Quick Answer

Build one weekly benchmark table from conversion rows that are fully traceable. Each row should link provider reference ID, booked rate, reference rate, execution timestamp, route tag, and currency pair; if any of that is missing, move it to exceptions instead of pricing decisions. Then compare bilateral dealing versus competitive routes only under matched size, tenor, and timing conditions. Escalate only persistent adverse variance in high-confidence rows, and use that evidence to renegotiate terms or reroute flow.

Where Conversion Spread Leakage Shows Up#

Small FX costs turn into real margin loss when you repeat them across payout corridors every week. In contractor, creator, and marketplace flows, the problem is rarely one obvious fee. It is the combined effect of spread, markup, and route choice, quietly narrowing platform margin unless you measure conversion cost the same way every time.

This guide gives you a practical weekly sequence. Map the all-in cost, benchmark it against a defensible reference, set decision rules, and then fix the routes and pricing terms that leak the most.

Before you start#

Use this guide if finance, ops, product, and engineering all touch a cross-border transaction, but no one owns a shared weekly view of conversion cost. That shared view matters because benchmark integrity is not just theoretical. The Financial Stability Board noted that concerns about the integrity of FX rate benchmarks were raised in 2013, tied to incentives around benchmark fixings. The practical takeaway is simple: if your reference is weak or inconsistent, your benchmark table can look precise while still pushing you toward the wrong actions.

- Map the all-in cost, not just the visible fee.

Start with every conversion event that affects payout economics and capture the rate you can verify, not the rate a provider markets. FX markup fees are, in plain terms, spreads and other costs added on top of a mid-market exchange rate. Your first checkpoint is whether each booked conversion can be tied to an execution timestamp, a provider reference ID, and the rate actually used. If you cannot tie those fields together, do not treat the result as benchmark-ready.

- Choose a defensible reference rate and freeze the method.

You need one benchmark method that finance and engineering both accept for the review period. The IMF's guidance on FX reference rate determination is useful because it highlights a point many teams miss: there is no one-size-fits-all method. Reference-rate design depends on transaction selection, timing, and data sampling choices. Document your method up front, then hold it steady long enough to compare like with like.

- Compare execution paths, not just providers.

Price moves for more than one reason. The market is fragmented, so effective pricing can differ across routes and timing windows. The BIS has noted that multiple trading venues have increased fragmentation in FX markets, and that execution algorithms are part of how these fragmented markets function. In practice, that means you need to compare execution paths side by side and monitor automation closely enough to catch the risks it can introduce.

- Fix the highest-leakage lanes first.

The goal is not a one-time treasury explainer. It is a weekly operating pattern. Map all-in cost, benchmark against a defensible reference, set decision rules, and then fix routing and pricing where leakage is highest. Keep one evidence pack as you go: raw export rows, reconciliation notes, and a short log of missing or late data. That is what you reach for when a provider challenges your benchmark or when internal teams start arguing over definitions instead of decisions.

Gather the inputs before you benchmark anything#

Benchmark only complete, traceable rows. Start with data completeness before pricing analysis. If you cannot tie each international payment or conversion to core identifiers, execution timing, and a currency pair, you do not have a benchmark set yet. You have a partial export that still needs reconciliation.

| Step | What to capture | Why it matters |

|---|---|---|

| Step 1 | One full-period raw export of every conversion event in the last closed reporting period, including payouts, collections, and treasury transfers | Finance should be able to trace a booked conversion to a raw row, and engineering should be able to trace that row to system records such as an API call, webhook, or settlement record |

| Step 2 | Quoted rate, booked rate, and one reference point at execution time, such as a mid-market rate or interbank exchange rate | Timing matters; if you only have end-of-day reference data, flag those rows as lower confidence |

| Step 3 | Flow type, settlement type such as spot trade, execution method such as bilateral dealing or competitive routing, plus one shared evidence pack | Clean tagging prevents mixed populations, and the reconciliation record gives you something concrete when a provider challenges your numbers |

- Step 1: Pull one full-period raw export of every conversion event.

Use the last closed reporting period and include payouts, collections, and treasury transfers in the same pull. For each row, keep the stable identifiers and timing fields your provider exposes, plus source currency, destination currency, amount, and any quote or booking identifiers. Your first checkpoint is simple: can finance trace a booked conversion back to a raw row, and can engineering trace that same row back to system records such as an API call, webhook, or settlement record?

- Step 2: Capture the rate context you can actually verify.

Keep the quoted rate, the booked rate, and one reference point at execution time, such as a mid-market rate or interbank exchange rate. Timing matters. Some benchmarks summarize only a small slice of the market, and benchmark fixings have drawn scrutiny before, so a loose daily average is a poor substitute for an execution-time reference. If you only have end-of-day reference data, flag those rows as lower confidence rather than blending them into your core comparison set.

- Step 3: Tag the route and build one shared evidence pack.

Mark each conversion by flow type, settlement type such as spot trade, and execution method such as bilateral dealing or competitive routing. Then keep one evidence pack with raw rows, reconciliation notes, and a short data-quality log for missing fields. A common failure mode is arguing over why one route looks expensive when the real issue is mixed populations. Clean tagging prevents that, and the reconciliation record gives you something concrete when a provider challenges your numbers.

Related reading: Same-Day vs Next-Day vs T+2 Payouts and the Real Cost to Your Platform.

Define all-in FX cost so teams stop arguing past each other#

Freeze the vocabulary before you compare prices. Once your rows are reconciled, lock the terms. If finance uses "spread" to mean every rate difference, while procurement uses it to mean market width and ops books fees elsewhere, your benchmark will turn into a naming dispute instead of a cost review.

Start with two buckets#

Start by splitting each conversion into two buckets: market context and provider take. For market context, keep one reference rate at the execution timestamp, not a loose daily average. The point is not to prove a perfect theoretical price. It is to separate normal market movement from what the provider charged on top.

For provider take, use simple internal labels your teams can apply the same way every week, for example:

- reference rate delta

- explicit fee

- markup

Do not force a row into "markup" just because the booked rate is worse than your reference. If the reference came from a different time window, you may be measuring timing effects rather than provider economics. That matters because benchmark fixings have drawn scrutiny, including trading activity around the WMR 4pm fixing window, and concerns about FX benchmark integrity were raised in 2013. Your definition sheet should name the exact reference source and timestamp policy you use.

Checkpoint: for any sampled spot trade, you should be able to show the booked rate, the reference rate used for comparison, the timestamp for both, and where any explicit fee was recorded.

Separate market width from provider take#

If your teams use terms like bid-ask spread and FX margin, define them explicitly in your own internal language and keep those definitions stable across teams. The key is consistency, not a terminology debate mid-review.

That distinction keeps negotiations useful. You are not arguing abstract market microstructure with a provider. You are asking a commercial question: what part of this cost reflects the market at that moment, and what part reflects your contract or routing choice?

Track non-obvious charges as their own fields when they appear in contracts, settlement messages, or post-trade records:

- hidden markup

- correspondent fee

- swap fee

If a charge appears anywhere in the terms or settlement evidence, label it explicitly instead of folding it into a generic spread number.

Freeze the definition sheet for one quarter#

Publish a one-page definition sheet and freeze it for one quarter. Keep it short: chosen reference rate, timestamp rule, how your team defines key terms, which charges count as explicit fees, and how hidden markup, correspondent fee, and swap fee are tagged.

Your evidence pack should include one marked-up sample trade, one contract excerpt or pricing schedule, and one post-trade record showing where each cost element appears. If you later improve the taxonomy, change it at quarter boundaries, not midstream. That is how you keep comparisons over time credible.

Build a weekly benchmark table that survives scrutiny#

Use one weekly table and make it traceable. Once your definition sheet is frozen, turn it into one weekly table and refuse side spreadsheets. The goal is not a pretty report. It is a benchmark view that lets finance, ops, and engineering inspect the same row, trace it back to evidence, and decide whether a price issue is real or just bad data.

Build rows you can defend#

Build the table at the row level you can defend: currency pair plus route identifier, with the execution mode shown explicitly. For each row, keep the volume, observed spread, observed margin, and variance from your chosen reference rate. If you already split reference rate delta, explicit fee, and markup in the prior step, this table becomes the weekly rollup rather than a new calculation exercise.

| Currency pair | Route identifier | Execution mode | Volume | Observed spread | Observed margin | Variance vs chosen reference | Liquidity bucket | Size band | Tenor | Confidence |

|---|---|---|---|---|---|---|---|---|---|---|

| EUR/USD | Route 1 | Mode A | fill from weekly sample | fill | fill | fill | fill | fill | spot or relevant tenor | High/Medium/Low |

| EUR/USD | Route 2 | Mode B | fill from matched sample | fill | fill | fill | fill | fill | spot or relevant tenor | High/Medium/Low |

| USD/MXN | Route 1 | Mode B | fill from weekly sample | fill | fill | fill | fill | fill | spot or relevant tenor | High/Medium/Low |

Do not let the row definition drift mid-quarter. If one team groups by provider and another by corridor only, the benchmark can hide routing effects. The reference source and timestamp rule matter most here. If an external benchmark is part of your method, record its name and timing policy in the table spec, not buried in a separate memo. Benchmark governance is not cosmetic. Regulation (EU) 2016/1011 and the European Commission's 24.7.2020 impact assessment make benchmark continuity, monitoring, and evaluation explicit governance concerns.

Checkpoint: you should be able to click from any weekly row back to the raw trade IDs, booked rate, reference rate, both timestamps, and the record that identifies the route.

Slice only by real price drivers#

Slice the table only by dimensions that plausibly affect comparability in your own book: liquidity bucket, transaction size band, and tenor where relevant. This is where many teams overfit. If you have thin data, three clean bands are better than twelve noisy ones. The benchmark should show whether cost differences persist after controlling for the main commercial and market context, not create a false sense of precision.

Tenor deserves special handling. If a corridor is mostly spot, keep spot together and do not blend it with forward-like or delayed settlement activity just because the currency pair matches. The same applies to transaction size bands. A route that looks expensive on pooled data may simply be taking your smallest or most operationally awkward tickets.

The common failure mode is mixing unlike trades and then calling the result a pricing problem. Another is tagging tenor or size inconsistently because those fields arrive late from providers. Keep a short evidence pack beside the weekly table: raw export, data-quality log, and one sample record for each slice rule so anyone reviewing the row can see how it was assigned.

Compare execution modes on matched conditions#

Compare execution modes only on matched conditions. Put one mode beside another for the same corridor, same timing window, same size band, and same tenor. You are not trying to prove that one route is always cheaper. You are checking whether your routing choice explains recurring variance once the context is held constant.

Add a confidence flag to every row and use it as a gating control, not a cosmetic label. Keep the rule set explicit in your table policy:

- Define what

High,Medium, andLowmean for your data. - Tie each level to documented checks, for example pricing field completeness, timestamp quality, and route clarity.

- Send unresolved rows to an exceptions queue before using them for pricing decisions.

Do not make pricing decisions from low-confidence rows. Park them in an exceptions queue, fix the data, and true them up next week. If you skip that discipline, the benchmark turns into a debate about data quality instead of a decision tool. If you need a refresher on the component math behind the columns, use How to Calculate the 'All-In' Cost of an International Payment first. Then make routing changes.

If you want a deeper dive, read How EOR Platforms Use FX Spreads to Make Money.

Set decision rules your team can run every week#

Act on persistent, matched, evidence-backed variance. With the table in place, stop debating one-off bad fills and decide what happens when a row stays bad. Treat missing benchmark proof as a risk signal, not a neutral gap.

Define escalation triggers from persistent variance#

Start with the corridor rows that show adverse variance versus your chosen benchmark rate under matched conditions. That is the key filter. If you skip normalization for matching conditions, you can end up escalating ordinary market movement as if it were provider markup or execution failure.

Do not invent a universal trigger number. Your own corridors may behave differently by size band and timing window. Instead, finance should approve corridor-specific thresholds and a persistence rule, then apply them only to rows with High confidence and matched conditions. If EUR/USD spot trades on a competitive route and a bilateral route are not matched by size band and timing window, the comparison is not ready for a commercial decision.

Your first escalation options are renegotiation or rerouting. Renegotiation fits when a provider path is still strategically important but repeatedly prices wide after normalization. Rerouting fits when the path is operationally replaceable and the benchmark evidence is strong enough to move flow without guessing.

Checkpoint: before you escalate any row, verify that the evidence pack contains the raw trade IDs, booked rate, benchmark rate, both timestamps, execution mode, and provider-path tag. A common failure mode is acting on a thin benchmark built from a narrow market slice or venue. That is not a theoretical concern. FX benchmarks can be derived from only a small slice of the market, which is one reason benchmark integrity drew formal concern in 2013.

Route matched flow to the better lane and block stale quotes#

If single-provider bilateral dealing is repeatedly worse than competitive paths for matched spot trade windows, move default flow to the competitive lane for that corridor. Do not turn that into a blanket rule for all pairs. Keep a fallback route for coverage gaps, outages, and corridors where the competitive path is thinner or less reliable operationally.

Volatility control belongs in the same weekly rule set because it changes how much confidence you can place in a quoted rate. A 5% swing in GBP/USD can happen in a matter of weeks and can materially impact contract profitability. When execution uncertainty widens, require firm-quote confirmation before booking and reject stale quotes in product logic.

For engineering, that means the API and webhook checks need to be explicit. Do not book a conversion if the quote has no firm validity indicator. Do not book it if accepted time cannot be tied back to the quote record, or if the booking response cannot confirm the final rate used. The document trail should include quote ID, quote creation time, any expiry or validity field the provider returns, acceptance time, booking confirmation, and final booked rate. A common risk is a product flow that caches a quote, waits on user action or downstream checks, then books after the market has moved.

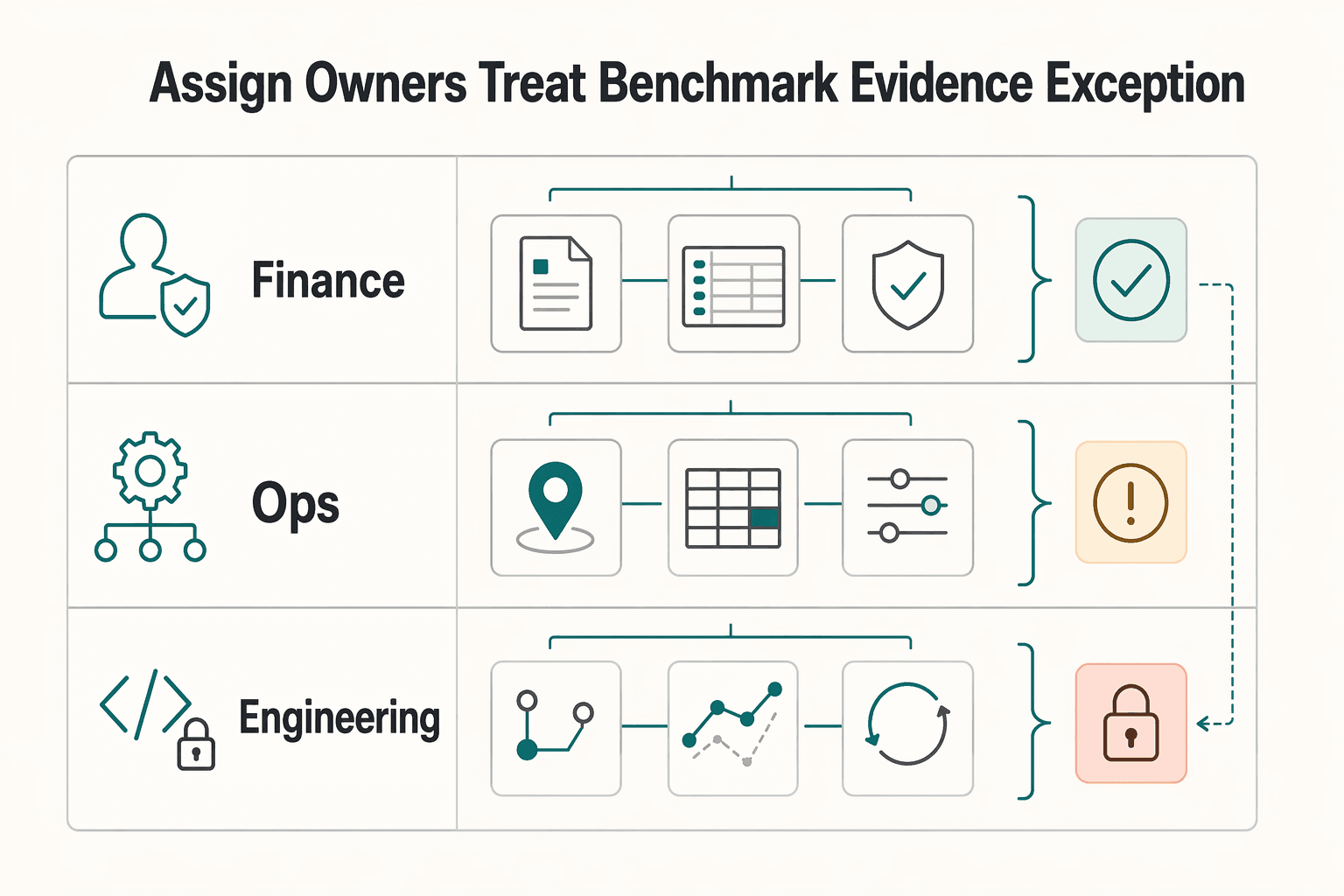

Assign owners and treat no benchmark evidence as an exception#

These rules only hold if ownership is unambiguous. Put them in a documented FX policy with clear governance and delegated authority. If your company already has a board-approved FX policy, this is where the weekly thresholds, rerouting authority, and exception rules should live.

| Team | Weekly responsibility | Key controls |

|---|---|---|

| Finance | Approves variance thresholds, persistence rules, and when renegotiation or rerouting needs sign-off | Thresholds, persistence rules, renegotiation or rerouting sign-off |

| Ops | Monitors exception rows, chases missing evidence, and prevents low-confidence data from being treated as settled fact | Exception rows, missing evidence, low-confidence data |

| Engineering | Enforces quote-validity checks, route defaults, and audit trails across API and webhook flows | Quote-validity checks, route defaults, audit trails |

Treat "no benchmark evidence" as a risk state for any high-volume corridor. If a corridor matters to margin and you cannot show a defensible benchmark row, do not assume pricing is acceptable. Hold it in review, limit unmanaged routing changes, and force evidence collection next week. Reactive spot conversion habits already leave margins exposed to FX swings. Missing proof should raise the temperature, not lower it.

A good weekly outcome is not a long meeting. It is a short list of corridor decisions: keep, renegotiate, reroute, or block pending evidence.

Fix pricing leakage in execution order#

Execution discipline is how you turn weekly FX decisions into real margin protection: fix the biggest corridors first, block stale pricing, route to the proven lower-cost lane, and reconcile booked outcomes back to what your ledger reports.

Step 1: Prioritize corridors by P&L exposure. Start with the highest-volume pairs where adverse spread or markup persists, then move to medium-volume corridors with chronic variance. Do not optimize everything at once. FX execution is now highly electronic and automated, but liquidity is fragmented across venues, so targeted changes are easier to validate and control. Before a corridor enters the fix queue, confirm matched trade IDs, route tags, booked rates, timestamps, and enough volume to separate persistent leakage from noise.

Step 2: Standardize quote capture and expiry handling. Treat stale-quote risk as a control problem, not a market surprise. Require quote-to-book traceability in product logic so accepted conversions are tied to a real quote record, not just displayed pricing. Capture quote ID, quote creation time, any provider validity or expiry field, acceptance time, booking confirmation, and final booked rate. If any link is missing, flag a control exception. Also, do not treat narrow benchmark windows as full-market truth; use them as reference points, then verify against your own quote-to-book trail.

Step 3: Route to the verified lower-cost path, with explicit fallbacks. Default to the lane that performs better under matched conditions, and keep a defined fallback for coverage gaps or provider incidents. In fragmented markets, the cheaper route in normal conditions may not be the most reliable route in stressed conditions. Log every fallback switch so temporary exceptions do not become silent defaults. If you operate under an Order Execution Policy, align routing rules to that policy, especially where product-specific rules take precedence.

Step 4: Reconcile booked outcomes back to platform margin. Close the loop post-trade so margin reflects final execution, not indicative assumptions. Reconcile final booked conversion rate, explicit fees, and route used against ledger margin for the same flow. Your control check should always answer: what rate the customer saw, what rate was booked, and which path produced it. If those do not align, fix the data model before further optimization.

Handle common failure modes and recover fast#

The fastest recoveries come from tighter controls, not new providers: lock one timestamp policy, audit effective spread on "zero-fee" flows, queue late data, and align definitions before review.

Step 1. Enforce one reference timestamp policy. Use one execution-linked event for reference-rate comparisons across finance, ops, product, and engineering. If teams benchmark the same trade at different moments, variance analysis becomes unreliable, especially because some exchange-rate benchmarks can reflect a single venue over a narrow window, including examples built from a two-minute trading period.

For each matched trade, store both the event label and exact timestamp used for the reference pull. If a row cannot be tied to that event, mark it low confidence and exclude it from rerouting or renegotiation decisions.

Step 2. Audit "zero-fee" pricing for hidden markup. Treat "zero fee" as a claim to test, not a cost conclusion. On matched transactions, compare the booked customer rate to the mid-market rate at the chosen timestamp and calculate effective spread.

If adverse spread is persistent on "free" conversions, move that route into pricing review. For consistent cost math, use How to Calculate the 'All-In' Cost of an International Payment.

Step 3. Queue late provider data instead of guessing. When provider data arrives late, hold those trades in an exceptions queue with provisional labels until missing fields arrive. Then true up the record in reconciliation so provisional rows do not become permanent noise in your benchmark set.

Track queue age, missing fields, and owner so unresolved items stay visible and practical.

Step 4. Publish one glossary and require pre-review sign-off. Use one shared glossary for cost terms before quarterly benchmarking reviews so finance and product are not comparing different formulas under the same labels. Keep definitions for mid-market rate, spread, margin, hidden markup, reference window, and booked rate aligned across review decks, SQL logic, and reconciliation notes.

The FX Global Code is useful guidance for integrity and effective market functioning, but it does not itself create legal or regulatory obligations, so internal ownership and sign-off still matter. Related: FX Markup vs. Exchange Rate Spread: How Payment Platforms Price Currency Conversion.

Align finance, ops, and engineering on control points#

You will keep seeing the same FX exceptions until your control points are explicit and consistently recorded. Use the split below as an internal operating model, not an external rule: finance sets policy and approval thresholds, ops handles daily exceptions, and engineering ensures implementation is idempotent and auditable.

Assign ownership by decision type#

Assign ownership by decision type, not by team preference. Define who approves margin and spread exceptions, who resolves operational breaks, and who owns the underlying control logic and audit trail. For every recurring exception, name one approver, one resolver, and one code owner.

Tie each control to stable event labels#

Map controls to stable event labels so teams can diagnose failures the same way. You can use labels such as quote created, quote accepted, conversion booked, payout released, and reversal or return processed, as long as they are used consistently. FX is volatile, and even small timing mismatches can distort FX comparisons.

Preserve end-to-end traceability to ledger posting#

Keep traceability from request through final ledger posting for each disputed cross-border transaction. If a transaction cannot be traced end to end, keep it out of approval and pricing decisions until the record is complete.

Conclusion and copy-paste 30-day checklist#

Do not end this work with a one-time benchmark deck. Close the month by locking definitions, proving data quality, and reconciling booked conversions back to reported performance metrics. Treat the checklist below as an operating pattern you can copy into your team doc, not as a market standard.

| Week | Action | Verification or risk |

|---|---|---|

| Week 1 | Lock terms and owners | Verification: a random sample of transactions should show the same labels and formulas in finance reporting and product logs. Red flag: teams still say 'spread' when they mean provider markup. |

| Week 2 | Build the benchmark table by currency pair and mark confidence | Verification: each high-confidence row should tie back to raw transaction evidence and a clear execution event. Failure mode: mixing quote times, acceptance times, and booking times in the same comparison window. |

| Week 3 | Apply decision rules and write down exceptions | Verification: every exception should name an owner, a fallback path, and the evidence for keeping it. Red flag: temporary manual overrides with no expiry date. |

| Week 4 | Reconcile outcomes and set the next cycle | Verification: disputed rows should be traceable from quote created to conversion booked to downstream reporting impact. |

- Week 1: lock terms and owners.

Freeze your internal definitions for core FX rate, spread, and margin terms for the next month so finance, ops, and engineering stop measuring different things. Publish one owner per field set and one source of truth for quote timestamp, booked timestamp, provider reference ID, quoted rate, booked rate, reference rate, and explicit fee fields. Verification point: a random sample of transactions should show the same labels and formulas in finance reporting and product logs. Red flag: if teams still say "spread" when they mean provider markup, your week 2 table will not be trustworthy.

- Week 2: build the benchmark table by currency pair and mark confidence.

Create one benchmark view by currency pair and provider path, then add a confidence flag based on timestamp quality and field completeness. Your first goal is not elegance. It is to isolate the corridors where leakage is material and well evidenced. Verification point: each high-confidence row should tie back to raw transaction evidence and a clear execution event. Failure mode: mixing quote times, acceptance times, and booking times in the same comparison window. Benchmark-integrity concerns in FX are not theoretical; the FSB noted such concerns in 2013, and its recommendations span benchmark calculation, market infrastructure, and market-participant behavior.

- Week 3: apply decision rules and write down exceptions.

Use the benchmark to decide which corridors or provider paths need policy review, pricing discussion, or tighter quote-age controls based on your own operating model. Keep the exception list explicit: coverage gaps, provider incidents, low-confidence corridors, and any cases where execution constraints require temporary alternate handling. Verification point: every exception should name an owner, a fallback path, and the evidence for keeping it. Red flag: "temporary" manual overrides with no expiry date.

- Week 4: reconcile outcomes and set the next cycle.

Compare actual booked conversion results to reported performance metrics and note where assumptions broke down. Review the month's failure modes, especially hidden markup, stale pricing, and late provider data, then carry only the unresolved items into the next monthly cycle. Verification point: disputed rows should be traceable from quote created to conversion booked to downstream reporting impact. A useful control reference here is the ISDA Suggested Operational Practices, updated February 24, 2026, which explicitly calls out data availability, integrity, validation, and response timing.

If you need implementation support, validate corridor coverage and control points with your provider team before rollout. That means confirming which corridors support your chosen routing path, what evidence they can return on each conversion, and how exceptions will surface when data arrives late or incomplete. If that evidence pack is weak, delay rollout and fix observability first.

For a step-by-step walkthrough, see How to Handle Currency Gain and Loss Reporting for a Multi-Currency Platform.

Frequently Asked Questions

What is the practical difference between FX spread, FX margin, and bid-ask spread for a platform team?

Treat FX margin as the extra charge your bank or provider adds on top of the trade. Keep that separate from the market-driven rate component. In plain terms, margin is the commercial take. If your reporting mixes those components, pricing decisions get harder to diagnose.

Which FX costs can we actually control, and which are outside our control?

You do not control the underlying rate of exchange, because rates are primarily market-driven. Margins added on top of rates are within provider or bank control, and you can influence them through provider choice and agreed terms. A useful checkpoint is clear disclosure of reference rate, booked rate, and fee fields; if key fields are missing, treat that row as low-confidence evidence.

How do we benchmark conversion cost if we only have partial real-time market data?

Be honest about the limit. Without accurate real-time market data, it is very difficult to get a clear picture of business FX rates. In that case, benchmark only the rows where timing and reference-rate data are reliable, and mark the rest as low confidence rather than averaging everything together.

How do we tell whether our margin on a currency pair is fair without overfitting to one week?

Do not chase a universal "fair" threshold, because none is supported here. Instead, compare the same currency pair over several weekly periods, segmented by transaction size, liquidity, and tenor. Lower-liquidity pairs and longer tenor are associated with higher margins. If adverse variance persists across matched weeks, renegotiate or reroute.

When does multi-bank dealing platform routing outperform bilateral dealing enough to justify added complexity?

No general result is supported here that multi-bank dealing platform (MDP) routing outperforms bilateral dealing by default. Treat it as a testable hypothesis: justify the added complexity only when your own like-for-like data shows repeatably lower all-in conversion cost, or better execution coverage, for the same corridor and timing window.

What are the clearest warning signs of hidden markup in "low-fee" conversion offers?

A key warning sign is a provider advertising zero or very low fees while the booked rate consistently lands well away from your reference rate. FX markup can be embedded in the rate itself, so ask for the quote, booked rate, provider reference, and any fee schedule in one evidence pack. If they cannot show how the price was formed, treat the offer as opaque.

Try a related tool

Ethan covers payment processing, merchant accounts, and dispute-proof workflows that protect revenue without creating compliance risk.

Sources

- bclawreview.bc.edu/articles/543/files/63ad48fbe15b9.pdftrusted

- bis.org/publ/mktc13.pdftrusted

- bis.org/publ/bppdf/bispap104.pdftrusted

- businesslawreview.uchicago.edu/print-archive/event-contracts-are-step-too-f...trusted

- cftc.gov/sites/default/files/idc/groups/public/@newsr...trusted

- cftc.gov/sites/default/files/idc/groups/public/@swaps...trusted

- ecfr.gov/current/title-12/chapter-II/subchapter-A/par...trusted

- elibrary.imf.org/display/book/9798229023184/CH002.xmltrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How EOR Platforms Use FX Spreads to Make Money

You can control more of your payout outcome than it first appears. As the CEO of a business of one, separate unavoidable costs from avoidable ones, then manage the compliance exposure that cross-border money movement creates.

How to Calculate the All-In Cost of an International Payment

Headline fees can understate true cost. The figure that protects margin is the net amount that lands with the recipient after conversion, transfer charges, and any downstream deductions.

How Payment Platforms Really Price FX Markup and Exchange Rate Spread

Platform teams can underprice cross-border payouts because they start with visible `transaction fees` and transfer charges, while the rate-layer cost sits inside the conversion rate. Transfer fees are the easiest line item to spot, but exchange-rate margin can be charged separately and may not appear in that fee line at all.