Quick Answer

Yes. For taiwan tax for foreigners, the core rule is that Taiwan taxes Taiwan-source income under the Republic of China (R.O.C.) Income Tax Act, and your filing path depends on resident or non-resident status. Start by documenting days present, then classify each income line by source, then verify whether withholding actually settles your obligation. Day bands and flat-rate references are not a substitute for source classification and filing checks.

Filing Path Starts With Residency Status and Source Rules#

Start with tax rules, not visa labels. A sequence that helps prevent common filing mistakes is: confirm residency status, classify each income stream by source, choose the filing route, then escalate only where facts stay unclear.

That order matters because tax mistakes usually stack on top of each other. A rough residency assumption can distort your source analysis. Weak source analysis can make a withholding rate look more conclusive than it is. Then filing month arrives, and instead of checking a return, you are rebuilding it from scratch. A disciplined sequence keeps each step tied to evidence before you move to the next one.

The core rule is narrower than many summaries suggest. Taiwan individual income tax applies to Taiwan-sourced income for both resident and non-resident individuals. An exemption can still apply under the Republic of China (R.O.C.) Income Tax Act or another law. The first question is not where you feel based. It is which income was sourced in Taiwan and under which status it was earned.

Use this order before you do any tax math:

- Build a day-count log for the taxable year.

- Mark each payment by service location, payer, and contract purpose.

- Check whether withholding happened and whether it actually closes your obligation.

- Confirm the filing path against official Alien Individual Income Tax instructions.

Keep those steps separate. Your day-count log should be based on actual travel and immigration records, not memory. Your payment review should happen line by line, not by broad client labels, because one payer can appear across different contracts or work periods. Your withholding review should ask two different questions: did withholding happen, and does that withholding actually end the filing analysis for that item. Only after those checks should you choose a filing route.

One threshold needs early attention: more than 90 days in a taxable year. At that point, remuneration paid by an employer outside the ROC for services performed inside the ROC can be treated as ROC-sourced income. Another frequent mistake is treating 18% as a complete answer. That rate appears in specific non-resident day ranges and does not replace source classification and filing checks.

Use official MOF eTax Alien Individual Income Tax guidance and instructions as your control set, then verify details with the relevant tax office when facts are unclear. Keep one evidence folder from day one with your stay log, contracts, invoices, payment records, and withholding slips. If you keep that folder current, filing season becomes a verification exercise instead of a reconstruction project. That shift is practical, not cosmetic: the more complete your file is before filing month, the less likely you are to make a rushed classification call just to finish the return.

Start With the Rules That Actually Drive Taiwan Tax#

The safest default is a strict hierarchy: official Taiwan government tax portals first, professional summaries second, blog explainers last. That order keeps your decisions defensible when guidance conflicts.

| Source tier | Use | Priority |

|---|---|---|

| Official Taiwan government tax portals | Pull the exact rule and write a one-line note | First |

| Professional summaries | Use as context to spot gaps or conflicts | Second |

| Blog explainers | Use to surface questions or organize your review, not to anchor a final filing position | Last |

Use secondary guides as context, not authority. Some professional and blog resources explicitly describe their content as high-level or informational and tell readers to verify details with licensed Taiwan professionals and official portals. That does not make those resources useless. They are best used to surface questions, organize your review, or warn you where assumptions commonly go wrong. They are not where you should anchor a final filing position.

Use this check sequence:

- Pull the exact rule from an official portal and write a one-line note.

- Compare third-party summaries only to spot gaps or conflicts.

- If numbers differ, mark the third-party figure as unverified.

- Keep an issue log for unresolved points before final treatment.

Make the issue log work for you. For each point, note the tax year, the question in plain language, the official page you checked, the date you checked it, and whether the issue is resolved or still open. If an official page answers part of your question but not all of it, note that gap instead of filling it with a blog sentence that only sounds certain. A short unresolved note is safer than a confident but unsupported assumption.

A common failure mode is treating fresh-looking figures as confirmed law. If summaries disagree, do not average them and do not pick the lower-tax answer; freeze the assumption, mark it pending verification, and proceed conservatively until official guidance resolves it. Add the verification date to each note so you can quickly see what is confirmed before filing. Also label your notes by tax year so you do not accidentally combine instructions, rate tables, and commentary written for different filing cycles. If you want a deeper dive, read The Taiwan Gold Card: A Visa for High-Skilled Professionals.

Decide Your Residency Status Before You Do Anything Else#

Decide and document your residency status before you classify any income, or later tax decisions can unravel.

Use a strict sequence and keep records with each step:

- Confirm your days of presence for the tax year from travel and immigration records.

- Assign residency treatment only after that day count is documented.

- Set a provisional filing route based on that treatment.

- If facts are incomplete, keep the status provisional and use the conservative assumption until verified.

The point is not just to reach a status answer, but to show how you got there. Keep a simple residency memo in your tax folder: the taxable year, your day count, the records used to support that count, your provisional or final status, and any open issue that still needs confirmation. If your count changes after you reconcile travel records, the memo should change too. That way, you are not guessing which version of the facts was used when you built the rest of the return.

If your year is close to a status boundary, do not optimize too early. Verify with current official Taiwan tax instructions before filing. Borderline cases are where people most often jump ahead to tax math because they want certainty fast. Resist that impulse. If status remains uncertain, keep both the status note and the filing path provisional, and do not let later calculations create false confidence.

If you hold a Taiwan Employment Gold Card, still run the same residency test. Visa or work status does not replace tax-status analysis, so keep your stay log, entry/exit records, and employment paperwork together. Treat high-level expat guides as context, not final authority, and escalate for case-specific advice when your tax and immigration timelines do not line up. A change in work authorization or employment arrangement may matter to your records, but it does not remove the need to complete the same resident or non-resident review.

Classify Your Income Into Taiwan Source and Non Taiwan Source#

Classify each payment by source before you calculate tax, and treat unclear items as taxable until you can verify them.

| Day range | Payment fact pattern | Treatment noted |

|---|---|---|

| Less than 90 days | Salary from a Taiwan-registered entity | Generally subject to 18% withholding |

| Less than 90 days | Remuneration from an entity registered outside Taiwan | Can be exempt in that specific fact pattern |

| More than 90 but less than 183 days | Taiwan taxable salary income | Described at a flat 18% rate |

Map income stream by stream, not client by client. Keep separate lines for salary, client services, contract payments, and edge cases such as property transactions, occasional trade income, and interest from mortgages. The goal is to avoid broad labels that hide differences inside a single relationship. The same payer can appear on multiple lines if the contract purpose changed, if the service location changed, or if one payment fits a salary review while another needs a different analysis.

Use this triage before computing tax:

- Identify the income type: salary, service fees, or non-salary item.

- Record where the activity happened and who paid.

- Mark whether withholding occurred, and for which item.

- Tag each line as

withholding-managedorself-reported pending review. - Keep uncertain lines in a provisional taxable bucket until confirmed.

Build the worksheet so someone reviewing it can follow it without guessing. Each row should link to a contract or other support, an invoice where relevant, a payment confirmation, and a short note on why you gave that item its current treatment. If one contract covered different activities or periods and the facts are not uniform, do not force a single label across the whole thing. Break it into separate review lines so you can see what is clear, what is mixed, and what still needs verification.

Do not apply salary withholding rules to every category. For non-residents in the less-than-90-day band, salary from a Taiwan-registered entity is generally subject to 18% withholding, while remuneration from an entity registered outside Taiwan can be exempt in that specific fact pattern. For non-residents in the more-than-90-but-less-than-183-day band, Taiwan taxable salary income is also described at a flat 18% rate. These are salary rules, not a shortcut for all income types, and withholding does not automatically remove declaration needs for every Taiwan-source item.

That is where many self-filed drafts start to drift. A person sees an 18% reference, decides the rate answers the whole problem, and stops testing whether the payment is actually salary, whether the day-range fact pattern fits, and whether the withholding treatment matches the source classification. Keep those checks separate. A correct rate attached to the wrong category is still a wrong result.

Checkpoint: each line item should have a contract, invoice, and payment confirmation. Add a short note on who paid, what was delivered, where work occurred, when payment was earned, and why the source classification was chosen. If one item lacks support, keep it separate so it cannot quietly change treatment for fully documented items. Related: Taipei, Taiwan: The Ultimate Digital Nomad Guide (2025).

One practical habit helps here: do not collapse everything into annual totals too early. Keep the line-by-line map visible until your classification work is done. Aggregated totals are useful later, but they can hide the one payment that has a different payer, a different work location note, or missing withholding support. Your first draft should make unusual items easier to spot, not easier to miss.

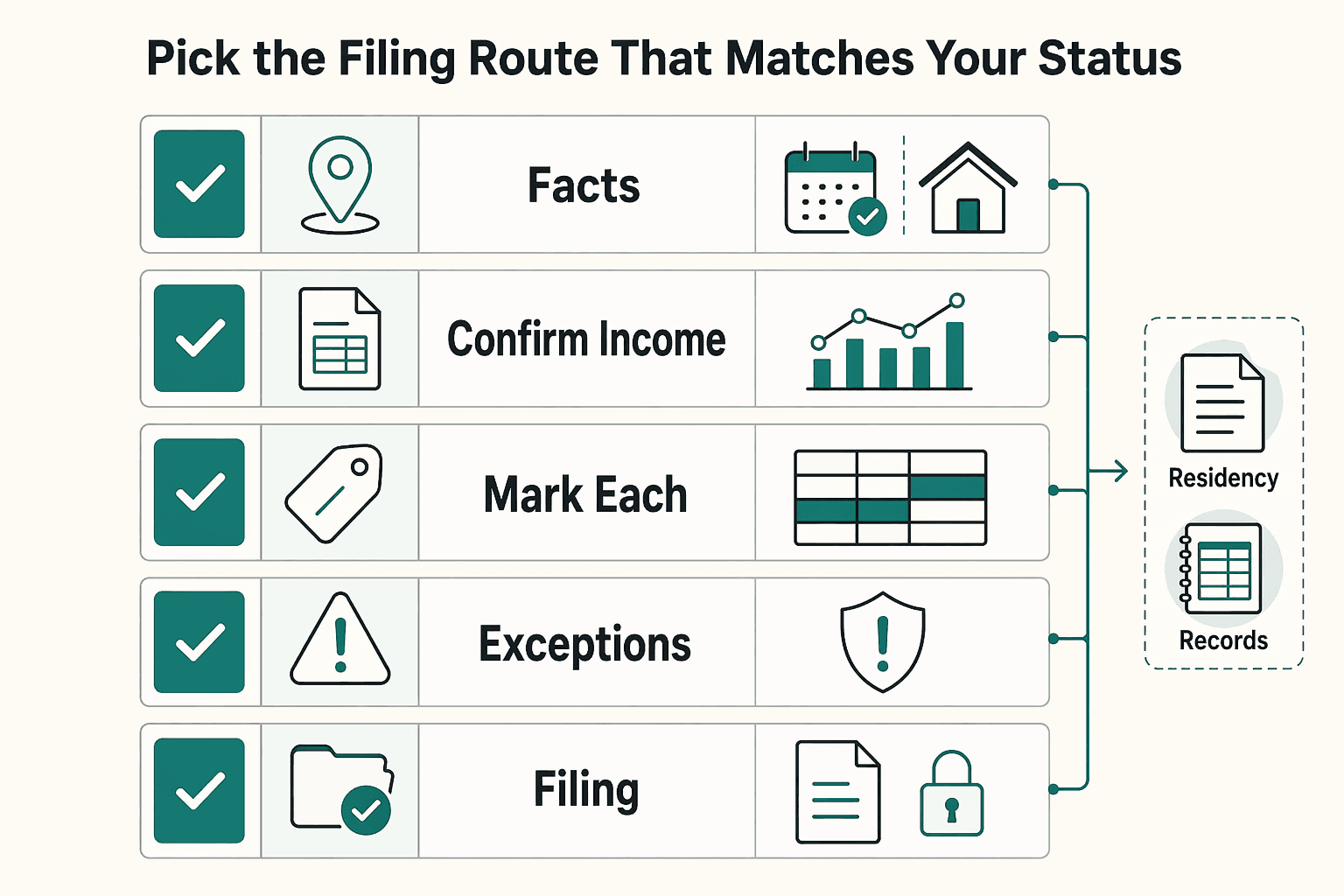

Pick the Filing Route That Matches Your Status#

Start with status, not a rate shortcut. Your filing route should follow your resident or non-resident classification for the taxable year (January 1 to December 31), based mainly on domicile in Taiwan and days present.

For resident treatment, plan for a normal individual income tax return and a full review of Taiwan-source income. For non-resident treatment, do not assume withholding alone closes the file; check current Foreign Individual Income Tax and National Taxation Bureau guidance before deciding that no return action is needed.

Use this routing checklist:

- Document status support (domicile facts plus day-count records).

- Confirm your income map is complete.

- Mark each line as withholding-managed or still pending review.

- Run exception checks against current official guidance.

- Record the filing decision, open questions, and who will verify them.

A simple cover sheet can make this easier. Put your status basis at the top, list the income streams underneath, mark which items are fully supported, and list any question that still affects the filing route. That turns the return from a loose pile of records into a decision file. It also makes escalation faster if you later need help, because the unresolved points are already separated from the items that are straightforward.

A common failure mode is relying on one "flat rate" claim without reconciling it to official instructions. If status support or source classification is weak, treat the filing decision as unresolved until verified. A line marked withholding-managed is not the same as a line marked closed. It still needs to fit the right status, the right source analysis, and the right official instructions for the year before you treat the route as settled.

Estimate Resident Tax Without Overconfidence#

If you are already in resident treatment, treat your first tax number as provisional: base it on the resident progressive rate table, then add exemptions and deductions only where eligibility is clearly documented.

Start with the published resident table for the relevant year. For 2026, the table runs from 0~610,000 × 5% up to 5,190,001 and above × 40% - 949,100. Use that as your baseline before any adjustments. The point of a baseline is not to finish the calculation in one pass. It is to separate the part that is clearly supported from the part that still depends on documentation.

Apply exemptions and deductions only when your facts match the published conditions. Residents can claim these items, including NT$97,000 per taxpayer, spouse, and dependent, and a higher NT$145,500 exemption in listed age-based cases. If eligibility is unclear, leave that item out in pass one.

Use a simple known vs unknown box in your worksheet:

- Known: resident status basis, tax year, confirmed income totals, confirmed withholding, published rate table.

- Unknown: exemption eligibility not yet documented, deduction category not yet matched to conditions, missing records.

This split does two useful things. First, it keeps you from blending confirmed numbers with hoped-for adjustments. Second, it shows exactly where to spend your verification time. If your draft tax number only changes when one exemption or deduction is added, that item becomes the next document check, not a vague worry sitting in the background.

If one item is uncertain, run two versions: a conservative estimate first, then an adjusted estimate after document verification. Keep both versions dated so changes are clear. A dated conservative draft is better than an undated optimistic one, because you can explain why the number changed and what evidence supported the change.

Also, keep the worksheet readable. A polished spreadsheet can still hide weak assumptions if every note is buried in formulas. Put unresolved items in plain language next to the numbers. If you cannot explain why an exemption or deduction is included in one sentence and point to the supporting record, it belongs in the pending column until you can.

Build Your Evidence Pack Before Tax Season#

Build one evidence pack before filing month so every number on your return maps to a document.

| Checkpoint | Action | Article note |

|---|---|---|

| Monthly | Collect invoices, withholding slips, payment confirmations, and contract updates | Save final documents, not just email copies |

| Quarterly | Reconcile totals and flag gaps early | Compare your worksheet to actual payment records and spot missing withholding support |

| Pre-filing month | Run a missing-item check against Required Document and your income map | Do a final document sweep, not the first attempt to organize the year |

Use the same tax-year boundary: January 1 to December 31. Keep status and income evidence together, since treatment for "Non-Residents of the R.O.C." and "Residents of the R.O.C." depends on length of stay. The pack should let you answer the same questions for each item every time: what the payment was, who paid it, when it was earned or paid, whether withholding applied, and how you treated it on the return.

Use the Required Document (Alien Individual Income Tax) page as your checklist anchor, then add your working records in one folder: employment contract, invoices, withholding records, and payment confirmations. Label files by tax year and income stream so review is fast. A practical structure is a main folder for the tax year, with subfolders for status records, salary items, service-fee items, other income items, withholding records, and filing confirmations. Within each folder, keep documents in the same order as your income map so you can move from worksheet line to file without hunting.

Use this operating cadence:

- Monthly: collect invoices, withholding slips, payment confirmations, and contract updates.

- Quarterly: reconcile totals and flag gaps early.

- Pre-filing month: run a missing-item check against Required Document and your income map.

Make each checkpoint do real work. Monthly collection should mean saving final documents, not leaving them in email. Quarterly reconciliation should mean comparing your worksheet to actual payment records and spotting missing withholding support while there is still time to ask for it. Pre-filing month should mean a final document sweep, not the first time you try to organize the year.

For payments, keep proof of payment route and final confirmation, because payment proof must be attached to the return unless you e-file. If you e-file, keep the submission confirmation and barcode payment slip record from the e-Filing path. Store those filing confirmations in the same year folder as the return draft and payment records, so the story stays complete from calculation through submission and payment.

Red flag: drafting from bank summaries without matching withholding or contract evidence. If a key document is missing, mark that line as pending and avoid aggressive assumptions until records are recovered. Bank summaries can help you spot totals, but they do not replace the underlying records that explain what each payment was and how it should be handled. When something is missing, make a short missing-document list with the item, the gap, and the next action needed to close it.

Know Your Escalation Triggers and Cross Border Constraints#

Escalate before filing if core facts are still disputed, especially when residency is borderline, income sourcing is mixed, or withholding records do not match your draft return.

Bring one clean file so your advisor can focus on judgment, not cleanup: stay timeline, income map, withholding records, payment proof, and a short note on each unresolved item. The short note matters. If you can explain each open issue in one or two lines, the advisor can respond to the real question instead of spending time reconstructing the background. Good escalation files are not larger; they are clearer.

Run Taiwan and home-country compliance in parallel. Keep treaty and double-tax-relief decisions in the advisory lane unless your facts are simple and fully documented. Parallel review matters because your Taiwan return, your residency story, your withholding treatment, and any foreign reporting position should not contradict each other. Even when each piece feels manageable on its own, timing differences and incomplete records can create avoidable mismatches if you leave one country's review until the other is already filed.

For US-linked filers, check Form 8938 early while you prepare the Taiwan return. Form 8938 is attached to the income tax return and applies when specified foreign financial assets exceed the applicable threshold. IRS guidance cites a $50,000 aggregate threshold for certain taxpayers, with higher thresholds for some filers, and states that if no income tax return is required for the year, Form 8938 is not required.

Keep entity type in view. Certain domestic corporations, partnerships, and trusts can also have Form 8938 obligations, with instructions referencing $50,000 at year-end or $75,000 at any time during the year. If your facts involve more than a straightforward individual filing picture, flag that early so the cross-border review starts with the right scope.

Use this escalation checklist:

- Residency status was close to a threshold.

- Withholding slips and ledger totals do not reconcile after review.

- Assets may trigger Form 8938 and filing status or thresholds are still unclear.

- FBAR or FinCEN reporting may apply, and current requirements are not yet confirmed with a qualified cross-border advisor.

Waiting until filing week to combine Taiwan and US obligations usually creates the most expensive rework. Early escalation keeps corrections smaller and reduces conflicting positions across returns. It also helps you avoid a common failure mode: finishing the Taiwan draft first, then discovering that the cross-border review needs records you never organized because you assumed the local return was already done. You might also find this useful: How to Legally Avoid Double Taxation: A Freelancer's Guide to Tax Treaties.

Conclusion#

Close the process the same way you started it: with disciplined sequencing and clear documentation. Use verified facts, keep uncertain points clearly marked, and avoid confidence built on incomplete support.

Final consistency check: status notes, income classification, draft calculations, and payment records should tell the same story. If one item does not reconcile, treat it as a stop signal and resolve it before submission. A short dated decision memo helps here because it captures what was confirmed, what remained open, and what action you took for this filing cycle.

Because the available support here is limited, keep country-specific conclusions narrow. For unresolved positions, keep assumptions narrow and flag them for professional confirmation. The goal is a return you can explain line by line, update quickly if better evidence appears, and defend without last-minute scrambling.

Frequently Asked Questions

Do foreigners pay tax in Taiwan if they only have Taiwan-source income?

Yes. Under the Republic of China (R.O.C.) Income Tax Act, Alien Individual Income Tax is levied on income derived from R.O.C. sources. If your income is Taiwan-source, treat it as taxable unless an official rule provides an exemption.

How do I determine whether I am a resident or non-resident taxpayer in Taiwan?

Use the official categorization in the Instructions for 2024 Alien Individual Income Tax, which separates taxpayers by length of stay in the taxable year. The taxable year is January 1 to December 31. If your day count is near a boundary, verify status before filing.

When does withholding at source mean I may not need to file a Taiwan return?

There is a non-resident path for stays of not more than 90 days in a taxable year where R.O.C.-source income is handled through withholding at the stated withholding-rate rule. That is not a universal filing exemption. If records show mixed treatment or exceptions, escalate before assuming no return is required.

What is the practical difference between resident progressive rates and non-resident treatment?

Resident treatment uses the Progressive Tax Rate (for resident use only). Non-resident short-stay treatment relies more on withholding mechanics in official instructions. Your status decision changes both tax computation and filing verification steps.

How should I handle exemptions and deductions when official conditions are unclear?

Apply the Table of Exemption and Deduction only when facts clearly match listed conditions. If eligibility is uncertain, run a conservative draft first and mark that item pending until documentation is complete.

Does having a Taiwan Employment Gold Card automatically change my tax residency result?

Gold Card status does not carry a separate tax residency classification under R.O.C. tax law. Use the official resident/non-resident categorization based on length of stay in the taxable year and confirm your filing facts before you submit.

When should I stop self-filing and hire a Taiwan tax professional?

Stop self-filing when residency is borderline, sourcing is mixed, or withholding records conflict with your draft. Escalate earlier if cross-border reporting obligations may apply in another jurisdiction.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- irs.gov/businesses/corporations/do-i-need-to-file-fo...trusted

- irs.gov/irb/2025-13_IRBtrusted

- foreignersintaiwan.com/blog/income-tax-filing-for-expatriates-in-ta...external

- taxathand.com/article/8988/Taiwan-China/2018/New-rules-on-...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Taiwan Gold Card Application Strategy for Remote Professionals

Treat this process as a chain of linked decisions, not a race to submit. If you are planning a serious move or a long stay in Taiwan, the safer outcome usually comes from choosing the right route first and proving each core claim before you pay or file. The Taiwan Employment Gold Card rewards that discipline because it combines four functions in one status: a work permit, resident visa, Alien Resident Certificate (ARC), and re-entry permit.

Taipei Digital Nomad Guide for 2026 Long-Stay Moves

Decide your legal stay path before you spend on flights, deposits, or a long coworking plan. In Taipei, that choice sets the timeline for everything else. If you treat the city like a casual base first and a regulated move second, you raise the odds of rework, document gaps, and avoidable continuity risk.

How Freelancers Can Legally Avoid Double Taxation With Tax Treaties

Classify the tax problem before you touch a return. If your income is mostly personal service fees across borders, this guide fits. If your issue is C corporation profits and shareholder dividends, you are solving a different problem.