Quick Answer

Start by confirming personal tax residency before making any Estonia company payment decisions. In this framework, e-Residency is a digital identity status, not a residency override, so you should test personal status first, then model company exposure and source-of-income risk. Run a pre-payment check on payout label, reporting impact, and proof artifacts, and pause transfers when treatment is unclear. Use EMTA guidance, keep dated records, and escalate early if cross-border facts do not align.

Start Here With the One Decision That Prevents Most Tax Mistakes#

Make this decision first: confirm your status and compliance assumptions before you invoice, pay yourself, or distribute company money.

If your life, clients, and banking span countries, this sequence reduces avoidable errors. Do not optimize tax outcomes before you can explain your status assumptions in plain language and back them with records.

Keep the boundary clear. This is practical guidance based on public Estonian tax and digital ID program positioning, not personal legal or tax advice. Hold one distinction fixed from the start: e-Residency status is not physical residency and not personal tax residency.

Put headline tax claims in context. You may see the retained-profit narrative, but that is not the same as no tax in all cases. Public guidance frames tax at distribution, and one cited rate is 22% for distributed profits.

Before any operational move, run these checks and write the answers in one dated note:

- Status check: separate what the digital ID program changes from your personal tax-residency analysis.

- Reporting check: prepare reporting obligations before operating.

- Cross-border check: review VAT implications and possible permanent-establishment exposure for your client setup.

- Evidence check: keep payment documentation for invoices, payouts, and business expenses.

Then lock a simple execution rule: no funds leave the company unless the payment label, filing impact, and proof artifacts are ready the same day. That helps prevent pay-now-classify-later mistakes.

This order matters because later corrections are usually harder than first-pass classification. An invoice issued under one assumption may trigger VAT review. A payout booked under the wrong label may force amended filings. A missing proof artifact can turn a simple explanation into a reconstruction exercise. The practical goal is not to predict every edge case in advance. It is to make sure each decision starts from a documented baseline that you can still defend weeks or months later.

Work through the sections that follow in order, then run the final checklist and escalation triggers before acting. If residency facts conflict or payment classification is unclear, pause and get qualified tax advice before moving money.

Define the Terms Before You Make Any Tax Move#

Start by defining the terms. e-Residency is a digital-residency initiative, and tax residency is a separate legal status under tax law.

An e-resident digital ID does not by itself make you an Estonian tax resident. Keep that line clear before invoicing, payouts, or distributions.

Keep legal labels separate in your records: private person, legal person, citizenship, and residence permit status. Citizenship follows your passport. Tax residency follows tax law. Do not treat a residence permit or Estonian citizenship as the same as digital status.

For Estonia exposure, start with EMTA's non-resident baseline: non-residents are taxed in Estonia only on income from Estonian sources. Tax treaties can change outcomes, so classify income type and source first.

Do not assume withholding always ends filing duties. EMTA says withholding is generally done at disbursement and non-residents usually do not file, but it also lists cases that still require self-declaration, including transfer-of-property income, sole proprietor business income, or income tied to a registered permanent establishment. EMTA also lists remuneration to a non-resident member of a management or controlling body as taxable Estonian-source income.

Before your next tax move, confirm these four lines in writing:

- Identity line: digital ID program status and ID details.

- Person line: your current tax-residency position and open uncertainties.

- Legal status line: citizenship and residence permit status, separate from digital ID status.

- Income line: whether each planned payment may be Estonian-source under EMTA categories.

Store those four lines at the top of your compliance file so every later decision points back to the same baseline. If any line is unclear, pause and escalate before money moves. For a refresher on the identity program, see Estonia's E-Residency Program: What is it and Who is it For?

A useful discipline here is to treat mislabeling as a control failure, not a wording issue. If your note says "resident" but does not say resident of where, it is incomplete. If it says "company payout" but does not say whether that is compensation, profit distribution, or another payment type, it is incomplete. The point is not perfect drafting. The point is that a later reviewer should be able to read the file header and understand which legal bucket each person, entity, and payment sits in before looking at any tax treatment.

Decide Your Personal Tax Residency First, Then Model Company Tax Exposure#

Handle this in order: confirm personal tax residency first, then model company exposure. If personal status is unclear, pause assumptions on invoicing, payouts, and treaty outcomes until you can defend the residency position.

Start with a country-by-country check for your home jurisdiction and Estonia. Record each result as likely resident, likely non-resident, or unclear. If countries point to different answers, treat that as an unresolved conflict and document it.

Apply treaty logic only after residency logic. Treaty structure handles residency first, while relief from double taxation comes later. Use treaty relief to reduce double-tax risk, not to replace your domestic tax analysis. Treaty benefits are not automatic because anti-treaty-shopping limits exist.

Then model company exposure using management facts, not only incorporation facts. Check where key management and commercial decisions are made, because another country may claim company tax residency on that basis. Estonian e-residency status does not change that test. For non-residents, exposure can also depend on the nature and extent of in-country business activity.

Keep one page of evidence notes for each major assumption so timing and intent are defensible later:

- Personal residency note: date, countries reviewed, current conclusion, open questions.

- Company management note: where key decisions were made and by whom.

- Treaty note: which treaty article supports the position and what it does not change.

- Authority note: whether you requested or obtained a company tax residency certificate from the Estonian tax authority.

When facts move, update the page the same day. A stale note is almost as risky as no note because it can lock in an assumption that no longer matches reality.

Dual-residence conflicts can take time because authorities may need to coordinate across countries. If your personal residency position is not clear on one page, stop and resolve that before finalizing company tax assumptions. For a treaty refresher, see How to Legally Avoid Double Taxation: A Freelancer's Guide to Tax Treaties.

A practical way to run this review is to separate "facts" from "conclusions." Facts are the things you can document directly: where you were, where decisions were made, who approved them, and which country positions remain open. Conclusions are the tax labels you apply after reviewing those facts. Keeping those layers separate makes later updates easier. If your facts change, you revise the conclusion note instead of rebuilding the whole file.

It also helps to mark each assumption as either active or provisional. Active means you are comfortable using it for the next payment or filing cycle. Provisional means you are still waiting on a document, formal confirmation, or advisor input. That small label prevents internal notes from being treated as final when they were only meant as placeholders while you investigate.

If you want a deeper dive, read Estonia's E-Residency Program: What is it and Who is it For?.

Decide When Estonia Can Tax You as a Non-Resident#

If you are a non-resident, start from this baseline: Estonia taxes only income received in Estonia.

Keep personal and company analysis separate. EMTA treats resident natural persons as having unlimited tax liability on income from Estonia and abroad, while non-residents do not. Separately, a legal person is a resident if it is established under Estonian law, so your personal and company positions can create different obligations at the same time.

Check permanent-establishment risk as a separate line. A non-resident's permanent establishment is not an Estonian resident, but it is taxed in the same way as a resident. That can change exposure even when personal status looks unchanged.

Before major changes, re-check current EMTA guidance. If facts are mixed, use EMTA's formal residency determination path in e-MTA, including Form R options, instead of relying on undocumented assumptions.

Before acting, confirm these four lines in writing:

- Personal line: is your place of residence in Estonia, or are you still non-resident on current facts?

- Presence line: did your stay approach or exceed 183 days over 12 consecutive calendar months?

- Company line: is the legal person still treated as resident under Estonian law, and is there a permanent establishment that could be taxed like a resident?

- Source line: can you clearly explain why income is or is not treated as received in Estonia under current guidance?

Add one more operational check before payment cycles restart: verify that your latest facts still match the four lines above. If they do not, treat prior tax treatment as provisional until reviewed.

If any line is unclear, take a conservative filing posture until clarified. Document uncertainty, avoid aggressive assumptions, and pause non-urgent structural changes.

One red flag remains constant: e-residency status does not automatically exempt you from taxation elsewhere. Even if Estonia's non-resident scope looks limited, another country may still tax you under its own rules.

A common failure mode is mixing a true statement with the wrong conclusion. For example, it may be true that you are a non-resident personally, but that does not answer whether a company payment is Estonian-source, whether a permanent-establishment issue exists, or whether another country is taxing the same income. Keep each question on its own line. Personal status, source of income, company residence, and permanent-establishment exposure should each be reviewable without borrowing conclusions from the others.

Related: Estonia Digital Nomad Visa: A Guide to Europe's Most Digital Society.

Choose How to Pay Yourself Without Creating Avoidable Risk#

Choose a payout method only when you can defend it in one sentence and document it before money moves. Avoidable errors often happen when people pay first and classify later.

For an OU, payout choice is also a tax-timing decision. Company profit taxation is generally deferred until profits are distributed, so different payout paths can create different tax and reporting consequences. Compare options in advance, then execute with records and timing that match the filings.

| Payout path | Typical business reason | What to confirm before payment | Records and timing to keep |

|---|---|---|---|

| Work compensation | Ongoing work for the company | How payroll declarations and related reporting are affected in Estonia and your personal residency country | Basis for payment, calculation, payment proof, payroll declaration timing |

| Profit distribution | Distribution of company profits to the owner | Distribution-based company tax timing in Estonia, plus personal tax and reporting treatment where you are resident | Distribution decision, amount calculation, payment proof, reporting entries tied to the distribution date |

| Other payment | A specific non-routine payment | Whether classification and reporting are supportable in Estonia and your personal residency country | Written purpose, supporting calculation, payment proof, filing treatment note |

Use this pre-payment checkpoint whenever location, billing pattern, or payout mix changes:

- Confirm the payout label and one-sentence business reason.

- Confirm expected treatment in Estonia and your personal residency country before funds leave the company.

- Confirm which filings are affected, including payroll declarations, VAT records where relevant, and annual report steps.

- Save same-day evidence: decision note, calculation, payment proof, and filing reference.

Add a practical gate for recurring payouts: if any monthly run includes a new country, new entity, or new payment type, mark that run for manual review and do not reuse prior classification by default.

Do not treat this status as a personal shield. It is a digital identity and business tool, not a visa or citizenship status, so it should not be treated as removing potential tax exposure outside Estonia. If classification is still unclear after this check, pause the transfer and escalate before payment.

The operational goal is consistency between three things: why the money left the company, how the payment appears in your books, and how it appears in your filings. Problems start when those three versions drift apart. If the bank memo says one thing, the ledger says another, and the filing logic assumes a third, you have created a preventable review problem even if the amount itself is correct.

For recurring owner payments, add a short monthly review note before release. Confirm whether the reason for payment changed, whether the amount changed for a specific reason, and whether any country facts changed since the last run. That review can be brief, but it should exist. This shows that recurring payments were still reviewed as current decisions, not treated as permanent defaults.

You might also find this useful: How to Legally Avoid Double Taxation: A Freelancer's Guide to Tax Treaties.

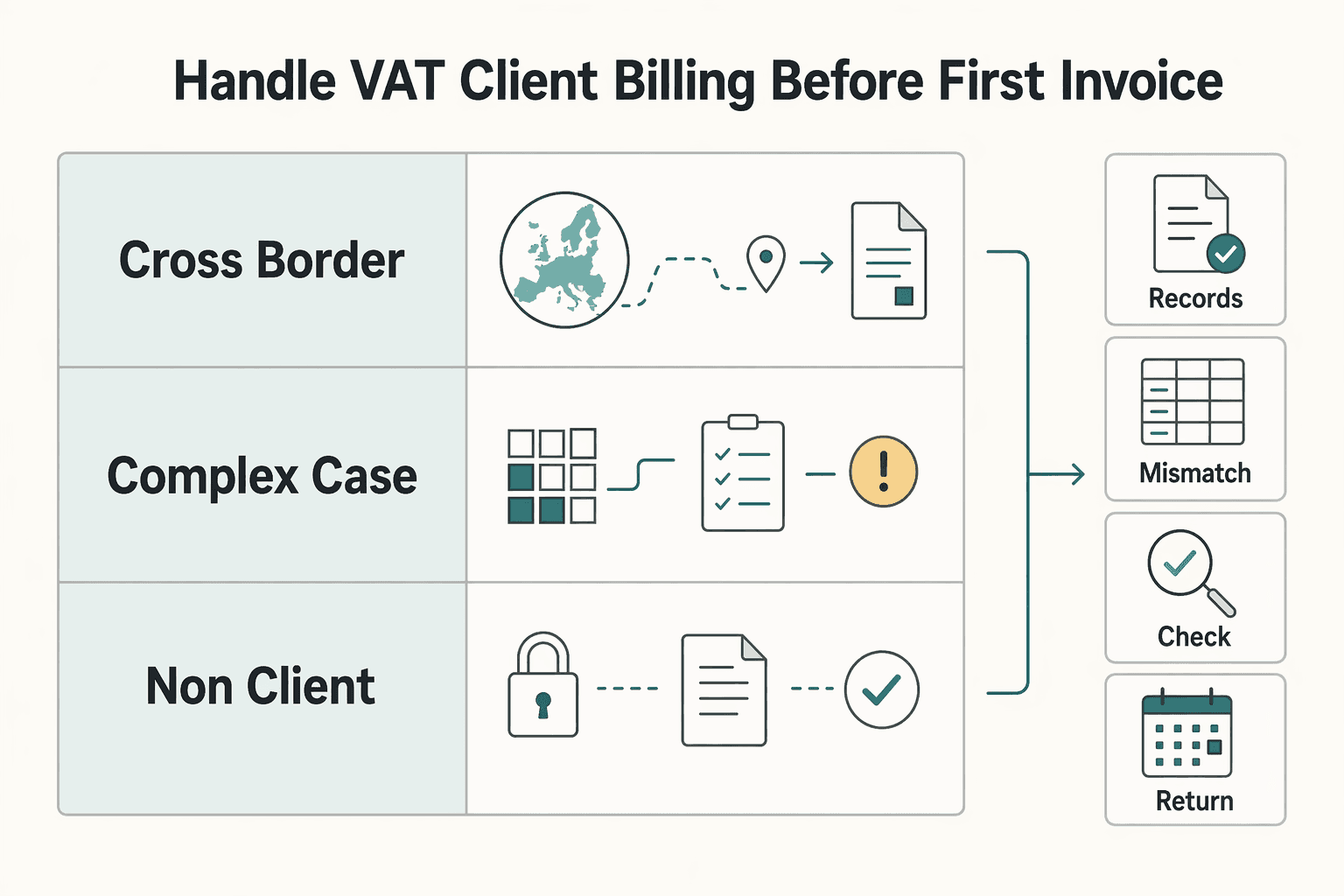

Handle VAT and EU Client Billing Before Your First Invoice#

Set VAT logic before you send invoice one. Treat value-added tax as setup work so your invoice template, client intake, and filing calendar match the transactions you plan to run.

For EU billing, treatment can vary by client type and cross-border pattern, so a single default invoice format may not fit every case. Build a small decision sheet first, then align your invoice fields and calendar to that sheet.

| Client pattern | Pre-invoice check | Operational impact |

|---|---|---|

| EU cross-border B2C e-commerce supplies in covered categories | Whether the EU-wide EUR 10 000 threshold is relevant to your specific supplies | Can affect where VAT is due and whether OSS is practical |

| Cross-border supplies that fit an OSS scheme | Whether to register in one Member State as your Member State of identification | VAT declaration and payment for supplies in that scheme can run through one portal |

| Complex cross-border facts with unclear treatment | Whether to request a VAT Cross-border Ruling in a participating country where you are VAT registered | More upfront effort, but clearer treatment before recurring invoicing |

| Non-EU client mix | Whether any part of the offer may still create EU VAT obligations | Avoids assuming non-EU billing is automatically outside EU scope |

Use this checkpoint before recurring invoices:

- Classify each offer and client route, then map which supplies may fall under an OSS scheme. If you choose an OSS scheme, declare all supplies that fall under that scheme via the OSS return.

- Check whether the EUR 10 000 threshold is relevant in your case, without assuming it applies to every service or transaction type.

- Lock filing cadence before go-live: OSS returns are quarterly for Union and non-Union schemes, and monthly for the import scheme.

- Keep regular VAT returns on your calendar. OSS returns are additional and do not replace the standard VAT return.

- If treatment is unclear, use conservative invoice wording and pause automation until reviewed.

For genuinely complex cross-border arrangements, CBR lets taxable persons request an advance ruling in a participating EU country where they are VAT-registered, subject to that country's national VAT-ruling conditions.

Keep a minimum evidence pack from invoice one: client classification record, threshold assessment note, VAT treatment rationale, and proof of what you filed and when. When recurring billing starts, review one sample invoice per route each period to confirm the setup still matches current facts.

A strong practical habit is to separate invoice generation from invoice release. Generate the draft only after client classification is complete, then check the VAT route against your decision sheet before sending. This is especially useful when multiple client routes share the same billing system. It reduces the chance that a default template applies the wrong treatment simply because a prior invoice used it.

Another useful control is route-based review rather than only client-based review. If several clients fit the same billing pattern, test one invoice from that route each period against the original setup. If one route changes, do not assume the others remain correct by association. Recheck the route itself, then the invoices created from it.

Keep a Minimum Evidence Pack That Survives Cross-Border Scrutiny#

Your evidence pack should let a reviewer trace each cross-border tax claim to a dated record quickly. Build it early, keep it compact, and fix any claim that cannot be tied to clear documentation.

Keep underlying business records separate from treaty-residency analysis. Keep dated records of the facts you relied on, then maintain a short treaty note listing the convention text you applied.

Use one index page that maps each claim to its proof and date so the file stays reviewable.

| Evidence item | What to keep | Why it matters |

|---|---|---|

| Treaty text reference | The U.S.-Estonia convention details used for the position, with treaty dates and article numbers | Shows which instrument governed the analysis |

| Treaty reasoning note | One-page memo referencing Article 4 (Resident), Article 23 (Relief from Double Taxation), and Article 22 (Limitation on Benefits) | Shows how residency, relief, and treaty-benefit eligibility were assessed |

| Supporting records log | Dated records linked to each material cross-border claim | Lets a reviewer trace key claims quickly |

| Procedure note | A brief note on when Article 25 (Mutual Agreement Procedure) and Article 26 (Exchange of Information and Administrative Assistance) may become relevant | Keeps dispute and information-exchange handling tied to treaty text |

For U.S.-Estonia treaty positions, identify the convention version used, including the signing date of January 15, 1998 and the general effective date under Article 28 of 1 January 2000, then list the article numbers you applied.

Run a recurring checkpoint to keep the pack usable:

- Match each material treaty claim to a dated supporting record.

- Re-test the treaty memo when residency facts or payment routes change.

- Confirm the memo still addresses Article 22 before claiming Article 23 relief.

- Flag unresolved treaty-eligibility questions before the next recurring payout cycle.

One failure point is claiming relief from double taxation without a clear Article 22 eligibility analysis. Document conflicts early so you can support information exchange requests under Article 26 and preserve a clean path to Article 25 if needed.

Before your next payout or filing cycle, pressure-test your assumptions with the tax residency tracker.

Think of the evidence pack as a chain of explanation, not a document dump. A reviewer should be able to start with the claim, open the index, find the source record, and understand why that record supports the claim without reading your whole archive. If the reviewer has to infer dates, guess versions, or compare mismatched records manually, the pack is harder to defend than it needs to be.

It is also worth adding a simple version habit. When a memo changes because facts changed, keep the old version and date the new one instead of overwriting it. That way your file shows what you believed at the time of each action. That time-sequenced record is often more persuasive than a single polished memo created after the fact.

Know the Reporting Touchpoints You Cannot Ignore#

Treat reporting steps as unresolved until you verify them from official tax authority instructions. Those tax-reporting details are not established here, so any EMTA schedule, filing ownership, declaration flow, or correction process should be marked as unknown until verified.

One excerpt in the current material is conference coverage from Latitude59, including a May 22, 2025 publication date and a 5.4% of GDP defense figure. That is not tax administration guidance, so it should not be used to set compliance actions.

Use one reporting calendar, but keep each line open until verified. If a line is unknown, keep it visible and assigned instead of silently assuming prior practice is still correct.

| Calendar line | Record now | Gate before next recurring payment |

|---|---|---|

| Filing item | Return or declaration name, placeholder if unknown | Confirmed in current official instructions |

| Reporting owner | Payer, recipient, or both, if known | Written owner assignment with date |

| Period and deadline | Covered period and target date, if known | Date verified from official instructions |

| Proof artifact | Receipt or submission acknowledgment slot | Linked once filing is completed |

Run a monthly reconciliation so uncertainty does not compound:

- List all payments made in the month by flow.

- Map each payment to the expected reporting line.

- Flag unknown, missing, or inconsistent items.

- Assign an owner and close each open item before the next cycle.

Add one escalation rule to this calendar: if the same unknown appears in two consecutive cycles, require advisor review before the next payout window.

To avoid memory-based filing, keep a repeatable checklist tied to filing artifacts while core reporting details are still being verified.

A good reporting calendar is not just a list of dates. It is also a control against drift. If a payment type appears in the ledger but not in the calendar, add it. If a filing artifact is missing, do not treat the task as complete just because someone says it was submitted. Completion should mean there is a linked proof artifact and a recorded owner for any follow-up.

When you do not yet know the exact reporting treatment, the safest path is usually to preserve visibility. Leave the item open, note what still needs verification, and assign a next step. Unknowns become risky when they disappear from the workflow, not only when they exist.

Spot the Red Flags That Mean You Should Talk to a Pro#

Escalate when your residency and filing position cannot be explained clearly with dated records and a treaty-consistent legal path.

The biggest red flag is unresolved residency conflict across countries. In Estonia, individual residency can turn on residence or the 183-days-over-12-consecutive-calendar-months test, while treaty provisions can override domestic treatment in cross-border cases. If those tests point in different directions and you cannot reconcile them, get specialist advice before the next filing cycle.

| Red flag | Why it matters | What to bring to the advisor |

|---|---|---|

| Residency outcome differs across countries | You can file under the wrong status, and treaty analysis can change whether Estonia treats you as resident or non-resident | Day-count timeline, travel history, residency notes, treaty article references |

| Your residency-related circumstances changed but were not formally handled | Individuals must notify the tax authority when residency-related circumstances change, so an old position may no longer match current facts | Before-and-after timeline, day-count records, and any notifications you made |

| You rely on older internet guidance | Published guidance may differ from what you originally used | The exact page and date you relied on and the Estonian Tax and Customs Board guidance you checked |

| Your records do not support timing and decisions | You may not be able to defend why a residency or reporting assumption was made when it was made | Dated decision notes, invoice and ledger links, and filing confirmations |

Two practical checkpoints: notify the tax authority when residency-related circumstances change, and complete Form R for determining tax residency. If you rely on treaty relief, anchor your memo to the treaty article you are using, such as Article 23 on relief from double taxation, and confirm your facts support eligibility. Treaty benefits are not automatic where a structure looks like treaty shopping.

When you brief an advisor, include the question you need answered, the decision deadline, and the current assumption you are using until advice arrives. That reduces back-and-forth and helps you avoid missing filing windows while waiting.

If your position depends on treaty interpretation and you also have conflicting residency signals, escalate now. If the conflict still cannot be resolved between jurisdictions, document that and assess whether Article 25 (Mutual Agreement Procedure) is relevant.

It also helps to define what success looks like before the call or memo request. Are you asking whether a payment can go out now, whether a filing needs correction, or whether a residency conclusion is still defensible? Narrow questions get better answers. Bring the shortest possible set of records that shows the issue clearly, but make sure that set includes the dated facts, the current assumption, and the deadline that makes the issue urgent.

Use Gruv Controls to Keep Your Tax Story Audit-Ready#

Audit-ready records are easier to defend when each income event is traceable end to end with dated records and stable IDs. If that chain breaks, resolve it before filing.

A practical standard is filing-grade metadata. Filing artifacts such as Form 20-F explicitly state scope and identifiers, for example period covered, filing date, and file number, then carry consistent identifiers across related records. At minimum, each entry should include date, period tag, counterparty, amount, and currency.

Add a short exception note whenever a record is corrected after the first entry. Include what changed, why it changed, and who approved it. That keeps later reviews focused on facts instead of guesswork.

The most useful control is consistency across systems. If your invoice tool, bank records, ledger, and document store all describe the same event differently, you create avoidable reconciliation work. Stable IDs and dated notes reduce that friction. The goal is not perfect software architecture. It is to make sure one reviewer can trace an event without needing unwritten context from the person who entered it.

Build one chain per income event#

Treat each invoice as the start of a chain that stays intact through collection and payout.

- Record invoice issuance and payment confirmation dates with clear timestamps.

- Keep approval context so the business purpose is reviewable later.

- Retain status history for reversals, exceptions, and manual changes.

- Run a monthly checkpoint before close so each outbound payment maps to a source event.

Where one income event later connects to several actions, keep the branch points visible. For example, if one collection later leads to a conversion and then a payout, the chain should still show that each step belongs to the same source event. A reviewer should not need to guess whether the payout came from business income, an internal transfer, or a different transaction entirely.

Reconcile collections, FX, and payouts before sign-off#

Reconcile at transaction level, not only net totals, so timing and amount differences are explainable.

- Match collected funds, balance movements, conversions, and payout outcomes by stable ID.

- Flag and resolve any payout that cannot be traced to a source invoice or approved transfer.

- Sign off only after breaks are resolved and notes are complete.

If there is a timing gap between collection and payout, note it instead of assuming the sequence is obvious. If there is an FX difference, note where it arose and which records show it. Transaction-level sign-off works best when small differences are explained while the context is still fresh.

Mask sensitive artifacts without losing review value#

Keep sensitive compliance and tax artifacts structured and access-controlled while preserving reviewability.

- Use masked views for routine review.

- Restrict unmasked access to authorized reviewers.

- Keep an access log of who viewed or changed sensitive records.

Masked review only works if the visible fields still let someone test the logic. Keep enough metadata visible to confirm the chain, the date, and the reason for the record without exposing more than necessary. That balance makes routine internal review faster while still protecting sensitive information.

Make Your Next Move Only After You Pass the Checklist#

Now convert the FAQ into action. Before any invoice or withdrawal, run this checklist and pause if one line is unclear.

Start with status assumptions. e-Residency is a digital ID for running a company remotely, not legal residency. Reconfirm personal tax residency separately, then check current EMTA guidance for your exact fact pattern and log the date.

Next, validate execution points for this transaction. Confirm a payout method you can defend, the VAT treatment, and the reporting responsibilities across relevant countries. Do not assume prior setups still apply, especially for recurring invoicing, because VAT implementation and digital reporting requirements can differ by country.

Then compile one evidence pack per action before money moves. Include a dated decision note, invoice and payout identifiers, reconciliation output, and the related reporting-calendar entry. Add a short cross-border note when social-tax issues may apply.

Close with an accountability step: set who will verify filing completion and where proof artifacts will be stored. This helps keep unresolved tasks from drifting into the next month.

Treat ambiguity as a hard stop. If you cannot explain the tax logic in plain language, escalate to a qualified tax professional and document the question, advice, date, and assumptions.

Status: digital ID status confirmed, personal tax residency reconfirmed, relevant EMTA guidance checked.Execution: payout route, VAT treatment, and reporting duties validated for this transaction.Evidence: decision note, identifiers, reconciliation snapshot, and calendar entry stored together.Escalation: unresolved points sent for advice early, with written records saved.

One final discipline makes the checklist more useful: sign it only for the transaction in front of you. Do not treat a prior signed checklist as standing approval for later invoices or payouts. Facts change, routes change, and payment labels change. A short current checklist is more protective than a detailed old one.

Frequently Asked Questions

Does e-Residency change my personal tax residency?

No. It is a digital identity status, not tax residency, and it does not grant citizenship or physical residence rights in Estonia or the EU. Treat personal tax residency as a separate determination and document it independently from your e-Residency records.

Can I be an e-resident and still be tax resident in another country?

Yes. You can hold this status and still be tax resident elsewhere because those are separate legal questions. The key mistake to avoid is treating the card as a residency override when filing or planning payouts.

When can a non-resident owe tax in Estonia?

A non-resident can still owe Estonian tax in specific Estonia-linked cases. One clear example is board member remuneration, which is taxed in Estonia even if the board member does not live there. Check each payment type before assuming there is no Estonian tax exposure.

Is e-Residency a legal way to avoid taxes in my home country?

No. The program is explicitly not a way to avoid paying taxes. Tax outcomes come from underlying legal facts, such as a company being legitimately tax resident in Estonia under international rules, and home-country tax can still apply, including to dividends.

What should I verify before paying myself from an Estonian company?

Before paying dividends, confirm share capital has been paid into the company bank account and the annual report has been submitted to the Business Registry. Then confirm how the payout is treated in Estonia and in your personal tax-residency country, since dividend income may still be taxed where you are tax resident. Keep dated records of these checks with the payout approval and filing notes.

How do tax treaty rules help with double taxation without removing core filing duties?

Tax treaty rules are designed to reduce double taxation and prevent fiscal evasion. Relief is not automatic, and benefits can be denied in treaty-shopping cases. Treaty relief does not automatically remove baseline filing and reporting duties in each relevant country while claiming treaty relief. For a practical walkthrough, see How to Legally Avoid Double Taxation: A Freelancer's Guide to Tax Treaties.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- taxation-customs.ec.europa.eu/archives/taxable-persons/vat-cross-border-ru...trusted

- taxation-customs.ec.europa.eu/system/files/2016-09/summary_vat_greenpaper.pdftrusted

- remoteworkeurope.eu/insights/estonia-tax-guide-digital-nomads-2026external

- unicount.eu/en/register-an-estonian-ou-online-in-2025-pr...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Should You Use Estonia e-Residency for Your Independent Business?

If you want a clear decision before paperwork, treat this as a fit test, not a sales pitch. Estonia e-Residency can help independent professionals, but only if you separate digital identity, immigration, and tax decisions from day one. Use the decision rules and application sequence below to keep execution clean.

Estonia Digital Nomad Visa Without Filing Surprises

Plan first, book later. Use this as a planning and verification guide so you catch preventable filing mistakes before they become expensive ones.

How Freelancers Can Legally Avoid Double Taxation With Tax Treaties

Classify the tax problem before you touch a return. If your income is mostly personal service fees across borders, this guide fits. If your issue is C corporation profits and shareholder dividends, you are solving a different problem.