Quick Answer

File Form 8802 with the required fee to request irs form 6166, then track status and validate the issued certificate before sharing it abroad. Use the certificate for residency proof tied to treaty or other foreign tax-benefit requests, not as evidence for a foreign tax credit claim. If your destination country has extra acceptance rules, confirm those in writing before filing so you avoid rework after issuance.

Start Here and Avoid the Costly Mistakes#

Start with purpose, not paperwork. Before anyone opens Form 8802, get clear on why the foreign payer or tax authority wants a U.S. residency certificate. That answer drives almost everything that follows: whether you should file at all, how the request should be framed, what tax period matters, and how much lead time you really need. If the reason stays vague, the rest of the process gets expensive fast.

The cleanest way to manage this is to split the work into two lanes from the start. One lane is the IRS request itself. That part is stable. The certificate is the IRS residency certification letter on U.S. Department of the Treasury stationery, Form 8802 is the required application path, and a user fee applies to each submission. The other lane is live verification. Foreign acceptance can vary by country and by the authority asking for the document, so you need to recheck current IRS instructions, processing status, fee details, and timing right before filing.

That separation matters. A lot of avoidable trouble starts when people treat the certificate as the whole assignment. It is not. You can complete the IRS piece correctly and still miss the real business deadline if nobody checked live processing conditions or whether the destination country wants extra steps after issuance. In practice, the IRS application is usually the easy part. The risk sits in timing, purpose, and destination-country acceptance.

Another common failure mode is trying to solve uncertainty by filing early. That usually makes it worse. If the foreign side has not clearly said what benefit it is granting, or if your team has not nailed down the needed tax period, you are not saving time by submitting. You are just moving confusion into a paid filing.

Use these checkpoints before you do anything else:

-

Define the exact foreign-side request. Get the payer or authority request in writing and keep the language explaining the purpose, such as treaty relief. If you cannot point to one clear message explaining why the certificate is needed, you are not ready to file. Filing first and clarifying later usually creates rework.

-

Lock the IRS facts that do not change. Make it clear in your internal notes that there is no alternate IRS route. The certificate comes from the IRS, it is issued on Treasury stationery, and the application path is Form 8802.

-

Keep stable facts separate from live checks. Stable facts include the basic role of the certificate and the known 2024 signature issue discussed later in this article. Live checks include the latest Instructions for Form 8802, Processing status for Form 8802, current fee details, and current timing guidance. Put those on separate checklist lines so nobody treats a changing item as fixed.

-

Set timing checkpoints before submission. Plan with buffer, not optimism. The IRS says to mail Form 8802 with the full user fee at least 45 days before you need the certificate, and says it will contact you after 30 days if a delay is expected. If an individual plans to use a mobile filing path, verify current eligibility before relying on it.

If different people share the work, assign one owner to confirm purpose and another to verify filing-day details. That keeps accountability clear and makes it much easier to spot whether the risk is substantive or just operational. If this certificate request is one piece of a larger cross-border tax project, The Ultimate Digital Nomad Tax Survival Guide for 2025 covers the wider context.

With that foundation in place, the next question is straightforward: confirm that this certificate is actually the right tool for the job before you invest more time in the application.

Do You Actually Need Form 6166 for This Client or Country#

Do not file just because someone abroad asked for "tax paperwork." The certificate is the right path when the real request is proof of U.S. residency for income tax treaty benefits. If that use case is not clear in writing, you are still scoping the assignment, not preparing an application.

| Issue | Path | Note |

|---|---|---|

| Treaty relief | Form 8802 | Residency certificate lane |

| Foreign tax credit | Form 1116 | Individuals, estates, and trusts |

| Foreign tax credit | Form 1118 | Corporations |

| VAT relief | Destination-country check | Acceptance depends on local rules |

Most confusion comes from mixing different tax tasks into one bucket. Treaty relief points to the residency certificate path. A foreign tax credit is a separate U.S. filing issue, so sending a residency certificate does not solve it. VAT relief sits in a third lane. The certificate may be accepted in some places, but that is a local acceptance question, not something to assume from the IRS side.

This distinction is where a lot of rework starts. A foreign payer may ask for a "tax certificate" or "residency proof" without telling you whether the real issue is treaty withholding, VAT treatment, or support for a different local filing. Until you translate that broad label into the actual benefit being claimed, you cannot tell whether the certificate, a foreign tax credit filing, or a local VAT process is the real answer. Filing while that point is fuzzy is usually just paying to guess.

Work through the classification in this order:

-

Confirm the purpose in writing. Get a clear statement from the foreign payer or authority about the benefit being claimed and keep that wording in your file. If the request is treaty-based, move forward. If the language is vague, stop and clarify instead of guessing.

-

Match the request to the right IRS path. To get the certificate, you submit Form 8802. If the real issue is a foreign tax credit, the forms are different: Form 1116 for individuals, estates, and trusts, or Form 1118 for corporations. The IRS notes there can be exceptions to filing Form 1116 in some cases.

-

Treat VAT relief as a destination-country check. The certificate can be used for income tax treaty benefits and certain other foreign tax benefits, but VAT-exemption acceptance depends on local rules. Confirm that acceptance before you spend time on the IRS application.

-

Escalate conflicting instructions early. If payer instructions and country guidance do not line up, get tax advice before submitting anything.

Use that sequence as your go/no-go test. If you have a clear written purpose and it matches the residency-certificate lane, keep going. If the foreign side is mixing labels or asking for several things at once, pause until the request is sorted. In practice, that pause saves time because it keeps you from building the wrong packet.

Once you know the request belongs in this lane, the next step is to get equally clear on what the document actually proves and what it does not. That boundary matters because it shapes both the application language and the expectations you set with the foreign side.

What Form 6166 Proves and What It Does Not#

Be precise about scope. The certificate is an IRS certification letter on U.S. Department of the Treasury letterhead confirming that the listed person or entity is a U.S. resident for U.S. income tax law purposes. That is why foreign payers and tax authorities ask for it when treaty benefits are on the table, and why many treaty partners accept it for that purpose. The IRS also notes that it may be used for certain other foreign tax-administration purposes.

Just as important, it does not prove U.S. tax payment. If the real need is support for a foreign tax credit claim, this is the wrong document for the job. That path runs through Form 1116 for individuals, estates, and trusts or Form 1118 for corporations, with the IRS noting there can be exceptions to filing Form 1116 in some cases.

That difference is more than semantics. If you send a residency certificate to answer a tax-paid question, the foreign side may still come back for different proof, and your U.S. filing work may still be incomplete. You end up doing two jobs instead of one because the first document never matched the actual issue. The clean rule is simple: if the foreign side needs residency proof for treaty treatment, use the certificate path through Form 8802. If the issue is a foreign tax credit, use the credit-form path instead.

This is also why purpose language matters later on. The document itself has a defined role, so your application and handoff should describe that role clearly instead of treating it like a generic tax letter. A vague request can sometimes be clarified early. A vague filing usually just creates questions later.

Once the document's scope is settled, the work becomes operational. The next task is to assemble a packet that tells one coherent story about one applicant, one purpose, and the relevant tax period.

What to Prepare Before You File Form 8802#

A clean packet beats a rushed packet. Most preventable delays start before the form is even filled out, when the name on the application does not match supporting records, the signer title is inconsistent, or the requested tax period does not line up with what the foreign side expects. It is much easier to catch those mismatches while everything is still on your desk than after the IRS has the file.

Start by building one working file that includes the application and every supporting item that belongs with it. That gives you one place to compare identity details, tax periods, purpose language, filing method, and payment steps before anything is transmitted. A short intended-use note helps here. It does not need to be elaborate, but it should make the purpose visible without forcing anyone to reread the full packet.

This prep stage often tells you whether you have one clean request or several issues hiding in the same packet. If the intended use, applicant identity, and tax period do not line up here, the form itself will not fix that for you. In practice, this is where experienced reviewers catch most of the errors that later get described as "processing delays." The delay usually starts with the file.

Use this prep sequence:

-

Build one complete Form 8802 file first. Start with the application - Form 8802 is the required request path - and keep the supporting documents with it. The goal is one review set, not a pile of disconnected files.

-

Confirm signer details before you sign. For an entity filing, make sure the signer's name and title match across the application and your supporting records. Fix any mismatch before submission instead of waiting for follow-up.

-

Choose the filing channel based on applicant type. Individuals can use standard PDF filing or Digital Adaptive Mobile Forms. Business entities cannot use Digital Adaptive Mobile Forms. If you file through Pay.gov, upload a copy of the application as one combined PDF and keep it within the 15MB limit.

-

Use the correct request type and timeline. Use the Additional Request box only when the original application was approved and there are no meaningful changes. Also remember the timing rules already noted: build to the 45-day mailing guidance, and do not submit a current-year request with a postmark before December 1 of the prior year.

-

Run a final identity-and-period check. Verify names, entity details, and tax-year references against the records you will rely on later. If those details are off now, the certificate can fail when you try to use it.

Before you move to data entry, read the packet straight through once as if you were the reviewer. It should read as one coherent request, with one applicant, one purpose, and the relevant tax period. If it jumps between labels, years, or signer identities, stop and fix the file before you sign or upload anything.

This prep work pays off twice. It lowers the chance of an avoidable delay now, and it makes later validation much easier because you will have a clean submission set to compare against the issued certificate. Once the file is coherent, the next step is to make the application language match that file exactly.

Complete Form 8802 Without Triggering Delays#

Treat the application as a matching exercise, not just a form-filling task. The fields, the purpose statement, and the underlying records all need to tell the same story. Consistency matters more than polished phrasing, because reviewers are looking for a coherent file, not creative wording.

The biggest delay risk here is rarely one dramatic error. It is usually a cluster of small inconsistencies that make the request harder to process: a purpose described one way on the form and another way in the notes, a tax period that does not match the records, or identity details that vary across documents. None of those problems looks large by itself, but together they signal a file that may need follow-up. The best control is to complete the form in order and then compare it line by line against the packet you prepared.

Purpose wording deserves extra care because it bridges the foreign request and the IRS application. If the foreign side said treaty relief, do not make the filing sound like a generic tax-letter request. If the use is VAT, say so consistently. The clearer that match is, the easier the file is to review and the easier it is to explain later if someone asks what was requested and why.

Use this approach when you fill it out:

-

Complete the form in sequence, then review for gaps. Start with identity and residency information, move to tax-period details, and then state the purpose. Do not leave blanks because you expect to explain them later, and use the current Instructions for Form 8802 where the form calls for additional information.

-

Make the purpose explicit and specific. If the use case is treaty relief, say income tax treaty benefits. If the use case is VAT, say value added tax (VAT) exemption. Keep the same wording across the form and supporting materials so the request is not described three different ways.

-

Run a record-match check before filing. Compare legal names, taxpayer identifiers, entity details, and tax-year references against your tax and payment records so the file is internally consistent.

-

Handle the fee and package carefully. A user fee applies. For non-individuals, Revenue Procedure 2018-50 is the cited authority for the fee increase. Confirm the current fee at filing time, then verify payment and final file packaging before you send anything.

A straight-through read at the end is worth the extra few minutes. The application should make sense without side explanations, and the purpose language should match what the foreign side asked for in the first place. Do not assume a later email or phone call will rescue a vague or mismatched filing. Once the form, the purpose statement, and the record set line up cleanly, you are ready to send it as one controlled package and manage the deadline like a real project.

Submit Pay and Track Your Request#

Once the application is out the door, the work shifts from form prep to deadline control. Even a good filing can go sideways here if nobody can prove what was sent, when it was sent, or how the timing compares to the outside deadline. Treat submission, payment, and tracking as one continuous job, not three separate admin tasks.

| Checkpoint | What to keep or watch | Article note |

|---|---|---|

| Submission bundle | Exact version sent, payment confirmation, and submission timestamp | Keep one proof bundle from the start |

| 45-day guidance | Mail Form 8802 with full payment at least 45 days before the certificate is needed | Minimum planning anchor |

| 30-day delay notice | IRS says it will contact applicants after 30 days if a delay is expected | Set your own escalation point if the business deadline comes sooner |

| Status tracking | Use Processing status for Form 8802 and log each change with the date and time | Track from day one |

| Routing context | Philadelphia Accounts Management Center | Note it in your records for follow-up |

Keep one proof bundle from the start. That means the exact version sent, the payment confirmation, the submission timestamp, and a simple date log showing where the request stands against your certificate-needed date. The goal is practical: no one should have to reconstruct the history under deadline pressure. If a client or colleague asks what was filed and what happens next, the answer should be visible from one folder and one timeline.

The IRS timeline gives you a baseline, but your real constraint is the date by which the certificate must be in someone else's hands. That may be a payer deadline, an authority deadline, or an internal cutoff tied to a broader filing. Whatever the outside date is, build your own checkpoints backward from that date rather than treating IRS timing guidance as a promise. The 45-day mailing guidance is a minimum planning anchor, not a reason to leave no margin.

Use these checkpoints after filing:

-

Submit the application and fee as one package. Form 8802 is required to obtain the certificate, a fee applies to every request, and the submission method depends on how you pay. Keep payment proof and the exact filing set together so follow-up is anchored to one record.

-

Treat the IRS timing guidance as a floor, not a promise. The IRS says to mail Form 8802 with full payment at least 45 days before the certificate is needed. Put the filing date, the needed-by date, and your internal follow-up dates on one calendar so delivery risk is visible early.

-

Track status from day one. Use Processing status for Form 8802 and log each change with the date and time. If you need to follow up later, that timeline is much easier to use than memory.

-

Set your own escalation point before the outside deadline tightens. The IRS says it will contact applicants after 30 days if a processing delay is expected, but that does not mean you should wait passively if your business deadline comes sooner. Escalate based on the risk to the actual use date.

-

Keep routing context in the file. For mailed certifications, note the Philadelphia Accounts Management Center in your records so follow-up stays organized.

This stage is easy to under-manage because the filing is done and the work can feel finished. It is not finished until the certificate is in hand and checked against what you asked for. When it arrives, treat receipt as a new control point, not the end of the process.

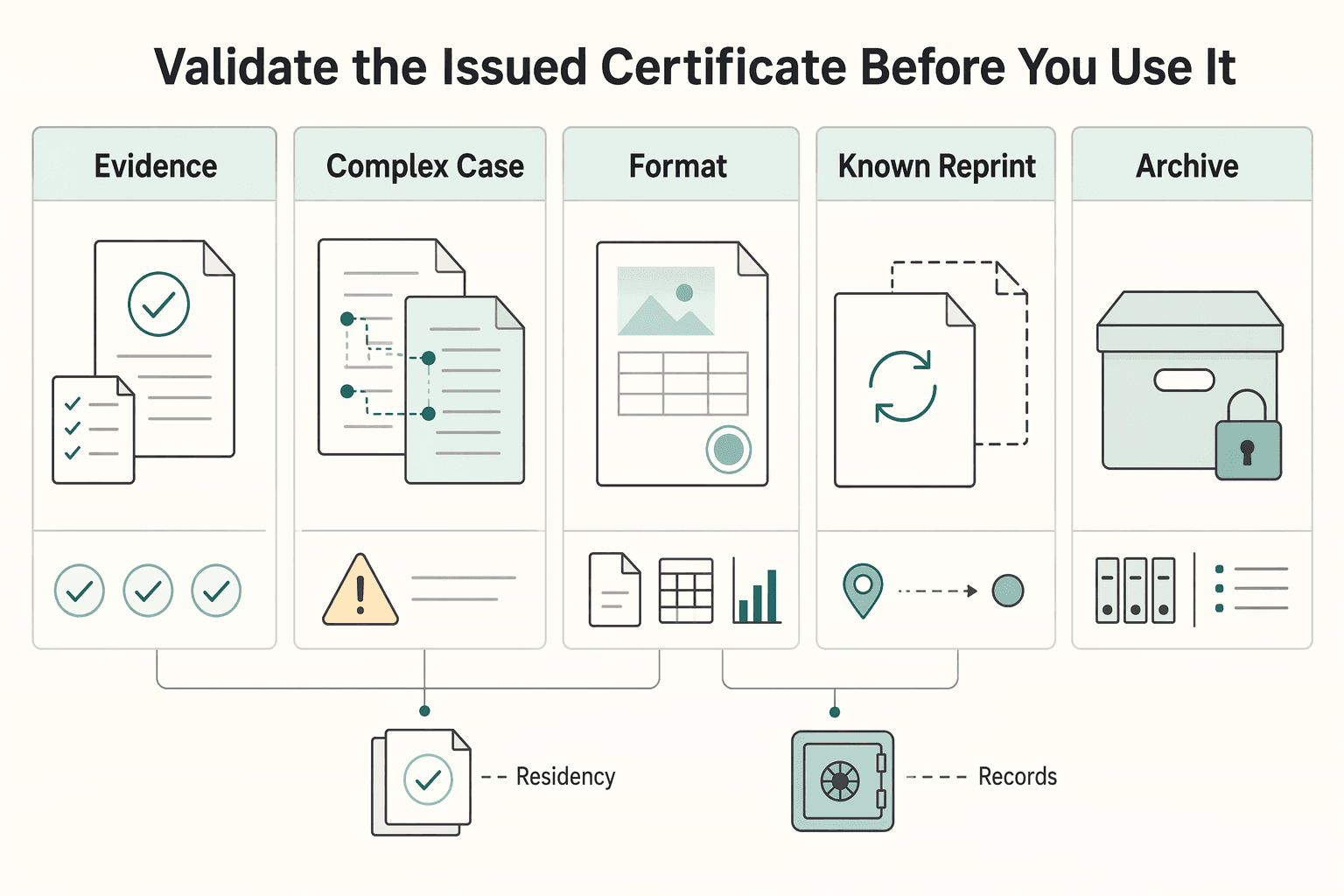

Validate the Issued Certificate Before You Use It#

Receipt is only a checkpoint. Before you send the certificate to a payer, a foreign authority, or even an internal team handling the next step, compare the issued document against what you asked for and what the destination expects. This is where the careful packet assembly from earlier pays off, because you already have a clean submission set for comparison.

| Check | What to confirm | Reference |

|---|---|---|

| Document type | Residency certificate on U.S. Department of the Treasury letterhead | Issued document |

| Identity details | Person or entity details are correct | Form 8802 submission set |

| Format | Issued details match the foreign payer's required format | Foreign payer requirements |

| Known reprint window | If issued from July 29 to Nov. 13, 2024, add an explicit verification step | IRS reported incorrect signatures and mailed corrected certificates |

| Archive | Keep the issued Certification of U.S. Residency, the Form 8802 submission set, and your verification notes together with a date stamp | Final audit package |

The goal of this review is simple: catch a usable-but-wrong document before it leaves your control. A small mismatch in identity details, tax period, or expected format may be fixable when you spot it immediately and much harder once the document has already been forwarded and relied on. In practice, this is one of the most valuable pause points in the whole process because it is the last moment when correction is still relatively contained.

Before you forward anything, ask a practical question: if the foreign side sees only this document and your handoff note, will the package make sense on first review? If not, fix the mismatch while the document is still in your hands. That question keeps you focused on real usability rather than just whether the IRS sent something back.

Run this final validation pass:

-

Confirm the document type and identity details. Verify that it is the residency certificate on U.S. Department of the Treasury letterhead and that the person or entity details are correct.

-

Reconcile it to your Form 8802 submission set. Compare the issued certificate to the application and related records you submitted. If core details do not match, pause before anyone uses it.

-

Match the format to payer acceptance before sending. Check the issued details against the foreign payer's required format so the package is usable on first review.

-

Apply the anomaly check for the known reprint window. If the certificate was issued from July 29 to Nov. 13, 2024, add an explicit verification step because the IRS reported incorrect signatures for that period and mailed corrected certificates.

-

Archive the final audit package. Keep the issued Certification of U.S. Residency, the Form 8802 submission set, and your verification notes together with a date stamp.

Do not skip the archive step. If the foreign side comes back with a question, or if you need to repeat the process later, that package lets you see exactly what was issued and exactly what you verified before release. That closes the IRS side of the work. The next question is separate, and it is often where teams get surprised: whether the destination country will accept the document in the form you now have. Related, if this request sits inside an India remittance file: The Freelancer's Guide to India's Outward Remittance Rules (LRS).

Handle Foreign-Country Acceptance Requirements#

A valid IRS certificate can still fail at the destination if local acceptance rules were assumed instead of confirmed. Keep that separation in view the whole way through: IRS issuance and foreign-country acceptance are connected, but they are not the same job.

This is also where teams lose time by assuming legalization is automatic or universal. It is not part of the IRS step itself, and the right path depends on what the destination actually asked for. Written instructions matter because they let you build the outbound packet to a defined target instead of to guesswork. When those instructions are missing, people tend to fill the gap with assumptions, and assumptions create last-minute rework.

The practical way to handle this is to get the destination checklist in writing, follow the exact legalization path specified, and build the outbound packet so each item maps to that checklist. If local instructions cut against what you expected from the IRS side, stop before you resubmit or legalize anything. Rework is usually less painful at that point than after the packet has already been sent.

Use this sequence:

-

Step 1: Get destination requirements in writing. Ask the payer or local authority for the exact acceptance checklist before you submit. Confirm whether they require legalization and any country-specific forms in addition to the certificate.

-

Step 2: Follow the legalization path they specify. Do not assume one route works everywhere. If the destination asks for Apostille or Authentication, use that exact route and document the decision in your file.

-

Step 3: Build a complete handoff packet. Include the issued certificate, proof of legalization, and a short cover note mapping each item to the destination checklist.

-

Step 4: Escalate conflicts before resubmitting. If local instructions conflict with your IRS-side assumptions, pause and get professional review. Keep a dated copy of the final outbound packet for audit and rework control.

By this point, the sequence should be clear: classify the need, prepare the file, complete the application carefully, submit and track the request, validate the document, and then confirm destination acceptance. That is the full job. The questions below cover the narrower points that usually remain once that sequence is clear.

Your Copy Paste Checklist Before You Request Form 6166#

Use this as the short version of the process. Run it top to bottom so you do not solve later steps before the earlier ones are settled.

-

Confirm the foreign use case in writing. Make sure the payer or tax authority is asking for U.S. residency certification for treaty or other tax-benefit treatment, and save that request in your file.

-

Recheck IRS guidance on filing day. Review the latest Instructions for Form 8802, Processing status for Form 8802, current fee information, and any current timing updates right before submission.

-

Build one clean filing set before you send anything. Make sure the application, supporting records, purpose wording, signer details, and tax-period references all tell the same story.

-

Complete Form 8802 against matching records. Check legal names, taxpayer details, tax-period details, and signer authority against the materials you will rely on later.

-

Submit with the required fee and keep proof. Send the application with the fee, keep payment confirmation and submission evidence together, and build enough buffer around the 45-day guidance.

-

Track the request against the real deadline. Log filing date, needed-by date, status checks, and your internal escalation point so timing risk stays visible.

-

Validate the issued certificate before sending it onward. Confirm it is on Treasury letterhead, confirm the identity details match your records, and apply any date-specific anomaly check that affects the issuance window.

-

Confirm destination-country legalization requirements in writing. Verify whether Apostille or Authentication is required before handoff and collect any local checklist items.

-

Escalate early if instructions conflict. If IRS process expectations and destination requirements do not line up, pause and get professional review before you resubmit or legalize anything.

Run the checklist in order and you reduce the odds of delay and rework. If the open issue is country-specific acceptance, Talk to Gruv.

Frequently Asked Questions

What is irs form 6166, in plain English?

It is a U.S. tax residency certification letter from the IRS, printed on U.S. Department of the Treasury letterhead. It can be used to support income tax treaty benefits and certain other foreign-country tax benefits.

How do I actually get Form 6166 from the IRS?

You request it by submitting Form 8802, and the IRS says use of Form 8802 is mandatory. A user fee applies to all Form 8802 requests.

What is Form 6166 used for under an income tax treaty?

The IRS says you may use Form 6166 to claim income tax treaty benefits in foreign countries. It is used as proof of U.S. residency status for that purpose.

Can Form 6166 prove I paid U.S. taxes for a foreign tax credit?

No. Form 6166 is a residency certificate. To claim a foreign tax credit, individuals, estates, and trusts file Form 1116, while corporations file Form 1118.

Do freelancers use the same Form 8802 process as companies?

Yes. The IRS procedure for requesting Form 6166 is submission of Form 8802.

Do I need Apostille or Authentication before I can use Form 6166 abroad?

The IRS excerpts used here do not address Apostille or Authentication requirements. Confirm any such requirement with the foreign authority requesting the certificate.

Where do I check current fees and processing time for Form 8802?

Check the IRS Form 6166 and Form 8802 pages for the latest fee and processing updates before you file.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

The Freelancer's Guide to India's Outward Remittance Rules (LRS)

Run your outward remittance like an operations process: clarify intent, keep supporting proof, confirm fees, then archive what happened in a reusable folder. If you are the CEO of a business-of-one, this is part of keeping your cashflow predictable. You do not need more theory. You need a system you can repeat every time you send money abroad under LRS in India.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.