Quick Answer

Start your ireland limited company setup in two tracks: complete CRO formation first, then handle Corporation Tax, VAT, and employer registrations as separate follow-up tasks. Keep a dated Known and Verify before filing list, freeze one final document pack, and submit from that single source. After incorporation, run weekly checks so legal records, contracts, invoices, and payment operations stay aligned.

Start Here So You Set Up Once and Avoid Rework#

Work in two tracks and keep them separate: complete CRO formation first, then handle post-setup registrations. That order reduces duplicate edits and missed follow-ups.

Before you begin, keep one dated checklist with Known and Verify before filing. If a threshold, timeline, or requirement is unclear, park it under Verify before filing and confirm it before you submit anything. Keep that list visible during every review so open items do not slip into filed documents.

- CRO formation first (company creation).

Set up your CRO account and complete formation details in one consistent pass, including officer appointments and share capital entries.

- Post-setup obligations second (operational compliance).

After incorporation, move to the post-setup registrations and compliance tasks that apply to your case. Treat these as separate from CRO filing and verify requirements before you submit.

- Decision rule for unclear items.

If a statutory timeline or threshold is uncertain, mark it Verify before filing and pause that task until you confirm it.

- Add a handoff log between track one and track two.

Record what was completed at incorporation, what still needs confirmation, and who owns each follow-up item. This keeps early compliance tasks clear when attention shifts from filing to operations and gives you a clean handoff: form the LTD once with aligned details, then execute follow-up tasks without guesswork.

Decide Whether an Irish Limited Company Is the Right Move for You#

Decide this before you draft filings. Use risk exposure, ownership plans, and your day-one admin capacity as the main filters, then confirm the legal position locally.

Use this as a practical filter, not a legal shortcut. Some grounding here uses non-Irish examples, so keep local thresholds, timelines, and filing duties in your Verify before filing list until confirmed.

- Compare risk exposure first.

Use the sole trader baseline: one owner with legal responsibility for business debts. If a dispute, refund issue, or unpaid invoice would create unacceptable personal exposure, treat that as a prompt to assess whether a Limited structure is warranted under local rules.

- Test ownership and client requirements.

If you expect to add a shareholder, split ownership, or contract through a distinct entity soon, flag that for local legal and tax review before deciding timing. If the work is still early-stage and lower-risk, deferring can be reasonable if you set a clear review point.

- Run a quick scenario contrast.

Case A: a solo consultant with mostly local, lower-risk work and simple operations. Case B: a contractor serving more counterparties and handling more compliance steps. If your current reality looks closer to Case B, prioritize the structure you can operate consistently and verify requirements locally.

- Set a dated review if you defer.

If you delay, set a firm review date with a qualified local adviser and revisit the same risk, ownership, and admin criteria with current facts. Add a short note on what would trigger an earlier review, such as a new client type, larger contract, or ownership change.

A workable rule: if risk exposure or ownership complexity is rising now, review incorporation now with local advice. If not, defer with a hard review date so the decision stays intentional.

Gather Your Pre-Registration Evidence Pack Before You Touch CRO#

Build your pre-registration evidence pack before you enter anything in CRO. This usually cuts avoidable rework across forms, drafts, and sign-off notes.

Public setup summaries are useful for planning, but they can conflict on fees and timing. For example, you may see a €50 fee mention alongside setup costs from 1,500 EUR, and timing estimates like 5-10 business days. Keep these items marked Verify before filing until confirmed against current CRO material.

- Assemble one draft formation folder.

Include the working documents and data you expect to use for filing, and keep them clearly labeled as drafts until verified. Keep one active version of each file so everyone reviews the same text.

- Prepare a name bank before availability checks.

List your preferred name plus backups so you can pivot quickly if the first choice is rejected.

- Create a

Known vs Verifysheet with CRO links.

Track fees, timing, and key constraints with a status (Known, Verify before filing, Blocked) and the CRO page to confirm against. Add a date note for each source so stale assumptions are easy to spot.

- Run one completeness review before any CRO entry.

Check that core fields and spellings match across all drafts. Start data entry only after high-risk fields are consistent and unresolved items are either verified or intentionally parked.

Use a simple naming pattern for drafts so the latest approved pack is obvious at a glance. If two versions of the same document exist, mark one as superseded immediately and keep the active version in one place.

Choose a Company Name That CRO Will Accept the First Time#

Choose for distinctiveness first, not personal preference. Name issues are an avoidable rejection risk if you test alternatives early and keep usable backups ready.

| Step | Action | Check |

|---|---|---|

| Build shortlist | Start with one preferred name and at least three alternatives you would actually use in contracts, invoices, and client communication | A rejection does not force a rushed rename |

| Remove similarity risk | Drop anything identical or too similar to existing registered names | If a name relies mostly on adding location or suffix words, replace it |

| Special approval check | Keep words that require special approval in a conditional list, not your primary filing list | Tag each option Clear, Needs approval, or Drop |

| Freeze filing names | Select one primary and two backups, then map them across your draft documents | A prepared backup list helps avoid document mismatches after rejection |

CRO can reject names that are identical or too similar to existing registered companies. Small edits may still fail that test, including adding words such as Ireland or Limited. Handle this before filing so you do not have to rename under time pressure.

- Step 1: Build a real shortlist, not one favorite.

Start with one preferred name and at least three alternatives you would actually use in contracts, invoices, and client communication. Expected outcome: a rejection does not force a rushed rename.

- Step 2: Remove high-risk similarity early.

Check each option against existing registered names and drop anything identical or too similar. Verification point: if a name relies mostly on adding location or suffix words, replace it.

- Step 3: Separate names that need special approval.

Some words require special approval before use. Keep those options in a conditional list, not your primary filing list. Verification point: tag each option Clear, Needs approval, or Drop.

- Step 4: Freeze one primary name plus two backups.

Select one primary and two backups, then map them across your draft documents so any swap stays clean. Failure mode and recovery: ad hoc renaming after rejection creates document mismatches; a prepared backup list helps avoid that.

Before you submit, confirm your primary and backup names appear in every draft that would be affected by a swap. That small check can save a full round of edits under deadline pressure.

Lock In Your Structure and Officers Before Filing#

Lock your structure, officers, and address details before you open filing forms. Entering fields without one approved reference is where preventable mismatches start.

A company is a separate legal entity, so your filing data should sit in one role-and-address matrix. Confirm your intended company type, then list each shareholder and director, and any other officer details you plan to file, exactly as you intend to submit.

- Confirm structure and filing data.

Match company type, names, and ownership entries across draft documents and the Form A1 data you plan to submit via CORE.

- Assign officers and handle role overlap.

If one person holds multiple roles, document backup coverage for signatures, records, and continuity. Keep the EEA-resident director or bond item marked Verify before filing until confirmed.

- Standardize registered address details.

Secure the registered office, then use one canonical registered-office address block everywhere so wording stays identical.

- Run one pre-submit check before CRO submission.

Approve the final matrix for company type, officers, shareholders, and address fields, then submit. Keep open verification items dated, including first annual return timing, until confirmed.

Add a final sign-off timestamp and owner initials on the matrix before filing. If any field changes later, update the same matrix first so every correction starts from one authoritative source.

Draft Core Formation Documents Without Guessing#

Draft formation documents from confirmed decisions, not template habit. If the formation text does not match your real ownership and management plan, you are setting up avoidable corrections later.

The Company Constitution is not filler text. It sets out the company rules and regulations, so it should reflect how the company will be owned and managed.

- Draft from confirmed decisions, not template convenience.

Use the structure and officer decisions you already locked in, then confirm the same names and role details across every document.

- Reconcile repeated ownership fields wherever they appear.

If drafts include repeated ownership or role headings, treat them as consistency checks and keep entries aligned across drafts and internal records.

- Align the filing pack before upload.

Formation requires Form A1 to the CRO with the Constitution and the appropriate fee, so confirm repeated fields first. Keep registered office wording identical because official post and legal notices are sent there. Keep minimum role checks visible: at least one shareholder and at least one director.

- Freeze one final version-controlled pack for sign-off.

Use one dated ready-to-file set for all signatories, with no parallel copies. If you spot placeholder names, old address text, or conflicting entries, pause and redraft from the single source file.

A short change log helps here. Note what changed, who approved it, and when it was updated so final sign-off is based on facts, not memory.

File with CRO in the Right Order and Track Approval#

File in a fixed internal order and log every action. Use this as an internal control checklist, not an official CRO filing sequence. The point is simple: submitted form fields should stay aligned with your approved Constitution and filing data from start to finish.

Before submission, confirm one final Constitution file, one approved officer list, and one approved Registered Office wording. Private-company formation is framed by the Companies Act 2014, and CRO provides company-registration guidance, so keep your records consistent as you file.

- Enter core company data from the locked pack.

Copy legal name, Registered Office text, and share details directly from final documents, then run a readback check.

- Confirm officer details line by line.

Enter director and company secretary details exactly as approved, and check each field against your master filing sheet.

- Upload only the final Company Constitution file.

Use the dated sign-off version and verify file name and version before submission.

- Capture submission details immediately.

Record timestamp, responsible person, receipt or reference details, and filing state in one submission log entry.

- Track CRO status and log follow-up requests.

For each request, record owner, due date, action taken, and which field or document changed.

If CRO asks for clarification, respond from the same master filing sheet and update that sheet before replying. That prevents quick fixes from creating a second, conflicting set of records.

One common risk is a mismatch between the filed form and the Constitution. If you find one, pause, correct the master pack, and log the updated submission in the same record.

Handle Non-Resident and Cross-Border Founder Constraints Early#

Treat founder-status uncertainty as a pre-submission gate, not a cleanup task. If residency and other founder-status questions stay unresolved, filings can move forward while eligibility risk stays hidden.

The material for this section is US state personal-income-tax residency guidance, where status is treated as fact-specific. Use it only as a reminder that these determinations can be case-specific, not as Irish incorporation rules.

- Separate filing data from founder-status checks.

Run one track for filing entries and one for founder-status verification. Every open item needs an owner and next review date.

- Use routing labels, not legal conclusions.

Mark each founder as straightforward or cross-border for triage only. The goal is early risk visibility, not legal conclusions from summaries.

- Apply a strict evidence rule.

If a founder-status conclusion is not confirmed against official Irish guidance, mark it Verify before filing and keep it open.

- Use a clear pause or proceed rule.

Proceed only when founder-status items are clear and documented. If any item is unclear or advice conflicts, pause submission and verify.

- Log every hold and restart in one record.

When you pause, record the trigger and missing evidence. When you restart, record what changed and why filing can continue.

Use a brief go-or-hold note before each filing milestone so everyone knows whether unresolved founder-status items are blocking progress. That note helps prevent accidental submission when key checks are still open.

Red flag: copying residency language from US tax pages into Irish incorporation decisions. Practical rule: if founder status is uncertain, pause, verify, then proceed.

Set Up Tax and Employer Registrations After Incorporation#

CRO approval starts compliance; it does not finish it. After incorporation, treat Corporation Tax, VAT where applicable, and payroll setup as separate tasks with clear ownership and evidence.

| Track | When to act | What to track |

|---|---|---|

| Corporation Tax | After incorporation | Track status from Not started to Submitted to Confirmed, with timestamped evidence at each step |

| VAT | Where applicable | Keep VAT as a distinct decision with its own evidence trail; if applicability is unclear, mark it Verify before filing and set a review date |

| Employer registration | As soon as hiring becomes real | Tie employee start dates to confirmed employer-registration status |

| Weekly record-quality check | Weekly in year one | Log open gaps, owners, target resolution dates, and blockers |

| Gap recovery sprint | If you find a gap | Submit missing registrations that week and update calendar entries and evidence links |

A company is a separate legal entity, and incorporation alone does not cover tax or employer readiness. Delays here create risk even when company registration is complete.

- Capture incorporation evidence immediately after CRO approval.

Store incorporation confirmation and related filing records in one core folder. Add tax and payroll actions to a first-year calendar with a named owner for each item.

- Register for Corporation Tax as its own action.

Do not assume this happened during incorporation. Track status from Not started to Submitted to Confirmed, with timestamped evidence at each step.

- Assess VAT separately and register when required.

Keep VAT as a distinct decision with its own evidence trail. If applicability is unclear, mark it Verify before filing and set a review date.

- Start employer registration as soon as hiring becomes real.

Company setup can allow legal hiring in Ireland, but payroll readiness still needs explicit setup. Tie employee start dates to confirmed employer-registration status.

- Run a weekly record-quality check in year one.

Late filings, missing registrations, and weak records can lead to penalties and loss of audit exemption. Log open gaps, owners, and target resolution dates every week. Include a short note on blockers so escalation decisions happen early.

- If you find a gap, run a same-week registration sprint.

One failure mode is assuming CRO completion covered tax and payroll automatically. Recover by submitting missing registrations that week and updating calendar entries and evidence links.

Where teams get stuck is ownership drift. Keep one named owner per registration task until confirmation is received, then archive proof in the same place used for weekly checks.

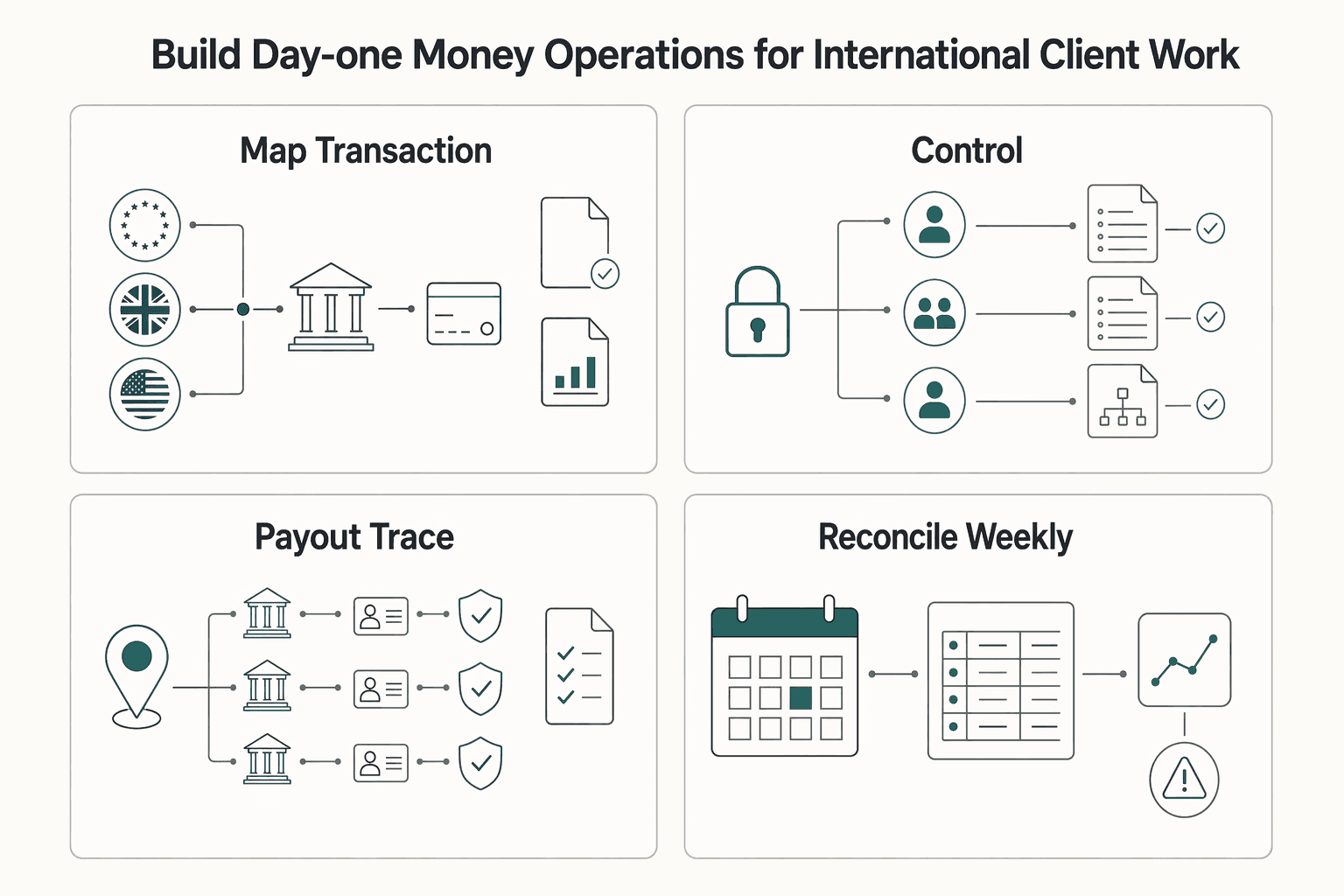

Build Day-One Money Operations for International Client Work#

Before payment volume grows, define one documented money path per region. Once EU, UK, and United States client payments arrive in different currencies, weak process design quickly turns into reconciliation risk.

Create one finance evidence pack from day one: incorporation records, company identity details used on invoices, collection account terms, payout approval rules, and monthly reconciliation logs. Keep each item tied to one owner so unresolved payment issues do not sit between teams.

- Step 1: Map the transaction path by region

For each region, document invoice currency, receiving account, conversion point, and final payout destination. Keep one clearly defined contracting and billing party for new work, for example, your Irish entity if that is your operating setup. In Ireland, a local legal entity can support legal hiring in-country and may offer more direct operational and compliance control than relying on an EOR model. Verification point: every new client has one traceable path from invoice issue to settled cash.

- Step 2: Standardize invoicing and collection controls

Use one invoice structure across regions so reconciliation does not depend on memory. Keep payment terms, currency, and payer identifiers aligned with ledger naming rules, and assign one owner for weekly collections follow-up. If income is classified internally, separate active trading and non-trading lines, then verify tax treatment with current Irish Revenue guidance before filing decisions. Verification point: no invoice enters collection without a matching ledger record and named owner.

- Step 3: Gate payouts with traceable, idempotent rules

For teams using Gruv where supported, set payout gates before release: invoice matched, funds received, conversion recorded, approval logged, and destination account confirmed. Use a unique payout key so retries do not create duplicate payments. Keep a timestamped decision trail for each payout so finance reviews are easy to reconstruct. Failure mode to watch: manual retries without unique keys, followed by duplicate payouts at month end.

- Step 4: Reconcile weekly and enforce a market-expansion rule

Run a weekly close for open invoices, settled payments, conversion differences, and unreconciled lines. If unresolved matches are already painful, clean the ledger before you add new markets. If you use a cross-border business account that advertises integrations with QuickBooks, Xero, or Sage, treat that as an efficiency aid, not a compliance guarantee. Keep jurisdiction scope clear: GOV.UK Practice Guide 78 applies to England and Wales land registration, not Irish operating controls. If expansion is still on the table, review jurisdiction implications in How to Choose a Jurisdiction for Your European Subsidiary.

Keep a short monthly exception log for payments that needed manual correction. Patterns in that log usually show whether your controls are working or whether one region needs tighter invoice and payout checks. If you want a deeper dive, read A Guide to Impact Investing for Freelancers.

Avoid the Most Common Setup Mistakes and Recover Fast#

Fast recovery usually comes down to one habit: lock critical inputs before filing, then clear every open item with a named owner and evidence. Treat this as a prevention and recovery checklist, not just a warning list.

A limited company is legally separate from its owners, and owners are responsible for debts only up to their financial investment. In practice, risk rises when filing records, tax setup, contracts, and payment operations stop matching.

- Step 1: Freeze filing inputs before registry submission

Set a pre-submission checklist for registered address, officer roles, and signing responsibilities. Require explicit final confirmation from each owner before filing. Verification point: the same address and officer details appear across all filing documents and internal records.

- Step 2: Make governing documents match real operations

Avoid copy-paste governing text. Align your key company documents with actual activities, share structure, and decision rights before submission, then re-approve if your model changes. Failure mode: generic wording conflicts with day-to-day operations and creates avoidable cleanup.

- Step 3: Keep Irish tax setup separate from UK Self Assessment rules

Track Irish tax setup as separate post-incorporation tracks with a named owner, status, and evidence, and verify local requirements through official Irish guidance. Do not reuse UK Self Assessment thresholds or deadlines as Irish rules. UK examples still help as warning signals: some taxpayers must notify HMRC by 5 October 2025 for the previous tax year, UK sole traders must register for Self Assessment if they earn more than £1,000 in a tax year, and filing without reactivating an existing Self Assessment account may delay a return.

- Step 4: Escalate founder-permission uncertainty before trading

If founder-permission or eligibility status is unclear, pause launch steps and verify through official channels before first invoice issuance. If status is clear, record confirmation in your evidence pack and proceed.

These mistakes are usually recoverable when you catch them early. The bigger risk is continuing sales and payments while filing, tax, or permission issues stay unowned. If expansion is next, pressure-test market choices in How to Choose a Jurisdiction for Your European Subsidiary.

Run a 30-Day Post-Incorporation Compliance Check#

Treat the first month as a structured review cycle, not a one-time cleanup. Confirm records weekly, fix mismatches quickly, and keep evidence in one place.

| Week | Focus | Evidence or check |

|---|---|---|

| Week 1 | Legal records and CRO documents | Store final incorporation records, Director and Company Secretary details, and CRO documents; record the Annual Return Deadline (ARD) and where it was verified |

| Week 2 | Corporation Tax and VAT status | Save submission receipts, confirmations, and next actions in the same folder |

| Week 3 | Contracts, invoicing, and payments | Correct mismatched names, addresses, or account details before issuing new invoices; keep one file linking contract, invoice, payment proof, and bookkeeping entry |

| Week 4 | Known vs Verify refresh | Assign an owner, source to confirm, and target date for every Verify item |

Set up one compliance folder before day one with clear owners and due dates for each item: entity records, tax registrations, commercial documents, and open questions.

- Step 1: Confirm legal records and CRO documents (Week 1).

Store final incorporation records, Director and Company Secretary details, and CRO documents in an accessible shared location. Check that company name, registered address, and officer details match across files. Record your Annual Return Deadline (ARD) and where it was verified, including CORE Company Search if used. Note any discrepancy immediately and assign an owner before week-end.

- Step 2: Validate Corporation Tax and VAT status evidence (Week 2).

Track Corporation Tax and VAT as separate tracks with clear status and evidence for each. Save submission receipts, confirmations, and next actions in the same folder. Keep this jurisdiction-specific and avoid carrying assumptions from other tax systems.

- Step 3: Reconcile contracts, invoicing, and payments with legal identity (Week 3).

Review active contracts, invoice details, and payment operations against your company legal identity. Correct mismatched names, addresses, or account details before issuing new invoices. Keep one complete file linking contract, invoice, payment proof, and bookkeeping entry.

- Step 4: Refresh Known vs Verify items and lock next actions (Week 4).

List unresolved statutory items in Ireland under Known and Verify. Assign an owner, source to confirm, and target date for every Verify item. Keep annual compliance in view: Irish companies are described as needing an Annual Return and financial statements each year, including when not yet trading, filed to the CRO by the Annual Return Deadline (ARD). Treat compliance as continuous operational work, not an annual-only task.

At day 30, run one short close-out review: what is complete, what is pending, and what needs external confirmation. That turns month-one cleanup into a repeatable cadence for the rest of year one.

Copy-Paste Setup Checklist and Next Step#

Use this checklist to keep your records aligned from formation through operations. Consistency across legal, tax, and payment records is what usually prevents avoidable rework.

- Choose entity and owners first.

If you are forming an Irish LTD, document who is the Director, Company Secretary, and Shareholder. Before filing, confirm at least one director and at least one issued share, then verify current CRO requirements.

- Prepare one final filing pack.

Lock the final company name and share details so the same details appear everywhere. If you use Limited/Ltd or Teoranta/Teo, keep that format identical across documents. If the name includes sensitive terms like Bank, confirm permission requirements before submission and verify with CRO guidance.

- File once and track every CRO follow-up.

Submit through the Companies Registration Office (CRO) only after a final field-by-field consistency check. Save receipts, assign one owner for follow-ups, and log each action with date and evidence.

- Activate operations after incorporation.

Open separate tracked tasks for tax actions, then put invoicing and payment controls in place under the company legal identity. If timing, thresholds, or requirements are unclear, keep them on a verify list until confirmed with current Irish guidance.

- Run an early Ireland review before scaling.

Review legal records, tax actions, contracts, invoices, and payment logs for alignment, then close open items with dated proof. If key verification items are still open, finish cleanup before expanding client volume.

Frequently Asked Questions

What are the exact steps to complete an ireland limited company setup from start to CRO approval?

This evidence pack does not provide exact Irish filing steps, fees, forms, or processing times. Treat this as unconfirmed until you verify current requirements in official Irish guidance.

What must be ready before filing with the Companies Registration Office (CRO)?

This evidence pack does not specify CRO pre-filing requirements. Confirm the required documents and checks directly from current Irish CRO guidance before submitting.

What changes immediately after incorporation for Corporation Tax, VAT, and employee obligations?

This evidence pack does not establish Irish Corporation Tax, VAT, or employee-obligation thresholds, deadlines, or filing steps. Verify each requirement with current Irish guidance before acting.

Can non-EU, non-EEA, non-UK, and non-Swiss founders set up a company in Ireland?

This evidence pack does not establish eligibility rules for those founder categories in Ireland. Confirm founder-permission requirements with official Irish guidance before trading or signing contracts. If eligibility is unclear, pause and escalate early.

Should I set up the company myself or use a formation service?

This evidence pack does not provide evidence to recommend DIY setup versus a formation service for Ireland. Decide only after you verify current Irish requirements and your capacity to manage compliance follow-up.

What are the most common filing mistakes, and how do I recover without major delay?

A common mistake is mixing UK HMRC Self Assessment rules into Irish tasks. This pack includes UK examples such as notifying HMRC by 5 October 2025 in some cases, possible penalties for late notice, first-time registration before online filing, online filing not covering partnership returns, and a £1,000 sole-trader trigger, but those are not Irish CRO rules. Recover by separating UK and Ireland checklists, assigning owners, and re-validating each open item with the right authority.

Try a related tool

A former tech COO turned 'Business-of-One' consultant, Marcus is obsessed with efficiency. He writes about optimizing workflows, leveraging technology, and building resilient systems for solo entrepreneurs.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

- ato.gov.au/businesses-and-organisations/international-t...trusted

- ato.gov.au/businesses-and-organisations/international-t...trusted

- tax.ny.gov/pit/file/nonresident-faqs.htmtrusted

- cro.ie/Registration/Companyexternal

- cro.ie/Registration/Company/Incidental-Obligations/...external

- revenue.ie/en/starting-a-business/starting-a-business/r...external

- youresidency.com/business/ireland-limited-company-setupexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

How to Choose a Jurisdiction for Your European Subsidiary

Pick your European subsidiary jurisdiction as an operating decision first, then map VAT administration around that choice. The aim is simple: one primary incorporation country and one fallback you can activate without restarting discovery. If your fallback depends on Estonia setup speed, map banking steps in [How to Open a Business Bank Account for Your Estonian Company](/blog/estonian-company-bank-account).

A Guide to Impact Investing for Freelancers

**Protect your cash buffer and payment reliability first, then build a values-based investing plan you can sustain through slow months and late invoices.** You're the CEO of a business-of-one, so your investing system has to respect operations first and ideals second.