment-00) rather than a finalized standard. Before committing broader budget, require evidence from an end-to-end flow that covers challenge, authorization proof, receipt handling, and reconciliation.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ag-dashboard.acquisitiongateway.gov/system/files/ptai/2023-12/4.%20Solicitation%...trusted

- cms.gov/regulations-and-guidance/guidance/manuals/do...trusted

- cms.gov/Regulations-and-Guidance/Guidance/FACA/downl...trusted

- dot.ca.gov/-/media/dot-media/programs/design/documents/...trusted

- elibrary.imf.org/view/journals/063/2025/009/article-A001-en.xmltrusted

- epa.gov/sites/default/files/2013-09/documents/npdesi...trusted

- medpac.gov/wp-content/uploads/2025/03/Mar25_MedPAC_Repo...trusted

- ocw.mit.edu/courses/16-885j-aircraft-systems-engineering...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Machine Payments Protocol Implementation Guide for Platforms

Machine Payments Protocol can be piloted now, but it is not a plug-in billing toggle. In a machine payments protocol implementation, the main risk is usually not whether HTTP `402 Payment Required` exists. It is choosing the wrong payment pattern for your traffic and controls, then creating reconciliation gaps, payout surprises, or brittle edge behavior.

Choosing Payment Rails for Autonomous Agent Transactions

Autonomous agent payments are technically viable now, but a workable launch still depends on rail choice, market fit, and controls under real operating conditions. Stripe describes MPP, co-authored with Tempo, as an open, internet-native standard for agent payments, and Forrester describes March 18, 2026 as a turning point. In many pilots, the gap between a good pilot and a bad one is operational durability, not protocol novelty.

How to Handle Multi-Currency Pricing for Your SaaS Product

**Treat SaaS multi-currency pricing as a get-paid system, not a checkout feature.** If you only localize the price label, you miss the points where margin and cash timing break. As the CEO of a business-of-one, your job is to make "getting paid" boring and predictable, even when you sell globally. Start by linking presentment, settlement, and payout so your setup can absorb delays and FX movement as you expand.