Quick Answer

Start with economic guardrails, then release rewards only after value is proven. Lock CAC and LTV assumptions, pick a reward model your margin can absorb, and use a fixed sequence: signup attribution, first successful payment, optional retained-activity milestone, then payout batch after a review hold. Keep attribution rules, idempotency handling, and ledger linkage consistent across teams. If payout cost per acquired user rises while retained referred revenue falls, pause and redesign before expanding.

What teams need from a referral payout platform#

Build referral payouts like a financial product, not a growth hack. Aim for acquisition lift you can explain economically and operate reliably. Teams can copy referral tactics before they define how reward spend maps to acquisition economics and who owns payout exceptions.

Start by separating two mechanics. Referral growth uses explicit rewards to motivate existing users to bring in new users. Viral growth relies on product-native sharing and is often tracked with the viral coefficient, or K-factor. Referral programs may convert better. Viral loops may scale faster but are usually less predictable. Many companies use both.

Treat headline growth stories as directional, not as proof. Reported outcomes like Dropbox's 3,900% increase in 15 months and Hotmail's 12 million users in 18 months are useful patterns, but they are not universal benchmarks. They also do not show that incentives alone caused those results.

This guide stays focused on referral-based payment incentives for platforms. It moves in order through prerequisites, incentive design, payout architecture, controls, launch testing, recovery, and a final checklist. The goal is to help you decide whether a paid referral model fits your platform and, if it does, which reward structure you can actually support.

Set prerequisites before you design incentives#

Set your economic guardrails and operating basics before you set reward amounts. If you skip that order, you can end up with a program that is hard to attribute, hard to manage, and expensive to correct.

Step 1. Lock the baseline you will not violate#

Define your launch baseline first: economic guardrails, unit-economics assumptions, and reward budget limits. If these are still unsettled, pause incentive design until they are clear.

Also confirm product satisfaction before you scale referrals. If customers are not already willing to recommend you, incentives may not solve the underlying issue.

Step 2. Verify attribution before reward design#

Make attribution explicit before you choose reward levels. Confirm that each customer has a unique referral link and define the attribution window you will honor. If you use cookie-based tracking, document that window clearly. One source cites 30-90 days as a common range.

Run end-to-end referral tests before launch so activity is trackable without ad hoc cleanup. Fragmented tooling is a known risk because it creates a disjointed customer experience and messy data.

Step 3. Confirm payout readiness and ownership#

Confirm that your payout process can be executed and reviewed consistently. Keep ownership explicit across teams so payout decisions and disputes do not stall.

Step 4. Build the evidence pack before go-live#

Capture a pre-launch baseline for acquisition mix and referral attribution performance. Use that baseline in the first month so you adjust from signal, not instinct.

Related: How to Create a Referral Program for Your SaaS Product.

Choose the growth mechanic you are actually building#

Choose the mechanic first. Use an explicit referral program when sharing is not core to product value, and treat product-native virality as a separate model you should prove with data.

Step 1. Separate incentivized referrals from product-native sharing#

An incentivized referral is a value exchange. You pay for a completed referred outcome. A product-native viral loop is different. Users share because sharing is built into how the product delivers value.

That distinction sets realistic expectations. For many products, sharing is additive, not core, so a referral offer can lift acquisition without creating self-sustaining viral growth. A give-and-get incentive can work, but it is not a hockey-stick guarantee.

Step 2. Measure the Viral coefficient before you choose the program shape#

Use the K-factor as a decision check: K = invites per user × invite conversion rate. Calculate it consistently with the same definition of a successful outcome you use for rewards.

If K < 1, referrals are supporting growth rather than creating a self-propelling loop. As a practical benchmark, well-run referral programs are often cited at about 10-20% incremental acquisition and roughly K = 0.1 to 0.2. K > 0.5 is described as exceptionally rare. Use a simple decision rule:

- If sharing is weak, consider explicit incentives.

- If sharing is already strong, add incentives only where payout-adjusted CAC still works against your LTV assumptions.

Sanity-check the economics before you scale. If paid blended CAC is $40, a $20 + $20 structure can look cost-neutral on paper, but keep it only if referred-user quality holds.

Step 3. Choose single-sided or double-sided rewards based on friction and margin#

Pick the reward shape that fits your economics and your conversion bottleneck.

| Mechanic | Conversion lift direction | Margin pressure | Payout complexity | Best fit |

|---|---|---|---|---|

| Viral growth loop | Depends on product-native sharing strength | Low direct payout cost | Low | Sharing is part of core product value |

| Single-sided referral program | Rewards the referrer only | Lower | Lower | Tight margins or strong invitee intent |

| Double-sided referral program | Rewards both referrer and invitee | Higher | Higher | Need to add value on both sides and CAC payback still works |

Start single-sided when you need tighter cost control and simpler operations. Use double-sided only when rewarding both sides is likely to justify the added reward cost. If not, narrow eligibility or step back instead of raising incentives.

Pick an incentive structure your unit economics can survive#

Pick the simplest reward design your economics and operations can support. Add complexity only when your own data justifies it.

If you are deciding between cash, credits, discounts, and recurring rewards, treat this as a finance and operations decision first. Start with the option you can measure, reconcile, and audit cleanly with your current attribution and payout systems.

Research on referral design shows why this matters. One paper proposes multi-level revenue sharing for referral-based marketing over online social networks and reports stronger collaboration incentives in simulation than a commonly used single-level model. It also shows a complexity tradeoff: in graph-based models, Shapley-value computation is #P-hard, while in tree-based models it becomes polynomial-time. Unless you already have strong measurement discipline, start single-level before you expand reward depth.

| Incentive type | Margin impact | Operational complexity | Abuse exposure | Recommended use case |

|---|---|---|---|---|

| Cash | Program-specific; model payout cost against retained referred value | Depends on qualification, attribution, and payout controls | Depends on how strictly qualifying outcomes are verified | Use when you can clearly define and verify qualifying outcomes |

| Account credit | Program-specific; depends on redemption behavior and platform economics | Depends on eligibility and redemption rules | Depends on eligibility and redemption controls | Use when reward value is intended to stay on-platform |

| Discount | Program-specific; model impact on realized revenue and conversion quality | Depends on discount logic and redemption rules | Depends on stacking and redemption controls | Use when discounting fits your pricing model and qualification logic is clear |

| Recurring reward | Program-specific; requires explicit modeling of ongoing liability | Can require more complex tracking because payouts span multiple periods | Depends on attribution and payout-release rules | Use only when retained referred value can be measured over time |

Before you launch copy, lock the payout math for each variant: expected referred conversion, payout cost per acquired user, and payback period under conservative assumptions. Keep one shared assumption file across growth, product, and finance so the qualifying event and attribution window stay identical.

Use these decision checkpoints:

- Consider one-time rewards when you need tighter liability control, cleaner reconciliation, or retained-value assumptions are still uncertain.

- Consider recurring rewards only when value is realized over time and each payout release can be tied to retained activity or revenue.

- Test double-sided rewards as a hypothesis, not a default. If invitees already convert once they engage in your data, added invitee payouts may raise cost without clear retained-outcome gains.

Set the kill condition before launch and enforce it. Pause the variant if payout cost per acquired user rises while retained referred revenue per acquired user falls versus baseline, unless a verified tracking or pricing change explains the movement.

Before you lock reward tiers, pressure-test your payback assumptions with the pricing calculator.

Define payout triggers, holds, and release timing#

Separate qualification from cash release. If payout quality matters, avoid treating signup alone as the point where money is earned. One workable policy pattern is to track referral attribution at signup, confirm value at first successful payment, optionally add a retained-activity milestone when your economics require it, then release after your internal reversal-risk window.

| Stage | Purpose | Timing |

|---|---|---|

| Signup attribution | Track referral attribution | At signup |

| First successful payment | Confirm value | After signup attribution |

| Retained activity milestone | Validate later value when economics require it | Optional later step |

| Held state | Cover reversals, attribution disputes, duplicate-account checks, and abuse checks | After a qualifying event and before release |

| Payout release | Release approved rewards through a payout batch | After the internal review or reversal-risk window |

Step 1. Lock the trigger sequence before you write referral copy#

Set trigger events in the order they prove value. One policy pattern is signup attribution, first successful payment, retained activity milestone, then payout release.

If you run a double-sided program, define timing for each side separately. The invitee reward and referrer reward can use different trigger timing.

Use one verification test for every reward: you should be able to identify one attributable referral record, one qualifying account, and one qualifying transaction or milestone. Referral links help because they rely on direct sharing behavior and first-party data.

Step 2. Add a hold before any cash leaves the platform#

After a qualifying event, you can move the reward into a held state before release. The hold can cover your internal review period for items such as reversals, attribution disputes, duplicate-account checks, and abuse checks. Then release approved rewards through a payout batch.

Write this rule explicitly: what starts the hold, what ends it, and who can approve exceptions. Weak design and execution are common referral-program failure points, and ambiguity here can create avoidable support and finance exceptions.

Timing is a tradeoff. Faster release may strengthen extrinsic motivation. Longer delays may reduce referral momentum if the incentive already feels weak or mismatched.

Step 3. Match payout method to what you can actually support#

Document supported payout methods before launch and align messaging to real operational behavior. If you support bank payouts, define the destination types and status states your team can track end to end.

If you reference rails such as FedNow or RTP, keep settlement and availability language conditional on your actual provider setup and market coverage. If you are comparing those rails, use this breakdown: FedNow vs. RTP: What Real-Time Payment Rails Mean for Gig Platforms and Contractor Payouts.

Step 4. Publish a policy table and assign owners#

Use one short policy table so growth, product, finance, and support execute the same rules.

| Trigger | Hold period | Clawback condition | Owner |

|---|---|---|---|

| Signup attribution recorded | Define your policy window | Define your invalid-attribution rules | Assign owner |

| First successful payment verified | Define your review window | Define refund and reversal handling | Assign owner |

| Retained activity milestone verified | Define your validation window | Define invalid-milestone handling | Assign owner |

| Payout release batch approved | Define post-approval handling | Define return, duplicate, and fraud handling | Assign owner |

If your value is realized after paid usage or retention, use that later proof point as the earning trigger instead of signup.

Build compliance and tax gates into eligibility from day one#

Put eligibility gates before payout release so rewards can be tracked and earned, but not paid, until required compliance and tax steps are complete.

Step 1. Block release until required compliance checks are complete#

Treat required compliance checks as payout-eligibility states, not post-incident cleanup. The exact checks and pass/fail criteria are program-specific, so define them in your own policy and enforce them before funds move.

Keep the operational split clear: commercially earned does not always mean payout-eligible. That lets growth keep attribution data while finance and payments teams control release risk.

Before launch, make sure blocked rewards show a high-level eligibility status and what category is still missing; include review timing and release-decision details according to your policy.

Step 2. Separate market and entity checks#

If you pay both individuals and businesses, split those paths early. Where your markets require it, business flows may need VAT or GST handling and other jurisdiction-specific outcomes.

Do not hardcode one global rule for every market. OECD guidance describes multiple platform-involvement models for VAT and GST, including cases where platforms can be made liable. Your eligibility logic should follow a maintained market-and-entity matrix rather than ad hoc exceptions.

Step 3. Put tax-document gating in the payout flow#

If tax documentation can be required, gate release on document status inside the payout flow instead of relying on a later rescue process. Keep status states explicit, for example requested, received, or missing, and store artifacts so finance can retrieve them for review.

Use caution with form-level specifics. The provided IRS material references filing artifacts such as Forms 1042-S, 1099, and W-2, but it is historical and not a current-year rules source. Operationally, define who owns tax-document collection decisions, when payout pauses, and where records are retained.

Step 4. Add a clear "not eligible yet" path#

Show users clear status and next steps without exposing internal review logic. Plain messages like pending verification, additional business details needed, tax document required, or unavailable in this market can move completion forward.

Internally, keep detailed reason codes and escalation notes. Externally, show only the current state and what the user should do next.

For a step-by-step walkthrough, see How to Build a Finance Tech Stack for a Payment Platform: Accounts Payable, Billing, Treasury, and Reporting.

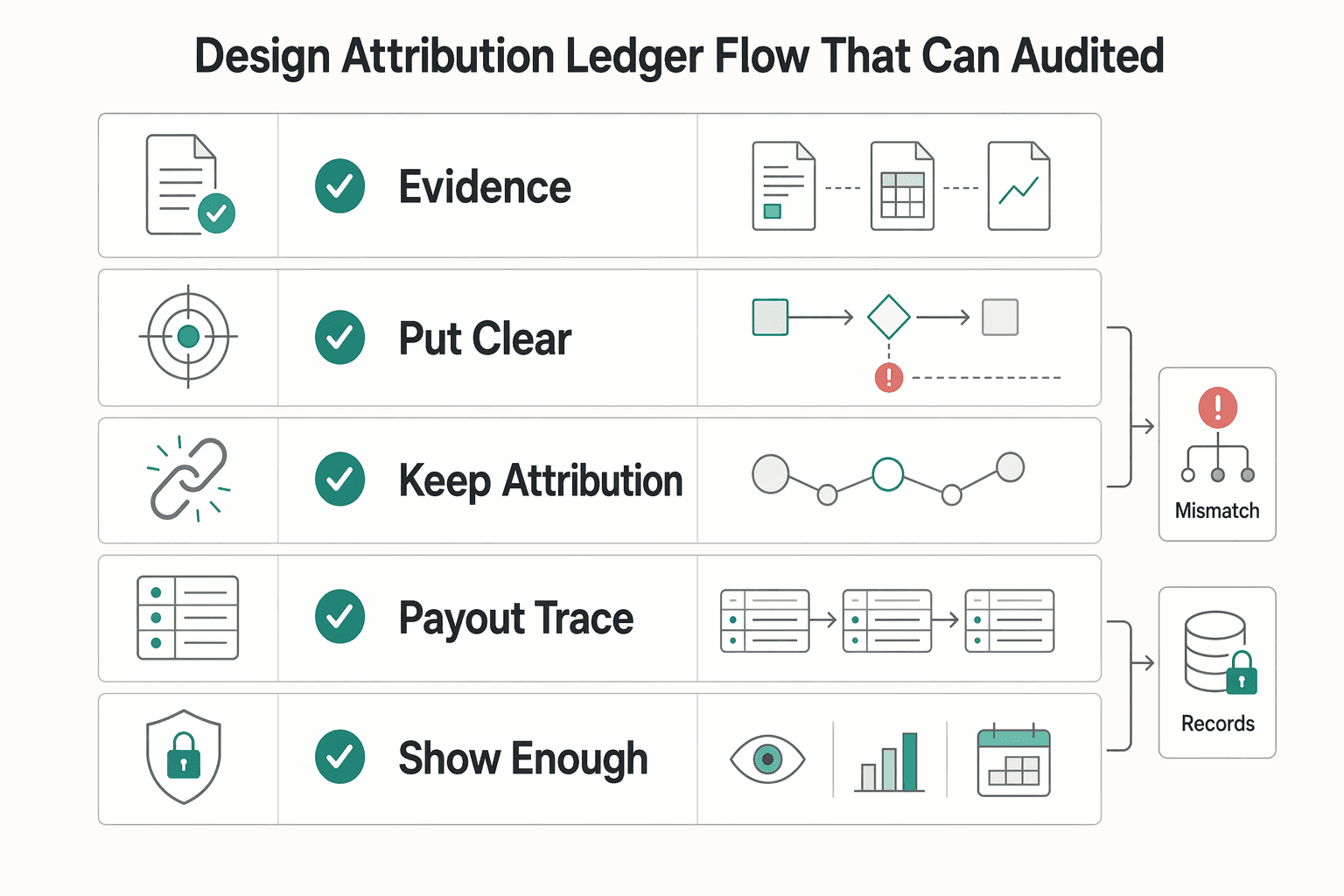

Design attribution and ledger flow that can be audited#

An auditable payout flow makes decisions traceable and transparent while limiting unnecessary data exposure. This is where a workable program becomes an operable one.

Keep the sequence consistent across systems:

- In group environments, define one source-of-truth order for profile-based content selection, feedback capture, payout amount determination, and decision recording.

- Put a clear validation checkpoint before payout amount determination so the amount is set only after relevant feedback is confirmed.

- Keep attribution rules explicit and consistent, and route ambiguous cases to manual review.

- Require clear traceability. Every payout decision should map to the relevant feedback and decision record.

- Show enough status to explain decisions, but limit exposure of sensitive data.

- Watch for exclusion risk in the flow, since digital incentive systems can perpetuate or exacerbate barriers for digitally excluded groups.

Launch with a controlled experiment and explicit scale gates#

Treat the first launch as a controlled test, not a broad rollout. This helps you interpret results more reliably and separate signal from noise.

Start small and decide in advance what success, pause, and expansion mean. Then hold yourself to those rules:

- Start with a limited cohort and one incentive variant.

Use a narrow slice you can isolate, such as one segment, geography, or product line, and keep one reward structure with one trigger path. A purchase-triggered reward keeps payout logic clearer because payout is tied to conversion, not just sharing. Avoid changing audience, incentive, messaging, and eligibility at the same time or attribution gets murky. If you already track a viral coefficient, separate that baseline before judging paid referral lift; a cohort near K > 1 can make referral lift look stronger than it is.

- Define a shared decision metric set before go-live.

Lock how you will calculate the core metrics you will use to judge performance, and keep one shared definition set across product, growth, and finance. Prioritize measures tied to conversion quality and retained revenue after incentive cost, not just top-of-funnel sharing.

- Set stop and scale rules before first results arrive.

Write down what qualifies for expansion and what triggers a pause before launch. Judge performance on conversion quality and retained revenue after incentive cost, not participation volume alone. If sharing rises while downstream quality falls, treat that as a pause signal.

- Use a regular review and one decision log.

Review results in one cross-functional forum so growth, product, and finance are interpreting the same data in context. Keep one log with the cohort, variant, metric definitions, current result, decision, and effective date for any change. If terms, eligibility, or messaging changed, the log should show exactly when. Without that, expansion decisions are harder to audit.

Operate the payout engine with exception handling and reconciliation#

As referral volume grows, build the payout engine for exceptions, not just the happy path. Keep exceptions visible, keep attribution traceable, and review records consistently so delays, missed rewards, and disputes do not erode trust.

Start with explicit exception categories in your operating view. Keep unclear or failed cases separate from routine referrals so teams can see the reason for each exception and the next action.

Make attribution your first control point. Each reward candidate should tie to a unique referral link or code and to the conversion event that made it eligible. Use the referred user becoming a paying customer as the reward trigger so release decisions stay concrete.

Treat spreadsheet-heavy operations as a risk signal once you are past more than a few dozen advocates. At that point, manual handling is more likely to create errors, missed referrals, and disputes.

Track referral activity and reward decisions in one place. The record should be clear enough that an operator can verify what happened without reconstructing the case by hand.

At minimum, keep these checkpoints connected: clicks, sign-ups, conversions, and the reward decision after a referred user becomes a paying customer. If records conflict or a status is unclear, move the case into manual review until it is resolved.

Review records on a routine your team can sustain. In each review, compare referral activity, reward decisions, and open exceptions so issues are handled before they accumulate.

Do not treat headline totals as finished if unresolved exceptions are growing. A stable program is one where attribution and exception volume are both under control.

Write clear handling rules before failures stack up. Failed cases will happen, and ad hoc handling can introduce delays and errors.

Keep a clear record of why a case was handled manually and what changed. Another operator should be able to review the case later and understand the decision end to end.

Handle common failure modes before they become expensive#

The costly breakdowns are usually visible early if you treat each one as a separate control problem: quality drift, payout integrity, abuse risk, and close-readiness.

| Failure mode | Early signal | Control response |

|---|---|---|

| Quality drift | Referral activity rises faster than attributable conversions | Tighten eligibility and reward scope and route uncertain cases to review |

| Payout integrity | Attribution is incomplete or ambiguous | Move the payout into exceptions and require an idempotency key for retries |

| Abuse risk | Fast rewards reach unproven accounts or sudden inflow spikes appear | Apply tighter fraud controls and heightened review |

| Close-readiness | Liabilities, released payouts, reversals, and open exceptions cannot be traced end to end | Keep ledger and payout records traceable end to end |

Watch the gap between referral activity and attributable conversions. If activity rises faster than attributable conversions, treat it as an internal quality-risk signal until the gap is explained. Consider tighter eligibility and reward scope for that cohort, and route uncertain cases to review before expanding access again.

Hold ambiguous cases instead of paying first and fixing later. If attribution is incomplete or ambiguous, move the payout into exceptions based on your risk policy. Require an idempotency key for every retry and reprocessing path to reduce duplicate payout attempts.

Tighten fraud controls before fast rewards reach unproven accounts. Treasury's 2026 National Money Laundering Risk Assessment identifies fraud and cybercrime among the top U.S. money-laundering threats and says these categories generate the largest volumes of illicit proceeds. Sudden inflow spikes can warrant heightened review.

Do not treat close-readiness as separate from payout operations. A period close is harder to defend when referral liabilities, released payouts, reversals, and open exceptions cannot be traced end to end in your ledger and payout records. When you rely on regulatory text for control decisions, use the official PDF on govinfo.gov. FederalRegister.gov's XML rendition is informational and does not provide legal notice to the public or judicial notice to the courts.

Related reading: FDIC Pass-Through Insurance for Platform Wallets: How to Protect Your Contractor Funds.

Set pause, rollback, and redesign rules#

Treat pause, rollback, and redesign as separate calls, not one kill switch. That lets you contain a broken channel without shutting down demand that only needed a narrower incentive.

| Action | Use when | Response |

|---|---|---|

| Pause | Pilot economics weaken while controls still look intact | Stop expansion and freeze new incentive tests until the cohort read is clean |

| Roll back | Control integrity breaks even if top-line growth still looks strong | Return to the last configuration with clean books and traceable payout decisions |

| Redesign | Growth is real but fragile | Keep the channel live for higher-quality segments, remove weak incentive tiers, and simplify where needed |

| Shutdown | Demand quality itself is the problem | Use a full shutdown only in that case |

Pause when your pilot economics weaken, even if controls still look intact. Use the economics checks defined in your pilot plan, then stop expansion and freeze new incentive tests until the cohort read is clean.

Keep the comparison consistent: use the same retention window, refund treatment, and attribution rules for referred and baseline users. Inconsistent definitions can make low-quality signup volume look like healthy growth.

Roll back when control integrity breaks, even if top-line growth still looks strong. Unresolved reconciliation gaps, repeated attribution conflicts, or compliance-gate bypasses should be treated as operating failures, not acceptable tradeoffs.

Return to the last configuration with clean books and traceable payout decisions. Each released payout should map to an attributable conversion record and the matching ledger entry.

Redesign when growth is real but fragile. Keep the channel live for higher-quality segments, remove weak incentive tiers, and simplify where needed instead of defaulting to a full shutdown. Use shutdown only when demand quality itself is the problem.

Use your own pilot data as the decision base. Treat external benchmarks as directional until your pilot data confirms they transfer to your platform. Use your pilot memo, source data, and version-checked policy documents as the basis for pause, rollback, or redesign, and share sensitive data only on official, secure sites.

If your pilot passes your control and economics checks, map execution details for compliance-gated batch releases in Gruv Payouts.

Copy and use this launch checklist#

Use this checklist to turn the earlier decisions into one reviewable record before launch. Referral channels can underperform even when incentives exist, so the goal is a single place to confirm economics, controls, and ownership.

Confirm economics first. Set your non-negotiables first: baseline CAC, LTV assumptions, and reward-cost guardrails. The model only works if rewards replace or reduce acquisition cost instead of adding a second cost layer.

Keep assumptions conservative. Referred customers are often described as higher quality, and one cited benchmark shows 16% higher LTV, but treat that as a hypothesis to validate in your own data. Verification point: keep one written sheet with baseline acquisition cost, absorbable reward cost, and the condition that makes the program unprofitable.

Lock design choices before you build messaging or payout logic. Decide the structure first: who qualifies, what triggers a reward, and when a reward can be delayed or reversed. If those are still undecided, teams will create conflicting answers once referrals start.

Ambiguity at payout time is a real risk. Referral marketing depends on trust, and trust can drop when users cannot get a clear reason for a delayed, denied, or reversed reward. Verification point: someone outside the project should be able to explain who gets paid, when, and under what conditions.

Enforce controls before funds are released. Your checklist should explicitly cover eligibility, attribution, duplicate-prevention checks, and complete internal records.

One failure mode to watch is rewards that cannot be clearly attributed. If a payout cannot be traced to a qualifying referral event and matching internal record, hold it. Verification point: test three referrals, including one failed or disputed case, and confirm the evidence trail end to end.

Validate operations in production terms. Make sure operations can run this in production: monitoring, failure handling, clear ownership, and regular reconciliation. Early referral growth is often more manual than expected, especially in cold start.

Run a simple process test: one success, one failure, one retry. Verification point: the on-call operator should know where failed payouts appear, where unmatched referrals go, and which report or export supports reconciliation.

Decide governance before go-live. Document governance before launch: review cadence and clear owners for approve, pause, rollback, and redesign. If ownership is just "the team," decisions will lag when economics or controls slip.

Require a dated approval record and one place to log ongoing decisions. Verification point: confirm who can pause the program the same day if quality drops or reconciliation gaps appear.

Need the full breakdown? Read How to Launch a Referral Program for Your Gig Platform with Built-In Commission Tracking.

Frequently Asked Questions

What is a referral-based payment incentive platform in practical terms?

It is a structured referral program where payouts are performance-based and released only after a qualifying event. Those events can include a sign-up, first purchase, or an ongoing subscription payment. In practice, it formalizes word of mouth into a system with clear payout checkpoints.

Referral growth vs viral growth loop: which should we prioritize first?

Prioritize the mechanism that best matches real user behavior. If product use naturally drives sharing, it can make sense to improve that loop first, because a referral program will not fix weak core product value. If customers are happy but not referring on their own, structured prompts and rewards are often necessary.

Should we run a Single-sided referral program or a Double-sided referral program?

There is no universal winner between single-sided and double-sided structures. Choose the model your LTV and business economics can support, then validate it in your own data. Treat the decision as a testable tradeoff, not a fixed best practice.

Should rewards be cash, credit, discount, or recurring payout?

Match the reward type to your LTV and business model rather than copying what is common. Cash, credit, or other incentives can work depending on how value is realized in your funnel. Recurring payouts can improve alignment with retention and customer quality, while one-time payouts can reduce long-term alignment and bias toward short-term volume.

When does a referral payout model become unprofitable?

It can become unprofitable when incentive cost rises faster than the retained value of referred customers. A practical check is whether payout costs still fit your LTV and business model under consistent measurement. High referral volume alone is not a health signal if quality or retention degrades.

How do we prevent referral fraud and payout abuse without killing conversion?

Use performance-based payout checkpoints instead of paying for raw invites. Release payouts only after a qualifying event such as a sign-up, first purchase, or ongoing subscription payment. This keeps incentives tied to real outcomes rather than unverified activity.

Which metrics prove the program is healthy beyond top-line referral volume?

Focus on quality and economics, not just referred-user counts. Track qualifying-event completion, retained referred value, and incentive cost relative to what those users actually contribute. Compare referred and baseline cohorts using the same retention assumptions so the read is reliable.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/dfars/part-252-solicitation-provisions-and-c...trusted

- cms.gov/files/document/unified-pac-report-congress.pdftrusted

- cms.gov/regulations-and-guidance/guidance/manuals/do...trusted

- congress.gov/committee-report/119th-congress/senate-repor...trusted

- federalregister.gov/documents/2025/11/25/2025-20907/medicare-pro...trusted

- federalregister.gov/documents/2025/08/04/2025-14681/medicare-pro...trusted

- home.treasury.gov/system/files/246/2026-NMLRA.pdftrusted

- hscrc.maryland.gov/Documents/Modernization/Model%20Documents/MD...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Choosing Nursing Agency Payout Models for Shift-Based Healthcare Staffing

Choose your payout model based on operational proof, not payout-speed marketing. For healthcare staffing platforms, the real question is whether payouts stay reliable when shifts change, get canceled, or are disputed.

How to Create a Referral Program for Your SaaS Product

A major early risk is not the reward. It is launching with fuzzy attribution, unclear ownership, and payout rules nobody can defend once disputes start. Build this channel as part of your revenue system, not as a side tactic. Otherwise, you may end up cleaning up support, finance, and trust issues after the first signups arrive.

FedNow vs RTP for Gig Platform Contractor Payouts

You are not choosing a payments theory memo. You are choosing the institution-backed rail path your bank and provider can actually run for contractor payouts now: FedNow, RTP, or one first and the other after validation.