Quick Answer

Use a court-first sequence: confirm Rule 23 approval and appeal finality, lock the Plan of Allocation logic, freeze the claimant universe, and release payments in staged cohorts. Keep class counsel on legal judgments while finance and engineering control batch release and retries. Treat post-settlement funding pages as a different product category. Close only after approved, paid, failed, returned, and unresolved records reconcile at claimant level.

How settlement disbursement operations work#

Search gets noisy here because three different categories use similar language: claims administration, post-settlement funding, and law-firm marketing. Treat them as interchangeable and you can make bad decisions about how payouts actually get done.

Claims administration is the operating lane for notice, claims handling, validation, and distribution. Post-settlement funding is a separate financing product for plaintiffs after resolution, often framed around speed, such as 24 to 48 business hours after approval. Law-firm consultation pages are generally built for client intake and marketing, not payout operations.

For an execution team, the filter is simple. Prioritize guidance tied to court approval, class notice, claimant handling, disbursement operations, reconciliation, and quality controls. If those elements are missing, you may not be looking at a practical implementation guide for controlled class payouts.

This article stays on that operating path. It covers payout execution from approved settlement through final closeout, with controls teams can review and run repeatedly. The focus is the middle of execution: claimant records, payment setup, staged release, exception handling, and proof that the run closed correctly.

Rule 23 is the legal anchor for this flow. In certified class actions, claims may be settled, dismissed, or compromised only with court approval, and the court must direct the best practicable notice to class members. Operationally, that ties payouts to the approval event and to the claimant population shaped by notice under the approved settlement terms.

The rest of this guide follows a decision path teams can actually use. It separates adjacent categories, defines law-firm and administrator roles, maps the approval-to-payment sequence, and puts in controls that hold up in compliance review and final closeout.

Define the operating model before choosing vendors#

Choose the operating model first, then evaluate vendors. Claimant payout operations, class counsel's legal role, and plaintiff funding products are not the same thing.

| Category | Core role | Operational signal |

|---|---|---|

| Claims administration | Notice, claims handling, validation, and distribution | Tied to court approval, class notice, claimant handling, disbursement operations, reconciliation, and quality controls |

| Post-settlement funding | Financing product for plaintiffs after resolution | Often framed around immediate cash or 24 to 48 business hours after approval, not class-wide payout operations |

| Law-firm consultation pages | Client intake and marketing; legal-representation lane | Not a practical guide to payout operations or distribution execution |

For this article, settlement disbursement is the process of paying each claimant after settlement approval under the court-approved distribution plan. In practice, distribution is tied to a Plan of Allocation, or another plan the court approves, so that court-approved plan should anchor your payout design.

A claims administrator often handles execution work, including claims adjudication, funds management, award calculations, and distribution services, and may support notice operations. Class counsel and the plaintiffs' attorney team remain in the legal-representation lane. Under Rule 23, the court appoints class counsel in a certified class action, and class counsel must fairly and adequately represent class interests.

Before you shortlist providers, ask which court-facing and operational artifacts they actually support. A credible claims-administration path should map to preliminary approval, where parties should identify a proposed settlement administrator, and to notice and distribution workflows. Also confirm who maintains the settlement website when class notice directs members there, since guidance contemplates a site maintained by the claims administrator or class counsel.

Post-settlement funding and settlement cash advance products address plaintiff cash flow, not class-wide payout operations. These products are described as immediate cash in exchange for an interest in future settlement proceeds, with repayment from the settlement. Pre-settlement versions are advances tied to expected recovery and are described by providers as non-recourse. If a vendor cannot show notice, claims adjudication, distribution, and court-plan alignment, treat it as a category mismatch, not an implementation path.

That distinction matters because the next step is not buying software or picking a payment rail. It is assigning who owns each part of the flow.

Assign ownership and handoffs across legal, ops, and engineering#

Set ownership before launch. If you wait, errors will surface when claimant files are already moving and no one has clear final signoff. For settlement disbursements, ownership mapping is a release control, not a paperwork exercise.

Start from the court-facing split in the process. Under Rule 23(g), the court appoints class counsel, while a settlement administrator may be retained to run notice, claims processing, and settlement fund distribution. Your internal finance and engineering teams still need named owners for payment-file release, closeout matching, and artifact storage.

Use a phase table before launch#

You do not need a universal RACI. As an operational control, define an owner, a final approver, and an evidence output for each step before the first claimant payment is released.

| Phase | Primary owner | Required handoff | Final approver | Evidence output |

|---|---|---|---|---|

| Class action lawsuit resolution and launch setup | Law firm / class counsel | Counsel provides approved plan terms, notice language, and administrator engagement details to claims administrator, finance, and engineering | Named legal owner for court submission; named internal approver for operational launch | Court approval records, administrator appointment record, notice and claims-payment method record |

| Claimant validation | Claims administrator | Administrator sends claimant status snapshots and validation outcomes to finance and engineering | One named ops or finance approver if internal review is required | Claimant status snapshot, duplicate or deficiency logs, website or intake export |

| Payment execution | Internal finance with administrator support, or administrator if contracted to execute | Finance and engineering receive approved payout file and method assignment; counsel is informed of release timing as needed | Single release approver | Locked payout file, batch approval record, payment attempt export |

| Exception handling | Claims administrator for claimant contact and remediation, finance for held funds | Exception queue shared with finance and engineering; counsel receives issues that affect plan interpretation | Named exception owner | Return and failure reports, reissue decision log, claimant communication record |

| Closeout reconciliation | Internal finance | Administrator delivers final payment and unpaid balance outputs; engineering stores final exports; counsel receives closeout pack | Finance lead | Reconciliation workbook, unresolved balance report, audit trail export, destruction and retention record where applicable |

Make the handoff package explicit#

Treat handoffs as evidence packages, not just file transfers. For claimant validation, include a status snapshot, an exception list, and the freeze date for the claimant universe used for payment. For payment execution, include the payout file, release approval, and an item-level export engineering can archive unchanged.

Before funds move, confirm that the approved claimant count, payout file count, and batch release count align. If they do not, resolve the mismatch before release.

Treat evidence as part of the job#

Recordkeeping belongs in the ownership model. At least one federal district standing order requires parties to identify the proposed settlement administrator, describe the selection process, and disclose proposed notice and claims-payment methods. The same order calls for addressing data-handling topics such as retention, destruction, audits, and crisis response. Even outside that district, those are practical checkpoints.

If a step is shared between the claims administrator and internal ops, name one final approver before launch and define the artifact that proves the handoff is complete. That keeps legal, operational, and technical responsibility clear through exception cycles and closeout.

Once ownership is locked, the real question becomes sequence. Payouts usually go wrong not because one step was missed, but because the right steps were done in the wrong order.

Run the end-to-end payout sequence in the right order#

Run payout only after the upstream gates are truly closed: approval and finality, claimant freeze, eligibility and payment-detail checks, method assignment, staged release, then claimant-level tie-out. If an earlier step is still changing, the payout file is not ready.

Gate on approval and finality#

Start your payment timeline from confirmed approval and finality status, not target dates. For a certified class, settlement requires court approval under Rule 23, and settlement flows can gate payment on appeal finality and completed claim review.

In practice, those are separate checkpoints. One settlement flow states that distribution starts only after court approval, appeals expiry, and claim-form review. In that matter, the final approval hearing was held on January 15, 2026, but that milestone alone did not trigger release. Another settlement reports appeals resolved and settlement final, with claim review underway, and initial distribution to valid claims beginning in May 2026.

Before release, lock an approval pack with the approval record, the applicable appeal-finality confirmation, and the exact plan terms your payout logic uses. If claimant counts or amounts were built on draft assumptions, refresh them before funds move.

Freeze the claimant universe before method assignment#

Do not assign payment rails to a moving claimant population. Freeze the final approved universe first, then assign each approved claimant to the allowed payment method under the settlement terms.

Claims administration includes intake, processing, eligibility and benefit-level determination, then payment issuance and tracking for authorized claimants. Live settlements also enforce cutoff points after filing deadlines. For example, BCBS ties eligibility to filing by November 5, 2021.

Before building any batch, run these checks for each claimant:

- inclusion in the approved claimant universe after the filing cutoff

- eligibility and benefit-level confirmation under the approved plan

- payment-detail validation for the selected or assigned rail

- fraud or anomaly flags reviewed before issuance

These controls belong before money movement. Reuters-reported data shows large fraud pressure signals, including more than 80 million claims with significant signs of fraud in 2023 and one case with a reported claims volume far above estimated product sales. Exact fraud-loss totals remain hard to quantify, but the operational takeaway is simple: validate first, pay second.

Some settlements offer electronic payment options or checks, and some distribute in installments with timing that can vary by class category and payment rail. That is another reason to assign methods only after the claimant universe is frozen.

Release in stages, not one blast#

Use staged cohorts so you can isolate failures without blocking the full settlement. Cohorts can be split by method, claimant segment, or risk profile.

| Stage | What must be true | Verify before next stage | Evidence to lock |

|---|---|---|---|

| Approval and finality | Court approval complete; appeal gate cleared where applicable | Plan terms and payout logic match | Approval pack |

| Claimant freeze | Filing window closed; included claims reviewed | Approved claimant count and total benefit amount | Frozen claimant export with freeze date |

| Method assignment | Payment method assigned per settlement terms | Method-assigned count matches approved count minus held exceptions | Method-assignment file and exception log |

| Batch release | Cohort file locked and approved | Batch count, dollar total, and release approval align | Locked payout file and payment-attempt export |

| Closeout | Returns and failures triaged | Paid count, exception count, unresolved balance known | Reconciliation workbook and unresolved-balance report |

Staging also lets you separate failure modes. Uncashed checks and returned checks need different handling than other payment exceptions. Treating all failures as one queue slows remediation and reissue decisions.

Reconcile from claimant level before you close#

Closeout is claimant-level work, not just batch-total math. You need status-level evidence for each approved record, such as paid, failed, returned, held, or pending remediation.

Administrator case-study language describes matching disbursed funds against detailed claimant-level tracking. Use that as your operating standard. Before close, confirm approved count, paid count, exception count, and unresolved balance, and tie them back to the frozen claimant universe and locked batch files. If any batch changes after approval, rerun preflight counts and relock the evidence package.

Once that sequence is stable, rail selection becomes easier. You are no longer choosing for convenience alone. You are choosing for recoverability and visibility.

Choose payout rails and batch logic that reduce operational risk#

After the claimant universe is frozen, payout rail choice is a control decision. Choose the setup that gives you clear status visibility, clean return handling, and a defensible audit trail. If you cannot see batch-level and item-level status during execution, keep volume low until you can.

Pick rails for recoverability, not just claimant reach#

Compare checks and electronic payouts on traceability and remediation, not preference alone.

| Rail | Operational strength | Common friction | Control to require |

|---|---|---|---|

| Check | Common in class settlements | Uncashed checks are common | Logged reminders, void/reissue workflow, and logged claimant contact attempts for audit trail |

| Electronic payout | Machine-readable lifecycle states and status-change events | Returned payouts are often driven by incorrect destination details | Upfront destination validation and a clear remediation queue |

Checks are not inherently wrong, but they do require active follow-up. In some settlements, reminder programs have improved check-cashing outcomes by as many as 20%, but do not assume that outcome will repeat in every program.

Electronic rails can improve operational visibility when your payment layer exposes statuses like processing, posted, failed, returned, and canceled, plus reporting and event feeds. In mixed-vendor models, align administrator and payment-partner records so the audit trail survives the handoff.

Make retries safe before you care about speed#

Duplicate-payment risk usually shows up during retries, so idempotency should be applied per payout operation, not only at the batch-file level. Use one stored idempotency key per payout operation and reuse that same key on retries.

The rule is simple. The same key returns the same result on retry, including failures. If a retry generates a new key, you can create duplicate disbursement records even when batch totals still look acceptable. Before release, confirm each payout item is tied to one claimant reference, one amount, one destination record, and one persisted idempotency key.

Require claimant-level status before high-volume release#

Batch totals are not enough. Every claimant should be traceable from authorization through claim and payment outcome. Before a high-volume wave, confirm your team can answer:

- Which batches are in flight, with item counts and total dollars?

- What is the current status of each payout attempt?

- For returned payouts, what is the return reason and remediation step?

- Can you export item-level status history for reporting and audit review?

If you cannot answer those reliably, do not launch at scale yet. Rolling releases are a practical way to catch return patterns, destination-data issues, and handoff gaps before they spread across the full class.

Good rails and retry logic still are not enough on their own. You also need release controls strong enough to stop bad batches before money moves.

Build controls that prevent duplicate, failed, or non-compliant payments#

The core control is release discipline. Do not release a batch unless policy, data, and balance checks all pass. If any gate fails late, pause the release and run preflight again instead of forcing exceptions through.

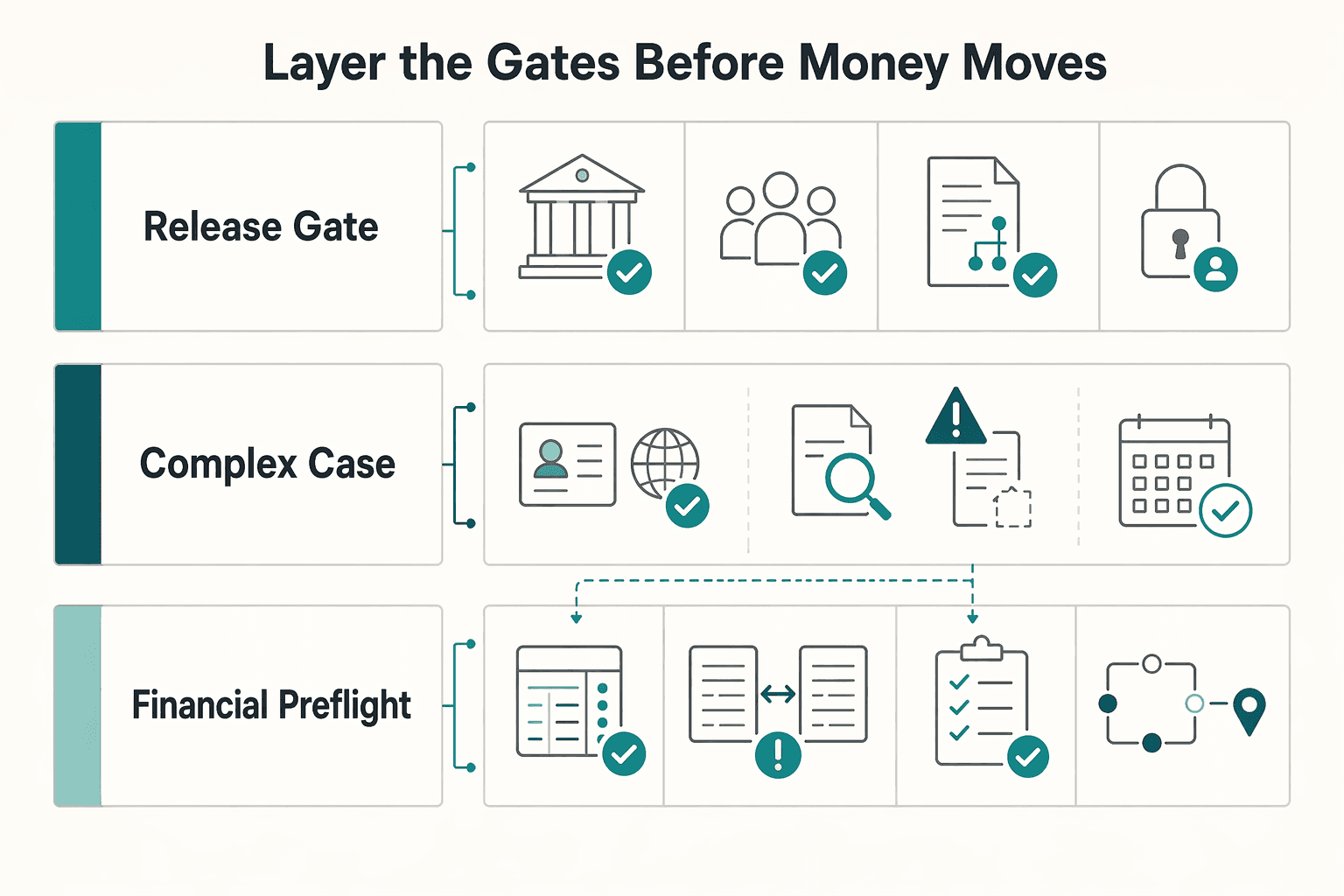

Layer the gates before money moves#

Start with governance, then compliance, then financial matching. If you are disbursing from a Qualified Settlement Fund, tie release to the court- or government-approved structure, the claimant population authorized for distribution, approved disbursement rules, and a named approver for higher-risk batches.

For identity and sanctions checks, apply the rules that actually govern your entity and workflow. Do not assume all law firms or administrators have identical obligations. Where CIP-style controls apply, run risk-based verification before onboarding or account use as required. In some regulated contexts, screening also includes government terrorist-list checks with separate OFAC obligations. Operationally, the priority is clear ownership, recorded outcomes, and no release before required checks clear.

| Control layer | What to verify | Evidence to retain |

|---|---|---|

| Policy gate | Batch matches court-approved claimant universe and payment rules | Release approval record, batch summary, claimant count and dollar snapshot |

| Identity or sanctions gate where applicable | Required screening completed and disposition recorded | Screening result, review notes, escalation outcome |

| Financial preflight | Batch dollars equal approved claimant dollars; no unexplained variance | Reconciliation export, exception list, final release sign-off |

Make every payout traceable at claimant level#

Traceability helps you prevent duplicate effects and speeds remediation. Keep one idempotency key per payout operation, and pair it with a stable payout ID linked to one claimant reference, one amount, one destination record, and one release wave.

Keep an audit trail that is effectively append-only, even if your system does not label it "immutable." At minimum, you should be able to show who approved release, when screening cleared, when an item was released, and whether it later failed, returned, canceled, or was reissued. In OFAC-covered transaction contexts, records must be full, accurate, and retained for at least 10 years. That makes retention and export quality core controls.

Before release, sample payout items and confirm claimant record, payout ID, amount, destination snapshot, and current status all match. If that check is slow or unreliable, your controls are weaker than they appear.

Re-run preflight when the batch changes#

Late changes are a common source of preventable failures, so rerun preflight whenever inputs shift. Common failure patterns can include duplicate claimant records, updated payment details after approval, and mismatches between approved totals and the disbursement file.

If a compliance result arrives late or destination data changes during approvals, stop the batch. Refresh claimant and payout snapshots, rerun duplicate and total checks, and rebuild the release file if needed. That extra cycle is often lower risk than remediating duplicate, failed, or non-compliant payments after funds move.

Even with strong preflight controls, some payments can still fail or go stale. That is why exception handling needs its own lane, not an afterthought queue.

Related: A Guide to the FTC's Proposed Ban on Non-Compete Clauses. Need a concrete baseline for compliance-gated, idempotent releases with audit-ready tracking? Review Gruv Payouts.

Design exception handling for returns, stale details, and unresolved claims#

Exception handling needs its own operating lane with clear ownership, evidence rules, and aging. Without that, unresolved items can blur payout status and leave settlement exposure open.

Classify failures by cause, not just by payment rail. A returned payment, an ACH administrative return, a duplicate claimant identity hit, and an unresponsive claimant each need different remediation steps, contact paths, and reissue evidence.

Classify by what actually happened#

Use a taxonomy that preserves reason codes and next actions:

| Exception type | Typical trigger | Primary owner | Reissue checkpoint |

|---|---|---|---|

| Returned payment | Returned check, failed delivery, claimant disengagement | Claims administrator or ops | Confirm claimant record, original payout ID, current destination details, and whether settlement terms allow reissue |

| Invalid account data | ACH administrative return such as R02 (Account Closed), R03 (No Account/Unable to Locate Account), or R04 (Invalid Account Number Structure) | Payments ops | Capture corrected account details after the failed attempt and verify they map to the right claimant |

| Duplicate claimant identity | Duplicate claim submission or suspicious overlap in identity/entitlement | Claims administration | Hold reissue until one valid payable claimant identity is resolved |

| Unresponsive claimant | No response to outreach, uncashed payment, or incomplete claim data | Claimant support team | Log outreach attempts and route per settlement terms to reissue, claims process, dormancy handling, or escheat path |

A single generic "failed payment" status is usually not enough. You can lose reason codes, contact history, and settlement-specific routing rules, which can weaken audit support and slow close.

Put each exception into an SLA-backed queue#

Define SLAs per settlement program, not one universal SLA across all programs. For each queue, document the owner, escalation path, claimant contact channel, and the evidence required before any reissue.

Settlement-specific websites, toll-free numbers, dedicated case email, and live support are common remediation channels. Keep every interaction tied to the claimant record.

Require an evidence pack before reissue. Some cases may only need updated destination details and outreach logs, while others may require documents such as name-change records or a death certificate. Before approving reissue, run one final comparison: original payout ID, failed-attempt status, claimant reference, approved amount, and new destination snapshot.

Track aging so finance can see unresolved exposure#

Track unresolved exceptions by aging bucket, count, dollars, oldest age, and expected disposition so finance can quantify open exposure for the settlement.

Checks need separate aging logic because outcomes change over time. Some programs instruct recipients to cash checks within 90 days, while UCC 4-404 states a bank is not obliged to pay a check presented more than six months after its date. Expired or uncashed funds do not follow one universal path. Depending on settlement terms, they may be reissued, handled through a claims process, held through a dormancy period, or escheated to the appropriate states.

If this view stays current and evidence-backed, finance has a clearer basis to explain and close unresolved exposure, reducing late surprises during final matching.

With exception handling defined, you can compare operating models on the thing that matters most: who can actually run this process end to end.

Compare operating models before you commit#

Once exception queues and aging are in place, decide who owns the payout operation. If your priority is scale, traceability, and clean closeout, current public evidence generally favors an administrator-led model over law-firm-led or funding-adjacent models.

Use this filter first: choose the model whose stated role includes claims administration and distribution. Public descriptions of settlement administration include claim validation and fund distribution, while the law-firm and funding examples below are positioned around different primary work.

Directional comparison#

This is not a market ranking. It is a directional score based on what the public pages say about each model's role.

| Operating model | Public positioning in current evidence | Control depth | Implementation burden for payout ops | Transparency from public pages | Claimant experience fit | Reconciliation readiness |

|---|---|---|---|---|---|---|

| Administrator-led, Verus LLC style | Verus describes "end-to-end class action administration" focused on efficiency, compliance, and claimant experience. JND publicly lists consultation, notice, claims processing, validation, and distribution as class action administration services. | High | Medium | Medium | High | High |

| Law-firm-led, Schroeter Goldmark & Bender / Reiff Law Firm style | SGB emphasizes handling class action cases for workers and consumers. Reiff emphasizes strategically crafting and pursuing class action lawsuits. | Medium for legal control, Low for payout operations | High | Medium | Medium-Low | Low |

| Funding-adjacent, RapidFunds / USClaims style | USClaims says "It's Not a Lawsuit Loan. It's Litigation Funding Simplified" and describes post-settlement funding as non-recourse advances against future settlement payments. RapidFunds' cited release says it provides funding for attorneys only, not plaintiffs. | Low for class-wide disbursement control | High if used as a payout substitute | Medium | Mixed | Low |

The scoring reflects where operations are centered. Administrator-led models are publicly framed around the settlement lifecycle, so claims validation and distribution are more likely to sit in one operating lane. Law-firm-led models are publicly framed around litigation and case prosecution, which does not by itself establish production payout operations.

Funding-adjacent models are easy to misread in search. In the cited pages, USClaims and RapidFunds describe funding products rather than class-wide settlement disbursement operations. USClaims' public 24 to 48 business hour timing is presented for funding after approval and does not, on its own, establish batch payout execution, exception handling, or final closeout across a claimant population.

What the scores imply in practice#

If you expect large claimant counts, repeated payout waves, and finance signoff, give the most weight to explicit claims administration. Verus markets end-to-end administration, and JND's public service list names consultation, notice, claims processing, validation, and distribution. Those are the layers needed to connect approved claimant status, payment attempts, and unresolved balances.

Law-firm-led setups can still work when counsel needs tight legal control over case communications and rules. The tradeoff is that legal ownership does not automatically provide distribution operations, and the cited law-firm pages do not by themselves establish claimant support staffing, status-level reporting, or reissue evidence standards.

Funding-adjacent vendors solve a different problem: plaintiff or attorney financing. If that is treated as proof of disbursement capability, you can still end up without a clear owner for claimant records, the batch-level payout audit trail, and closeout evidence.

Known unknowns you should force into procurement#

Public search results still leave key operator questions open. The cited pages do not confirm fee structures, SLA commitments, integration depth, or comparable payout success metrics across these models. Some administrator pages route buyers to contact or RFP flows instead of full commercial and technical detail, and Verus also uses a contact-led path.

Your checkpoint should be an artifact pack, not website polish. Before committing, ask for:

- a sample payout status export with item-level states

- an exception log showing reason codes and reissue history

- an end-of-cycle closeout package tying approved amounts, paid amounts, returns, and unresolved balances

If a provider cannot produce those artifacts, treat that as a material risk. Also plan for limited public benchmarking. A Duke Judicature source notes there is no complete or reliable source covering all class-action settlements. Use direct operating evidence over marketing breadth when you choose a model. Ask these questions early enough to force concrete answers.

For a step-by-step walkthrough, see How to Write a Final Demand Letter Before Legal Action.

Ask procurement questions that expose real capability#

Use procurement to verify operating readiness, not just category fit. Require concrete answers and sample artifacts on ownership, reporting, and exception handling before you commit.

| Artifact or ask | What to request |

|---|---|

| Settlement administrator details | Document the proposed settlement administrator, how selection was run, how many administrators submitted proposals, and which notice and claims-payment methods were proposed |

| Data-handling controls | Provide specificity on retention, destruction, audits, crisis response, and responsibility for administrator error and insurance |

| Intake and notice report | Show date-stamped file receipt, record volume, and undeliverable-notice counts |

| Claimant-universe reconciliation | Show deduped class-member counts |

| Processing summary | Cover claim forms, opt-outs, and objections |

Start with the U.S. District of Minnesota class-settlement standing-order checklist. Ask the vendor to document the proposed settlement administrator, how selection was run, how many administrators submitted proposals, and which notice and claims-payment methods were proposed. Require the same specificity on data-handling controls, including retention, destruction, audits, crisis response, and responsibility for administrator error and insurance.

Make ownership boundaries explicit in writing. A court-authorized settlement site can be supervised by counsel while controlled by the court-approved settlement administrator, so your contract should clearly assign who owns claimant communications, payment files, and remediation queues.

Request three sample operational artifacts tied to core administration work:

- an intake and notice report with date-stamped file receipt, record volume, and undeliverable-notice counts

- a claimant-universe reconciliation showing deduped class-member counts

- a processing summary for claim forms, opt-outs, and objections

Do not accept generic assurances that reporting exists. Filed administrator declarations show the level of detail you should expect, including date-stamped intake volume, deduped claimant universe, and exception counts.

Finally, force a clean separation between settlement disbursement and post-settlement funding. Post-settlement funding is described as financial support after settlement but before funds are disbursed, which is a cash-flow product, not proof of claims-administration capability. If a vendor cannot separate those offerings or provide artifact examples, treat it as a production-readiness red flag.

Once you know what capability looks like on paper, the next challenge is getting it live without losing control.

Execute a 90-day implementation plan without losing control#

Keep the first rollout narrow and auditable, and do not scale your first settlement cohort until ownership, reporting, and closeout evidence work under live conditions.

| Period | Focus | Key output |

|---|---|---|

| Days 1 to 30 | Lock control boundaries, not volume | Written ownership map signed by legal, finance, ops, engineering, and the claims administrator; reporting schema locked before any pilot |

| Days 31 to 60 | Keep any pilot limited and tie it out fully before expanding | Signed closeout pack tying approved distribution amounts to paid, returned, and unresolved amounts |

| Days 61 to 90 | Operationalize dashboards, escalation paths, and recurring control tests | Dashboards for payout lists, batch status, material exception counts, and expected deposit dates; named owner and evidence before reissue |

Days 1 to 30#

Use month one to lock control boundaries, not volume. Finalize one written ownership map signed by legal, finance, ops, engineering, and the claims administrator, if in scope. It should name the owner for claimant file readiness, payment file release, and exception remediation and reissue approval.

Sequence the work around actual notice and intake timing. Rule 23 requires the court to direct the best practicable notice under the circumstances, so avoid treating the claimant universe as final too early in notice, intake, and adjudication. Claims administration can span notice coordination, adjudication, funds management, and distribution. That is why ownership lines must be explicit.

Lock your reporting schema before any pilot. Require batch-level and item-level fields for approved claimant count, approved dollar total, attempted payments, successful payments, returns or rejects, unresolved balance, and reissue status.

Days 31 to 60#

If a pilot is part of your rollout, keep it limited, then stop and tie it out fully before expanding. The goal is to prove that exceptions route to the right owner with the right evidence, not just that happy-path payments clear.

Use a signed closeout pack as the gate. It should tie approved distribution amounts to paid, returned, and unresolved amounts, with item-level support for each variance. If the pilot needs spreadsheet patching to produce that package, do not scale.

Treat fund size and claimant-level execution as separate risks. A settlement fund can be defined while the number and value of claimed losses remain uncertain until later, so the pilot should test how operations handle changes in claimant population and payable amounts after the fund is set.

Days 61 to 90#

Operationalize dashboards, escalation paths, and recurring control tests after a clean pilot closeout. Dashboards should show payout lists, batch status, material exception counts, and expected deposit dates where the rail provides that visibility.

Define escalation by failure type, not team preference. Returned payments, invalid account data, duplicate claimant identity, and unresolved claimant outreach should each have a named owner and required evidence before reissue.

Use risk-based control testing rather than a single global cadence. FFIEC guidance gives 12-18 months as an example interval for independent testing, and notes testing may need to be more frequent when errors or deficiencies are found. That framework does not automatically govern every law firm or claims administrator, but it is a practical reference for when to retest sooner.

Apply country and program checks in every phase. Payout availability can vary by industry and country. Required account details can vary by bank location, and some platforms note an initial payout is often scheduled 7-14 days after the first successful live payment. Confirm market and program constraints before committing timing or payment methods to claimants.

If you want to run that model through Gruv, use it as an execution layer with clear boundaries.

Use Gruv capabilities to operationalize this model#

Use Gruv as the execution layer, not the legal authority layer. Rule 23(e) court approval and Rule 23(g) class counsel boundaries still apply, so eligibility decisions, settlement-plan changes, and claimant-facing legal judgment should stay with class counsel and plaintiffs' attorney teams.

Map the process to modules your finance and engineering teams can control and test:

- Use collections for inbound money movement where your process needs it.

- Use payout batches for staged claimant disbursements.

- Use webhook-driven status updates to keep claims and finance systems in sync.

- Use batch reports, item-level breakdowns, and reconciliation exports for closeout evidence.

Keep the design ledger-first: compliance-gated payouts, idempotent retries, and an audit trail from request through completion, failure, or retry. Before launch, confirm three controls: stable request or batch references on every payout attempt, item-level status flowing back into your internal record, and closeout exports that do not require spreadsheet patching.

Do not merge legal review and payment execution ownership. Keep claims-specific legal calls with the claims administrator, class counsel, or plaintiffs' attorney teams, and keep payout release thresholds, retry rules, and exception routing with finance and engineering.

Do not assume universal coverage. Gruv support for rails, countries, and funding options is program-dependent, so talk to sales before making claimant-facing promises about payout methods, compliance checks, or closeout outputs.

Conclusion#

Success here comes down to control and proof, not marketing. For class settlements, your operating model has to survive court approval gates, payout exceptions, and closeout without losing claimant-level traceability.

Settlement disbursement is court-governed from the start. Rule 23(e) requires a finding that a settlement is fair, reasonable, and adequate, and court-authorized communications can make timing explicit: payments only after final approval and after appeals are resolved. If your workflow treats approval, notice, validation, payout, and closeout as one generic payments flow, you miss the gate that actually controls release.

The practical next step is to choose one operating model, assign one owner for each handoff, and test it on a bounded claimant cohort before scaling. The pilot should end with artifact-level proof, not just "money sent." You need approved-to-paid matching, failed or returned isolation, unresolved balance tracking, and a final tie-out that agrees across operations and finance records.

When you evaluate providers, ask for evidence that maps to court and finance reality:

- approval record or payout authorization tied to the release batch

- claimant-level status export with approved, paid, failed, returned, and unresolved states

- exception log with reissue evidence requirements

- closeout output tying batch totals to approved totals and open liabilities

- draft or sample closeout report aligned to court reporting expectations

Post-distribution reporting is a concrete benchmark. The Northern District of California Post-Distribution Accounting Form, effective April 5, 2024, tracks fields such as "Number of checks not cashed" and "Amount of settlement funds distributed to class members," and filed materials show administrators submitting final distribution reports to the court. Design to that standard: what was approved, what was delivered, and what remains outstanding.

Use one production filter: can this process produce a reliable audit trail for every claimant? If not, it is not ready. If yes, and you can prove it on a limited cohort first, you are in a stronger position for court scrutiny, finance review, and real exception volume.

Related reading: How a US Freelancer Should Draft a Governing Law Clause with an Asian Client. If you are validating market or program fit before rollout, talk to Gruv to confirm coverage and control requirements.

Frequently Asked Questions

What is legal settlement disbursement in a class action lawsuit, and who owns each step?

Legal settlement disbursement is the post-approval process of paying class members under a court-approved settlement plan. Under Rule 23, a binding settlement is approved only after a hearing and a finding that it is fair, reasonable, and adequate, and Rule 23(g) appoints class counsel for the legal side. In practice, ownership is often split: counsel handles legal judgments and court filings, a claims or settlement administrator validates claims and determines allocations or payment amounts, and internal operations teams may handle payment-release controls, status tracking, and closeout reconciliation.

How are class action claimants paid after settlement approval in practice?

Programs may pay in stages, not in one blast. Claim validation and disputed or unresolved claims can delay full distribution, and one court filing states that full payment could not be completed at that time. In the Payment Card settlement, class counsel requested an initial partial distribution on August 20, 2025, and the court approved that motion on October 30, 2025.

How do I choose between a claims administrator model and a law firm managed model?

Choose the model that can clearly own notice, validation, exceptions, and audit evidence. If scale, claimant-level status visibility, and closeout reporting are priorities, favor explicit administration operations. If a law-firm-managed approach is proposed, require clear ownership for claim validation, allocation decisions, disputed-claim handling, and accounting or tax records before launch.

What controls prevent duplicate or non-compliant settlement disbursement payments?

Use preflight checks before each batch: approved claimant count, total approved amount, and documented disputed-claim and claim cut-off handling. Then enforce a release gate so late compliance flags can pause the batch. Where blocked-property rules apply, remember the initial reporting deadline can be 10 business days from the block date.

What should finance and engineering monitor daily during a high volume payout cycle?

Track four daily signals: released count, paid count, failed or returned count, and unresolved open balance. Claimant-level or payout-level status is critical when batches partially clear and partially fail. If status changes cannot be tied back to internal records, closeout work becomes more manual.

How should teams handle returned payments, stale claimant details, and unresolved claims?

Handle these as separate exception types with a named owner, contact path, and reissue evidence requirements. Distribution plans can require disputed-claim procedures and a claims cut-off date, so your workflow should preserve those distinctions instead of collapsing everything into retries. Aging by exception category helps keep unresolved items visible after the original batch closes.

What vendor questions best reveal whether a provider can support production grade claims administration?

Ask for artifacts, not promises: a sample payout-status export, an exception log, and an end-of-cycle audit package. Require clear ownership for notice, claim validation, disputed claims, accounting, tax filings, and payment operations, since responsibilities can be split across counsel, administrators, and program offices. Also ask for proof of claimant payment visibility and return handling. Real programs show claimant status lookup and multi-rail payouts such as checks and PayPal, with windows like 90 days for checks and 30 days for PayPal redemption.

Try a related tool

Avery writes for operators who care about clean books: reconciliation habits, payout workflows, and the systems that prevent month-end chaos when money crosses borders.

Priya specializes in international contract law for independent contractors. She ensures that the legal advice provided is accurate, actionable, and up-to-date with current regulations.

Sources

- bsaaml.ffiec.gov/manual/AssessingTheBSAAMLComplianceProgram/03trusted

- cand.uscourts.gov/rules-forms-fees/northern-district-guideline...trusted

- cftc.gov/IndustryOversight/AntiMoneyLaundering/dsio_a...trusted

- cit.uscourts.gov/sites/cit/files/Rule%2023.pdftrusted

- congress.gov/crs-product/IF12763trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-V/part-5...trusted

- fjc.gov/content/judges-class-action-notice-and-claim...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Handle Termination of an International Contractor

When you terminate an international contractor, treat it as a controlled legal and operational event, not a one-off conversation. A messy exit can trigger five risks at once:

FTC Non-Compete Rule Status in 2026 and Freelancer Contract Risk

The practical issue is simple. You can still be asked to sign restrictive language that limits future clients or service lines, even though the federal rule is not in effect. The FTC's 2024 rule was stopped on August 20, 2024, before its planned September 4, 2024 effective date. In 2025, the Commission voted to dismiss its appeal and accede to vacatur, and it later [removed the Non-Compete Rule from the Code of Federal Regulations](https://www.federalregister.gov/documents/2026/02/12/2026-02866/revision-of-the-negative-option-rule-withdrawal-of-the-cars-rule-removal-of-the-non-compete-rule-to) effective February 12, 2026.

How to Handle an EEOC Discrimination Charge

When an **eeoc discrimination charge** arrives, get control of the record before you decide how to respond. The safest sequence is simple. Clean up the documents, build the timeline, confirm the process path, and assign clear ownership.