Quick Answer

Pick two disbursement lanes: ACH-first for routine payouts and a separate urgent lane, then test both in a constrained cohort before any new-market rollout. The go/no-go decision is record quality, not rail count: each payment should tie to sign-off, remittance details, provider status, and an accounting outcome in systems such as Xero or Zoho Books. Expand only when retries and investigations have named owners.

How to Choose a 2026 Disbursement Model#

For operators evaluating new markets, the key decision is operational: choose the disbursement model your team can run cleanly across your vertical, country mix, and risk profile. That is the practical lens behind b2b payment trends 2026 platforms rethinking contractor vendor disbursements.

The 2026 signal is directional, but easy to overread. One newsletter summary said 67% of merchants now see payments as a key business focus, rising to 78% among digital leaders. It also described a shift from single-PSP setups to multi-processor models averaging four per merchant. The takeaway is useful, but the tradeoff matters just as much. More reach and routing flexibility also bring more complexity.

One 2026 vendor release described teams moving from spreadsheet-driven, one-by-one payouts to bulk disbursement flows that consolidate many payouts into one run. It also said one interface can support ACH, wire transfers, checks, and digital-wallet payouts. In that example, transactions sync to accounting platforms such as Xero and Zoho Books for automatic record updates. Even if adoption is uneven, the practical lesson holds: payout design affects accounting quality, not just payment speed.

This article compares five practical models for contractor and vendor disbursements, then maps the controls and rollout order that reduce rework. The models are judged by day-to-day operating fit:

- how cleanly accounts payable can approve, batch, and release payouts

- how much downstream burden support or receivables teams carry when remittance data is weak

- whether reconciliation is mostly automatic or turns into month-end cleanup

- where control and exception-management burden grows as rails or providers are added

- how country-level constraints change what works

Country variation is a real constraint, not a footnote. One 2026 guide compares real-time payment systems across 10+ countries, including UPI, PIX, FedNow, Faster Payments, and SEPA Instant. A model that works in one market can break in another when local method expectations and provider coverage differ.

The recommendation is simple: choose a model only after you can prove two controls. First, each payout traces cleanly to an accounting entry with audit-ready visibility. Second, clear owners handle exceptions, retries, and remittance mapping when flows fail. Without those controls, adding faster rails or more providers can create manual work before it creates value.

Treat expansion as an operating-readiness decision, not a rail-shopping exercise: does your payment setup hold up at real volume without degrading reconciliation or increasing avoidable payout risk?

How this list is scored and who should use it#

Use this list when you are selecting disbursement architecture for market expansion or adding payout options. If you only need one domestic rail for a stable workflow, this is probably more than you need.

Best fit#

This scoring is for teams at the point where payment operations start limiting scale, not for first-time setup. Early-stage businesses often under-prioritize B2B payments, so this section is aimed at the stage where ownership gaps and exception handling begin to hurt execution.

What gets weighted#

We score models on operational fit, not rail marketing. The real test is whether you can add payout rails without increasing manual burden across payment operations.

We also weight data usability after funds move. That includes remittance fidelity and whether payout data can be matched cleanly in your accounting workflow.

What to verify before trusting any score#

Ask for proof, not a roadmap slide. You should be able to trace a completed payout to its approval record, remittance details, and resulting accounting entry.

No-go rule#

If no one clearly owns exceptions, retries, and remittance mapping, pause expansion. Cross-border payments can be slow and expensive, and risk and compliance pressure can reduce correspondent banking access in some corridors. Adding payout options without clear ownership usually increases operational risk.

Quick comparison of the 5 disbursement models#

Use this as a decision scaffold, not a benchmark. The useful question is not which rail sounds most modern. It is where control and data complexity will land in your operating model.

The research behind this article points to payments moving online quickly, including B2B, but it does not validate rail-by-rail performance outcomes.

This table is directional only. Validated thresholds for fraud pressure, ISO 20022 interoperability, or launch timelines are not established here, so scored readiness labels are intentionally omitted.

| Model | Best for | Primary rails | Required systems | Control burden | Failure modes | Time-to-launch | Fraud readiness | Data interoperability |

|---|---|---|---|---|---|---|---|---|

| 1. ACH-first with selective real-time escalation | Teams that want one default path plus tightly scoped exceptions | ACH as default, with exception rails as needed | Approval ownership, payee data controls, remittance capture, ERP posting path (to validate) | Context-dependent (not validated here) | Implementation-specific (not validated here) | Confirm with the relevant authority | Verify in-app | Verify in-app |

| 2. Virtual card-led control for approved vendor segments | Teams prioritizing policy control for specific supplier groups | Virtual cards plus fallback rail(s) where needed | Supplier segmentation, card control rules, ERP mapping for remittance and fees (to validate) | Context-dependent (not validated here) | Implementation-specific (not validated here) | Confirm with the relevant authority | Verify in-app | Verify in-app |

| 3. Real-time first for time-critical payouts | Teams where payout timing is operationally sensitive | Real-time rails first, with fallback rail(s) | Identity checks, approval design, exception ownership, ledger sync (to validate) | Context-dependent (not validated here) | Implementation-specific (not validated here) | Confirm with the relevant authority | Verify in-app | Verify in-app |

| 4. ERP-native disbursements tied to reconciliation quality | Teams optimizing for close quality and traceability | Rail-agnostic routing through ERP-centered approval and posting logic | ERP ownership, master data discipline, remittance field governance (to validate) | Context-dependent (not validated here) | Implementation-specific (not validated here) | Confirm with the relevant authority | Verify in-app | Verify in-app |

| 5. Cross-border hybrid for phased market entry | Teams entering multiple markets with non-uniform payout constraints | Multi-rail mix by market and payee type | Routing rules, normalized provider outputs, evidence handling, ERP translation layer (to validate) | Context-dependent (not validated here) | Implementation-specific (not validated here) | Confirm with the relevant authority | Verify in-app | Verify in-app |

How to use this comparison#

Do not treat a rail name as proof of control. Compare models by whether you can preserve approval context, remittance detail, and accounting traceability end to end without manual repair.

Because rail-by-rail performance, fraud-rate differences, or ISO 20022 adoption outcomes are not validated here, use the table to set test priorities rather than make final claims. For a closer look at one option, read Virtual Credit Cards for Platforms: How to Issue Single-Use Cards for Contractor and Vendor Payments.

Model 1 ACH-first with selective real-time escalation#

For many teams, the practical starting point is ACH as the default path, then escalating only defined exceptions to real-time payments when timing is operationally critical. That keeps the standard flow predictable while still giving you a faster option for urgent cases.

- Best for: Predictable payout cycles where most disbursements are not urgent, but a limited set of cases cannot wait for standard processing.

- Pros: A clear default path for operations, plus targeted access to real-time rails for exceptions that need immediate movement.

- Cons: If escalation criteria are unclear, exception handling can drift into manual follow-up; this model also does not remove broader B2B friction, including slow or expensive flows in some cross-border contexts.

- Concrete use case: Process contractor and vendor disbursements through ACH by default, and route only SLA-critical payouts to real-time payments using documented approval triggers and explicit exception ownership.

Model 2 Virtual card-led control for approved vendor segments#

Treat this as a narrow, test-first option for pre-approved vendor segments, not a default rollout. The available evidence supports market attention on B2B payments and card issuing. But the provided excerpts do not include direct virtual-card operating evidence, so you should not assume virtual cards will automatically improve policy enforcement, traceability, fraud outcomes, or reconciliation performance in your environment.

Where this model fits#

Use this model when you can define exactly which vendors, spend types, and approval conditions are in scope, and keep a fallback rail, including ACH, where acceptance and downstream posting are still uncertain.

That caution fits current market context. FT Partners (March 2026) tracks the space with dedicated IPO, M&A, and financing sections, and highlights high activity around FinTech Meetup (March 30 to April 1, 2026; 4,000+ attendees; 50,000+ meetings). PYMNTS also notes that strategic decisions now define trajectory amid rapid digital transformation, M&A, and economic pressures, so local operating fit still has to be proven.

What to verify before you expand#

Before you expand beyond a contained pilot, confirm with internal evidence:

- supplier acceptance for the invoices or spend types in scope

- remittance delivery in a format the supplier can process reliably

- mapping from payment records to your internal invoice, vendor, or purchase references

- complete operating evidence: approval trail, payment reference, remittance output, and posting result

If suppliers update payment preferences through intake forms, include a verification gate. Payment-related intake should not be treated as a frictionless surface.

Rollout decision rule#

Scale this model only when pilot evidence shows stable supplier handling, reliable posting, and controlled exception ownership. If those checks are not stable yet, keep scope narrow and continue using existing rails, including ACH, for segments where execution is already predictable.

Model 3 Real-time first for time-critical contractor payouts#

Use this model when payout timing is part of the payee experience, not just a treasury preference. If a meaningful paid-worker segment depends on frequent transactional payouts as working income, separate those time-critical payouts from your routine vendor lane.

That split is grounded by the demand pattern, not by any single rail choice. Nearly one-third of millennials depend on transactional payouts from gig work and tips as their main source of income. That supports separating urgency-based payout cases from routine vendor payment policy.

Where this model fits#

This is a targeted operating model, not a full outbound-payment replacement. It fits when you can define clear urgency criteria for contractor payouts and run those cases separately from normal vendor disbursements.

Start with narrow scope. Keep real-time-first handling limited to approved contractor scenarios, and expand only after your handling and posting flow are stable.

What to verify before you scale it#

Before broad rollout, confirm you can maintain consistent end-to-end records for each urgent payout case from initiation through final posting. If those records are incomplete or inconsistent, scaling can increase cleanup work faster than it improves payout timing.

The main tradeoff#

The upside is precision: you reserve faster payout handling for contractor moments that justify it. The tradeoff is operational complexity, especially as routing expands.

There is also a broader shift from single-processor setups to multi-processor models, averaging four per merchant. That can increase reach and flexibility, but it also adds complexity. Payment orchestration through one API can help with routing and local-method support, but it is not always the best fit. Alternatives can be more appropriate depending on your scale and geography. Related: The State of Global Contractor Payments 2026: Fees Speeds Rails and Trends.

Model 4 ERP-native disbursements tied to reconciliation quality#

If speed is not the bottleneck, reconciliation can be. Use this model when close quality is your launch gate, not payout speed. The core question is whether your payment data can move from approval to bank movement to ledger update without creating recurring manual cleanup.

This differs from a real-time-first lane. The value here is traceability and posting reliability. If that chain is weak, adding payout options can increase manual reconciliation work instead of reducing it.

Where this model fits#

This model fits teams that use the ERP as a system for AP and AR, not just reporting. In practice, you are checking whether payment activity returns with enough reference detail to support automatic reconciliation and invoice-to-cash continuity.

Fortis describes the upside directly: when transactions flow into the operating platform, manual reconciliation and invoice chasing can drop. For contractor and vendor disbursements, that is the point of the model: preserve context with the payment, not just settlement status.

What you gain when the plumbing is ready#

The gains are operational, not flashy: cleaner invoice-to-cash continuity, better batch visibility, and stronger automatic reconciliation potential. Fortis also cites Ardent Partners that digital workflows can reduce invoice processing time by up to 50%. That is a useful signal even though outcomes vary by implementation.

Guidehouse adds why this matters strategically: payment capability is tied to broader transformation programs, and over 70% of financial institutions' IT transformation programs include at least one payments-related overhaul. That includes adjacent work such as ISO 20022, real-time settlement readiness, and treasury modernization.

What usually breaks first#

A common failure mode is that payment execution improves while follow-through work still stalls. Fortis notes that payment programs can plateau with missed collection opportunities and extra follow-up. The disbursement parallel is similar: money movement modernizes, but manual follow-up and reconciliation work can persist in exception queues.

What to verify before launch#

Base launch readiness on repeatable evidence, not demos.

| Checkpoint | What to verify | Evidence to keep |

|---|---|---|

| Remittance mapping | References consistently map to the right invoice or bill and vendor or customer record | Matched samples and an exception log with aging + owner |

| Approval routing | Higher-risk payments capture required sign-off before initiation | Transaction or batch records showing manager or CFO approval where required |

| File and batch handling | Bank files and grouped batches import and post back cleanly | Sample files, batch results, and final posting outcomes |

Two concrete control examples from the source material are worth testing against your own stack. One is manager or CFO signature routing when required. The other is support for CODA files plus grouped payment initiation, including one listing that cites support for 26 Belgian banks. Treat those as implementation checkpoints, not universal standards.

A practical launch rule is to proceed only when remittance-to-invoice matching is stable in a pilot cohort and exception queues are owned by named AP or finance ops roles. If record quality is still uneven, fix that first. This model pays off when data integrity is treated as a product requirement. For related upstream controls, see Vendor Data Management: How Platforms Keep Contractor Payment Details Accurate and Compliant.

Model 5 Cross-border hybrid for phased market entry#

Once your reconciliation chain is reliable domestically, this is the model for phased international expansion. Use it when you need consistent reconciliation evidence across cross-border flows, not just faster payout speed. The operating goal is to keep reporting and controls comparable as geography changes.

This builds on Model 4: first prove your reconciliation chain is reliable, then prove it stays reliable as you add new corridors and counterparties.

Where this model fits#

This model fits when your expansion plan is segmented by geography and deal type, not treated as one generic international rollout. FT Partners' March 2026 lens is useful as a scoping pattern here because it frames market analysis through geography and deal-type breakdowns across sectors. Treat each corridor as a scoped decision with explicit assumptions, ownership, and success checks before broader rollout.

What a pragmatic rollout looks like#

Roll out in narrow phases, then expand only after the first phase produces clean operational evidence. The core risk is less about the payment-method mix itself and more about adding country logic ad hoc so references, statuses, and exception handling become inconsistent market by market.

PYMNTS' midpoint-2025 framing is a practical reminder: these are high-stakes decisions under simultaneous transformation, M&A activity, and economic pressure, so early phases should stay small enough to inspect.

What to standardize before adding the next country#

Before expansion, require the same minimum operating record for every payout:

- corridor identifier, method used, and beneficiary record version at initiation

- approval record, provider reference, and returned settlement status

- ERP posting outcome, plus named exception owner and aging when matching fails

If you cannot compare payouts across corridors using the same fields, pause expansion and fix that first.

Risks and decision rules#

A likely failure mode is bolting country-specific steps onto a domestic process. Money may still move, but comparability can drop and manual cleanup can grow.

Also track emerging settlement designs. Flagship notes that in the last 12 months some corporates and financial institutions have begun using fiat-backed stablecoins to reduce cross-border settlement times. Treat that as a market signal to monitor, not a substitute for consistent beneficiary data, approval trails, and posting outputs.

Control layer required before scaling any model#

Scale is safer when your control layer stays stable across routing choices. As teams move from a single PSP to orchestration or multi-processor setups, often averaging four processors per merchant, reach can improve, but operating complexity rises with it. Orchestration is one option, but other architectures can still be viable depending on scale and geography.

That matters across every model in this list, especially during periods of rapid payments change. Keep controls consistent as volume, countries, and providers expand so your evidence chain remains usable.

- Fraud pattern ownership

If check fraud, business email compromise, or social engineering are in scope, define control playbooks before you add more rails. Ownership and escalation design are operating choices, so document who can hold payouts, who validates change requests outside email, and who approves release.

- Evidence pack from request to posting

Use a consistent evidence bundle for each payment, such as approval trail, provider reference, ledger event, and reconciliation export. If you run orchestration through one API across multiple providers, capture your internal payout ID and provider reference at initiation so reconciliation and posting stay traceable as routing changes.

- Authorization surfaces for payout-detail changes

Treat sensitive payout-detail updates as controlled authorization events, not routine service requests. For bank account, beneficiary, or payee changes, require a verifiable authorization surface and retain documentation tied to the record version that changed; DocuSign-verified updates are one possible method, not a universal requirement.

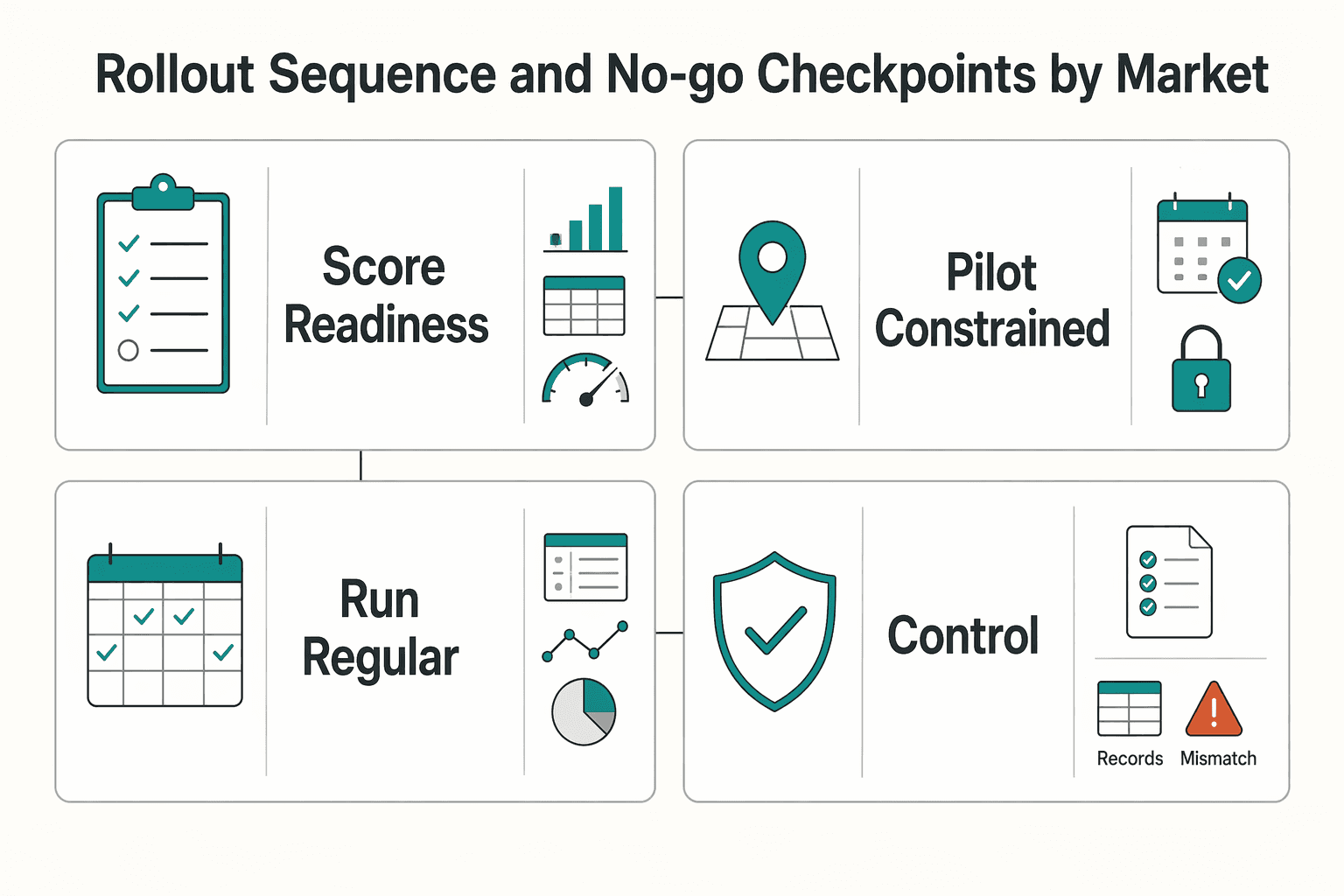

Rollout sequence and no-go checkpoints by market#

After the control layer is stable, roll out in phases, not all at once. Treat each market expansion as a governance and data-readiness decision first, then an execution decision.

- Score readiness before committing a market

Use a simple scorecard to test whether your operating model and data are ready to support reliable posting, reporting, and investigations. The real gate is usually governance and data quality: clear accountability, a defined reporting hierarchy, and a central system for vendor information.

- Pilot a constrained cohort with explicit pass/fail criteria

Start with a phased cohort focused on critical and higher-risk vendors rather than a broad launch. Define decision statements, testable hypotheses, and measurable checkpoints before the first live transactions so execution is evaluated against a written pass-or-fail view.

- Run regular operational checkpoint reviews

Review the same checkpoints on a regular cadence with owner, age, and next action visible for open items. Keep the evidence pack consistent across teams so exceptions and investigations are tracked from one shared record instead of fragmented handoffs.

- Apply a no-go rule when control pressure worsens

Do not expand scope while reconciliation exceptions, unresolved investigations, or data-quality gaps are trending in the wrong direction. Escalate it as a risk item, fix ownership and data gaps, and resume expansion only after the operating evidence stabilizes.

Conclusion#

A workable 2026 strategy is not adding every rail. It is choosing the disbursement model that fits each market segment, then proving it operationally before you expand. Check use fell to 26% from 33%. Yet only about 22% of companies report that most eligible B2B payments are digital, which suggests that more options alone do not guarantee broader digital adoption.

Pick two models that fit the segment#

Start with a shortlist, not a menu: one model for routine payouts and one for exception cases. Make that choice by vertical context, country mix, and the accounting burden your team must carry after funds move.

The demand to reassess is real but uneven. One cited source reports 76% of organizations expect to update payment strategy within three years, while broader digital adoption still appears stalled. In practice, expansion can slow when remittance handling, approval evidence, and posting logic remain partly manual.

Require proof in the records, not just in the payout screen#

A pilot is useful only if it produces audit-ready visibility. The key check is whether payouts flow into your accounting layer with records updated automatically, rather than waiting for manual matching. One concrete example in the source material is direct transaction sync into Xero and Zoho Books.

If you pay independent contractors, include a tax-reporting checkpoint, including readiness for Form 1099-NEC preparation. A clean front-end payment flow is not enough if contractor data and remittance records fail when reporting season arrives.

Scale only when the pilot stays boring#

Do not scale on speed alone. Scale on consistency under load. Run a constrained cohort and watch for signs that manual work is returning: spreadsheet cleanup, missing remittance detail, or accounting records that need repair.

One grounded warning matters here: operational complexity rises sharply during reporting and reconciliation periods. In the cited source example, bulk flows replace pay-one-by-one execution, but higher throughput can still expose weak processes faster. If manual matching returns as volume grows, fix the evidence trail before adding coverage.

The takeaway is simple: expansion decisions should be won with repeatable operational proof, not rail count. Build a two-model shortlist, run a constrained pilot, and move forward only when reconciliation, controls, and accounting outputs remain stable without rescue work. If you are narrowing to two rails and need coverage validation by market, review Gruv Payouts for compliance-gated disbursement workflows.

Frequently Asked Questions

What are the top B2B payment trends in 2026?

The clearest direction is faster, more transparent payment experiences, more embedded payment flows, and more automation inside finance operations. Another shift is strategic posture: payments are increasingly treated as a business priority, with one cited source reporting 67% of merchants and 78% of digital leaders viewing payments that way. Public coverage signals direction, but it does not provide complete 2026 adoption rates by rail.

Why are platforms rethinking contractor and vendor disbursements now?

Because the hard part is often not moving funds, but controlling the workflow around identity checks, payment collection, and clean book updates. As platforms handle onboarding, cross-border payments, and vendor disbursements in one stack, control gaps become more visible. That is why disbursement redesign is increasingly an operations decision, not just a rail decision.

Is real-time payment enough to modernize disbursements?

Not by itself. Faster movement helps only when controls, reconciliation, and posting logic are reliable. If records and book updates do not consistently tie out, speed may increase exceptions instead of reducing them.

What are the biggest blockers to modernization?

Common blockers are manual or siloed control points and the added complexity that can come with expanded provider coverage. This risk grows in orchestration and multi-processor setups, where reach and flexibility can improve alongside complexity. The core test is whether you can securely monitor and audit each financial interaction across your operating workflow.

How should payment methods be chosen by vendor type?

Current public excerpts do not provide a definitive vendor-type method matrix. A practical approach is to choose methods based on control coverage, compliance needs, and reconciliation reliability rather than rail momentum alone. If a segment repeatedly creates posting or reconciliation issues, tighten method and controls before expanding volume.

Which systems matter most for scale?

The evidence here supports prioritizing integration quality over any single system name. Verify that payment events carry usable invoice references and can be reconciled cleanly in your books. A practical completion check is straightforward: invoice sent, payment collected, and books updated.

What should you verify before scaling a new provider or rail?

Verify an auditable evidence trail, not just a successful demo. You should be able to trace payment events from collection through book updates and reconciliation in operations. That check matters even more in multi-processor models, where one cited source describes merchants averaging four processors per merchant.

What is still unknown in current public trend coverage?

Public reporting is useful for spotting themes but thinner on market-by-market and segment-by-segment operating proof. Before you scale, ask partners for operating evidence on exception rates, posting accuracy, and investigation handling. If your weak point is vendor master data, start with Vendor Data Management: How Platforms Keep Contractor Payment Details Accurate and Compliant.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 5 external sources outside the trusted-domain allowlist.

- legislature.vermont.gov/assets/Legislative-Reports/ADS-2026-Annual-R...trusted

- sec.gov/Archives/edgar/data/806968/00016282802601965...trusted

- sec.gov/Archives/edgar/data/0001845815/0001104659260...trusted

- aciworldwide.com/wp-content/uploads/2022/04/Prime-Time-for-Re...external

- bain.com/insights/embedded-financeexternal

- europeanpaymentscouncil.eu/sites/default/files/inline-files/B2B%20Payme...external

- fintechwrapup.com/p/payments-as-strategic-advantage-theexternal

- fortispay.com/category/blog/paymentsexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Platforms Keep Contractor Payment Details Accurate and Compliant

Reliable contractor payouts start with controlled vendor data, not the payout click. What looks like a payout failure is often an upstream record problem, and ACH return codes like `R03` and `R04` only make that visible once a payment is processed.

Gig Economy 2026: Payment Volume Trends, Payout Rail Readiness, and Platform Consolidation

Treat **gig economy 2026 payment volume trends** as an execution question, not a headline-growth story. Some inputs are measurable now, including platform counts, payout-rail behavior, and jurisdiction-specific compliance requirements. What remains uncertain is any single, verified global gig payment volume number for 2026.

Choosing Global Contractor Payment Rails in 2026 Without False Precision

This article is about payout rails for an international contractor program, not transport infrastructure. The real decision is which markets to open first after you price total payment friction, not just the headline transfer fee.