Quick Answer

Choose by worker type and control reality: use EOR when hiring a Full-time Employee without a local Legal Entity, use AOR for a true Independent Contractor model, and treat Direct Contracting as high risk when day-to-day supervision resembles employment. For AOR vs EOR platforms, the deciding factors are contract scope, country fit under Labor Law, and clear ownership for incidents before launch.

How These Models Change Compliance Ownership#

Choosing between Agent of Record, Employer of Record, and Direct Contracting is not only a procurement decision. It is also a compliance-risk and controls decision for teams trying to grow across markets without avoidable exposure.

That framing matters because the labels are easy to confuse, and the cost of getting them wrong is real. One source warns that confusing AOR and EOR can create compliance risk and operational inefficiency, and another warns compliance miscues can lead to fines and penalties. In practice, the question is not which model looks simplest in a vendor demo. It is which model aligns with worker type and your compliance processes.

For orientation, an Agent of Record, or AOR, is a third party that mainly manages independent contractors, freelancers, and consultants for a business. An Employer of Record, or EOR, is another model used to manage a global workforce. Direct Contracting is included here as a separate path to compare alongside AOR and EOR. The real question is where misclassification risk can appear and what your team must verify before launch.

The scope here is deliberately narrow and sober. Global workforce expansion brings local labor law, tax regulation, and local employment practice issues. So no model should be treated as universally compliant, and no provider label should be treated as proof that a setup is defensible.

Before onboarding, validate the country, worker type, and contract path together. Confirm your internal compliance review steps and who is accountable for them.

The main failure mode is assuming the commercial model name answers the compliance question by itself. It does not. Worker misclassification can still arise if a contractor is treated like an employee in practice. If your launch spans more than one market, treat each market as a separate compliance check.

By the end, you should have a practical way to evaluate AOR, EOR, and Direct Contracting through a controls lens rather than a feature checklist. You will leave with a decision matrix, clear escalation triggers for legal and risk review, and a reporting checklist your team can apply this quarter.

For a step-by-step walkthrough, see Choosing a Defensible SAR Filing Model for Payment Platforms.

AOR EOR and Direct Contracting at a glance#

Use worker type and legal-employer setup as your first filter, not feature lists. If you are hiring a Full-time Employee without setting up a local Legal Entity, EOR is usually the default starting point. If the engagement is truly Independent Contractor-led, AOR is often fit-for-purpose for contractor compliance and invoicing support.

| Criteria | Agent of Record (AOR) | Employer of Record (EOR) | Direct Contracting |

|---|---|---|---|

| Worker type fit | Independent Contractor | Full-time Employee | Varies by your engagement model |

| Legal employer status | Does not act as legal employer; supports contractor compliance and invoicing | Acts as legal employer on behalf of the client company | No provider acts as legal employer for you |

| Need for your local Legal Entity | Commonly used for international contractors; confirm by country and contract | Commonly used when hiring international employees without setting up a local entity | Must be confirmed by country, worker type, and contract path |

| Worker Misclassification exposure | Can still arise if contractor reality conflicts with contractor status | Contractor misclassification is less central when the worker is engaged as an employee; employment compliance still applies | Must be assessed directly under your model and local rules |

| Payroll ownership | Supports contractor payments/invoicing rather than employee payroll | Handles employee payroll, benefits, and tax obligations | Owned by your internal process |

| Tax deductions ownership | Confirm exact responsibilities in the agreement | Included in EOR employment/tax handling scope | Owned by your internal process |

| Compliance burden | Shared with provider for contractor workflows | Shared with provider for employment administration | More responsibility remains in house |

| Operating factor | AOR | EOR | Direct Contracting |

| --- | --- | --- | --- |

| Onboarding speed | Provider- and country-dependent | Provider- and country-dependent | Process-dependent |

| Control depth | Shaped by contractor model and provider terms | Business oversight may stay with you while employment admin runs through provider | Direct control with direct responsibility |

| Required internal headcount | Depends on review/approval ownership | Depends on review/approval ownership | Depends on what you keep in house |

| Audit evidence availability | Depends on provider reporting and your retention | Depends on provider reporting and your retention | Depends on your record quality and controls |

The table is a starting filter, not a final approval. Before launch, confirm SLA terms, country coverage depth, and contract carve-outs in the provider agreement. For model-specific risk and fee mechanics, see What is the 'Withdrawal Penalty' on EOR Platforms?.

Who holds the liability when something goes wrong#

The model name alone does not determine liability. For AOR, EOR, and Direct Contracting, separate two decisions up front: potential legal exposure under local labor laws, tax regulations, and local employment practices, and operational accountability inside your team when an incident starts.

Sources frame AOR and EOR as two ways to manage a global workforce, and they also frame EOR as the option that can legally employ international talent. That difference matters, but it is still not a blanket answer for every dispute, pay issue, or tax problem. You need to verify country scope, contract terms, and how the relationship works in practice.

| Failure type | AOR | EOR | Direct Contracting |

|---|---|---|---|

| Worker Misclassification dispute | Do not assume the label settles legal exposure. Validate contractor treatment in practice and confirm what the agreement actually covers. | Legal employment status is a key difference, but dispute handling still depends on contract terms and country setup. | Treat as high risk if day-to-day control looks like an employer relationship; escalate to legal before onboarding. |

| Labor Law violation | Exposure can still depend on local rules and your operating reality, not only provider branding. | Legal-employer structure can change responsibilities, but you still need country-specific role clarity in writing. | Your company is directly in scope, so legal and compliance ownership should be explicit before launch. |

| Pay error | Confirm whether the issue is inside provider scope or your internal process. | Confirm who owns correction steps and worker/regulator communication in each country. | Internal ownership is direct; remediation and records should already be assigned. |

| Tax Deductions failure | Do not assume tax handling responsibilities without explicit contract language. | Do not assume all tax responsibility transfers by default; verify exact obligations in writing. | Define ownership at onboarding, or cleanup risk moves to your internal team later. |

Legal liability and operational accountability are different#

Legal liability is who may be answerable under law and contract. Operational accountability is who investigates, who responds, who remediates, and who records the incident internally. If you assign only one of these, incident response usually breaks under pressure.

Use one practical rule before go-live#

If your platform sets day-to-day control like an employer, treat Direct Contracting as high risk and escalate to legal before onboarding. Use that rule early, not after a complaint.

If you want one operating baseline, use this: EOR can change how employment is structured, but it does not remove the need to verify responsibilities and incident ownership by country and contract. AOR and direct contracting need tighter control checks whenever the working reality starts to resemble employment.

When Direct Contracting is efficient and when it is a trap#

Direct Contracting is efficient when contractor status is genuinely defensible and you can show that your setup was compliant from the start. It becomes a trap when you scale across regions without that discipline, because misclassification, tax, and permanent establishment (PE) risk can increase quickly, and delayed fixes are usually far more expensive.

| Checkpoint | Direct Contracting can work when | Escalate out of Direct Contracting when |

|---|---|---|

| Contractor-status defensibility | The role and working model can be defended as true contractor engagement. | Day-to-day control starts to look like an employment relationship in practice. |

| Cross-region expansion risk | You are not expanding faster than your compliance review can support. | You are hiring contractors across multiple regions without a clear, documented review, especially if a US company may face misclassification, tax, or PE risk. |

| Governance quality | Your compliance and governance safeguards are clear before disputes happen. | Safeguards are thin, unclear, or dependent on a non-professional setup that may not protect your interests in a dispute. |

The practical rule is simple: if the role is business-critical and ongoing, do not keep it on Direct Contracting without written legal review. Keep that review tied to the jurisdiction and actual role facts so you are not defending assumptions later. The common failure mode is drift: the work starts as contractor work, then becomes embedded capacity while governance stays unchanged.

Once you know when Direct Contracting works, the next step is choosing the right mix across your workforce and markets. We covered that in more detail in Choosing ERP Sync Patterns for Payment Platforms.

How to choose by workforce mix and market footprint#

If your workforce is mixed, segment by cohort instead of forcing one model across everyone. In practice, use AOR for Independent Contractor cohorts and EOR for employee hires in countries where you do not have a Legal Entity.

| Scenario | Better fit | Why it fits | Verify first |

|---|---|---|---|

| Contractor-heavy creator platform | AOR | AOR does not employ your in-house staff and is typically used for contractor populations. | Confirm the work is truly contractor-led and your contract/evidence records are complete. |

| Employee-heavy regional launch | EOR | EOR is the legal employer for international employees and handles payroll and benefits administration. | Confirm you have no local Legal Entity and that employee onboarding/pay/benefits ownership is clear. |

| Mixed marketplace with sellers plus internal teams | Split model | Mixed contractor-and-employee populations become complicated quickly, especially across countries where you lack an entity. | Segment by role type and jurisdiction before launch. |

Where one-model plans break#

Single-model plans usually break when external earning cohorts and internal operating staff are treated as the same legal/workforce case. Independent Contractor groups may fit AOR, while employee roles usually point to EOR where no entity exists. Blending both under one approach increases classification confusion and weakens your audit trail.

Reassessment triggers that should prompt a review#

Reassess immediately when contractor roles become manager-led, follow employee-style direction, or shift into long-duration core capacity. That kind of employer-like control is a misclassification warning sign, and some cited cases have ended in millions in settlements.

Keep the decision documentary, not verbal: store role rationale, contract type, supervision model, and jurisdiction review in one evidence pack for each cohort.

Choosing the model is only half the job. The other half is running onboarding, payout, and records in a controlled sequence. Related: How EOR Platforms Use FX Spreads to Make Money.

The operating sequence from onboarding to payout to audit trail#

After you choose the right worker model, execution order is the control point: do not mark someone payable until classification, screening, contract, and tax-profile states are complete and traceable in one record.

| Stage | Decision gate | Evidence to retain | Common failure |

|---|---|---|---|

| Pre-onboarding | Is this person being treated as a contractor or employee for a documented reason? | Role rationale, jurisdiction review, approver, date | Worker type decided informally with no defensible record later |

| Screening | Has identity or business verification cleared your intake rules? | Status result, review notes, hold reason, timestamp | Profile appears onboarded, but screening is still pending or reopened |

| Contract and tax docs | Are agreement and tax records collected before first payable activity? | Signed contract version, W-8 or W-9 if your program uses them, document timestamps | Missing or stale tax profile found only when finance starts reporting prep |

| Payout setup | Is the payee actually ready to receive funds? | Payout method status, approval state, release controls | First payout fails because payee setup is incomplete |

| Exceptions and audit trail | Can you explain each hold, release, and correction later? | Exception log, approver actions, payout event record, reconciliation output | Manual fixes with no durable trail |

Treat tax collection as a release gate#

If your program depends on W-8, W-9, or Form 1099 data, collect and validate it before first payout, not at year-end scramble. Keep versioned records, a clear owner for missing documents, and a visible hold state so gaps are not bypassed operationally.

| Item | Article note | Operational handling |

|---|---|---|

| W-8 | Collect and validate before first payout if your program depends on it | Keep versioned records, a clear owner for missing documents, and a visible hold state |

| W-9 | Collect and validate before first payout if your program depends on it | Keep versioned records, a clear owner for missing documents, and a visible hold state |

| Form 1099 data | Collect and validate before first payout if your program depends on it | Do not wait for year-end scramble |

| FEIE | May apply only when the taxpayer has foreign earned income and a tax home in a foreign country; one qualification route uses a physical presence test of 330 full days in a 12-month period; claiming FEIE does not remove the need to file a U.S. return reporting that income | Use as a routing flag, not an assumption |

| FBAR | FinCEN maintains a dedicated FBAR reporting and due-date reference page | Use as a routing flag for support triage |

For U.S.-linked support workflows, FEIE and FBAR are best handled as routing flags, not assumptions. The IRS says FEIE may apply only when the taxpayer has foreign earned income and a tax home in a foreign country, and one qualification route uses a physical presence test of 330 full days in a 12-month period. The IRS also states that claiming FEIE does not remove the need to file a U.S. return reporting that income. FinCEN maintains a dedicated FBAR reporting and due-date reference page for support triage.

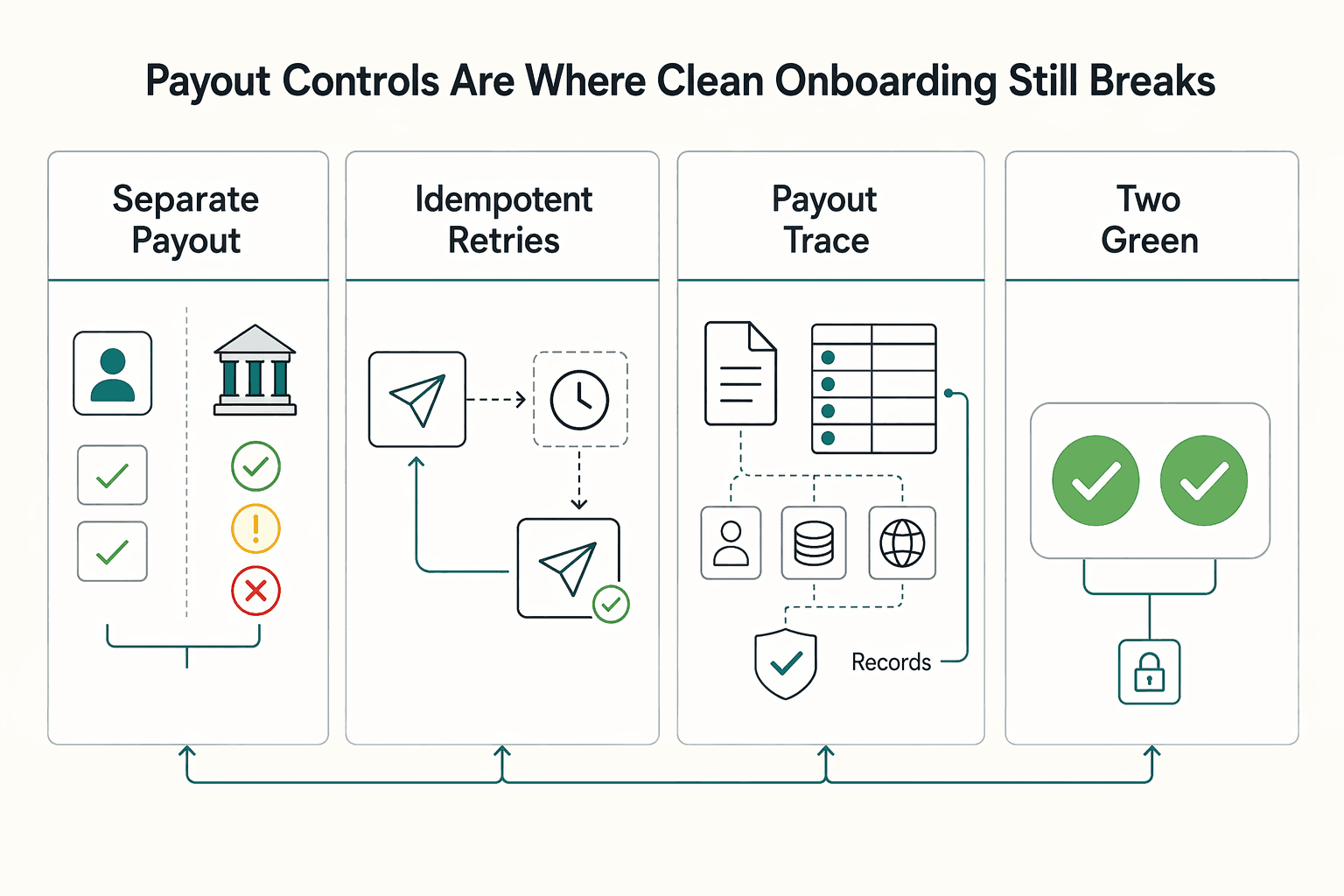

Payout controls are where clean onboarding still breaks#

Compliant onboarding can still fail at payout when AML checks, tax-profile checks, or payee setup are incomplete. Track provider payout status separately from worker onboarding status so teams can see "ready to work" versus "ready to pay."

| Control | Purpose | Article note |

|---|---|---|

| Separate payout status from onboarding status | Shows ready to work versus ready to pay | Useful when AML checks, tax-profile checks, or payee setup are incomplete |

| Idempotent retries for payout submission | Stops timeouts from creating duplicate attempts | Named as an operator control to reduce avoidable payout incidents |

| Ledger-backed payout reconciliation | Links each payout event to payee, amount, currency, and approval path | Named as an operator control to reduce avoidable payout incidents |

| Two green lights definition for onboarded | Requires both work readiness and pay readiness | Define onboarded as two green lights, not one |

Two operator controls reduce avoidable payout incidents. Use idempotent retries for payout submission so timeouts do not create duplicate attempts, and reconcile each payout event to a ledger-backed record with payee, amount, currency, and approval path. Define "onboarded" as two green lights, not one.

Roll these records into a monthly pack that compliance and finance can actually review. Related reading: Freemium vs. Free Trial vs. Reverse Trial: Which Acquisition Model Works for Payment Platforms.

The reporting checklist compliance and finance should run every month#

Your monthly pack should prove decisions and exceptions with evidence, not just summarize activity. Treat it as a liability file: under an AOR model, you may still carry final legal responsibility for misclassification, while under an EOR model the provider is the legal employer for full-time employees and manages payroll, benefits, taxes, and compliance.

Keep the pack small but strict. For each open or changed item, show the owner, decision date, current status, and the record that supports it.

| Pack section | What to include | Primary owner | Why it matters |

|---|---|---|---|

| Classification decisions | New contractor vs employee decisions, rationale, approver, jurisdiction, effective date | Compliance or legal | AOR scope is contractor administration, and misclassification risk may still sit with your entity |

| Unresolved misclassification reviews | Open cases, aging, temporary controls, next review date | Legal or risk | Open reviews can weaken your model if they remain unresolved |

| Pay and tax deduction exceptions | Compensation discrepancies, missing tax data, withholding issues, correction status | Finance or pay ops | Even when payroll/tax administration is handled by a provider, your team still needs a clear exception trail |

| Labor law change log | Market changes under review, affected roles, needed contract or process updates | Legal with operations input | Jurisdiction fit can drift after launch |

The evidence layer is the real control. Include approval logs, payout exception registers, and reconciliation exports so compliance and finance can replay what happened and verify that holds, releases, and corrections were handled in the system record.

A simple monthly check works well: exception counts and values in the narrative should tie to reconciliation for the same period, and each open classification or pay issue should have a named owner and next action date.

Set the cadence before you need it#

Use a monthly operational review plus a quarterly legal/risk checkpoint as a governance choice, not a regulator-set rule. If the same high-risk exception appears in consecutive monthly packs, escalate the market or operating model instead of carrying it forward.

This same discipline also improves cost control by forcing faster ownership and escalation decisions. Related reading: Choosing Small Payment Institution or Authorised PI for UK Payment Platforms.

Hidden costs and escalation triggers teams miss#

The biggest cost miss is usually not the provider fee. It is choosing the wrong operating scope, then paying for duplicate controls, heavier internal review, and remediation after a mis-scoped direct contractor setup.

EOR and AOR are different lanes, not substitutes. EOR is the legal employer for workers in scope, while AOR is positioned for independent contractor engagement. When teams blur those scopes, they often end up running parallel processes and cleaning up avoidable classification or pay-reporting issues.

| Model or decision | Hidden cost teams miss | What to verify early | Escalate when |

|---|---|---|---|

| AOR for contractor populations | Internal legal/compliance review load can stay high where classification is unclear | Role scope, supervision pattern, contract terms, and exception ownership | Classification disputes keep recurring in one market |

| EOR for employee hiring in new markets | Parallel tooling and handoff overhead if contractor and employee lanes are run separately | Provider scope, pay/tax handoffs, and evidence trail for corrections | You are expanding without a local entity and worker scope is drifting |

| Direct Contracting in-house | Remediation exposure if scope is wrong, including penalties, back taxes, and legal issues | Tax-document completeness and documented classification rationale before onboarding | Tax-document gaps remain unresolved or worker control starts looking employment-like |

Where cost creeps in#

AOR and EOR can reduce burden, but they do not remove internal accountability. Employment laws, tax requirements, and classification rules vary by location, so your team still needs clear exception handling, ownership, and records.

Entity planning is another common blind spot. If you skip EOR and plan direct employee hiring, local entity setup can take several months and involve significant setup expense, which can become a launch risk on its own.

When to stop and escalate#

Trigger specialist legal or tax review when any of these appear: new market entry without a local entity plan, repeated classification disputes, or unresolved tax-document gaps affecting clean reporting or pay operations.

| Trigger | Response | Article note |

|---|---|---|

| New market entry without a local entity plan | Trigger specialist legal or tax review | Listed among the cases that should trigger review |

| Repeated classification disputes | Trigger specialist legal or tax review | Listed among the cases that should trigger review |

| Unresolved tax-document gaps affecting clean reporting or pay operations | Trigger specialist legal or tax review | Listed among the cases that should trigger review |

| Two consecutive reporting cycles with unresolved high-risk exceptions | Pause expansion in that jurisdiction | Wait until ownership, controls, and evidence are back in line |

Use a strict internal governance rule: if two consecutive reporting cycles still show unresolved high-risk exceptions, pause expansion in that jurisdiction until ownership, controls, and evidence are back in line. A model label alone is not a defense if execution is weak.

Conclusion#

The durable decision rule is simple: pick the model that matches your operational control and compliance responsibilities, not the one with the nicest vendor demo. Agent of Record, or AOR, is framed around managing independent contractors for compliance and invoicing, while Employer of Record, or EOR, legally employs workers on your behalf and handles employee pay, benefits, and tax obligations. If you are hiring international employees and want to avoid setting up a local legal entity, EOR is often a cleaner starting point. If you are engaging international contractors, AOR is the more natural fit.

That also means you should stop treating these as mutually exclusive choices. A blended approach can be the more realistic answer for platforms with mixed worker populations. Use one model for contractor cohorts and another for employee hires where your entity footprint does not support direct employment. The wrong move is forcing a single model across every jurisdiction and worker type just because procurement wants fewer vendors.

Your next step should be operational, not theoretical. Apply the at-a-glance matrix to your current populations, then test whether your controls actually support the answer it gives you. A useful checkpoint is to verify that your provider agreement says the same thing as your internal operating assumption. If the provider is positioned as managing independent contractors, confirm the contract scope reflects that. If the provider is positioned as the legal employer, confirm employee pay, benefits, and tax obligations are actually covered in the agreement and in the handoff between your team and the provider. Before you expand, lock down three basics:

- Assign each new market and worker group to one model on purpose: AOR, EOR, or Direct Contracting.

- Run a regular review cadence and document who escalates classification, pay, tax, or contract exceptions.

- Define a stop point before launch so unresolved high-risk issues do not drift into "we will fix it after onboarding."

A common failure mode is not picking the wrong acronym first. It is letting the model drift after launch. A contractor population starts being managed like staff, or an employee hire is rushed into a market where your entity, provider terms, and internal approvals do not line up. Once that happens, the problem is no longer vendor selection. It is evidence, ownership, and remediation.

Use this article as a decision aid, not as a substitute for specialist review. Market rules can change, provider terms vary, and operational constraints are rarely identical across countries. Before execution, confirm your assumptions with legal and tax specialists in the jurisdictions that matter most.

Frequently Asked Questions

Can AOR replace EOR for every international hiring case?

No. Agent of Record is positioned for independent contractor populations, while Employer of Record is for full-time employee hiring and handling payroll, benefits, and labor law compliance. If you are hiring full-time employees in a region where you do not have a legal entity, the guidance here points to EOR rather than stretching AOR beyond contractor use cases.

When does Direct Contracting become too risky to justify?

There are no fixed direct-contracting risk triggers or legal thresholds to point to. Treat this as a legal and compliance decision based on local law, contract terms, and how the work is actually structured.

Do you need a local Legal Entity for AOR or EOR?

One common rule is straightforward: use EOR for full-time hiring in regions where you lack a legal entity. AOR is framed around contractor engagement rather than full-time employment, but local validation is still required before launch.

Who is legally responsible under AOR, EOR, and Direct Contracting?

At a high level, EOR is used for full-time employee employment administration, while AOR is used to manage contractor compliance, classification, and payments. This guide does not define uniform liability boundaries across providers, contracts, or direct-contracting models, so those details still need to be checked case by case.

Can you run AOR and EOR together in one platform operating model?

Yes. At least one framework presents AOR and EOR as complementary rather than mutually exclusive, which can fit mixed workforces. If you combine them, keep worker-type boundaries explicit from the start.

What records should finance keep to be audit-ready across markets?

This guide does not specify a required finance record set for audit readiness. Define the record standard with finance, legal, and your provider agreements for each market.

When should compliance or legal intervene before a new country launch?

Bring them in before launch when you are hiring full-time employees without a local legal entity, or when worker type is unclear between contractor and employee models. Additional escalation thresholds are not defined in this grounding and should be set with legal/compliance per market.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- academia.edu/64999604/Dictionary_of_Acronyms_and_Technica...trusted

- aqmd.gov/docs/default-source/rule-book/Proposed-Rules...trusted

- commerce.alaska.gov/web/Portals/18/pub/Events/Public%20Hearings/...trusted

- congress.gov/119/crec/2026/03/11/172/45/CREC-2026-03-11-s...trusted

- courts.michigan.gov/492df8/siteassets/publications/msc-bound-vol...trusted

- docs.cpuc.ca.gov/PublishedDocs/SupDoc/A2505009/9084/603941257...trusted

- energy.gov/sites/default/files/2022-10/Dual_Challenge-V...trusted

- faa.gov/air_traffic/publications/media/PCG_Bsc_w_Chg...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

What Is the Withdrawal Penalty on EOR Platforms?

For buyers, the practical question is simple: what was approved, what arrived, and how long it took. Treat that end-to-end payout result as the real cost signal, then keep enough records to reconcile it later.

How EOR Platforms Use FX Spreads to Make Money

You can control more of your payout outcome than it first appears. As the CEO of a business of one, separate unavoidable costs from avoidable ones, then manage the compliance exposure that cross-border money movement creates.

The Best Community Platforms for SaaS Businesses

Start by classifying the job. If you want access to other people's audience, ideas, or conversations, you are choosing a community to join. If you want a place your customers or members use under your brand, with your rules and structure, you are choosing software you will need to operate every week.