Quick Answer

Choose the best workation cities europe shortlist only after confirming tax and paperwork sequence, not lifestyle appeal. Prague, Budapest, Lisbon, Barcelona, Berlin, and Krakow should be compared through delivery reliability, admin friction, eligibility timing, and complex-case fallback. The practical rule is simple: no deposit or long lease until your VAT route is confirmed, your filing rhythm is mapped, and ownership of documents is clear.

Start Here Before You Pick a City#

Pick a city only after you can explain how client delivery and tax admin will work there in the same month. If either part is unclear, lifestyle fit is noise.

| Path | Eligibility or trigger | Next step |

|---|---|---|

| Cross-border SME route | If Union annual turnover is above EUR 100,000 in the current or previous calendar year, the route is not available | File one prior notification in your Member State of establishment; plan around a process that should not exceed 35 working days |

| OSS | Your activity fits One Stop Shop | Choose one Member State of identification and map declaration, payment, record-keeping, and audit duties before you move |

| VAT Cross Border Ruling | VAT treatment is unclear | Request it in the participating EU country where you are registered for VAT |

Start with sequence, not neighborhoods. Since 1 July 2021, EU cross-border B2C VAT rules changed, including the move from older intra-EU distance-sales thresholds to one EU-wide EUR 10,000 threshold. That detail will not choose your city for you, but it will tell you whether your current setup can travel without avoidable rework.

Run these checks before you compare rent, weather, or coworking options:

- SME eligibility check: If Union annual turnover is above EUR 100,000 in the current or previous calendar year, the cross-border SME route is not available. If you are eligible, file one prior notification in your Member State of establishment and plan around a process that should not exceed 35 working days.

- OSS registration decision: If your activity fits One Stop Shop, choose one Member State of identification and map declaration, payment, record-keeping, and audit duties before you move.

- Complex transaction fallback: If VAT treatment is unclear, request a VAT Cross Border Ruling in the participating EU country where you are registered for VAT.

Keep your evidence pack in one place before any long-stay booking: proof of VAT status, prior-notification records where relevant, and a filing calendar tied to your invoice cycle. This is not paperwork for later. It is your readiness test.

A quick self-check helps here. Write one line for your VAT route, one line for your next filing date, and one line for the document owner. If any line is blank, do not choose between cities yet. You are still defining how the move will run.

Use one plain-language filter before you commit: can you state your VAT path, filing rhythm, and document owner in a few sentences without guessing? If the answer is no, stay in research mode. That pause is a practical control, not delay for its own sake. It protects you from choosing a city that looks great on paper but adds admin pressure you cannot absorb once deadlines start.

Who This List Is For and How Cities Are Scored#

This guide is for remote professionals deciding between Prague, Budapest, Lisbon, Barcelona, Berlin, and Krakow who need to keep delivery quality and compliance stable at the same time.

Treat it as an execution ranking, not a travel ranking. Country-level headlines can help with context, but they do not tell you whether your city-level setup holds when invoices, filing dates, and housing timelines collide.

Score each city against four decision factors:

- Reliability pressure: What does one missed delivery week cost in revenue and client trust?

- Admin friction: How heavy are registration, declaration, payment, record-keeping, and audit obligations for your setup?

- Eligibility and timing: Can you use simplified routes, and does your move window fit expected processing time?

- Complex-case risk: If treatment is unclear, do you have a fallback path before long housing commitments?

Weight these factors intentionally. If you run client-facing retainers, reliability pressure usually deserves first priority. If your work is project-based with flexible timing, admin friction and eligibility timing may carry equal weight. The point is not to invent a perfect formula. It is to stop making a lifestyle-first call and discovering later that filing ownership is still unclear.

Think in downside scenarios, not best-case narratives. If one delayed week could damage active accounts, prioritize stability and clear ownership over cheaper rent. If your timeline has buffer and your revenue is less sensitive to one rough week, cost control can carry more weight as long as admin steps still clear on time.

A practical rule that holds up in real planning: choose infrastructure-first cities when delivery stability protects your income, and choose budget-first cities only when connectivity, timing, and compliance steps are already mapped.

If two cities still look equal, break the tie with timing confidence. Pick the one where the next filing cycle is clear, documents are ready, and fallback steps are usable if one approval slows down. Then use the table below as a shortlist filter, not a popularity contest.

For a concrete next step, Browse Gruv tools.

Quick Comparison Table for the Cities Most Often Mentioned#

Use the table to narrow your choices, then validate execution details before any deposit. A city stays on the shortlist only when the tax route is confirmed and the first filing cycle is realistic.

| City | Best for | Key pros | Key cons | Best use-case |

|---|---|---|---|---|

| Prague | Structured trial month | Fast first-pass check against your VAT and timing checklist | A late compliance start can break an otherwise strong plan | Keep it when the EUR 10,000 cross-border B2C threshold context is clear for your activity |

| Budapest | Cost-controlled planning | Clear go or no-go when eligibility is mapped early | Lower monthly costs do not offset admin delays | Keep it only if cross-border SME eligibility is realistic under the EUR 100,000 Union turnover cap |

| Krakow | Focused work sprint | Works well when your admin timeline is explicit before move-in | Declaration and record duties still apply throughout the stay | Use it when your schedule can absorb up to 35 working days for cross-border SME registration processing |

| Lisbon | Longer-stay planning | Good fit when the paperwork route is mapped before commitment | Demand pressure increases downside if you commit before checks are complete | Prioritize after confirming whether OSS in one Member State of identification fits your case |

| Barcelona | Client-facing periods | Strong option when delivery rhythm and tax plan are both stable | Higher fixed commitments raise risk if assumptions are unresolved | Choose it after your declaration, payment, and record-keeping path is fully defined |

| Berlin | High-structure work cycle | Strong fit when reliability matters and process ownership is clear | Pressure rises quickly if paperwork timing drifts | Use it after deciding whether OSS is enough or a CBR request is needed for complex cross-border transactions |

Use the table in two passes. First, remove any city where your route is still unresolved. Second, compare only the remaining options by delivery risk during your first filing cycle. This avoids a common mistake where a city looks attractive in a table but fails during the first month of real admin deadlines.

When a city is still pending, define what has to become true before you move it to confirmed. Useful checkpoints are route confirmation, completed prior notification where relevant, and a filing calendar tied to first invoices. If you cannot name those checkpoints clearly, that city is blocked for long commitments.

Lisbon and Prague for First-Time Long Stays#

For a first long stay, pick the city where your VAT sequence is clear first. Lisbon and Prague can both work, but neither forgives last-minute admin.

The real tradeoff is commitment speed versus documentation confidence. One option may tempt you into a faster housing decision, but speed is a liability when filing steps are unresolved. Compare both cities with the same checklist and the same assumptions before preference takes over.

Run these five checks in both locations:

- Since 1 July 2021, cross-border B2C VAT rules changed, including the EU-wide EUR 10,000 threshold.

- If OSS fits your setup, use one Member State registration and confirm declaration, payment, record-keeping, audit, and exit handling.

- If you plan to use the cross-border SME scheme, confirm eligibility first. Union turnover must not exceed EUR 100,000 in the current and previous calendar year.

- If eligible for the SME route, file prior notification and plan for processing that should not take longer than 35 working days.

- If cross-border VAT treatment is still unclear, request a VAT Cross-border Ruling in the participating EU country where you are registered for VAT.

If both cities still look viable, use this tie-breaker. Ask which option gives you clearer filing ownership, fewer compressed dates, and easier fallback if one approval step moves late. Pick that city first, even if the lifestyle preference points the other way.

In practice, the lowest-risk choice is a short initial stay with a normal client load and the same admin checklist in both cities. Extend only after you confirm two outcomes under real conditions: delivery quality stayed steady, and the paperwork sequence held under timing pressure.

Budapest and Krakow for Budget-First Planning#

Budget-first planning works only when lower costs stay predictable and admin timing stays intact. If either side slips, the cheaper headline disappears fast.

Treat Budapest and Krakow as execution decisions, not discounted backups. Before you label either one affordable, check whether you may cross the EUR 10,000 cross-border B2C threshold during your stay. If VAT treatment is complex, file a VAT Cross-border Ruling request in the participating country where you are VAT-registered before taking on longer housing commitments.

Use one gate before you sign anything:

- Confirm fixed monthly costs are predictable across the full stay window.

- Verify your VAT route still fits expected revenue levels.

- Check that your calendar can absorb required registration steps.

This is where many budget plans lose discipline. People lock in the lowest-rent path, then discover that a delayed filing step forces rushed housing choices or expensive timing changes. Lower monthly cost cannot rescue a weak sequence.

If you plan around the cross-border SME scheme, keep the EUR 100,000 Union turnover cap visible from month one and account for a process that should not take longer than 35 working days after prior notification. If those dates do not fit your move window, delay booking and protect cash flow instead of forcing the timeline.

A common failure mode is building the plan from the lowest rent estimate while ignoring sequence risk. Once registration steps slip, total cost climbs through rushed housing choices and avoidable process stress. That is why budget-first planning still begins with timing discipline.

Barcelona and Berlin for Infrastructure-First Planning#

When a missed delivery week is expensive, Barcelona and Berlin should be treated as reliability decisions first and cost decisions second. The city matters less than whether your tax path is fully mapped before you sign housing.

Infrastructure-first planning is about controlling variance, not chasing status. Paying more can be the better financial move when it lowers the chance of delivery disruption during filing milestones. That logic works only when responsibilities and dates are assigned in advance. Without clear ownership, a higher-cost city simply magnifies process mistakes.

Do not assume either option is automatically safer. Apply the same gate to both:

- Confirm which VAT route you will use.

- If OSS applies, verify one Member State registration covers eligible declaration and payment duties.

- If you plan to use the cross-border SME route, verify the EUR 100,000 Union turnover cap and that the expected 35 working day registration timeline fits your move window.

- Map filing dates and record-keeping requirements before move-in.

A useful operator check is to rehearse a single month of execution. Note who handles each filing step, who stores records, and what happens if a document request arrives during peak client delivery. If that simulation is unclear, the city is not ready yet.

If any core item is unresolved, pause the commitment. A clear admin sequence protects client trust better than lower monthly costs paired with filing uncertainty. Once that sequence is solid, you can judge whether higher fixed commitments are justified.

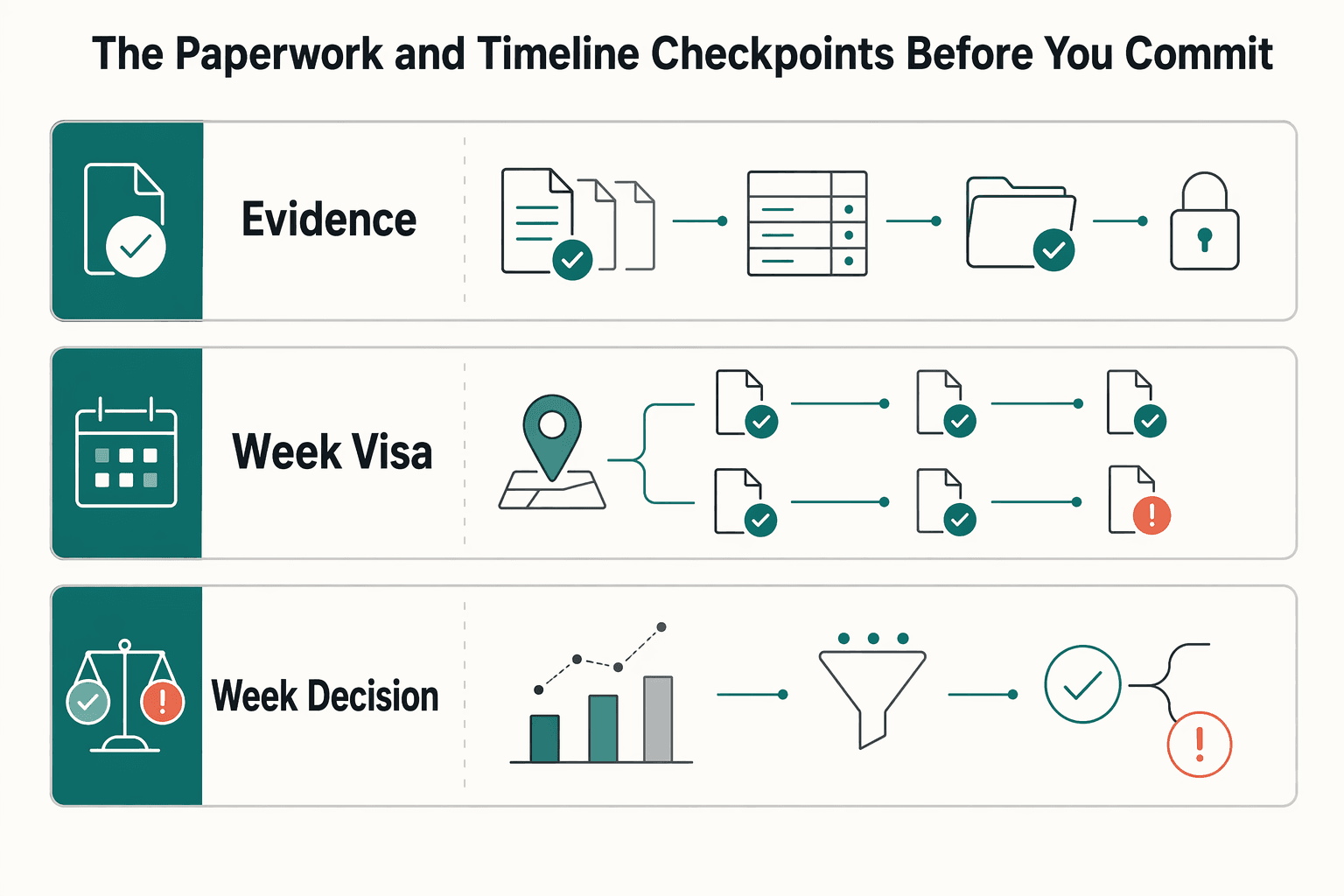

The Paperwork and Timeline Checkpoints Before You Commit#

Do paperwork in sequence before you pay deposits. This eight-week plan turns uncertainty into a clear go or no-go decision and makes city comparison much easier.

| Weeks | Focus | Key checkpoint |

|---|---|---|

| Week 1-2 | Shortlist and document map | Cut the list to two or three cities; assign an owner to each file; define submission order |

| Week 3-4 | Visa check and tax route fit | Validate visa requirements; test route fit for OSS versus the cross-border SME scheme; file one prior notification in your Member State of establishment for the SME path |

| Week 5-6 | Build the evidence pack | Include proof of VAT status, prior-notification records where relevant, and a filing calendar tied to declaration and payment dates |

| Week 7-8 | Go or no-go decision | Commit only when housing proof is in hand, tax treatment is clear, and filing dates are realistic; use the 35 working day expectation for SME registration as a planning checkpoint, not a guarantee |

- Week 1-2: Shortlist and document map

Cut the list to two or three cities using hard filters, then build one document map per path. Assign an owner to each file, define submission order, and write what counts as complete for every item. Separate routes early. OSS is one Member State registration path for covered VAT duties, while the cross-border SME scheme has different entry conditions and gates.

This phase feels simple, which is why weak plans often slip through here. Stay strict: if a city only works when ownership is vague, it does not actually work. The output you want is concrete: one route candidate, one owner map, and one list of dependencies that could block move-in.

- Week 3-4: Visa check and tax route fit

Validate visa requirements early against official criteria before committing money. In parallel, test route fit for OSS versus the cross-border SME scheme based on your activity and timeline. For the SME path, file one prior notification in your Member State of establishment, which acts as the contact point with other Member States.

Treat this as a true dependency, not admin you can catch up on after arrival. By the end of this phase, you should know which route you are pursuing and what must be submitted next. If that answer is still fuzzy, stop before deposits.

Use a simple closeout question at the end of week 4: can a teammate review your route choice and arrive at the same next action without extra explanation? If not, the plan is still too ambiguous.

- Week 5-6: Build the evidence pack

Prepare one organized file set for registration, declarations, payments, and audit-ready records. Include proof of VAT status, prior-notification records where relevant, and a filing calendar tied to declaration and payment dates. Keep versioned copies and a dated checklist so follow-up requests are easy to answer consistently.

If you plan to use the cross-border SME exemption, monitor the EUR 100,000 Union turnover cap continuously and wait for EX number confirmation before treating supplies as VAT-exempt. This checkpoint catches most execution gaps early: missing records, unclear owners, and conflicting dates are red flags, not minor admin tasks.

Before moving forward, run one verification pass: confirm every file has an owner, every date has a reminder, and every unresolved item has a next action. Anything unowned at this stage usually becomes urgent later.

- Week 7-8: Go or no-go decision

Commit only when housing proof is in hand, tax treatment is clear, and filing dates are realistic for your first client cycle. Use the 35 working day expectation for SME registration as a planning checkpoint, not a guarantee. If a core dependency is uncertain, move the window instead of forcing the date and drifting into the Tax Resident of Nowhere risk.

Before final commitment, run a dry sequence on paper: first invoice date, declaration cutoff, payment date, and who submits each item. This single exercise exposes ownership gaps before money is locked into housing.

The common breakdown is fragmented ownership. One person tracks housing, another tracks tax, and nobody owns final readiness. Keep the full sequence in one checklist with dated status and named owners. If you want another example of a documentation-heavy relocation path, read The Taiwan Gold Card: A Visa for High-Skilled Professionals.

The bridge from planning to commitment is simple: if the sequence survives a dry run with named owners and realistic dates, move ahead. If it does not, adjust city or timing while changes are still cheap.

Red Flags That Should Make You Change City or Timing#

Treat one failed checkpoint as enough to pause. Waiting for clarity is usually cheaper than cleaning up a lease, filing error, or timing mismatch after arrival.

Most avoidable failures follow the same pattern: the city still feels attractive, so planning keeps moving while documents fall behind. Use these signals as hard controls.

- Country headline replaces city-level checks

A country mention in a roundup is not enough to book a specific city. Keep options open until each candidate has a workable filing calendar, clear document ownership, and housing proof. If your plan depends on cross-border B2C treatment, confirm the EUR 10,000 threshold context applies to your activity.

- Forum advice cannot be verified in documents

If advice cannot be tied to official forms, filing steps, or authority guidance, stop and verify before spending money. Maintain an evidence pack with registration status, submission dates, and pending actions. For complex VAT treatment, CBR requests are filed in the EU country where you are VAT-registered and must follow that country's VAT ruling conditions.

- Visa, housing, and tax are validated separately

A green light in one lane does not protect the other two. Lease timing, visa sequence, and VAT route need to clear in the same window. Under the cross-border SME route, prior notification comes first, and VAT exemption starts only after EX number grant and confirmation.

- Budget works only in a best-case month

If the plan works only when every date lands perfectly, delay commitment and add a contingency month for admin slippage. Keep threshold logic clean: EUR 100,000 is the cross-border SME scheme Union turnover ceiling, while EUR 10,000 is the cross-border B2C e-commerce threshold context.

Decision fatigue is another warning sign. Teams sometimes keep a city because they are tired of comparing options, not because documentation improved. If you cannot point to what changed in the evidence pack, execution risk did not change either.

When a red flag appears, freeze commitments first, then update your evidence pack, then reset the decision date. That order prevents emotion from driving the next move.

Use these red flags as decision controls, not discussion points. If one appears, adjust city choice or timing before you sign.

Pick a City You Can Actually Execute#

Choose the city you can run on schedule, not the one with the loudest reputation. A strong decision is one where delivery, budget, and compliance still hold when real deadlines arrive.

Before signing, run these checks in order:

- Tax path is executable: Map one route with named owners, filing dates, and fallback actions. If OSS is your route, confirm one Member State registration covers eligible EU distance sales and cross-border services.

- Timeline is realistic: Align your move date with actual processing expectations. For cross-border SME access, registration should not take longer than 35 working days after prior notification, and VAT-exempt supplies start only after your Member State of establishment grants and confirms the EX number.

- Threshold logic is clean: Keep rule contexts separate and test assumptions against the correct threshold. Do not mix the EUR 100,000 SME cap with the EUR 10,000 e-commerce threshold.

Run one final document check against your move calendar and first client cycle. If a core dependency is unresolved, keep the shortlist open and delay commitment.

Execution confidence should be your closing criterion. If the same checklist still makes sense under deadline pressure, you are ready to commit.

If Portugal remains your preferred option, continue with Portugal Digital Nomad (D8) Visa: A Complete Guide. Then review Tax Resident of Nowhere risk before final dates, or Talk to Gruv to confirm what is supported for your specific country or program.

Frequently Asked Questions

What makes a city one of the best workation cities in Europe?

For this checklist, "best" means your admin path is clear before you commit: which VAT context applies, which thresholds apply, and when registration and filing steps happen.

What is the difference between a workation and digital nomad life?

These sources do not define lifestyle labels. For planning, treat shorter vs longer or repeated cross-border stays as an admin-sequencing question and validate VAT steps early.

Which cities are most commonly recommended right now?

City rankings vary widely by source and change frequently. Check recent travel and digital-nomad publications for up-to-date recommendations.

How should I compare cities when rankings are incomplete?

Use one scorecard with admin readiness first: applicable VAT context, key thresholds, and timing. Keep thresholds separate by context, including the EUR 10 000 e-commerce threshold and the EUR 100 000 Union turnover limit for the cross-border SME scheme.

Is a country-level ranking enough to choose a city?

No. These materials are EU/country-level VAT administration guidance and cannot validate city-level timing, costs, or document readiness.

When should I pick Lisbon over Prague or Budapest?

These sources cannot determine whether Lisbon, Prague, or Budapest is the right choice. Decide only after your VAT path and timeline are workable for your planned country context.

What is the biggest planning mistake before a long stay?

Committing to major costs before VAT sequencing is clear. Under the cross-border SME scheme, file one prior notification in your Member State of establishment, confirm your Union turnover stays within EUR 100 000, and plan for a process that should not take longer than 35 working days after receipt of that notification.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Portugal Digital Nomad Visa Decisions That Prevent D8 Delays

Start with verification, not paperwork. In this research set, some material is useful only as EU VAT context, not as D8 instruction, and mixing those categories is one of the fastest ways to build the wrong plan. We use the same separation rule in [Global Digital Nomad Visa Index](/blog/global-digital-nomad-visa-index) comparisons.

Taiwan Gold Card Application Strategy for Remote Professionals

Treat this process as a chain of linked decisions, not a race to submit. If you are planning a serious move or a long stay in Taiwan, the safer outcome usually comes from choosing the right route first and proving each core claim before you pay or file. The Taiwan Employment Gold Card rewards that discipline because it combines four functions in one status: a work permit, resident visa, Alien Resident Certificate (ARC), and re-entry permit.

The Tax Resident of Nowhere Myth and the Real Risk in 2026

A "tax resident of nowhere" position may be possible in narrow cases, but it can be hard to defend when your records are inconsistent. The practical target is simpler and stronger: choose one tax residency position you can defend across filings, contracts, and account reviews.