Quick Answer

Start by deciding residency status, then pick the filing route that matches your facts and records. For italy tax for expats, the practical path is to document resident vs non-resident treatment, confirm whether Modello 730 or Modello Redditi PF applies, and keep US-side reporting separate through Form 8938 and FBAR. If any benefit depends on assumptions instead of evidence, treat it as unavailable until reviewed.

Taxes in Italy as an Expat Freelancer Without Guesswork#

Start with one objective: make filing choices you can defend with records, not assumptions. As a freelancer or consultant, you do not need to predict every line item on day one. You need a position that stays consistent from client onboarding to invoicing to return prep. The avoidable mistake is signing work or claiming a benefit first, then trying to explain the tax result later. You are aiming for a position that holds together all year, not a best-case assumption that falls apart when forms and bank records have to match.

The first question is whether you are treated as a tax resident or non-resident for the year. That answer drives the filing route, the income scope, and the proof you need to keep. It also tells you which later calculations are worth doing and which are a waste of time until residency is settled.

Special regimes need their own review. The flat-tax and impatriate rules are different options for different fact patterns, and eligibility gets overread fast when you start from generic summaries instead of your own file.

Before you commit, do three things:

- Draft a short residency memo for the tax year using facts you can already prove.

- Build one evidence folder with registration records, address history, income breakdown, and client geography.

- Tag each point as confirmed, uncertain, or advisor-needed. If eligibility is uncertain, treat the benefit as unavailable until confirmed.

That last step matters because people often price the year around an assumed benefit, then learn too late that flat-tax or impatriate treatment does not fit the facts. If a point is advisor-needed, write the question down in plain English now so it does not disappear into filing-season stress. When the file is mixed, a short technical review is usually cheaper than fixing the wrong position after filing.

Once that groundwork is done, get the labels straight before you calculate anything. If double taxation is part of your year, you may also find this useful: How to Legally Avoid Double Taxation: A Freelancer's Guide to Tax Treaties.

The Terms That Actually Change Your Tax Outcome#

Most avoidable mistakes start before the math. They start when tax labels are used as if they mean the same thing across countries, forms, and special regimes. Your outcome gets much easier to manage when each term points to one authority and one filing home. When labels bleed into each other, people compare the wrong options, save the wrong documents, and answer the same question twice in different ways.

Keep these categories separate:

Resident/non-resident: decide the status for the filing year and document the facts behind it.Modello 730/Modello Redditi PF: treat these as separate Italian filing paths and confirm which one applies.Partita IVA,forfettario regime,lavoratori impatriati: these are setup and eligibility decisions, not interchangeable shorthand.

On the US side, apply the same discipline. Form 8938, FATCA, and FBAR are related, but they do not go to the same place and they do not serve the same purpose. Form 8938 reports specified foreign financial assets above the applicable threshold and is attached to your income tax return. One IRS baseline example uses an aggregate value above $50,000 for certain taxpayers, with higher thresholds for joint filers and taxpayers residing abroad. If no income tax return is required for the year, Form 8938 is not required. FBAR is separate from Form 8938 and goes through the FinCEN electronic filing channel. FATCA is the broader regime connected to Form 8938.

A short glossary helps here. Put the term in one column and its filing home in the other: Italy return, US return attachment, or FinCEN e-filing. Mark each item as defined now or pending review. If a label does not map cleanly to one authority and one channel, stop there. Terms without a clear home are how duplicate reporting and missed reporting begin.

With the language sorted, move to the decision that changes almost everything else: residency. Related: The 2025 Global Digital Nomad Visa Index: 50+ Countries Compared.

Are You an Italian Tax Resident This Year#

Settle residency before you do any serious estimate. If the facts are mixed, treat the position as high risk and work from resident treatment until your records support non-resident treatment. In practice, many cross-border filing problems start here. The hard part is not usually counting days. It is proving where your real base was when days, registrations, and work activity point in different directions.

Use a strict yes-no sequence and answer it from documents, not memory:

- Were you in Italy for most of the tax year, often referenced as

183 days or more, depending? - Do your home-base facts point to Italy, for example domicile for more than six months?

- Do your registration ties point to Italy, including the Anagrafe (Italian public registrar)?

A common failure mode is counting days carefully while leaving the harder ties undocumented. Another is assuming that a Codice Fiscale settles the issue. It does not. On its own, a Codice Fiscale does not make you an Italian tax resident.

Messy years need both narratives tested against the file, not against the result you want. Frequent travel combined with strong Italy ties and ongoing Italian client work can support resident treatment, which puts worldwide income in scope. A clear foreign base with limited Italian presence supports a non-resident profile, but only if you document that position and separate Italian-source income from everything else. When both stories are partly true, do not force a non-resident answer without proof.

Before filing season, turn that judgment into a verification pack:

- Prepare a short residency memo with your timeline, addresses, and country-by-country presence.

- Attach support for each claim, such as travel logs, registration records, leases, invoices, and account mapping.

- Label each item as proven, uncertain, or missing. If key proof is missing, keep the more conservative filing posture.

The goal is not perfect paperwork. It is a filing story your records can support if someone asks how you reached it. Keep the memo short enough that another person can follow it without retelling your whole year. Once residency is set, the operating setup becomes a practical choice instead of a guess.

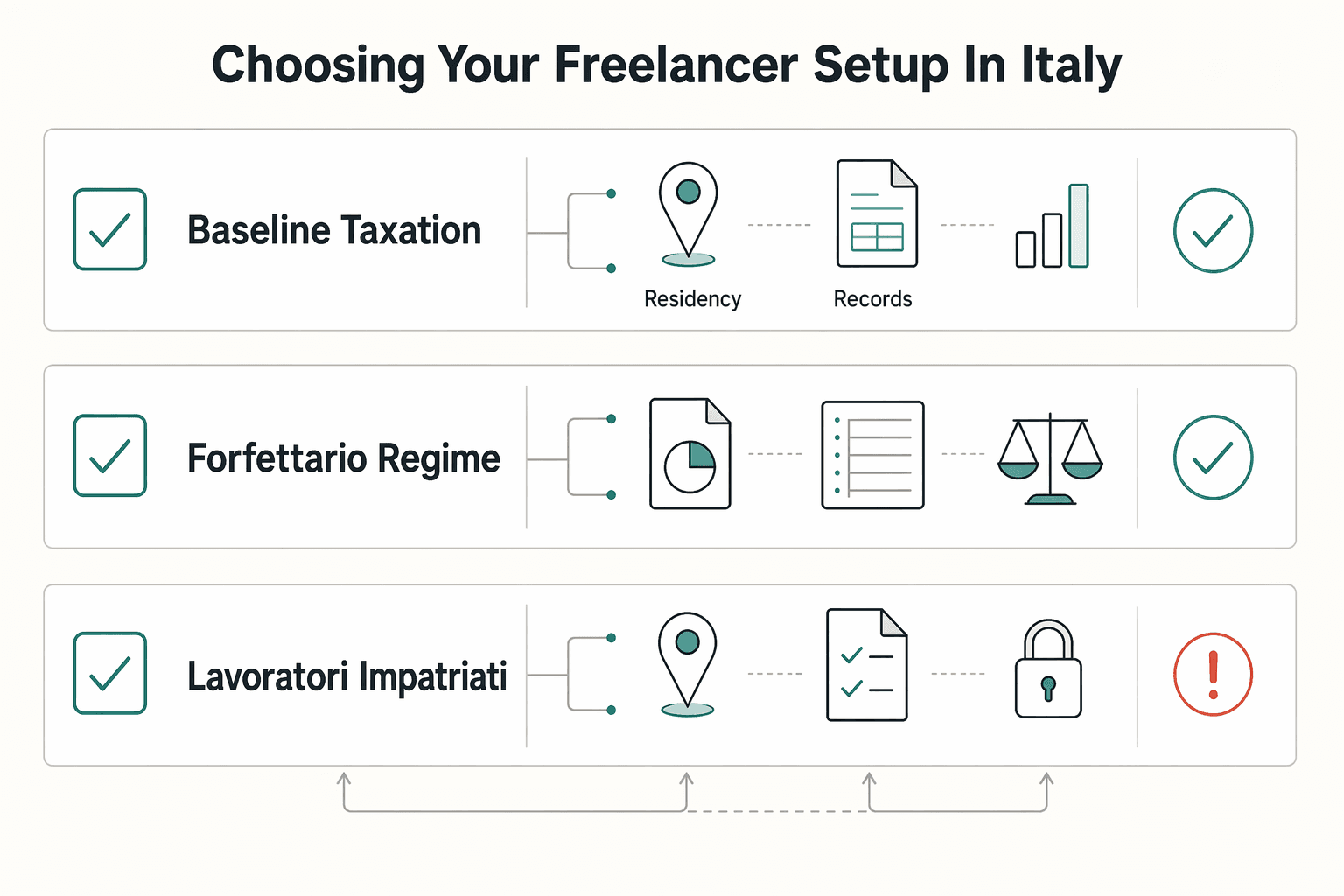

Choosing Your Freelancer Setup in Italy#

Choose the operating setup before you price clients or sign recurring work. If you expect ongoing activity in Italy, start with Partita IVA planning. The common failure mode is treating setup like admin cleanup and only later discovering that the chosen regime does not fit your income, deductions, or the evidence needed to support eligibility. By then, invoices are already out, habits are set, and fixing the mismatch costs more than getting the setup right early.

This is a compliance and cash-flow decision, not a branding decision. The choice between baseline taxation and the forfettario regime should follow your income pattern, deductible cost profile, and medium-term plan. If costs are meaningful, simplicity can be expensive. If costs are light, extra complexity may create work without enough return. If you are also considering lavoratori impatriati, run that as its own eligibility review and work from documents, not summaries.

Before you invoice long-term clients, confirm the core registrations are actually in place. Freelancers are generally expected to have a codice fiscale, VAT registration, and INPS registration. Social security contributions are mandatory, invoice compliance depends on correct VAT coding and the required electronic format, and filing and contribution deadlines vary by income and regime. That means the setup choice affects more than tax cost. It changes how you bill, what you need to save, and what you need to calendar. A setup decision that looks minor in spring can create avoidable problems in autumn if the invoice rules and payment obligations never matched the regime you picked.

| Lane | What to verify first | Common failure mode |

|---|---|---|

| Baseline taxation | Expected income pattern and deductible cost profile | Choosing by habit without checking cash impact |

forfettario regime | Eligibility evidence, record rules, and deduction impact | Choosing simplicity, then finding a mismatch later |

lavoratori impatriati | Whether your facts and documents support access | Assuming online summaries are enough proof |

Keep one caution in your notes: the Flat tax regime for foreign retirees is a niche path. Do not assume it applies to active freelance work just because it appears in expat search results. Search results often collapse very different regimes into the same list. Your file cannot.

Before you lock anything in, write a one-page setup memo that records the option you chose, the option you rejected, and why. Keep registration confirmations, tax IDs, and setup correspondence in one folder. Calendar filings, INPS payments, and tax prepayments using estimated income. Then test invoice readiness before invoice one, using the correct VAT coding and required electronic format. The memo does not need to be elegant. It just needs to show what you chose, what proof supports it, and what still needs confirmation.

If two options still look plausible, pick the one with clearer eligibility evidence and a cleaner audit trail. That is usually a better trade than chasing a benefit you may struggle to support later. If you want a deeper dive on the visa side, read Italy Digital Nomad Visa: Your Guide to La Dolce Vita. Once the setup is fixed, you can model take-home on the right base instead of guessing from a headline rate.

How the Italian Tax Stack Hits Real Take Home#

Do not price freelance work from a headline rate. Real take-home comes from a stack of rules and obligations, so the useful model starts with your net target and works backward. Scenario work beats false precision here. What matters is not pretending you know every line today, but knowing which layers belong in the model before you quote work.

Start with scope. Resident treatment generally pulls worldwide income into the calculation, while non-resident treatment generally limits the calculation to Italian-source income. If scope is wrong, every later estimate is wrong with it.

Then layer in the taxes that actually hit the year. Public summaries describe a progressive national band of 23% to 43%, with regional and municipal taxes often in the 1% to 3% range. Those are planning ranges, not guaranteed outcomes. They help you frame scenarios, but they do not replace a calculation tied to your status, income mix, and filing route. They give you a frame, not a reason to quote one blended number and move on.

Before you call any number net, include contributions where they apply, the filing obligations that come with your route, and the prep overhead tied to that route, often Modello 730 or Modello Redditi PF. In practice, this is where underpricing starts. The headline rate looks manageable until local taxes, contributions, and return costs land together.

A practical rate-setting pass should include:

- two scenarios, one conservative and one expected

- scope, national tax, local tax, contributions, and filing costs in each scenario

- any ambiguous item marked

confirm-with-advisor, including the often repeatedaround 3.9%claim - a mixed-income test if you earn from both Italian and non-Italian clients

At this stage, a rough model is fine as long as you are honest about uncertainty. Price from target post-tax take-home, back into required gross revenue, and hold back cash against the more conservative case until the missing facts are confirmed. A conservative model is not pessimism. It keeps you from borrowing from your tax reserve later.

Red flag: treating one percentage as your all-in burden. That shortcut is where late-year cash shortfalls usually begin. A solid estimate only helps if the filing operation keeps pace, which is why the next step is form choice and deadline control.

Filing Operations and Deadlines Without Last-Minute Panic#

Picking the form early saves more trouble than chasing the deadline later. The choice changes workflow, timing, and payment handling, so make it early enough to organize the year around it. In Italy, natural persons file with Modello 730 or Modello Redditi PF based on income profile, not preference. People often fixate on the deadline date and miss the steps around it. That is what creates last-minute panic.

| Filing path or channel | Typical fit | Baseline deadline (year after tax year) | Practical output |

|---|---|---|---|

Modello 730 | Employees and retirees with qualifying income sources | 30 September | Filed return record |

Modello Redditi PF | Broader personal profiles, including many self-employed cases | 31 October | Filed return plus payment handling, often including F24 generation |

| Registered post | Non-residents abroad who cannot file electronically | 30 November | Paper filing proof and mailing record |

Tax returns are filed every year, and some non-resident cases are restricted to Modello Redditi PF only.

The easier way to run the year is to work backward from the filing date. Keep records current during the year, then do a pre-submission reconciliation across invoices issued, cash received, and the categories used in the return. If those three views do not line up, fix the mapping before you file. Filing should be the final assembly step, not a reconstruction project built from missing documents and memory. By the time the deadline arrives, the return should already be mostly assembled because your records were kept in the right shape all along.

Keep one evidence folder for each tax year:

- final return copy

- sending protocol downloaded from your secure area after submission

- payment confirmations, including

F24proof where relevant - correspondence with

CAFor your qualified professional

Save each proof as you go, not weeks later when portals, passwords, and memory become part of the problem. Keep the sending proof in the same place as the filed return so payment and filing records stay attached. If you also report to the US, link those records now rather than trying to reconcile them after the Italian return is done.

If You Also File in the US, Prevent Double-Reporting Errors#

The US side is mostly a consistency exercise. Treat it as one coordinated reporting job so the same foreign-asset facts show up the same way across forms and filing channels. It gets much easier once you stop treating it as cleanup after the Italian return. The goal is not to duplicate work. It is to reuse the same facts carefully so both sides of the year tell the same story.

Form 8938 is used to report specified foreign financial assets and, when required, must be attached to your annual US income tax return. A specified individual includes a US citizen, and certain specified domestic entities can also be required to file. IRS guidance for certain taxpayers references an aggregate value exceeding $50,000. If no income tax return is required for the year, Form 8938 is not required for that year.

Keep the reporting map simple:

- annual

IRSincome tax return, withForm 8938attached when required FBARfiling toFinCENthrough its electronic channel

Before filing, run one consistency check across your account records, Form 8938 inputs, and FBAR inputs so names, ownership details, and reported values line up. Use the same underlying account list, the same ownership description, and the same saved support across both filings. Filing in Italy does not remove that US step, so the clean approach is to keep one set of facts and reuse it carefully rather than rebuild the US side from scratch later.

Once that map is working, the next job is simple but important: keep the supporting documents in one place so the same facts can support both sides of the year.

Your Compliance Document Pack and Monthly Checkpoints#

Your document pack should be boring on purpose: one place, clear naming, and the same facts reused across filings. That is what keeps a cross-border position defensible when Italy, the US, and your advisor are all looking at the same year. It also cuts rework. When a question comes up, you are not rebuilding the year from email threads, bank downloads, and memory.

Keep a single year-based file set for residency evidence, Partita IVA records, Italian filing documents such as Modello 730 or Modello Redditi PF, and US confirmation records. Where relevant, store treaty notes, Certificate of Coverage, and FBAR or Form 8938 confirmations in the same structure so each filing position points back to the same underlying facts. The point is not elegance. It is traceability.

One channel rule is worth keeping in view: Form 8938 and FBAR can both apply, and one does not replace the other. Form 8938 is attached to the annual IRS income tax return when required. FBAR is FinCEN Form 114 and is filed directly with FinCEN, not with the IRS.

| Item | Where it goes | What to retain |

|---|---|---|

Italian return (Modello 730 or Modello Redditi PF) | Italy filing channel | Final return copy, sending protocol, and F24 proof where relevant |

Form 8938 | Attached to annual IRS income tax return | Filed return package and attachment copy |

FBAR (FinCEN Form 114) | Filed directly with FinCEN | Submission confirmation and saved filing record |

A monthly control pass keeps the file from drifting:

- categorize new income and account activity

- reconcile account names, ownership details, and balances to your tracking records

- save new filing confirmations in the same dossier

- log unresolved classification questions for follow-up

You are not recalculating the whole year every month. You are preventing drift and catching mismatches while they are still small. Small discrepancies compound fast once one record set changes and another does not. If a filing position depends on facts you cannot evidence, stop there and get professional review before submission. That same standard answers most of the common questions below.

The Practical Next Step Most Expats Skip#

The common thread in those questions is simple: your answer is only as good as the file behind it. That is why the next move is not more reading. It is one short decision memo.

Write one decision memo now. Put your residency position, operating setup (Partita IVA and regime), filing route, and US overlap obligations in one document. Keep it short, dated, and specific enough that an advisor could review it without reconstructing your year. For each issue, note the answer you are using, the proof you already have, and the point that still needs review. That single page turns a pile of cross-border tasks into positions you can manage, review, and defend.

Start with residency because it sets scope. Resident treatment means Italy can tax income from all sources, while non-resident treatment limits scope to income earned in Italy. Record the facts and documents behind the position. If your file supports non-resident treatment, note that filing generally routes through Modello Redditi PF with non-resident status marked.

Then lock the setup decision with evidence. If professional activity has already started, include your Partita IVA opening date and confirm registration filing within 30 days from start. If you are using forfettario, track annual eligibility checks and document the EUR 85,000 revenue ceiling, EUR 20,000 labor expense ceiling, and any same-year trigger above EUR 100,000 that affects eligibility.

Run a 30-day setup sprint with dated checkpoints:

- finalize records structure for contracts, invoices, bank proofs, returns, and payment receipts

- calendar Italian milestones, including

Modello 730by 30 September 2026 and theRedditi PFpaper window from 15 April to 30 June 2026 where relevant - calendar US milestones, including

FBARdue April 15 with automatic extension to October 15 - pre-clear uncertain cross-border contribution treatment and document

Certificate of Coveragesteps when needed

The point of the sprint is to surface missing proof while there is still time to fix it. Do not wait for perfect clarity on every issue before you organize the file. Treat any unclear benefit as unavailable until eligibility and documentation are verified. Close the sprint with one reconciliation meeting with your advisor or qualified professional, and confirm that each filing position is backed by documents before submission. If you need a second read on what your file actually supports, Talk to Gruv.

Frequently Asked Questions

Am I automatically an Italian tax resident if I spend most of the year in Italy?

Treat residency status as fact-specific and confirm with a qualified advisor.

Do expats in Italy always pay tax on worldwide income?

Confirm treatment based on your specific residency status and facts.

Which form should freelancers expect to use, `Modello 730` or `Modello Redditi PF`?

This grounding pack does not support a definitive choice between Modello 730 and Modello Redditi PF. Use advisor review for form selection.

How does `Regional income tax` interact with national taxation?

Confirm current local rules before modeling.

Is the `Flat tax regime for foreign retirees` relevant if I still work as a freelancer?

Verify eligibility before relying on it.

If I am a US person, do I still need `FBAR`/`FinCEN` and `FATCA`/`Form 8938` after filing in Italy?

Italian filing does not by itself eliminate U.S. reporting. Form 8938 can be required when specified foreign financial assets exceed the applicable threshold and is filed with your annual U.S. income tax return; FBAR is a separate FinCEN filing.

What details in public summaries are too incomplete to rely on without advisor confirmation?

Avoid one-size-fits-all threshold claims. Form 8938 thresholds depend on filer category, and higher thresholds can apply to joint filers and taxpayers residing abroad.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- irs.gov/businesses/corporations/do-i-need-to-file-fo...trusted

- ssa.gov/international/Agreement_Pamphlets/italy.htmltrusted

- taxation-customs.ec.europa.eu/system/files/2020-01/tax_policies_in_the_eu_...trusted

- taxation-customs.ec.europa.eu/system/files/2017-11/taxation_paper_70.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Italy Digital Nomad Visa in 2026 for Remote Professionals

Treat this as a filing decision before you treat it as a lifestyle move. The appeal of living in Italy is obvious. Whether this works comes down to document quality, clear classification, and whether your file tells the same story from the first page to the last.

The 2026 Global Digital Nomad Visa Index for 50+ Countries

Start with legal fit, not lifestyle filters. The practical order is simple: choose a route you can actually document, then decide where you want to live. That single change cuts a lot of wasted comparison work and stops you from falling in love with places that were never a real filing option.

How Freelancers Can Legally Avoid Double Taxation With Tax Treaties

Classify the tax problem before you touch a return. If your income is mostly personal service fees across borders, this guide fits. If your issue is C corporation profits and shareholder dividends, you are solving a different problem.