Quick Answer

Use a fixed reward tied to one provable event, then release payment only after that event is recorded. The RemoFirst example in the article uses a $500 referral reward triggered when the referred client starts paying, not at form submission. That structure reduces low-intent volume, limits duplicate-claim disputes, and gives Finance a clean approval path tied to realized value.

What a Contractor Referral Program Needs to Work#

If your goal is real contractor growth without giving back margin, tie rewards to a qualifying event you can prove. Teams break referral plans by paying too early, using fuzzy definitions, or copying a generic template that grows submissions faster than profitable supply.

A public example makes the point better than theory. RemoFirst advertises a fixed $500 reward for referrals, but not when someone fills out a form. The payout is triggered only once the referred client starts paying through RemoFirst. That is the part worth copying. Not the dollar figure, but the discipline of a clear trigger linked to revenue. A fixed reward can work well when your onboarding path is predictable and you can tell, with very little debate, whether a referral actually became productive.

Another pattern is commission-style partner positioning. Variable payouts can feel safer when referral quality is uneven because cost moves with conversion. In practice, it works only if your tracking is mature enough to prove who referred whom, what converted, and when commission was actually earned. Without that, a variable model may not protect unit economics.

So this guide stays focused on one operating outcome: grow contractor supply while protecting unit economics with explicit payout triggers, controls, and verification steps. That means you should decide your qualifying event before you write promo copy. If you cannot answer "what exact event releases payment?" in one sentence, you are not ready to launch.

There is also a useful verification lesson in the RemoFirst flow. After form submission, it says it emails the client contact and CCs the referrer. That small detail creates visible evidence that the referral was received and routed. You do not need that exact mechanism. You do need something equivalent: a timestamped intake record, a first-submission rule, and a later status change that proves the trigger happened.

One failure mode is paying on lead submission because it feels easy. That can lift volume, but it can also invite duplicate claims, low-intent referrals, and disputes when Finance asks what, exactly, was purchased or activated. The rule to remember: do not promise a reward until you can verify the event that earns it and reconcile that event back to margin.

Choose the payout model that matches your margin reality#

Choose the model your records can prove, not the one that sounds more advanced. If onboarding criteria are strict and outcomes are predictable, start with a fixed bounty tied to a clear trigger, for example completed onboarding or first paid engagement. If lead quality varies and you can reliably track source, conversion, and earned payout, test a variable commission through a Client Referral Program or Industry Consultant Partnership.

Do not set payout economics from a Reddit or r/Contractor success story. Forum anecdotes are useful for spotting abuse patterns, not for setting benchmarks.

Step 1 Choose fixed unless your tracking can support commission#

A fixed bounty is usually the safer starting point because it uses one qualifying event, one verification step, and one payout decision. This is easiest to run when accepted referrals are relatively similar in value.

Use commission when payout should move with conversion value and your attribution is mature. Poor commission design can distort pipeline quality, weaken forecasting, and slow growth, so this model only works when ownership and event tracking are clean.

Checkpoint before choosing commission: can you prove the chain from referrer -> referred contractor -> conversion event -> payout approval without manual reconstruction? If not, it is too early for commission.

Step 2 Match the model to margin, activation, and timing risk#

Fixed bounty puts more timing risk on you because cost is committed once the trigger is met. That tradeoff is often acceptable when margin per activated contractor is healthy and activation is steady.

Variable commission puts more timing risk on the referrer because payout depends on later conversion. That can protect margin when quality is uneven, but only if source attribution and status records are durable. If Finance is reconciling from spreadsheets and ad hoc approvals, operational and compliance exposure rises.

Commission also increases record-keeping complexity because the earning event usually happens later. If onboarding, tax collection, or compliance workflows are still loose, fix that process first.

Step 3 Use a simple matrix before writing policy#

| Gross margin per contractor | Expected activation rate | Payout timing risk | Better starting model | Why |

|---|---|---|---|---|

| Healthy and consistent | Predictable | Low | Fixed bounty | Simple trigger, fast verification, easier reconciliation |

| Uneven by role | Mixed | Medium | Fixed bounty with later trigger | Keeps rules simple while reducing early payout risk |

| Sensitive or hard to predict | Volatile | High | Variable commission | Lets payout follow realized conversion value |

Before launch, test recent referrals or applications and confirm you can identify source, first submission, qualification result, and activation date from existing records. If you cannot, stay with a fixed model and a later payout trigger.

Define minimum policy rules before you promise any reward#

Before launch, lock the policy in writing so eligibility, qualification, and disputes are decided from records, not memory.

| Rule area | What to define | Control |

|---|---|---|

| Eligibility | Who can refer, who cannot, what counts as a new referral, and how first submission is determined | Use one intake record and consistent event history for each referral |

| Qualifying event | Pick one reward trigger and keep the wording identical across the policy page, intake form, approval queue, and payout notice | Add a terms-precedence line so the current written policy supersedes earlier explanations |

| Exceptions and disputes | Create a short appendix for verification and dispute resolution procedures | No manual payout without a journal entry, evidence reference, and named approver |

Step 1 Lock eligibility before you open the program#

Define who can refer, who cannot, what counts as a "new" referral, and how first submission is determined when two people claim the same contractor. Keep participation rules and qualification rules separate so operators are not mixing access rules with payout approval rules.

Use one intake record and consistent event history for each referral. If a reviewer cannot resolve eligibility from the written policy and the record trail, tighten the policy before launch.

Step 2 Choose one qualifying event and use the same wording everywhere#

Pick one reward trigger and keep it identical across the policy page, intake form, approval queue, and payout notice. Whether you choose viable lead, completed onboarding, or first paid engagement, consistency is what prevents conflicting promises across teams.

Add a clear terms-precedence line so the current written policy supersedes earlier oral or written explanations. This reduces later disputes over which promise controls.

Step 3 Document exceptions and disputes for auditability#

Create a short appendix for verification and dispute resolution procedures, then route every approval, denial, and exception through it. For each decision, log the reason in Ledger Journals and attach the related API event records so Finance and Ops can trace what happened.

Set a hard control: no manual payout without a journal entry, evidence reference, and named approver. This reinforces transparency and fair treatment when disputes arise.

This pairs well with our guide on Build a Freelance Referral Program Without Payout Disputes.

Prepare prerequisites and operating artifacts before launch#

Do not launch until one packet can answer operator questions without side messages or tribal memory. If Finance, Ops, and Product are not using the same current documents and the same approval owner, exceptions turn into policy debates.

Step 1 Assemble a single launch packet#

Create one versioned packet with four items: referral policy, payout terms, dispute process, and a named approval owner. Keep the structure explicit: scope, applicability, then decision owner. FAR Part 31 models this clearly by separating 31.000 Scope of part from Subpart 31.1 - Applicability instead of blending both.

Your checkpoint is simple: can Finance approve or deny a case from the launch packet alone? If policy lives in one place, payout terms in another, and exceptions in chat, you are not ready.

Step 2 Draw the process and flag open capability gaps#

Document the process as a flow chart or diagram before launch. PHMSA explicitly asks for a "flow chart or diagram that describes processes that will be followed," and the same discipline prevents handoff confusion in referral operations.

Use that diagram to mark what is live versus still pending in your operating setup. If any required step is not ready, label it as a gap and assign an owner.

Step 3 Record unresolved legal and tax questions in writing#

Write unresolved legal and tax questions directly into the packet instead of leaving them implied. Treatment can vary by jurisdiction, and the current evidence does not settle those rules.

If a market is still under review, state that plainly and assign an owner and target date for resolution. That is safer than ad hoc local interpretation once approvals begin.

We covered this in detail in How to Launch a Referral Program for Your Gig Platform with Built-In Commission Tracking.

Build the referral-to-payout sequence with hard checkpoints#

Build this sequence as a controlled handoff chain: one intake record, one qualification decision, one verified payout trigger, and one reconciled payout record.

| Stage | Required action | Checkpoint |

|---|---|---|

| Intake | Use one intake schema, capture needed identifying and consent fields, and assign an immutable referral ID | Run duplicate checks before review using one documented method |

| Qualification | Route accepted referrals through a shared status model and log a concrete reason each time status changes | Keep reason categories standardized so another operator can reconstruct the decision |

| Activation trigger | Release payout only after the single defined trigger is verified against the referral record | Confirm the referral has not already been paid and lock state before approval |

| Reconciliation | Settle approved rewards in batches and reconcile outputs back to the referral and accounting records | Treat any missing link as an open exception and review exceptions on a fixed cadence |

Step 1 Intake: standardize fields, then screen for duplicates#

Use one intake schema across every submission path so matching and review stay consistent. Capture only the fields you need to identify parties, document consent, and preserve submission order, then assign an immutable referral ID.

Run duplicate checks before review using one documented method applied the same way every time. If a case needs an override, require a short evidence trail so the exception is explainable later.

Step 2 Qualification: route decisions with clear pass/fail reasons#

Move accepted referrals through a shared status model and log a concrete reason each time status changes. Keep reason categories standardized so a second operator can reconstruct the decision without side messages.

That consistency matters: standardized categories make review and later checks easier, while vague labels create payout disputes later.

Step 3 Activation trigger: pay only after the chosen event is verified#

Release payout only after the single trigger your program defines is verified against the referral record. Before approval, confirm the referral has not already been paid and lock state to prevent duplicate rewards.

After approval, post the accounting record in your system, attach the key identifiers, and notify both parties of the outcome.

Step 4 Reconciliation: settle in batches and close exceptions on a fixed cadence#

Settle approved rewards in batches, then reconcile batch outputs back to the referral and accounting records. Treat any missing link as an open exception, not a soft pass.

Use a fixed exception-review cadence and watch trend direction. If exceptions rise, pause new referral intake and fix matching and routing logic before you increase incentives.

If you want to reduce payout friction without losing control, see Invisible Payouts: How to Remove Payment Friction for Contractors Without Sacrificing Compliance.

Add compliance and tax gates that do not break conversion#

Keep intake light, but make payout release a hard compliance checkpoint. Collect core identity data at referral submission, then require all higher-friction checks before the payment instruction is created.

| Review area | What to do | Key detail |

|---|---|---|

| Compliance gate | Add a compliance-hold state before payout approval and run KYC, KYB, or AML review on the payee if required | Every paid referral has either a passed review or a documented, owner-approved exception |

| Tax documents | Set an internal decision table for W-8, W-9, 1099, and FBAR-related handling before launch | Record the form type, collection date, named payee, and referral ID |

| FEIE | Route FEIE questions to tax handling review instead of relaxing documentation | Physical presence test: 330 full days during 12 consecutive months; FEIE maximum $130,000 per qualifying person (2025) and $132,900 per person (2026) |

| VAT checks | Validate VAT details before release only where the payment structure makes VAT treatment relevant | If treatment is unclear for a market, pause launch for that market until the rule is documented |

Step 1 Lock the gate before money moves. Use the same approval checkpoint from the prior section and add a compliance-hold state before payout approval. If your market or program requires KYC, KYB, or AML review, run it on the payee tied to the reward before payout is sent. Your control test is simple: every paid referral has either a passed review or a documented, owner-approved exception.

Store separate records for each payout party. Keep the referring contractor, referred contractor, and any business entity distinct so one party's review result is never reused for another by accident.

Step 2 Define tax-document handling early. Exact workflow rules or thresholds for W-8, W-9, 1099, and FBAR-related handling are not established here. Do not guess. Set an internal decision table with your tax owner before launch: who provides what, when collection is due, and whether payout is blocked if documentation is incomplete.

At minimum, record the form type, collection date, named payee, and referral ID. Keep referral rewards and contractor service payments as separate policy and ledger streams so treatment remains explainable.

Step 3 Treat FEIE as a review topic, not a shortcut. If someone raises the Foreign Earned Income Exclusion, route it to tax handling review instead of relaxing documentation. The IRS states FEIE applies only to a qualifying individual with foreign earned income, and that income still must be reported on a U.S. return.

Under the physical presence test, the person must be present in a foreign country or countries for 330 full days during 12 consecutive months, and those days do not have to be consecutive. The FEIE maximum is $130,000 per qualifying person (2025) and $132,900 per person (2026). If your team references IRS LB&I practice materials, treat them as context only; the cited unit says it is not an official pronouncement of law.

Step 4 Use VAT checks only where your structure makes them relevant. VAT validation rules are not established here. Keep your policy narrow: if a referral reward is paid through a structure where VAT treatment may apply, validate VAT details before release and keep that review separate from contractor service-payment handling. If treatment is unclear for a market, pause launch for that market until the rule is documented.

For a step-by-step walkthrough, see How to Build a Trust and Safety Program for Your Contractor Marketplace.

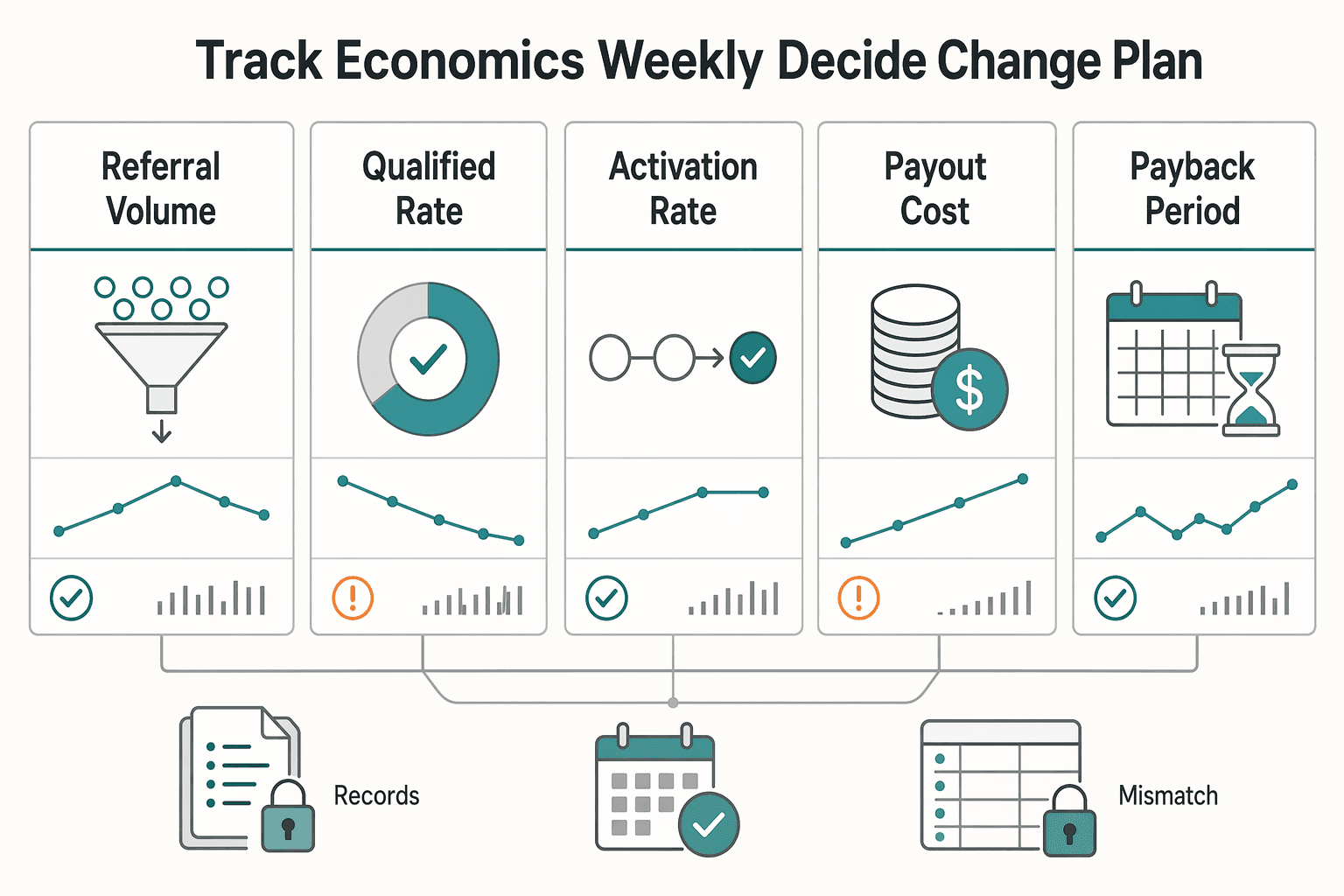

Track economics weekly and decide when to change the plan#

Use one auditable weekly scorecard, and change definitions before you change reward size. If qualified rate falls while payout cost rises, treat it as a control problem first.

Step 1 Build one scorecard with fixed definitions. Track referral volume, qualified rate, activation rate, payout cost, and payback period, split by channel and model type. Lock denominator definitions once, document them, and keep Finance, Ops, and Growth on the same logic.

| Metric | Split by | Why it matters |

|---|---|---|

| Referral volume | Channel, referrer cohort | Shows intake quality shifts |

| Qualified rate | Channel, role type | Tests eligibility and trigger quality |

| Activation rate | Model type, channel | Confirms downstream conversion |

| Payout cost | Fixed bounty vs commission | Shows margin pressure |

| Payback period | Channel, model type | Shows recovery speed |

Step 2 Keep the event trail verifiable. For sampled paid referrals, confirm the full path in your records: referral created, qualification result, activation event, payout approval, payout sent, journal posted. If Webhooks and Ledger Journals cannot support that trace, do not use the trend to justify plan changes.

Step 3 Track failure indicators as core metrics. Treat duplicate claims, manual overrides, payout retries, and webhook mismatches as control signals, not support noise. Keep both pre-release checks and post-settlement checks so you can catch failures before payout and detect silent issues after payout.

Step 4 Change rules before raising rewards. When qualified rate drops and payout cost climbs, tighten eligibility, duplicate logic, and trigger definitions first. Raising incentives before fixing definitions usually scales low-quality intake and increases manual review load.

Need the full breakdown? Read How to Build a Gig Platform Referral Commission Model That Protects Margin.

Common mistakes and how to recover fast#

When controls break, recover like a corrective-action workflow: verify the error, then change the rule before more payouts go out.

- Mistake: paying on lead submission only.

This usually buys volume before quality. Move the trigger to completed onboarding or first engagement, set an effective date, and state how in-flight referrals are handled.

- Mistake: no duplicate policy.

This turns normal overlap into payout disputes. Enforce a first-submission rule and publish the evidence standard tied to API logs so decisions are consistent.

- Mistake: Finance cannot reconcile payouts.

Do not release rewards until each payout maps to a payout ID, the related Payout Batch, and Ledger Journals. If that chain is incomplete, hold release and fix reconciliation first.

- Mistake: compliance is bolted on late.

Put KYC/KYB/AML checks before payout approval and reroute pending cases to review. If you reference legal language in policy updates, do not treat FederalRegister.gov prototype/XML text as official legal notice.

Conclusion#

Paying more is not always the fix. The referral program that tends to hold up has payout mechanics your margin can absorb, one trigger people can verify, and controls tight enough that Finance is not cleaning up exceptions every week.

Referrals can be useful. One source describes them as especially strong leads, and construction hiring guidance points out that referral programs can speed hiring and improve the odds of cultural fit. That upside can disappear when your reward rule is vague, your hiring flow is unstructured, or your payout record cannot be defended later. The practical next step is to turn the policy into an operating checklist before you invite a single referral.

Copy and adapt this launch checklist#

Step 1. Write the model choice and trigger in one paragraph. State whether you are paying a fixed reward or a variable amount, then name the single event that unlocks payment. Your verification point is simple: if an ops lead, recruiter, and Finance owner explain the trigger differently, you are not ready to launch.

Step 2. Publish eligibility, duplicate, and approval rules before inviting referrals. Define who can refer, what counts as a new referral, and who has final signoff. The failure mode here is predictable: duplicate claims, retroactive exceptions, and arguments over candidates who were already in process.

Step 3. Attach the referral path to a structured hiring process. This matters more than the incentive amount. A structured process helps you identify skilled labor quickly, and it gives you pass or fail reasons you can point to later when a reward is approved, denied, or delayed.

Step 4. Make reconciliation boring before you scale volume. Keep one record for each referral from submission through payout approval and payment completion. The checkpoint is that every paid reward ties back to one policy rule, one qualifying event, and one approval record with no manual guesswork.

Step 5. Check legal and tax requirements for your market before launch. Do not assume one global treatment. Requirements can vary by market and program, so document what applies before launch.

Step 6. Review economics weekly and tighten policy before raising incentives. Track referral volume, qualified rate, payout cost, and exception count. If quality drops while payout cost rises, do not respond by increasing the reward. Tighten the trigger, narrow eligibility, or improve screening first.

The practical rule to keep#

Treat referral rewards as part of compensation design, not as a shortcut for weak recruiting operations. Market awareness still matters, and regular salary benchmarking helps keep compensation competitive. Start with a policy you can explain, verify, and reconcile. Raise incentives only after the numbers show that the channel is producing quality without eroding margin.

Related reading: How to Create a Referral Program for Your SaaS Product.

Frequently Asked Questions

What is a contractor referral program in practical operating terms?

In practice, it is a structured way to source new contractor candidates through recommendations from people you already work with. The key parts are simple: who can refer, what counts as a valid new referral, what milestone unlocks payment, and who approves the payout. If those four points are vague, you do not really have a program yet.

Should we pay a flat referral bonus or a commission to existing contractors?

Start with a flat bonus when your qualifying event is clear and discrete, such as completed onboarding or first engagement. A commission only makes sense if you can reliably define the base, the percentage, the payment period, and the exclusions in writing. If you cannot explain the calculation in one short paragraph, choose the fixed amount.

When should a referral payout trigger: lead, onboarding, or first engagement?

The cleaner choice is onboarding or first engagement, not raw lead submission. One referral-program guide notes that successful programs often tie rewards to both hire and retention milestones, with examples like a lump sum after 90 days or 6 months or staggered payouts such as 50%/50%. If quality risk is high, pay later and tie at least part of the reward to retention.

What rules reduce duplicate or fraudulent referral claims?

Publish a first-submission rule and define what "new" means before launch. Also consider excluding HR personnel, senior leadership, and direct hiring managers to reduce conflicts of interest, as one referral-program guide recommends. A practical check is whether the referral was submitted before the candidate was already under review. A common risk is paying after the person was already in process.

How much should we pay if public benchmark data is thin?

Use public examples carefully. One source cites $250 to $5,000 as a broad referral-bonus range by role and industry, but that is not a universal contractor benchmark. If your data is thin, start with a conservative fixed reward, connect it to a real milestone, and review whether the activated contractor value justifies it after a few payout cycles.

Do referral payouts require different compliance or tax handling across markets?

Yes, you should assume local review is needed rather than copying one global rule. The evidence here does not support a single tax treatment across jurisdictions, and regulated contexts can change the analysis. For example, California public-works scope includes work done under contract and paid wholly or partly with public funds, which is a reminder not to import private-program assumptions into every market.

How do we run referral payouts at scale without losing auditability?

Standardize the record you keep for every payout: referrer, referred contractor, qualifying milestone, approval date, payment date, and exception reason if anything was overridden. Your verification checkpoint is straightforward: every paid reward should tie back to one written policy rule and one completed milestone. The red flag is manual exceptions piling up outside the policy, because that is usually where disputes and cleanup start.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/far/part-31trusted

- acquisition.gov/far-overhaul/far-part-deviation-guide/far-ov...trusted

- courts.ca.gov/system/filestrusted

- dir.ca.gov/dlse/faq_independentcontractor.htmtrusted

- eda.gov/strategic-initiatives/disaster-recovery/supp...trusted

- epa.gov/system/files/documents/2023-07/Community-Gra...trusted

- federalregister.gov/documents/2011/09/16/2011-23695/medicaid-pro...trusted

- gao.gov/assets/a302564.htmltrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Best Way to Pay a Team of Contractors in Latin America

If you need to pay contractors in Latin America without cashflow surprises, start with risk, not convenience. Cross-border payouts can break on delays, hidden FX loss, or compliance friction, so the cheapest-looking option is not always the safest one to run.

Invisible Payouts: How to Remove Payment Friction for Contractors Without Sacrificing Compliance

Invisible payouts should make life easier for contractors without hiding the controls your team needs. Contractors should get a predictable, low-friction flow, while internal teams can still enforce and document payout decisions when needed. If you run contractor payouts at scale, you need both outcomes at once. We recommend treating every easy payout as a controlled release path your team can replay later.

Paying Unbanked Contractors in Developing Markets: Best Payout Routes for Platforms

If your team needs to send money to contractors, creators, freelancers, marketplace sellers, or other non-payroll recipients across borders, the payout decision can look deceptively simple at first. On paper, you are choosing a payment rail. In practice, you are choosing an operating model that affects onboarding, compliance, support load, engineering effort, treasury visibility, failure recovery, and the degree of legal risk your company is willing to carry.