Quick Answer

Choose an EOR when you need a legal employer in a country where you do not have a registered entity, and choose a PEO when your own entity already exists and you want co-employment support. In eor vs peo decisions, the key checkpoint is contract allocation: verify who signs employment terms, who runs payroll and benefits locally, and where compliance liability sits before you commit.

For a global independent professional, structure is a strategic choice, not just back-office admin. The question is not which HR label sounds better. It is which model protects your autonomy, allocates risk clearly, and lets you work across borders without unnecessary complexity.

This guide keeps the focus on that decision. The throughline is simple: choose the model that fits your legal setup, the country where the work happens, and the level of compliance responsibility you want to carry.

Start with the core difference between EOR and PEO#

Start with the distinction that drives the whole decision: whether you already have a registered legal entity in the country where the work will happen.

- What is an Employer of Record (EOR)? An Employer of Record is a compliance partner that becomes your legal employer in a country where you do not have your own company registered. You find the client and do the work, but the EOR handles payroll, local taxes, benefits, and local labor-law administration on your behalf. It is the employer on paper, while you keep control of the client relationship and the actual work.

- What is a Professional Employer Organization (PEO)? A Professional Employer Organization works through co-employment. It partners with your existing, registered business entity to share certain employer responsibilities. The PEO may handle payroll, benefits, and HR administration, but you and your company still remain legally involved and share that risk.

- The critical distinction. The decision turns on one question: Do you already have your own registered legal entity in the country where you will be working? If the answer is no, as it is for most independent global professionals, an EOR is the compliant option. If the answer is yes, a PEO becomes possible, though it is often less practical for a borderless working model.

A quick comparison#

| Vector | Employer of Record (EOR) | Professional Employer Organization (PEO) |

|---|---|---|

| Legal Entity Requirement | None. The EOR provides the legal entity. | You must have your own registered business entity in-country. |

| Employment Status | The EOR is the sole legal employer of record. | Co-employment model; you and the PEO share employer status. |

| Liability | The EOR assumes nearly all legal and HR-related liability. | Liability is shared between your company and the PEO. |

| Ideal Use Case | Engaging clients in new countries without the cost of setting up a local company. | Managing HR for an established local business serving clients in that same country. |

| Global Scalability | High. A single EOR partner can help you work in many countries smoothly. | Low. Requires a new entity and provider for each new market. |

Pillar 1: The Autonomy Audit - Who Is Really in Control?#

If autonomy is your first filter, start here. In many EOR arrangements, day-to-day control stays between you and your client, while a PEO can introduce more HR-policy oversight because of co-employment. The practical job is to separate work direction from employer administration, then make sure the contract keeps that line clear.

With an EOR, the provider is the legal employer for local employment administration, while day-to-day work direction usually stays on the client side. With a PEO, co-employment means responsibilities are shared, and the exact split depends on the agreement and the jurisdiction. Do not rely on labels alone.

Where control actually sits#

Use this as a screening tool, not a guarantee. Contract terms and local law decide the edge cases.

| Autonomy lever | EOR | PEO |

|---|---|---|

| Work direction | Usually stays with your client or operating business; legal employer status does not automatically transfer delivery control. | Usually stays with your business operationally, but co-employment can add HR process requirements. |

| Schedule control | Often stays client-side for assigning and scheduling tasks, subject to local attendance and leave compliance processes. | Your business usually sets schedules, but scheduling and leave processes can be shaped by the service agreement. |

| Client communication | Can remain direct between you and the client; confirm whether notices, invoicing, or conduct issues must route through the provider under your contract. | Can involve shared handling when the contract assigns HR reporting or related channels to the PEO. |

| Policy constraints | Usually lighter on project operations, heavier on statutory employment administration. | Often broader because co-employment agreements may allocate more HR policy and benefits administration to the PEO. |

| Offboarding control | Commonly influenced by client direction, with required legal and process steps under local law and contract. | More shared; offboarding often runs through both your business decision and PEO HR procedure. |

If you are reviewing a U.S. CPEO, keep one point separate from everything else. Responsibility for employment-tax filing and payment can sit with the CPEO for wages it remits. That does not automatically give it operational control over your work.

Your clause review sequence#

Do not start with price. Start with control.

| Clause area | What to review | Article note |

|---|---|---|

| Scope of authority | Limit who can instruct you, approve deliverables, bind your business, or speak on your behalf | This is where apparent-authority risk starts |

| IP assignment chain | Make sure your client agreement and provider agreement work together so ownership transfers cleanly | For U.S. copyright, transfer language should be in writing and signed |

| Exclusivity and non-compete | Narrow the language so restrictions address real conflict prevention | State-level variation still matters |

| Termination mechanics | Confirm who can trigger offboarding, how client direction is communicated, what notice applies, and what contract steps must be completed before separation is finalized | Test termination mechanics before separation is finalized |

| Dispute language | Review venue, governing law, confidentiality, and fee allocation | Arbitration clauses are often enforceable |

Review scope of authority first. Limit who can instruct you, approve deliverables, bind your business, or speak on your behalf. This is where apparent-authority risk starts.

Next, check the IP assignment chain from end to end. Your client agreement and provider agreement need to work together so ownership transfers cleanly. For U.S. copyright, transfer language should be in writing and signed.

Then narrow any exclusivity and non-compete language. Do not assume a broad federal rule solves this. State-level variation still matters. Restrictions should address real conflict prevention, not block your wider business.

After that, test termination mechanics. Confirm who can trigger offboarding, how client direction is communicated, what notice applies, and what contract steps must be completed before separation is finalized.

Finally, read the dispute language carefully. Arbitration clauses are often enforceable, so venue, governing law, confidentiality, and fee allocation all affect your practical position if something goes wrong.

How to explain it to clients#

Keep the explanation operational and direct: "I work with an EOR as my compliance and payroll partner in this country. They handle local employment administration, while I remain your direct point of contact for scope, delivery, and communication under our contract."

That framing makes the administrative structure clear without weakening your role. If a provider tries to control routine project communication outside the contract, treat that as a contract-boundary issue and resolve it before signing.

For many cross-border independents, the autonomy choice still follows entity setup. If you do not already have a local entity, an EOR is often used to separate compliance administration from day-to-day work direction. If you do have an entity and are considering a PEO, expect more shared HR administration unless the contract clearly shows otherwise. Related: A Guide to Employer of Record (EOR) Services.

Pillar 2: The Risk Assessment - Protecting You and Your Client#

Risk is easier to manage when ownership is explicit. In practice, an EOR can create a cleaner allocation for in-scope employment administration. The provider can be the legal employer for local employment administration, while you and your client still retain key commercial decisions. If you are comparing this with a PEO, treat every promise about protection as unproven until it is written into the agreement.

What the provider owns and what you still own#

Use this as the baseline split:

- The EOR can act as the legal employer and handle statutory compliance and benefits administration tasks under local law.

- Your client still owns compensation philosophy, benefits expectations, and budget.

- Assume you still own your personal tax residency position unless your contract and adviser confirm otherwise. Do not assume that local payroll and employment administration solve where you are personally taxable.

One practical warning: what works cleanly in one country may break in another. Local legal rules and expectations differ, so a benefits or HR setup that works in one jurisdiction may not translate well to the next.

Quick risk map: individual, client, provider#

| Risk area | Provider risk (EOR model) | Client risk | Your individual risk | Who is primary liable | Who handles disputes | Who carries compliance burden | What remains your responsibility |

|---|---|---|---|---|---|---|---|

| Statutory benefits and local-law administration | EOR can own statutory compliance and benefits administration it contractually accepts | Client expectations may exceed what local law allows | Service or documentation gaps can affect you directly | Contract-defined; verify by country and task | Contract-defined; set named escalation contacts | Often provider for accepted local employment-admin scope | Verify outputs, for example enrollment and records, match what was promised |

| Compensation philosophy and benefits budget | Provider executes within agreed scope | Client sets strategy, expectations, and budget | You may face misalignment if promises exceed local reality | Usually client for strategy and budget choices in this benefits context | Contract-defined commercial and legal owners | Mostly client for policy decisions, with provider execution in scope | Confirm country-level deliverability before you rely on it |

| Personal tax residency | Not established as provider-owned in these materials | Not a client-owned substitute for your filings | You remain exposed if residency or tax filings are missed | Not established as transferable here; assume you remain responsible unless advised otherwise | Your tax adviser or filing contacts | Assume you, unless confirmed otherwise in writing | Track residency and filing obligations yourself |

| PE exposure review | PE ownership and transfer are not established in these materials | Client still carries legal and tax review obligations | Your work pattern and authority may still require review | Not established in these materials; confirm via contract and country counsel | Set a written escalation path with client and provider legal contacts | Not established in these materials | Escalate early and keep conduct aligned with contract terms |

PE risk as a decision framework#

Treat PE as a review item, not a sales claim. These materials do not establish PE trigger tests, thresholds, day-count rules, or definitive liability allocation, so do not assume exposure is eliminated or transferred by default.

Use this escalation rule. If your contract structure, your client-facing role, or your day-to-day work pattern could be read as local presence, stop and require written review by the client and the provider. Any country-specific threshold or day-count rule should stay pending until it has been verified against provider, contract, and local source records before use.

A short due-diligence checklist#

Before you sign, get these points in writing:

| Checklist item | Verify in writing |

|---|---|

| Contract and termination map | Who owns filings, statutory benefits, notices, offboarding steps, and regulator responses |

| Indemnity scope | What is covered, excluded, capped, and carved out |

| Compliance support | Current compliance or regulatory checklist for the country in scope |

| Escalation process | Named owners for payroll and employment administration, legal notices, and client issues |

| Post-transition controls | If you switch providers, require a post-transition audit and define what will be monitored |

If you want a deeper dive, read What to Do If You've Been Misclassified as an Independent Contractor.

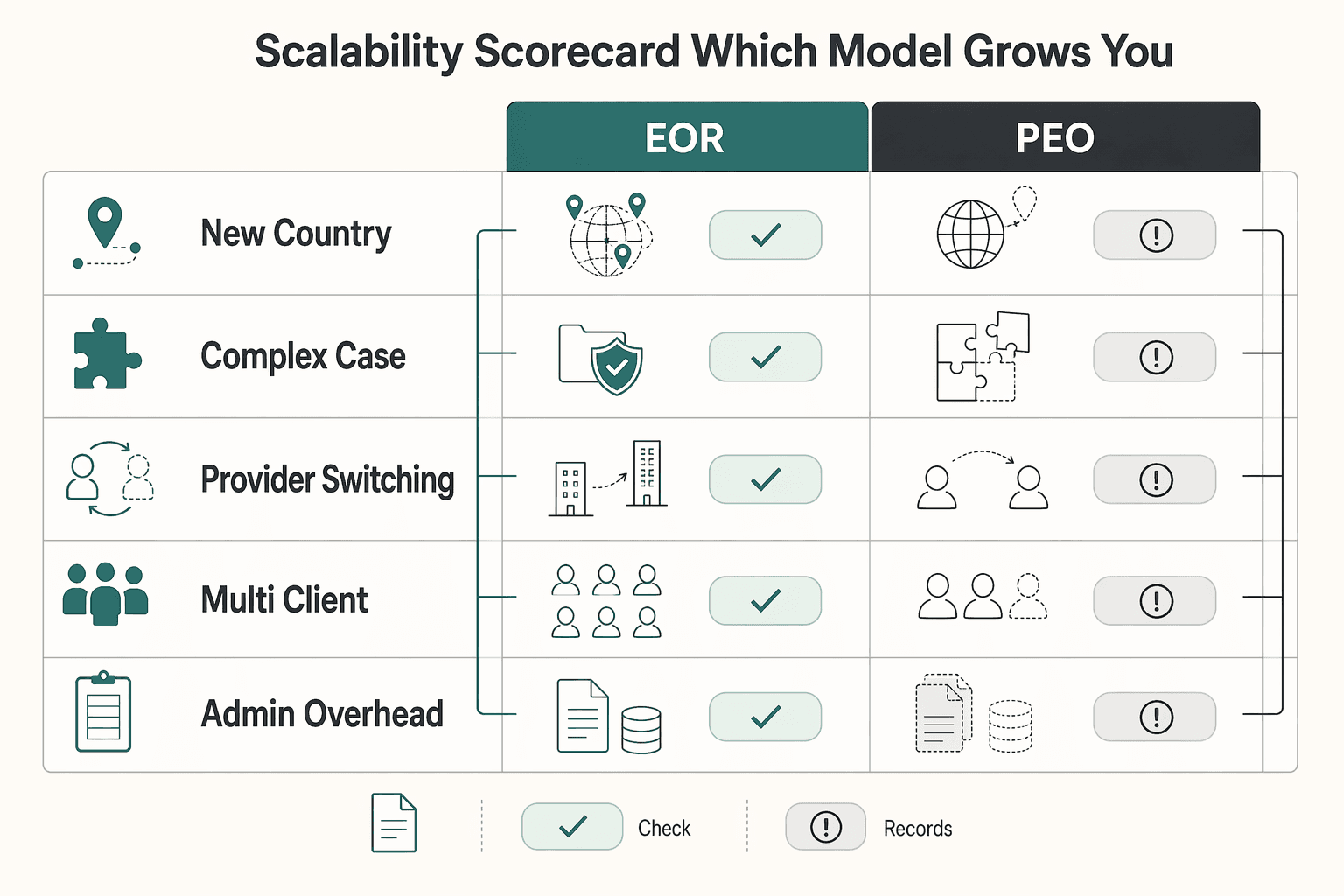

Pillar 3: The Scalability Scorecard - Which Model Grows With You?#

If your plan includes more than one jurisdiction, the support here is stronger for the EOR model. In this comparison, EOR has clear support for compliant multi-country hiring. For PEO, treat expansion assumptions as unproven until each requirement is confirmed in writing.

| Scalability point | EOR | PEO |

|---|---|---|

| New-country launch path | Built for compliant multi-country expansion; the provider can employ on your behalf while you manage day-to-day work | Not established here as a multi-country launch model; verify local prerequisites before treating it as expansion-ready |

| Entity dependency | The provider employs on your behalf; confirm how this aligns with your internal hiring and compliance ownership | Entity and registration requirements are not established here; confirm in writing |

| Provider switching friction | Review contract portability, records access, notice periods, and offboarding duties before assuming a smooth move | Friction level is not established here; verify handoff terms and data access |

| Multi-client support | Multi-country support is established; verify multi-client operating terms for each engagement | Support pattern is not established here; ask how separate engagements are handled country by country |

| Admin overhead | Provider handles payroll, tax, and benefits administration within scope; you keep daily work direction | Scope varies by provider; confirm who owns payroll, benefits, filings, and worker communications |

Setup speed is where buyers often get distracted by promises, so use a process view instead.

| Setup stage | EOR | PEO |

|---|---|---|

| 1. Confirm operating scope | Confirm country coverage and role fit | Confirm local operating prerequisites and service scope |

| 2. Define terms | Set employment terms and required payroll or benefits inputs | Define service scope and admin ownership terms |

| 3. Contract review | Review service agreement, responsibilities, and escalation path | Review responsibilities, filings, and transition terms |

| 4. Onboarding | Launch onboarding and compliance checks | Launch onboarding after prerequisites are met |

| Common delay points | Long compliance checklists, local labor requirements, inclusion demands | Delay pattern is not established here; verify by provider and country |

If procurement is part of your growth path, ask for evidence of legal and compliant hiring practices in every geography listed on the RFP. Timing and setup cost are not established in these materials, so verify ranges directly with each provider.

Scale readiness checklist#

Before you treat either option as ready for growth, verify these three points:

| Readiness point | Verify |

|---|---|

| Contract portability | Can agreements, worker records, and notices transfer cleanly if you switch providers? |

| Cross-border payroll continuity | Who owns payroll cutoffs, tax data handling, and benefits continuity during a transition? |

| Compliance handoff quality | Do you have named contacts, escalation steps, and country-level proof packs ready for clients or procurement teams? |

Match the model to your verified operating map. In this comparison, EOR is the clearer path for cross-border growth. A PEO makes sense only where its fit has been explicitly confirmed for your footprint.

You might also find this useful: Deel vs. Remote: A Comparison from the Freelancer's Perspective.

If your scorecard points to needing one compliant flow as you add countries and clients, review Gruv's freelancer Merchant of Record option.

Conclusion: Choose Your Structure, Own Your Strategy#

The core rule is simple. Choose an EOR when you need a legal employer in a country where you do not have a local entity. Choose a PEO when you already have a local entity and want co-employment HR support.

That is the real decision in EOR vs. PEO. Focus on legal-employer structure, compliance allocation, and whether your current entity setup matches the country where the work happens.

You can preserve day-to-day work control in either model, but the legal wrapper changes what follows. With an EOR, the provider is the legal employer in-country while your business keeps managerial control of the work. With a PEO, you keep ownership and operational control, but employment responsibilities are shared rather than shifted.

This is also where expensive mistakes happen. In a PEO arrangement, responsibilities and liabilities are allocated in the Client Service Agreement, so review that document line by line. If U.S. payroll is involved, do not assume tax responsibility fully transfers just because the PEO runs payroll. The IRS says the Common Law Employer generally remains responsible, with limited exceptions. If CPEO status is part of the proposal, confirm exactly which remuneration it remits.

| Decision point | EOR | PEO |

|---|---|---|

| You have no entity in the hiring country | Usually the fit | Not the fit |

| In-country employment model | Provider is the legal employer | Co-employment model with your company |

| Compliance ownership | Typically sits with the legal employer, per contract scope | Shared and allocated by CSA |

| Expansion path | Useful when entering countries without forming entities first | Useful when you already have registered entities where hiring occurs |

If a provider cannot clearly identify the hiring entity, exact country coverage, and the contract language that allocates liability, you do not have enough to decide.

Do this next:

- Confirm your target-country setup and whether you already have a registered entity there.

- Verify liability boundaries in the contract terms, especially the CSA or equivalent allocation language.

- Choose the model that matches your structure, not the sales narrative.

For a step-by-step walkthrough, see The Best PEO Services for Small Businesses.

Before you finalize your operating model, use a quick coverage check with Gruv to confirm market and program fit for your specific setup.

Frequently Asked Questions

Can you use an Employer of Record if you are a solo professional?

Usually, yes, if you need a legal employer in a country where you do not have a local entity. In this model, the provider is the legal employer and handles employment contracts, payroll, and benefits in-country, while you still manage day-to-day work and performance. Before you sign, confirm who signs the contract, the exact hiring country, and whether payroll and benefits are actually executed there.

Is a PEO ever the right choice for one person?

It can be, if your company already exists in the country and you want HR administration rather than a legal-employer setup. In a PEO co-employment arrangement, you remain the legal employer and still carry compliance liability. Verify your entity prerequisites, confirm jurisdiction fit, and treat cross-border use as unproven unless the provider confirms it in writing.

Which model works better if you move between countries or plan to expand?

EOR is usually the better fit when you need to operate without opening a local entity in each country. PEO fits when you already have and want to use local entities. Before you sign, ask for a current country-by-country capability list, including payroll coverage and where payroll and benefits are executed. | Situation | Better initial fit | | --- | --- | | Solo professional, no local entity | EOR | | Company with existing local entity | PEO | | Multi-country payroll needs | EOR (verify exact country coverage) |

Does using an EOR change your personal tax residency?

The grounding here does not establish personal tax residency outcomes. Treat personal tax residency as a separate issue from payroll administration, and make sure the agreement states which payroll tax filings the provider handles and which questions remain yours.

Who carries compliance risk if something goes wrong?

In this comparison, EOR is described as taking on compliance risk as legal employer, while with PEO your company still carries compliance liability. That affects your exposure, client conversations, and contract risk allocation. Read the service agreement for exact risk scope, escalation ownership, and carve-outs.

Can you still work with multiple clients?

Possibly, but do not assume this from the EOR or PEO label alone. Your operating freedom depends on contract terms and provider process boundaries. Review exclusivity, non-compete, conflict, and approval clauses, and ask whether separate documentation is required for each client relationship.

What should you verify before picking a provider?

Verify the core checkpoints in writing: who is the legal employer, whether a local entity is required, who signs employment contracts, who executes payroll and benefits in-country, who carries compliance liability, and whether payroll can be managed across every country you need. If you are considering a PEO, confirm jurisdiction fit before signing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ecfr.gov/current/title-26/chapter-I/subchapter-C/part...trusted

- ftc.gov/legal-library/browse/rules/noncompete-ruletrusted

- irs.gov/government-entities/third-party-payer-arrang...trusted

- irs.gov/tax-professionals/certified-professional-emp...trusted

- law.cornell.edu/wex/apparent_authoritytrusted

- law.cornell.edu/uscode/text/9/2trusted

- nlrb.gov/about-nlrb/what-we-do/the-standard-for-deter...trusted

- nrc.gov/docs/ML0405/ML040570023.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

What to Do If You've Been Misclassified as an Independent Contractor

Treat this as a protection problem first, not a label debate. If your work was treated as an independent contractor arrangement even though the relationship functioned differently, your first goal is to protect pay, rights, and records while you choose the least risky escalation path. You can do that without making accusations on day one, which often keeps communication open while you document what happened.

When to Use an Employer of Record for International Hiring

An Employer of Record lets you hire in another country through a third party, without setting up your own local entity first. The provider handles key compliance mechanics, but it does not hand off every employment risk.

Deel vs Remote for Freelancers Who Need a Clear First-Payout Decision

Choose the platform that makes your first payout cycle predictable and your contracts easier to defend. This is an operating decision, not a brand contest.