Quick Answer

Start with a fee-baseline decision, not a platform preference: move only if current Stripe Billing economics and operating drag no longer support the next 12 months of pricing and packaging changes. In this case, the team compared domestic card, international card, FX, Connect, and Managed Payments exposure, then required a frozen data snapshot and object-level mapping before cutover. They reduced launch risk by validating via API, running parallel checks, and promoting cohorts only after invoice and renewal parity held.

Why the Team Moved Off Stripe Billing#

In a billing-migration scenario, a SaaS team moves core billing from Stripe Billing to Gruv when monetization options start to outrun billing control. The pressure is usually concrete. Product wants more pricing freedom, founders want growth without more margin drag, RevOps wants cleaner operations, and finance still needs invoices, renewals, and tax treatment to stay defensible.

That is the real tension in a move like this. Moving quickly can open up packaging changes, usage pricing, or new payout flows. But speed gets expensive if invoice accuracy drops or reconciliation gets harder right after cutover. A migration only helps if it expands what you can sell without making finance trust the numbers less.

Before you start#

Use this guide as an execution note, not a feature tour. It does four things: shows you how to decide whether a move is worth it, how to execute it, which checkpoints catch bad cutovers early, and which post-launch signals show whether the new setup is actually better.

The practical stance is simple. If your current setup is blocking pricing and packaging decisions that matter in the next 12 months, migration deserves serious attention. If not, the burden of proof is higher. Billing changes create hidden work in data cleanup, contract handling, invoice parity testing, and finance review even when the end state is stronger.

A good early checkpoint is ownership. If product can change plans without finance agreeing on how those changes land on invoices, revenue timing, or tax handling, pause before you scope the move. That is a common failure mode. It can show up later as invoice disputes, renewal exceptions, and month-end close friction.

Scope limits that matter early#

Scope gets expensive to change once build work starts, so set the boundaries before anyone treats the design as fixed. Controls and module availability can vary by market, program, and compliance setup, so do not assume a design that works in one region carries over unchanged to another. The EU is the clearest example.

For EU cross-border B2C activity, VAT rules changed on 1 July 2021. The previous distance-sales thresholds were replaced by a new EU-wide threshold of EUR 10 000. The One Stop Shop, or OSS, lets a taxable person register in one single Member State, the Member State of identification, for relevant VAT declaration and payment. That matters in migration planning because invoice logic, tax reporting, and record retention may need to line up before you move production traffic.

If you already sell into the EU, verify three things before treating scope as fixed:

- whether you use OSS today, and if so, your Member State of identification

- whether your cross-border B2C sales are near or above the EUR 10 000 threshold

- whether you have the records needed for registration, VAT declaration and payment, record keeping, and possible audits

For more complex cross-border VAT treatment, taxable persons can request a VAT Cross-border Ruling in participating EU countries. That is not a reason to delay every migration, but it is a clear warning against rushing scope when tax treatment is still unsettled.

Related: A Guide to Usage-Based Pricing for SaaS.

Decide if moving from Stripe Billing to Gruv is economically justified#

Move for economics, not aesthetics: migrate when billing is constraining pricing, pressuring margin, adding reconciliation drag, or making payout costs material.

| Fee item | Amount | Context |

|---|---|---|

| Domestic cards | 2.9% + 30¢ | Stripe standard pricing lists this for each successful domestic card transaction |

| International cards | 1.5% | Additional charge |

| Currency conversion | 1% | Additional charge |

| Manually entered cards | 0.5% | Additional charge |

| Managed Payments | 3.5% | In addition to standard processing fees; subscription payments can have additional charges |

- Price your current Stripe setup before comparing platforms.

Use your exact Stripe configuration, because pricing varies by product and model. Stripe standard pricing is pay-as-you-go with no setup, monthly, or hidden fees, with domestic cards listed at 2.9% + 30¢ per successful transaction. Additional charges can stack, including 1.5% for international cards, 1% for currency conversion, and 0.5% for manually entered cards. If you use Managed Payments, the 3.5% fee is in addition to standard processing fees, and subscription payments can have additional charges. Verification: review a recent month and tag fees by standard processing, Managed Payments, Connect, international card, and FX components.

- Use a hard trigger for the next 12 months of monetization changes.

List what product actually needs to ship in the next year, then test whether your current billing architecture supports it without finance-heavy workarounds. If it does, defer migration. If pricing experimentation is blocked by billing architecture, migration is economically justified.

- Separate strategy from migration vanity.

"Vendor consolidation" alone is not a business case. Define explicit outcomes: lower fee exposure, clearer Merchant of Record posture, or simpler cross-border Payouts. For Stripe Connect, confirm your pricing model before comparing:

- If you handle pricing, Stripe lists $2 per monthly active account and 0.25% + 25¢ per payout sent.

- If Stripe handles pricing, Stripe says you do not incur additional account, payout volume, tax-reporting, or per-payout fees.

If you cannot state which model applies, you are not ready to compare economics.

- Set decision rights before launch planning.

Treat unclear ownership as a no-go checkpoint. Finance and product should agree in writing on who approves pricing changes, fee assumptions, payout logic, and reconciliation sign-off before detailed planning begins.

For a step-by-step walkthrough, see How to Compare SaaS Billing Benchmarks Before Expansion.

Assemble prerequisites and the migration evidence pack#

Build one migration evidence pack before engineering starts so finance, RevOps, and engineering are validating the same baseline.

- Freeze and export the Stripe Billing baseline.

Create a dated snapshot of your product catalog, contract terms, invoice states, payment-method token references, and active renewal schedules. Keep export names, timestamps, and row counts in this snapshot so everyone is working from the same population.

- Assign named owners and explicit approvals.

Set one accountable owner each for finance, RevOps, engineering, and compliance, with written sign-off points for data readiness, cutover readiness, and post-cutover reconciliation. If a metric has no owner, treat that as a launch blocker.

- Ground EU VAT treatment in your records before cutover week.

For EU cross-border B2C e-commerce, VAT rules changed on 1 July 2021, and previous intra-EU distance-sales thresholds were replaced by an EU-wide threshold of EUR 10 000. If you use One Stop Shop (OSS), record your Member State of identification because OSS registration is done in one Member State and is used for covered VAT declaration and payment; OSS guidance also covers record keeping and audits. If VAT treatment is complex across borders, capture whether a VAT Cross-border Ruling (CBR) is needed, noting that requests are filed in the participating EU country where the requester is VAT-registered.

- Define success metrics before cutover.

Set measurable targets for invoice correctness, renewal continuity, payout success, reconciliation close time, and exception volume. Define pass/fail rules up front so finance can approve outcomes without interpretation.

That keeps migration planning tied to evidence rather than assumptions.

Map Stripe Billing objects to Gruv modules and constraints#

Build the object map before you touch production data. If a conversion can change invoice amount, invoice timing, tax treatment, or payout timing, treat it as a finance decision, not just an engineering task.

Start with a working table and mark each row verified or unverified so owners can resolve gaps quickly.

| Stripe Billing object | Gruv module to evaluate | Decision | Verification focus |

|---|---|---|---|

| Product and price records | Invoicing | Migrate as-is, transform, retire | Price logic, billing interval, tax treatment, and support where enabled |

| Subscription and renewal schedule | Invoicing | Migrate as-is, transform | Scheduled changes, grandfathered terms, trial handling, and recurring behavior where supported |

| Invoice, credit note, and open balance history | Invoicing, ledger-linked wallets | Migrate as-is, transform | Historical parity, open amount carry-forward, and whether wallet treatment is appropriate |

| Customer credit or stored balance | Ledger-linked wallets | Transform, retire | Ledger posting rules, expiry logic if any, and finance sign-off if revenue timing changes |

| Collection or account-routing objects | Virtual Accounts | Transform | Coverage varies by market/program, onboarding requirements, and feature availability where enabled |

| Outbound disbursement use cases | Payouts | Transform | Program eligibility, payout timing, compliance gates, and market/program coverage |

Separate true 1:1 moves from redesign classes early: scheduled subscription changes, coupon logic, credits, and region-specific payment or tax behavior. These are usually where migrations drift from "same result, new system" into commercial changes.

Apply region rules before finalizing customer, invoice, or tax mapping. For intra-EU B2B sales to an EU VAT-registered business, the seller does not charge VAT on that sale. For sales to final consumers in the EU, VAT may need to be charged at the consumer-country rate, and Member States can apply VAT rules differently. If a transform drops or reinterprets tax-driving attributes, pause and require finance or compliance approval.

Keep payment behavior split in the map instead of collapsing it into one generic path. Stripe Standard pricing shows 2.9% + 30¢ for successful domestic card transactions, 0.8% for ACH Direct Debit with a $5.00 cap, and an additional 1.5% for international cards; custom packages and country-specific rates also exist. That is enough to validate domestic card, international card, and bank debit handling separately during mapping.

Execute migration in six controlled phases with go no-go checks#

The safest execution pattern is to migrate the billing-critical core first, then defer cleanup or linking work until after cutover. Keep the launch scope tight: if a task does not change billing continuity or financial outcomes, treat it as post-migration work.

If contract and pricing patterns vary a lot, cut over in phased cohorts. If variability is low and source data is clean, a narrower rolling cutover can be enough.

| Step | Action | What you are proving | Go or no-go check |

|---|---|---|---|

| Step 1 | Scope discovery | You have a clear now-vs-later migration perimeter | Each object has an owner, a transform decision, and an exception label |

| Step 2 | Normalize data | Inputs are consistent enough for reliable migration | Required fields and key financial attributes reconcile to the source snapshot |

| Step 3 | Validate in sandbox via API | The target flow behaves as expected before production use | Approved test scenarios complete with expected states and event outputs |

| Step 4 | Run in parallel | New outputs align with current production behavior | Parity checks pass on an agreed sample and event handling stays stable |

| Step 5 | Cut over by cohort | You can move production traffic without losing control | Rollback conditions are documented and first-cohort checks pass |

| Step 6 | Stabilize after cutover | Deferred tasks do not disrupt ongoing operations | Daily variance and exception checks support expansion or closure |

Step 1. Scope discovery. Lock the migration perimeter before build. A practical rule is to bring over the records needed for continuity first, then schedule non-critical cleanup as post-migration work.

Step 2. Normalize data. Define canonical values before loading anything. Freeze a pre-cutover extract and reconcile it so finance and engineering are working from the same baseline.

Validate behavior before you move real traffic#

Step 3. Validate in sandbox via API. Test complete behavior, not just record creation. For Gruv integrations, include retry and replay checks so repeated requests do not create duplicate financial outcomes.

Step 4. Run a true parallel period. Compare outputs side by side on a fixed sample. Treat unexplained mismatches as a stop signal, not a rounding footnote.

Cut over in cohorts, then stabilize#

Step 5. Cut over by cohort. Start with the cleanest segment, confirm controls, then expand. Write rollback triggers and ownership before the first production cohort.

Step 6. Stabilize and defer the rest. Keep post-cutover work focused: cleanup and linking can be completed after migration when the billable core is stable.

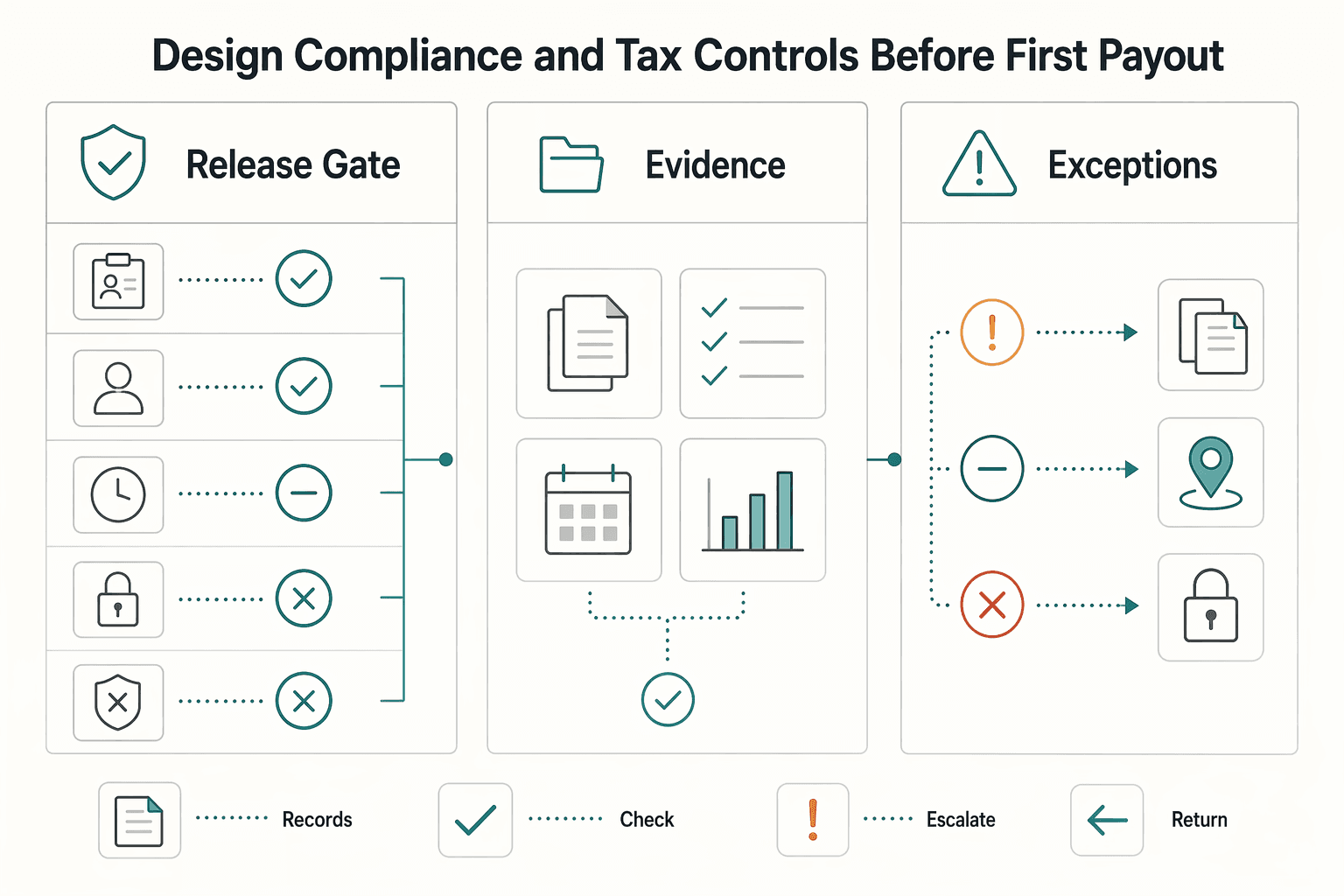

Design compliance and tax controls before first payout#

Before your first live payout, treat compliance and tax controls as go/no-go gates, not post-launch cleanup. If you cannot show who approved eligibility, what was reviewed, and why a payout was held or released, pause money movement.

| Control area | What to define or track | Key detail |

|---|---|---|

| Payout gates | Account states such as pending review, eligible, held, and blocked | Require a decision timestamp, owner, and reason code on each payout-eligible record |

| Tax document register | W-8, W-9, 1099, FBAR, and FEIE handling | Track document type, tax year, received date, reviewer, storage location, and status in one place |

| Evidence trail | Decision logs, document receipt/version details, approver/access records, and linked payout or hold events | Agree upfront on what evidence must be reproducible for GDPR and PCI DSS review readiness |

| Exception paths | Verification fails, missing documents, or payouts held for review | Route cases to a tracked exception queue with owner, next action date, and customer outreach path |

Step 1. Set payout gates before any funds move. Define clear account states before Payouts are enabled, for example: pending review, eligible, held, blocked, and require a decision timestamp, owner, and reason code on each payout-eligible record. Use your approved policy source for KYC/KYB/AML decisions, and make the refusal point explicit when verification is not cleared.

Step 2. Build a document register for tax handling where enabled. Keep one register for tax artifacts instead of splitting records across email, tickets, and spreadsheets. If your flow includes W-8, W-9, 1099, FBAR, or FEIE handling, track document type, tax year, received date, reviewer, storage location, and status in one place.

Step 3. Lock the evidence trail for review and scrutiny. For GDPR and PCI DSS review readiness, agree up front with privacy and security owners on what evidence must be reproducible, then retain it consistently. A practical baseline is decision logs, document receipt/version details, approver/access records, and linked payout or hold events. If IRS Practice Unit material appears in your process notes, label it as background only, not binding authority.

Step 4. Add explicit exception paths. Document what happens when verification fails, documents are missing, or a payout is held for review. Route incomplete or stale records to a tracked exception queue with owner, next action date, and customer outreach path, rather than clearing issues in chat or spreadsheets. For FBAR timing, rely on current FinCEN filing due-date resources and posted extension notices, not memory.

Track unit economics and operating health after cutover#

After cutover, judge the move economically, not technically: keep the new setup only if it improves operating outcomes you can measure. If margin, billing workload, and reporting speed do not improve against baseline, treat the migration as unproven.

Step 1. Build a post-cutover scorecard against the pre-cutover baseline. Lock metric definitions before review so finance and RevOps are comparing the same segments, window, and extract timing each cycle.

| Metric | What to compare after cutover | What it tells you |

|---|---|---|

| Gross margin impact | Net revenue collected versus payment, support, and billing-related operating cost | Whether the new design is improving economics |

| Billing ops effort | Hours or tickets spent on invoice fixes, credits, exceptions, and billing questions | Whether complexity shifted into manual work |

| Failed-payment handling | Recovery trend and unresolved failed-payment backlog | Whether revenue collection got stronger or noisier |

| Payout exception rate | Held, blocked, or manually reviewed payouts as a share of payout attempts | Whether money movement is stable enough to scale |

| Reconciliation cycle time | Time from period close to finance-ready reconciled numbers | Whether leadership can trust and use the numbers |

Use external case-study outcomes as context, not targets. For example, one ERP transition case study reports 95% billing accuracy and 60% faster reporting, while the same narrative describes a team that needed 11 days to produce a due-diligence MRR breakdown before improvements.

Step 2. Tie product decisions to scorecard movement. Change packaging or pricing only when the scorecard shows a clear mismatch between how customers consume value and how you charge. Evaluate adding Merchant of Record or Virtual Accounts only when tax/compliance or reconciliation pressure is materially affecting operating health. Avoid stacking multiple major changes at once unless the scorecard supports that combined move.

Step 3. Run a 30/60/90 cadence with explicit ownership. Set joint finance and RevOps reviews at day 30, 60, and 90, with clear keep/optimize/rollback calls each round. The core check is simple: are business outcomes improving in line with your migration goals, or are you still carrying the same operational drag under a new billing stack?

Common failure modes and fast recovery actions#

When post-cutover control drifts, the fastest safe recovery is to pause expansion, reconcile from frozen snapshots, and restore traceability before you clear backlog.

| Failure mode | Immediate action | Recovery focus |

|---|---|---|

| Invoice mismatches after cutover | Freeze cohort expansion immediately | Reconcile against frozen source snapshots, rerun corrected posting jobs via API, and confirm the same snapshot reproduces the same result |

| Payment-method continuity breaks | Isolate affected segments first (US/EU) | Run targeted remediation on the broken renewal path, validate upcoming renewal schedules on a sample, then re-enable broader cohorts |

| Compliance blockers stall payouts | Route held cases through the documented KYC/AML exception path | Publish a daily unblock queue with clear ownership and case status; use a CBR advance ruling path if complex cross-border VAT treatment is unclear |

| Finance loses trust in numbers | Issue daily reconciliation packs | Use ledger-to-invoice audit trails until variance stabilizes and avoid expanding reporting claims until disputed cases are traceable end to end |

Failure mode: invoice mismatches after cutover. Freeze cohort expansion immediately. Reconcile against frozen source snapshots, then rerun only corrected posting jobs via API and confirm the same snapshot reproduces the same result before scaling again.

Failure mode: payment-method continuity breaks. Isolate affected segments first (US/EU). Run targeted remediation on the broken renewal path, validate upcoming renewal schedules on a sample, then re-enable broader cohorts.

Failure mode: compliance blockers stall payouts. Route held cases through the documented KYC/AML exception path and publish a daily unblock queue with clear ownership and case status. For EU cross-border B2C VAT, keep OSS handling disciplined: since 1 July 2021, rules changed; OSS allows registration in one Member State of identification for declaration and payment, but record-keeping and audit duties still apply. If VAT treatment is unclear on a complex cross-border transaction, use a CBR advance ruling path rather than guessing.

Failure mode: finance loses trust in numbers. Issue daily reconciliation packs with ledger-to-invoice audit trails until variance stabilizes, and avoid expanding reporting claims until disputed cases are traceable end to end.

Conclusion#

The winning move is not to migrate fast. It is to enter Gruv with controlled economics, clean object mapping, and audit-ready operations on day one.

That sounds stricter than most launch pressure allows, but billing migrations should be treated as financial deployments, not just technical installs. Teams get into trouble when architecture, compliance, and unit economics are split into separate tracks, then one decision changes all three. If finance cannot trace a Gruv invoice back to the Stripe Billing source record and the approved transform rule, you are not ready to cut over.

- Unify the decision before you approve launch.

Put finance, product, and RevOps on one signed decision memo. That memo should state why you are moving now, which customer cohorts move first, what metrics define success, and which transforms are allowed to change invoice behavior or revenue timing. This is the point where migration stops being a vague platform project and becomes an operating decision with named owners.

- Prove data integrity before you expand cohorts.

Detailed mapping is one of the highest-value controls in the project. Stripe Billing objects may not move over cleanly without interpretation, so your mapping table needs explicit decisions for migrate as-is, transform, or retire. Your verification checkpoint is simple: run a parallel period, compare invoice parity and renewal continuity on a frozen sample, and confirm payout status integrity before you move the next cohort. If results are inconsistent on the same source extract, freeze rollout and fix mapping before scale makes cleanup expensive.

- Carry compliance and economics into post-cutover operations.

Do not treat KYC, AML, or VAT checks as last-minute launch tasks where enabled. They affect who can transact, who gets paid, what gets held, and what evidence must be stored when exceptions happen. The first 30 to 90 days also need an owner cadence around invoice accuracy, reconciliation close time, payout exceptions, and any DSO movement. If finance loses trust in the numbers after go-live, the migration is not complete even if transactions are processing.

Copy and paste this into your launch notes, then refuse to waive items under deadline pressure:

- Decision memo signed by finance, product, and RevOps

- Stripe Billing to Gruv mapping table approved with transform rules documented

- Parallel run and go or no-go criteria passed on invoice parity, renewal continuity, and payout status

- Compliance and tax gates validated where enabled for KYC, AML, and VAT handling

- Post-cutover scorecard live with named owners and review cadence in place

If you can check every box with evidence, you are not just moving billing. You are giving the business a billing foundation it can actually trust.

Related reading: Subscription Billing Software for SaaS Platforms Without Guesswork.

Frequently Asked Questions

What is a SaaS billing migration case study, and how is it different from a pricing case study?

A billing migration case study explains how a team moved the billing system and what changed in billing operations such as invoices, renewals, and payouts. A pricing case study is narrower. It focuses on packaging, plan design, or monetization changes, even if the billing stack stays the same. If the main risk is operational accuracy rather than price perception, you are likely looking at a migration story.

What are the top failure modes when moving from Stripe Billing to another platform?

Common failures include misfired invoices, revenue recognition errors, and missed renewals. Treat those as high-priority risk signals during migration testing. If those issues appear, pause expansion and resolve them before moving additional cohorts.

How do you de-risk go-live without freezing growth for a quarter?

Use a parallel run and phase the rollout by customer cohort instead of doing a single cutover. Before moving the next cohort, verify that invoice accuracy and renewal handling meet your predefined success metrics. A phased approach gives teams more room to catch issues early.

Which metrics prove migration success for founders, RevOps, and finance?

Define the scorecard before the project starts, not after cutover. Grounded examples include invoice accuracy and, where relevant, Days Sales Outstanding (DSO). Teams can then judge whether operational risk is dropping and whether fee impact is improving as volume changes.

When should a team migrate now versus defer the move?

Migrate when the current billing setup is limiting planned monetization changes or when fee impact is becoming material as transaction volume grows. For example, standard card pricing can include 2.9% + 30¢ for domestic cards, plus 1.5% for international cards and 1% for currency conversion, while Managed Payments can add 3.5% per successful transaction. Connect pricing can also add 0.25% + 25¢ per payout sent and $2 per monthly active account. Defer when the current setup still supports near-term needs and migration risk outweighs near-term benefit.

What unknowns must be resolved before committing to migration scope?

Resolve the evidence set first: product catalog, contract terms, invoice states, active renewal schedules, payment-method continuity assumptions, and owner sign-off across core functions. A common scope risk is hidden transformation work when legacy billing data does not map cleanly into the target model. If ownership for those decisions is still unclear, pause scope approval.

How do compliance requirements like GDPR and PCI DSS change migration design?

They can affect migration design, but exact control requirements should be validated with your compliance and legal teams for your specific environment. Include compliance sign-off gates before cutover rather than treating compliance as a late-stage review.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- das.nebraska.gov/materiel/purchasing/120277%20O3%20REBID/Gene...trusted

- europa.eu/youreurope/business/taxation/vat/cross-borde...trusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- gear.delaware.gov/wp-content/uploads/sites/103/2025/11/2025-GE...trusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- scholar.afit.edu/cgi/viewcontent.cgitrusted

- spaces.calstate.edu/wiki/spaces/UMA/44007479.htmltrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Writing Case Studies for B2B SaaS That Buyers Trust

If you work independently, you do not need another gallery of polished examples. You need a way to produce B2B SaaS case studies that help a buyer trust the result, help a client feel fairly represented, and hold up in review when someone asks, "Where did this number come from?"

SaaS Usage-Based Pricing for Predictable Cashflow and Fewer Disputes

If you are considering **saas usage-based pricing**, treat it as an operations and collections decision first. Pricing works best when the usage unit can be measured, shown on the invoice, and explained by someone outside your product team.

The Best Tools for Managing Subscription Billing

**Protect cashflow by selecting for recovery and control first, then layering convenience features.**