Quick Answer

Start by making W-8 collection a payout gate: route foreign individuals to Form W-8BEN, route foreign entities to Form W-8BEN-E, and hold any record with conflicting profile facts. For W-8BEN platform compliance, tie each approval, hold, or escalation to retained evidence so reviewers can explain the decision later. When valid documentation is missing, treat release as blocked because the article flags potential default 30% withholding exposure on certain payments.

Why W-8BEN and W-8BEN-E Matter for Contractor Payouts#

W-8BEN platform compliance is a pre-payout control, not a paperwork exercise. If you act as the withholding agent, your job is to classify the payee correctly, collect the right form before money moves, and keep enough evidence to explain why you paid, held, or escalated.

- Start with payout risk

Treat tax documentation as a release gate where U.S. withholding may apply. The practical consequence is simple: collect the form before first payment, because without a valid Form W-8BEN, 30% withholding may be required. If your process allows a first payment before documentation is valid, fix that first.

- Route by payee type

Correct routing starts with legal status. Form W-8BEN is for foreign individuals, while non-U.S. entities use Form W-8BEN-E. When this step is guessed or forced, downstream errors become more likely. Your intake data should clearly separate foreign individuals, foreign entities, and records that need a different path before payout review.

- Keep records that defend the decision

Collection alone is not enough unless you can connect the submitted form to the onboarding facts and payout decision that relied on it. A practical control is to retain W-8BEN records before payments begin. Keep the form, routing facts, and approval or hold outcome tied together so later review does not become reconstruction work.

- Design escalation into the model

This guide is for compliance, legal, finance, and risk owners who need reliable handling for standard cases and fast escalation for edge cases. Use explicit hold points and escalation triggers when facts do not align. Do not treat secondary explainers as tax advice. Verify material interpretations against official IRS instructions or other official sources, and confirm FederalRegister.gov web text against authoritative editions before using it as a control basis.

- Keep controls small but effective

A smaller control set that actually blocks bad payouts is better than a complex process built on weak classification. Start with the essentials: correct form collection before payment, durable retention, and a real stop when documentation does not support release. Optimize tooling and queue flow after those controls are working.

This pairs well with our guide on Gruv Platform Payments for Global B2B Payouts and Compliance.

How to Use This Framework#

Use this as a prioritization filter for pre-payout controls, not a maturity checklist. Put your effort where it most reduces withholding exposure and makes decisions easier to defend.

- Score for withholding risk first

Rank each control by how much it reduces release errors under U.S. withholding rules, then by how clearly the result can be defended in review. If a control fails, ask whether it could push you into a default withholding position such as 30%, or miss a fact pattern that needs specialist handling, such as a Section 1446(f) case with 10% withholding exposure. Tie each score to evidence: the submitted form, routing facts, reviewer outcome, and checklist version used.

- Apply it only to pre-payout form routing

Use this framework only where you must route Form W-8BEN and Form W-8BEN-E before payout release. Keep routing separate from deeper validation so foreign individuals do not get sent through an entity path, and foreign entities are not reviewed as individuals. Wrong routing can produce invalid-form outcomes, trigger maximum automatic withholding in payment logic, and create avoidable payee disputes.

- Use an explainability check

Treat this as an internal operating rule, not an IRS requirement. If your team cannot clearly explain routing, validation, and escalation on one live record, fix core controls before adding more tooling. The test is simple: show the collected form, why that form family was selected, and why payout was approved, held, or escalated. If that explanation depends on tribal knowledge or scattered notes, your audit defense is weak.

Related: GDPR for Marketplace Platforms: How to Handle Contractor and Seller Personal Data Compliantly.

Control Comparison Matrix#

Use this matrix to gate payout decisions, not to classify forms. Auto-approve only when the record is complete, internally consistent, and supported by your internal checklist. Where guidance is absent, hold or escalate.

| Control | Owner | Best-fit volume | Key Internal Revenue Code anchor | Failure mode | Evidence artifact | Escalation trigger | Minimum viable now | Mature state | Decision |

|---|---|---|---|---|---|---|---|---|---|

| Form W-8BEN routing and completeness | Compliance ops | Core individual lane | Confirm with the relevant authority beyond general withholding context | Record is incomplete or facts conflict | Submitted W-8BEN and internal review record | Reviewer cannot explain approval clearly, or key facts conflict | Require completeness before payout; hold on mismatch | Structured intake and consistent rule-assisted review for clean records | Auto-approve only when your internal checklist is satisfied; otherwise hold or escalate |

| Form W-8BEN-E status capture and validity control | Compliance ops with tax reviewer backup | Core entity lane | Chapter 3 and Chapter 4 (FATCA) status declaration | No valid W-8BEN-E on file can require default 30% withholding on certain payments; incorrect or missing forms increase operational burden | Valid W-8BEN-E on file, Chapter 3 and 4 status selections, reviewer or rule outcome | Entity status is unclear, submission is incomplete, or status cannot be resolved | Require a valid W-8BEN-E before covered payouts and hold inconsistent files | Rule-based entity review with status capture and evidence retention on one record | Auto-approve only when form validity and status alignment are clear; otherwise hold or escalate |

| Form W-8ECI exception handling | Tax or legal reviewer | Exception lane | Effectively connected income withholding-exemption claim | ECI claim is processed as a standard foreign-status case without specialist review | Submitted W-8ECI and specialist disposition note | Any ECI claim in the file | Hold all W-8ECI records for manual review before payout | Written specialist criteria tied to payout gating, with retained rationale | Escalate |

| Form W-8IMY edge-case capture | Tax or legal reviewer | Exception lane | Confirm with the relevant authority (QI agreement is referenced, but W-8IMY criteria require separate verification) | Confirm with the relevant authority | Confirm with the relevant authority | Confirm with the relevant authority | Define handling in specialist policy outside this matrix | Dedicated specialist path with explicit ownership and written criteria defined internally | Not set here |

Keep two operating checks in place. First, prioritize W-8BEN-E controls early because missing valid form coverage can force default 30% withholding on certain payments. Second, keep W-8ECI visible as an exception lane, and treat W-8IMY routing, evidence, and escalation criteria as requiring separate internal definition.

If you want a deeper dive, read FATCA Compliance for Marketplace Platforms: Identifying and Reporting Foreign Account Holders.

Control 1: Payee Classification and Form Routing Gate#

This gate should classify payees before payout release, based on retained profile facts, not on whichever form was uploaded first. Keep your routing logic for Form W-8BEN, Form W-8BEN-E, Form W-9, Form W-8ECI, and Form W-8IMY explicit in internal policy. Specific W-8/W-9 routing rules are not established here on their own.

Start with profile facts, then route#

Capture legal status, tax residence, and whether the payee is acting as a beneficial owner or in a more complex capacity before document review. If those facts conflict with the submitted form, consider holding the record for documented review instead of forcing a match to clear the queue.

Use the right authority standard when building routing logic. In the IRS's own language, the Internal Revenue Bulletin is authoritative for official rulings and procedures, while issue synopses are reader aids and "may not be relied upon as authoritative interpretations."

Treat conflicts as a stop condition with evidence#

A hold only helps if the reason is preserved. Retain the exact facts that triggered the stop so a later reviewer can defend the decision. At minimum, keep the submitted form, key profile fields, reviewer notes, and the checklist version used at decision time.

Keep exception forms out of the default lane#

When facts do not clearly fit your standard beneficial-owner review path, route to an exception branch (Form W-8ECI or Form W-8IMY) instead of leaving the call to reviewer discretion in the common queue. The grounding excerpts do not establish branch requirements for those forms, so your policy needs to define that escalation path clearly.

Validate the gate with periodic sampling#

Sampling tells you whether the gate is classifying correctly or just moving volume. Review approved records on a recurring cadence and confirm routing aligns with retained profile fields, not just form completeness. This matters because Bulletin No. 2023-38 (September 18, 2023) describes a cited NPRM under which certain brokers would furnish payee statements for customers on or after 1/1/2025, with some basis reporting on or after 1/1/2026. That proposal does not prove any W-8 or W-9 routing rule, but it does raise the cost of weak upstream classification.

For a step-by-step walkthrough, see W-8BEN-E Entity Type for UK Limited Companies and Platform Controls.

Control 2: Intake Packet and Attestation Design#

If intake does not collect enough structured information up front, reviewers may have to rebuild the record from PDFs, emails, and profile fragments. That can slow decisions, increase inconsistent calls, and weaken the audit trail.

| Intake control | Required capture or branch | Cited context |

|---|---|---|

| Standardize core identity and tax-residence capture | Use one packet for foreign individuals and one for foreign entities; capture legal name, country of tax residence, treaty-claim indication, and any FTIN-related representation requested | Framed as an internal design choice for consistency |

| Gate treaty claims | If treaty benefits are claimed, require the additional treaty inputs your policy defines before the record can advance | Publication 515 says withholding agents may not accept certain treaty claims in specific suspension scenarios, including Belarus-related interest payments from December 17, 2024 through December 31, 2026, unless ended earlier |

| Bind submission to attestation evidence | Retain the timestamp, exact consent or certification text shown, and the intake version active at submission time | Relevant during filing-system transitions, including 2025 Forms 1042-S due March 15, 2026 using IRIS or FIRE, and 2026 Forms 1042-S due March 15, 2027 when IRIS is required |

| Reject incomplete treaty packets | If treaty-required fields under your policy are blank, return the packet for correction before reviewer assignment | Helps protect queue quality and leaves a defensible record if a decision is later questioned |

Publication 515 supports the direction here: it places payee identification inside Chapter 3 and Chapter 4 withholding context and includes an explicit "Identifying the Payee" topic. For a withholding agent, intake is a practical quality gate for whether a submission is reviewable.

- Standardize core identity and tax-residence capture

Use one intake packet for foreign individuals and one for foreign entities, but keep the core model aligned. Capture the same key facts in the same fields each time, for example legal name, country of tax residence, treaty-claim indication, and any FTIN-related representation your packet requests. This is an internal design choice for consistency, not an IRS-prescribed field list.

- Gate treaty claims as a required branch

If a payee claims treaty benefits, require the additional treaty inputs your policy defines before the record can advance. This helps keep unsupported or incomplete treaty claims out of the manual queue. The risk is practical: Publication 515 says withholding agents may not accept certain treaty claims in specific suspension scenarios, including Belarus-related interest payments during the stated period from December 17, 2024 through December 31, 2026, unless ended earlier.

- Bind each submission to attestation evidence

Treat timestamped attestations and versioned consent text as internal controls. Each submission should retain the timestamp, the exact consent or certification text shown, and the intake version active at submission time. That trail matters when rules change and during filing-system transitions, including 2025 Forms 1042-S due March 15, 2026, using IRIS or FIRE, and 2026 Forms 1042-S due March 15, 2027, when IRIS is required.

- Reject incomplete treaty packets before reviewer assignment

As an internal control, do not assign reviewers to records that are incomplete on their face. If treaty benefits are claimed but treaty-required fields under your policy are blank, return the packet for correction. This can add front-end friction, but it helps protect queue quality and leaves a defensible record if a decision is later questioned.

Need the full breakdown? Read How Platforms Should Collect and Validate Form W-8BEN-E for Foreign Entities.

Control 3: Validation Rules and Exception Triage#

Automation helps only when the rule is deterministic and the pass-or-fail result is explainable. If a record falls outside those rules, stop it, show the hold reason, and send it to human review with the evaluated facts.

- Write rules the way IRS instructions are written

Avoid broad checks like "valid form on file." Build rule families by document path, and encode exceptions explicitly. The 2025 Instructions for Form 1040-NR show the pattern: complete applicable Schedule OI items, treat Schedules 1 through 3 as conditional, and apply line-specific exceptions when using related instructions. They also show a wrong-form failure mode: Schedule A (Form 1040-NR) is not used with Forms 1040 or 1040-SR. If you e-file, software will generally determine which schedules are needed. A complete-looking document can still be the wrong one for the facts.

- Keep auto-approval narrow and fully documented

Limit auto-approval to records that match your written rules exactly. If required fields are missing, inconsistent, or exception flags are present, route to review instead of passing on judgment. Store the rule version, fields evaluated, per-rule outcomes, and whether approval was automated or overridden. If a decision depends on free text or interpretation-heavy evidence, it belongs in exception review.

- Escalate ambiguity early instead of force-fitting records

When intake facts suggest the submitted form may not match the payee scenario, move the record to tax or legal review instead of forcing an automated pass from partial onboarding data. The goal is early containment, not guessing from incomplete facts. Make hold reasons specific and practical, and require an evidence pack that includes the submission, triggering fields, rule outputs, reviewer notes, and final decision owner.

- Tune with measured errors, not queue pressure

Maintain rules using false accepts and false rejects by rule ID, not anecdotes or total exception volume. Use both as quality signals: false accepts indicate records passed under current rules, while false rejects indicate avoidable operational friction. Review samples of approved and rejected records on a fixed cadence, and raise the bar for rule changes so coverage does not erode.

To standardize form intake before your triage queue, use the W-8 form generator and map each field to your pass/fail rules.

Control 4: Withholding Decisions and Payout Gating#

This is where tax review becomes real. If release tooling can bypass tax-document status, your earlier controls can become advisory instead of operative.

- Status-fed payout authorization

Make payout release consume the same tax-document status object your reviewers use, not a separate ops flag or spreadsheet note. For records your workflow routes through tax-document handling, authorization should read the current state, the rule version used, and whether the outcome was automated, reviewed, or overridden. The provided IRS excerpt does not specify Form W-8BEN vs. Form W-8BEN-E routing or an automatic payout-block requirement, so treat those as internal policy decisions that need legal or tax validation.

A practical check is to sample released payouts on a fixed cadence and confirm the payout event read the same status object the reviewer saw. Releases tied to stale snapshots or manual notes can create a bypass path.

- Named hold logic for unresolved cases

When a payout falls into a withholding-sensitive path and the documentation decision is unresolved, move it into a specific hold state with a named owner. Avoid generic "documents pending" buckets. Hold reasons should clearly distinguish missing documentation, record inconsistency, and unresolved reviewer decisions so teams can escalate the right issue quickly.

Keep an evidence pack for each held payout: submitted documents, routing fields, hold reason, payout ID, reviewer notes, and final decision owner.

- Override sign-off that expires

Allow overrides, but treat them as controlled exceptions rather than convenience releases. As an internal control policy, require owner sign-off with the reason, scope, time limit, and remediation target date, and bind the override to a specific payee or payout event.

Review active overrides on a fixed cadence. Repeated overrides for the same unresolved issue can indicate a control design problem, not a one-off.

- Legal review for threshold-driven withholding rules

If gating logic depends on backup-withholding thresholds, do not implement from an Internal Revenue Bulletin synopsis alone. Internal Revenue Bulletin 2026-5 (January 26, 2026) points to REG-112829-25 (page 452) and describes proposed changes under section 3406 that account for the section 6050W(e) de minimis TPSO exception, including situations where a threshold does not apply. The proposal is framed as reflecting recent statutory changes.

Treat that as a trigger for tax or legal review before production, since IRB synopses are reader aids and may not be relied on as authoritative interpretations.

The tradeoff is straightforward: stricter gates can reduce unresolved withholding risk, but they can slow payout SLAs and increase exception volume. Make that tradeoff explicit and measure the operational cost openly.

Control 5: Re-Solicitation and Change-in-Circumstances#

Once payout gating is in place, the next risk is control drift. A correct day-one decision can become wrong when payee facts or external rules change.

| Trigger or check | What to do | Article detail |

|---|---|---|

| Meaningful profile changes | Treat changes to country, entity type, treaty claim, or beneficial-owner facts as potential re-solicitation events and route them into a named task for fresh Form W-8 review | Keep payout status aligned to that review outcome and focus on exact field mapping |

| External rule and filing-process changes | Respond to rule changes between scheduled reviews and use cutovers as re-review triggers for documentation and status-field readiness | Publication 515 points teams to IRS.gov/Pub515; examples include Belarus and Russia suspension impacts, IRIS for 2026 Forms 1042-S due March 15, 2027, and FIRE retirement for tax year 2026 and filing season 2027 |

| Old and new form lineage | Keep prior and current Form W-8 versions linked under one payee record rather than overwriting history | Preserve prior outcome, re-solicitation reason, submission timing, and updated review result |

| Cadence plus event-driven checks | Run a periodic re-solicitation cadence as a backstop and layer event-driven triggers | Use a regular control test; if changed profiles were paid without refreshed review, treat it as a control failure |

- Trigger re-solicitation on meaningful profile changes

Treat changes to country, entity type, treaty claim, or beneficial-owner facts as potential re-solicitation events, not routine profile edits. Route these changes into a named task for fresh Form W-8 review, and keep payout status aligned to that review outcome. Focus on exact field mapping, not a generic "profile updated" signal, so reviewer-used fields and payout authorization stay in sync.

- Trigger re-solicitation on external rule and filing-process changes

Re-solicitation should also respond to rule changes between scheduled reviews. Publication 515 points teams to IRS.gov/Pub515 for post-publication developments, and it includes examples where treaty treatment changes by date and jurisdiction, including Belarus and Russia suspension impacts. Operational changes matter too: IRIS must be used to e-file 2026 Forms 1042-S (due March 15, 2027), and FIRE is set to retire for tax year 2026 and filing season 2027. Treat those cutovers as re-review triggers for documentation and status-field readiness.

- Preserve lineage across old and new forms

For audit continuity, keep prior and current Form W-8 versions linked under one payee record rather than overwriting history. Reviewers need a clear timeline of what changed, when it changed, and which rule context supported each decision. Preserve enough metadata for audit continuity: prior outcome, re-solicitation reason, submission timing, and updated review result.

- Use cadence rules plus event-driven checks, then test regularly

Run a periodic re-solicitation cadence as a backstop, and layer event-driven triggers to catch higher-risk changes faster. Track completion by cohort so stalls are visible by population or workflow. Use a regular control test (for example, monthly): sample changed profiles and confirm re-solicitation was issued, replacement documentation was collected when required, and re-review occurred before payout release. If changed profiles were paid without refreshed review, treat it as a control failure.

Control 6: Audit Evidence Pack and Control Testing#

The excerpts available here are a securities filing record (Form S-4/A) and a Tax Notes page with license terms. They do not establish IRS-defined Control 6 requirements for W-8 workflows, so treat the framework below as an internal operating standard, not a legal minimum.

1. Standardize one evidence pack per decision#

Use one consistent evidence pack for every reviewed payee record so the decision trail can be reconstructed without pulling from scattered tools.

For each artifact, retain the version actually reviewed and the metadata needed to explain the outcome, for example timestamps, who acted, and what changed. Where records include immutable filing metadata (such as filing date or registration number), keep that in the audit trail as part of the checkpoint record.

2. Map each artifact to the decision it supports#

Organize records by decision point, not by generic folders. Your evidence map should show which artifact supports which documented internal conclusion.

Keep the linkage field-level where possible, so the outcome is traceable to the facts used at review time. Preserve lineage when records change, so the final file still reflects the version and context that supported the payout decision. Any IRS-mandated artifact-to-code-point mapping is not established here.

3. Test the control with a written house standard#

Use a consistent testing table and make clear that these are internal operating choices, not legal minimums. Specific IRS-mandated sample sizes, fail criteria, and remediation-owner assignments should be confirmed with a qualified adviser.

| Control objective | Test method | Sample size | Fail criteria | Remediation owner |

|---|---|---|---|---|

| Evidence completeness on released payouts | Verify the core evidence pack is complete and linked to one decision trail | Set by risk tier and volume | Any released record missing a required artifact | Compliance operations |

| Payout gating integrity | Compare review status and timing against payout release or hold timing | Set by risk tier and volume | Release before valid review, or hold without documented basis | Payments and finance |

| Escalation discipline | Review escalated cases for clear ownership and final disposition | Set by escalation volume | Missing escalation rationale, owner, or final disposition | Tax or legal owner |

| Change lineage continuity | Check re-solicited records for prior and current linkage and decision continuity | Set by change volume | Unlinked versions or payout tied to stale review context | Compliance operations |

4. Retain enough to defend the decision, and only what you can protect#

More evidence can improve defensibility, but it also increases privacy, storage, and access-control burden. Define a retention scope that proves the decision and payout outcome, then control access accordingly.

Avoid duplicate copies across chat, tickets, and shared drives when they do not add control value. Also avoid over-redaction that removes the fields needed to justify the decision. If third-party content licenses restrict uploading content to external tools, enforce that in your handling process.

We covered related operational context in Gig Worker Tax Compliance at Scale: How Platforms Handle 1099s W-8s and DAC7 for 50000+ Contractors.

Control 7: Rule-Change Governance and Ownership#

Stale rule logic can become a control failure, so treat tax-rule updates like production changes: dated, owned, tested, and tied to primary text.

1. Keep one dated rule-change register#

Use one register that records the source item, issue date, affected logic, implementation decision, owner, QA sign-off, and rollout date. A practical anchor is the Internal Revenue Bulletin issue itself: Internal Revenue Bulletin 2025-4 (January 20, 2025) includes identifiable items such as T.D. 10018, T.D. 10019, and Notice 2025-3.

If you already track older references, keep them in the same register for continuity. You need to prove which item changed your policy, when you assessed it, and what review or product logic changed. The bulletin's Finding List of Current Actions on Previously Published Items helps maintain that chain.

2. Make ownership specific by decision type#

Named owners are an internal control choice, but they make accountability testable. Define who owns the interpretive tax position, where legal review is required, who updates product flows, who implements rule logic, and who approves release quality.

Avoid generic owners like "compliance team" or "platform." If no one can identify a named approver for the rule decision and a named approver for release, you have activity, not governed change.

3. Close the loop on every dependent artifact#

A rule change is not complete until dependent artifacts are updated and recorded together. Use a closure checklist that covers reviewer scripts, substitute forms, knowledge-base and training material, and intake prompts tied to foreign-status documentation (for example, Form W-8BEN-E).

Keep the updated checklist version, revised text, training record, and approvals in one place. This prevents partial rollouts where system logic changes but reviewer behavior stays on old guidance.

4. Regression test against real edge cases before release#

Regression should use historical edge cases, not only happy-path samples. Notice 2025-3, listed in IRB 2025-4, provides transitional relief from backup withholding tax liability and associated penalties, and it references calendar year 2027, calendar year 2028, and a boundary before January 1, 2029.

When a rule depends on an external condition, test for evidence the condition occurred. In Notice 2025-3, 2028 relief ties to submitting payee name and TIN data to the IRS TIN Matching Program and receiving a response. Also keep QA anchored to primary item text, since bulletin synopses may not be relied on as authoritative interpretations.

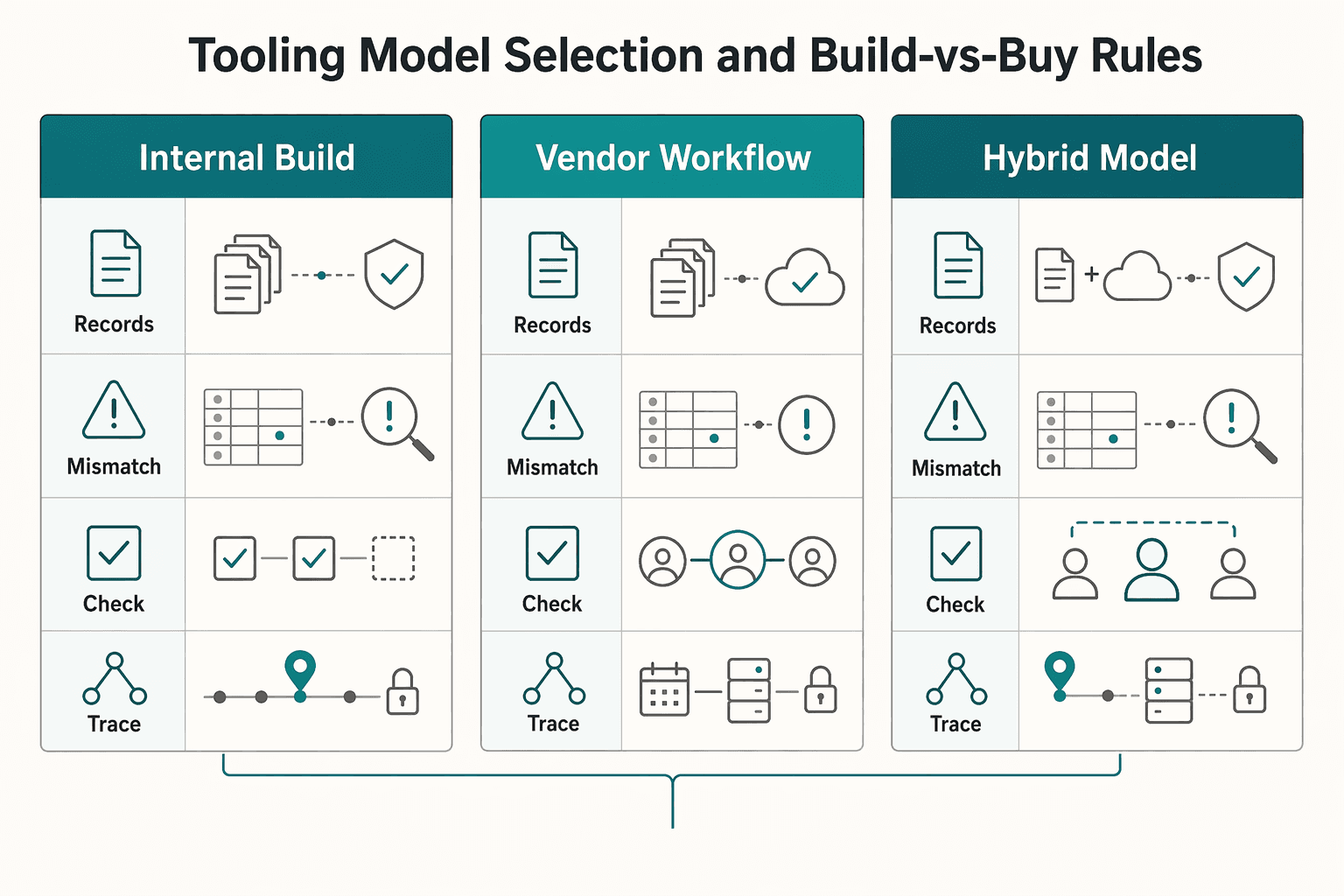

Tooling Model Selection and Build-vs-Buy Rules#

Choose the lowest-complexity model that still proves three things every time: which official text you relied on, who approved the rule decision, and what record state existed before payout decisions.

| Model | Works when | Key control point |

|---|---|---|

| Internal build | Your team can handle tax-rule changes with release-level discipline | Keep the exact source artifact used for interpretation; IRB synopses are reader aids and FederalRegister.gov XML does not provide legal or judicial notice |

| Vendor workflow | Your main gap is process consistency and audit-trail completeness | Require the underlying official item, not just a dashboard note, and keep that artifact in your change log |

| Hybrid model | You want automation for routine collection and record management, with named human owners for rule interpretation and approvals | Automate repeatable steps while keeping higher-judgment decisions reviewable and attributable |

For W-8BEN platform compliance, this section supports evidence-quality and change-control guardrails; it does not establish a complete build-vs-buy decision on feature breadth alone.

- Internal build

This works when your team can handle tax-rule changes with release-level discipline. Each rule ticket should keep the exact source artifact used for interpretation, such as the weekly Internal Revenue Bulletin item and date, or the printed PDF from the relevant Federal Register entry. Main risk: teams lean on convenience layers. IRB synopses are reader aids, and FederalRegister.gov XML does not provide legal or judicial notice.

- Vendor workflow

This works when your main gap is process consistency and audit-trail completeness. A vendor can standardize intake and record handling, but you still need source-traceability controls in your own governance. Main rule: if a vendor flags a change, require the underlying official item, not just a dashboard note. Keep that artifact in your change log, for example the printed PDF tied to Federal Register document 2023-17565.

- Hybrid model

This works when you want automation for routine collection and record management, with named human owners for rule interpretation and approvals. Main benefit: you can automate repeatable steps while keeping higher-judgment decisions reviewable and attributable.

For regulatory tracking, treat IRB synopses and FederalRegister.gov convenience formats as aids, not controlling text; verify FederalRegister.gov research against an official Federal Register edition and retain the official artifact for each change-log entry.

Common Failure Modes and Escalation Matrix#

Your escalation matrix should separate payout-document controls from taxpayer-return obligations, then route only what a first-line reviewer can actually verify before release.

Start by treating form-routing and evidence-quality issues as control failures, and send specialist-only topics through a separate branch defined by your internal policy. Keep the trigger, owner, and required evidence explicit so a second reviewer can reconstruct every hold and release decision.

Form 8938 and FBAR need a hard scope boundary in this workflow. Form 8938 is used to report specified foreign financial assets, is attached to the annual return, and is filed by that return due date, including extensions. Filing Form 8938 does not replace the FinCEN Form 114 (FBAR) requirement, and these taxpayer filings should be handled separately from payer-side W-8 documentation controls.

| Trigger | Risk level | Owner | SLA | Required evidence before payout release |

|---|---|---|---|---|

| Form 8938 or FBAR is presented as substitute support for W-8 status | Defined by internal policy | Defined by internal policy | Defined by internal policy | Valid W-8 status documentation and a note confirming Form 8938/FBAR are separate taxpayer reporting obligations |

| Form 8938 review is done without confirming taxpayer filing context and applicable threshold rules | Defined by internal policy | Defined by internal policy | Defined by internal policy | Filing context, threshold analysis, and reviewer note |

| Form 8938 is treated as complete without confirming annual-return attachment and return due-date timing (including extensions) | Defined by internal policy | Defined by internal policy | Defined by internal policy | Case record showing Form 8938 attachment to the annual return and due-date tracking |

| Form 8938 is treated as replacing FBAR review | Defined by internal policy | Defined by internal policy | Defined by internal policy | Case note confirming separate FBAR assessment where applicable |

Where Form 8938 is reviewed for context, keep thresholds and filing conditions precise in the case record: applicable thresholds depend on taxpayer context, certain specified domestic entities use the $50,000 end-of-year and $75,000 anytime tests, and Form 8938 is not required if no income tax return is required for that year.

Conclusion#

Strong W-8BEN platform compliance is an operating discipline, not a document-collection task.

- Classify correctly and collect before first payment.

Route by filer type first: Form W-8BEN is for foreign individuals, and Form W-8BEN-E is for non-U.S. entities. Then enforce pre-payment collection, because collecting before first payment is the checkpoint that helps avoid full 30% U.S. withholding. If you pay across multiple income types, confirm whether separate collection artifacts are needed instead of assuming one blanket form covers every case.

- Anchor decisions to authoritative sources, not summaries.

Use official IRS instructions and escalate complex cases to tax or legal specialists when needed. Treat vendor guides, internal summaries, and bulletin synopses as orientation, not authority. For traceability, record the exact version and date used in your rule log, since the Internal Revenue Bulletin is the Commissioner's authoritative channel for official rulings and procedures.

- Scale controls by risk and volume, but keep gating and evidence intact.

You do not need an oversized process on day one, but you do need consistent routing and validation. As volume grows, consider payout holds for missing or inconsistent documentation and keep decision evidence for exceptions.

Use the matrix to phase controls by risk and volume, then harden governance as your cross-border payout footprint grows.

Related reading: W-8BEN Controls for Platform Payouts to Foreign Contractors.

If you want to map this control model to your payout flow and market constraints, contact Gruv.

Frequently Asked Questions

Who gives Form W-8BEN, and to whom?

A foreign beneficial owner provides Form W-8BEN to the U.S. payer acting as the withholding agent when requested. For platform controls, collect the required W-8 form before first payment so tax-status checks happen inside the payout gate, not later in an exception queue.

What is the key difference between Form W-8BEN and Form W-8BEN-E?

The main distinction is filer type: Form W-8BEN is generally used for foreign individuals, while Form W-8BEN-E is for foreign entities. Do not route by name alone, because vendor guidance notes that a single-shareholder contractor LLC may still be treated as an individual for this choice. If submitted form type and legal-status records conflict, hold and review before release.

Is collecting a W-8 form enough?

No. Collecting a form alone is not a complete control. You also need validation, exception handling, payout gating, and retention of the reviewed form so decisions are auditable. A grounded example is reviewing the form, applying a treaty rate (for example, 10%) instead of a default 30%, and keeping the reviewed form on file. Invalid forms can also trigger maximum automatic withholding in platform logic.

What if valid W-8 documentation is missing at payout time?

Use a hold-and-escalate path and avoid releasing payouts based on undocumented assumptions. If the form is missing, invalid, or inconsistent with onboarding records, pause release until an authorized reviewer resolves the case and records the decision. In some setups, invalid documentation can also push the system to a higher withholding outcome.

Can software fully solve this?

No. Software improves consistency but does not replace tax or legal judgment for higher-risk exceptions or rule changes. Use automation for collection, first-pass routing, and evidence storage, then escalate edge cases for human review. That includes cases where facts may point away from a beneficial-owner certificate and toward Form W-8ECI.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- federalregister.gov/documents/2023/08/29/2023-17565/gross-procee...trusted

- federalregister.gov/documents/2023/08/29/2023-17565/gross-procee...trusted

- irs.gov/irb/2024-31_irbtrusted

- irs.gov/publications/p515trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC11799246trusted

- sec.gov/Archives/edgar/data/1824920/0001193125212364...trusted

- sec.gov/Archives/edgar/data/0001973062/0001493152260...trusted

- taxpayeradvocate.irs.gov/wp-content/uploads/2020/08/Volume-1.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

FATCA Compliance for Marketplace Platforms: Identifying and Reporting Foreign Account Holders

For marketplace teams handling cross-border payouts, FATCA work is mostly a control-design problem. You need to decide what to implement first, what evidence to keep, and what to escalate before a payout creates avoidable reporting or withholding risk. The practical question is not whether FATCA exists, but which controls actually reduce reporting errors and potential 30% withholding outcomes.

GDPR for Marketplace Platforms: How to Handle Contractor and Seller Personal Data Compliantly

Treat this as an operating decision, not a policy exercise. If you own compliance, legal, finance, or risk for a platform, your job is to decide who owns each GDPR duty. You also need to define what evidence must exist, what your team reviews on a recurring basis, and which issues need escalation before a launch or vendor change goes live.

UK Online Safety Act Compliance for Marketplace and Platform Operators

Treat the UK Online Safety Act as operating work now, not a policy debate. The most practical way to reduce uncertainty is to run an auditable implementation plan: make an initial scope call, stand up baseline controls, assign owners, and keep records you can defend if Ofcom asks questions.