Quick Answer

Use a go/no-go workflow for the uk hpi visa: verify current GOV.UK route wording before each paid action, then submit only after your records pass a consistency check. Keep a dated decision log that captures the page checked, the document matched, and the owner of the next step. Run HMRC Self Assessment on a separate track so 5 October 2025 and 31 January stay tax deadlines, not visa timing signals.

Start Here: What the UK HPI Visa Solves and What It Does Not#

From day one, treat this as a two-track plan. First, verify immigration rules before each paid step. Second, keep tax administration separate so you do not confuse HMRC deadlines with visa milestones. This article is strongest on Self Assessment mechanics, so use the GOV.UK High Potential Individual visa page and current Home Office wording for route criteria each time you act. For tax day-count planning, pair this with Understanding the UK's Statutory Residence Test (SRT).

Keep one shared decision log across both tracks. For each step, record the page checked, the date checked, the document you matched against, and the person responsible for the next action. That record turns vague confidence into a verifiable position when you are tired, rushed, or juggling several deadlines.

What this guide gives you#

Use this article as three connected tools:

- A date-based plan with checkpoints before each paid or time-sensitive decision.

- A document pack structure that records what you collected, when, and why it matters.

- Clear decision points that force a same-day official check before submission.

Use the sections in order when you are preparing, then return to the final checklist before each payment or submission. The goal is not to move slowly. The goal is to avoid preventable resets.

What it does not solve for you#

Keep visa steps and tax administration on separate tracks. These HMRC checks belong on the tax track:

| HMRC check | Grounded detail |

|---|---|

| Need to send a return | Confirm whether you need to send a tax return before registering for Self Assessment. |

| First-time online filing | Register before using the filing service. |

| Older Self Assessment account | Reactivate it before filing or your return may be delayed. |

| Sole trader income trigger | If sole trader income is more than £1,000 in a tax year (6 April to 5 April), registration duties apply. |

| Late notification and payment | Guidance flags potential penalties after 5 October 2025, and payment is due by 31 January. |

| Registration detail | Keep your National Insurance number ready for registration. |

Those checks can become urgent during a move, but they do not tell you whether your route is ready. Label your tasks by track so one urgent item does not hide another.

Most preventable errors come from stale assumptions. Add a final verification checkpoint before every submission. If your move timing is still fluid, pair this plan with Understanding the UK's Statutory Residence Test (SRT).

If you want a deeper dive, read The 2025 Global Digital Nomad Visa Index: 50+ Countries Compared.

Define the Rules Before You Plan Your Move#

Build a rule log before you spend money. If a core term is not confirmed on current official pages, treat your plan as provisional.

Treat route-specific terms as unverified until you confirm them on current official guidance.

For planning the route, verify these items first:

- the exact eligibility terms for your route

- the timing rules and deadlines for your case

- whether any third-party verification is explicitly required

Keep two columns in your notes: confirmed on official pages and unverified. Only take paid steps from the confirmed column.

For each confirmed line, add a short proof note in plain English. Use a simple format: what you checked, where you checked it, and what that means for your next action. If you cannot write that note clearly, move the line back to unverified.

If any route-specific timing or list-based requirement is unclear, pause and verify it on official pages before you pay for anything. Keep a dated check before each paid step so your decisions follow current wording, not third-party summaries.

The same sequencing discipline shows up in HMRC guidance. First-time online filers must register for Self Assessment before using the service. Existing accounts may need reactivation, and filing without reactivating can delay a return. Late notification can lead to penalties (for example, after 5 October 2025 for the prior tax year), and 31 January remains the payment date. Once your rule log is clean, run a quick fail-fast pre-check before any spend.

Run a 15-Minute Eligibility Pre-Check Before Spending Money#

Use a fail-fast check before you pay for anything. This checklist applies to Self Assessment tax steps, not route eligibility rules. One unresolved blocker is enough to pause and verify on live GOV.UK pages.

Mark each line Yes, No, or Unsure, and attach proof for every answer.

| Pre-check item to verify now | Current answer | Evidence needed per answer | Verify now trigger |

|---|---|---|---|

| Do you need to send a tax return before registering for Self Assessment? | Yes / No / Unsure | Dated notes from the current GOV.UK guidance you used | Unclear whether you need to file |

| If you are filing for the first time, are you registered for Self Assessment before using the online filing service? | Yes / No / Unsure | Registration status details and dated notes | First-time filing with no confirmed registration |

| If you have registered before, do you need to reactivate your Self Assessment account? | Yes / No / Unsure | Account status records and dated notes | Prior registration exists but reactivation status is unclear |

| Are your records ready (for example bank statements or receipts)? | Yes / No / Unsure | Organized records for the return | Missing or incomplete records |

Set a short timer, complete each row, and convert every Unsure into a specific verification action with an owner and deadline. Keep a strict rule: no filing while any core row is unresolved. Also note any applicable deadlines shown on the page you used (for example, 5 October 2025 for telling HMRC in the described cases, and 31 January for tax bill payment).

When a row stays unresolved, write the exact blocker. Is the blocker missing evidence, conflicting dates, unclear policy wording, or unclear account status? Clear blocker labels prevent wasted research and help you decide whether to pause, escalate, or defer.

Keep one folder for dated page captures and personal records. If an answer has no document and no date, treat it as unverified. Before moving on, do a quick consistency sweep so names, dates, and filing assumptions line up across all rows.

Build Your Document Pack in the Right Order#

Sequence matters more than speed. Confirm account and record prerequisites first, then move to filing steps.

Use two lanes in your folder: verified now and pending official check. If an item stays in pending official check, do not rely on it for filing.

| Pack item | What to store now | Verification gate before filing | Failure if skipped |

|---|---|---|---|

| Self Assessment registration status | Record showing whether first-time registration is needed | Confirm requirement before online filing | First-time filers must register before using the service |

| Account access status | Note confirming whether an older account needs reactivation | Confirm status before filing | Filing can be delayed if an existing account is not reactivated |

| Core records | Dated bank statements or receipts folder | Confirm records are complete and current | Missing records can undermine accurate filing |

| Identity checkpoint | National Insurance number readiness note | Confirm NI number is available before registration | Registration is blocked without an NI number |

Track each file with owner, issue date, expiry date, source, status, and last verified date. If owner or last verified date is blank, the item is not ready.

Use a naming pattern that makes review easier: document type, person name, issue date, and version. Keep older versions instead of overwriting them. That makes it easier to explain what changed if a later check reveals a mismatch.

Before you submit, run a final consistency audit on the pack itself. Confirm the same personal details appear across all required records, confirm no file is stale, and confirm each document supports a specific filing entry.

Keep HMRC dates in the same folder but on a separate timeline: late notification for the referenced year can trigger penalties after 5 October 2025, and payment is due by 31 January. With records in place, you can map a realistic week-by-week plan.

Map a Week-by-Week Timeline From Decision to Arrival#

Use a gated weekly plan, not a fixed arrival promise. Every block stays provisional until you confirm current route guidance.

| Week block | Checkpoint | Verification gate before moving | Delay buffer action |

|---|---|---|---|

| Week 1 | Scope and guidance check | Confirm the current official guidance you are relying on and log the date checked | Pause paid steps if any core rule is unclear |

| Week 2 | Record consistency check | Confirm names, dates, and identity details match across your records | Fix conflicts before moving on |

| Week 3 | Submission readiness | Submit only when the required information is complete and internally consistent | Move submission to the next block if any required item is unresolved |

| Week 4 | Post-submission follow-up | Confirm any follow-up requests are resolved before making fixed plans | Shift target arrival timing if follow-up is still open |

| Week 5+ | Decision planning | No verified inside-versus-outside decision window is provided here | Keep travel and housing commitments flexible |

| Final pre-travel block | Arrival readiness | Recheck status and match identity details to travel bookings | Resolve mismatches before non-refundable spend |

Treat each handoff between blocks as a checkpoint, not a formality. If a prior block is incomplete, do not force the next step. Forced sequencing can create expensive rework in later weeks.

Add one formal buffer checkpoint after submission. If records need correction, move the plan by a full block rather than compressing later steps.

If freelance income may exceed £1,000 in a tax year, add Self Assessment actions to this same calendar. Register for Self Assessment when required, keep your UTR ready for online filing, note the HMRC notification deadline (5 October 2025 for the 6 April 2024 to 5 April 2025 tax year in the provided guidance), and plan to pay your tax bill by 31 January. If your structure choice is still open, compare setup tradeoffs with Sole Proprietorship vs LLC for Global Freelancers in 2026.

A simple closeout rule helps: end each planning week by listing what is verified, what is pending, and what cannot move until verification is complete. That keeps momentum without turning uncertainty into accidental commitment.

Choose the Right Filing Path Outside vs Inside the UK#

Treat filing location as a live verification decision. Rely on current GOV.UK wording immediately before submission.

| Decision point | Outside the UK (working plan) | Inside the UK (working plan) | What you must verify on GOV.UK before submit |

|---|---|---|---|

| Start point | Unverified here | Unverified here | Current route criteria and location rules on submission day |

| Required steps | Unverified here | Unverified here | Exact step order and required documents for your location |

| Timing expectations | Unverified here | Unverified here | Any official timing language, treated as planning guidance only |

| Dependants | Unverified here | Unverified here | Current dependant rules for your case and filing location |

In practice, filing location can change your planning risk. In both cases, rely on live wording.

Run one final pre-submit check and log it:

- Reopen the relevant GOV.UK page and record the date and time checked.

- Confirm your filing location still matches live criteria.

- If dependants are included, confirm current rules for your case.

- Confirm you have completed any stated prerequisites before submitting.

That is simple risk control. The same pattern appears in HMRC guidance: missing prerequisites can delay submission, and missed notification dates can trigger penalties.

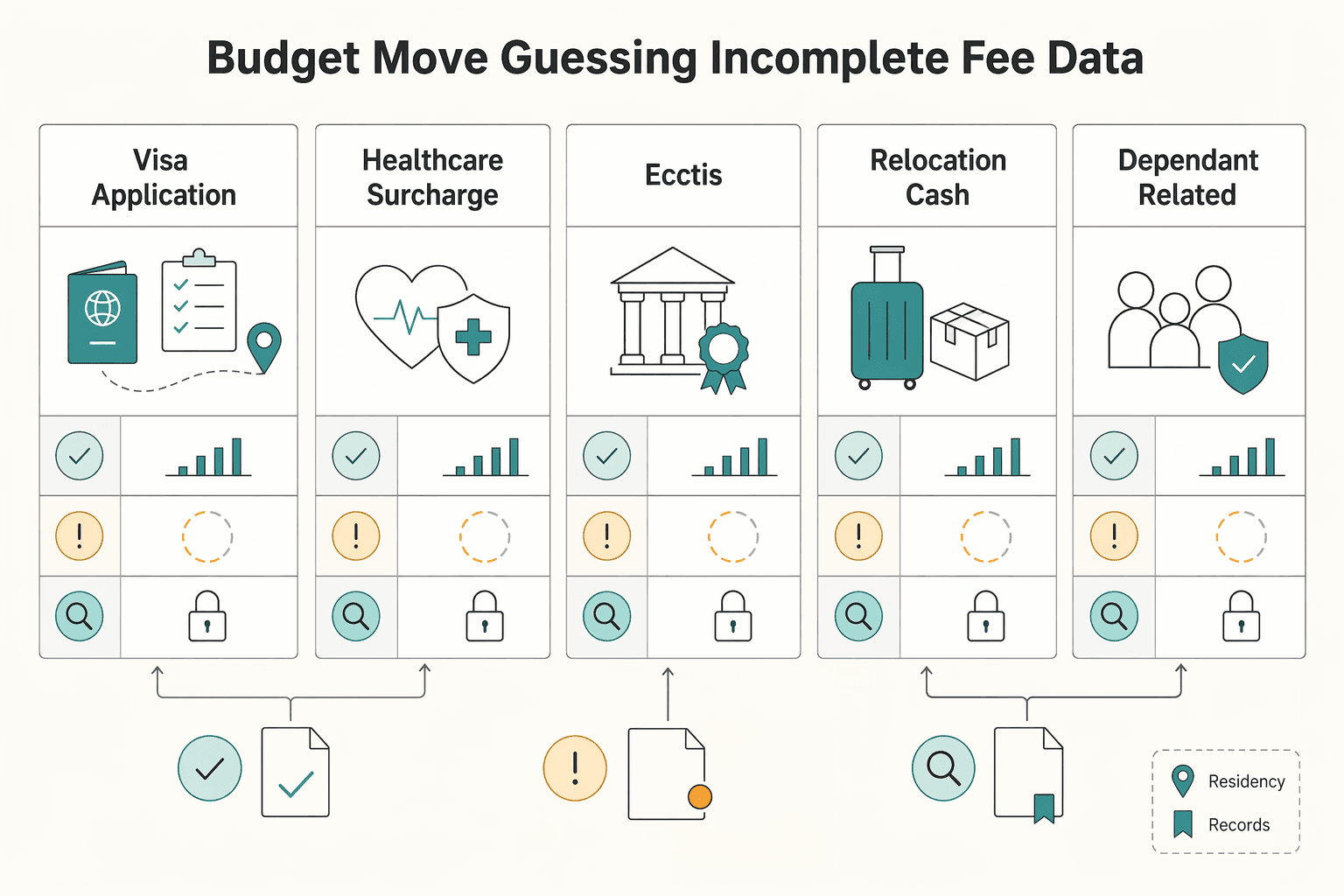

Budget the Move Without Guessing on Incomplete Fee Data#

Budget with three buckets: Known, Unknown, and Verify now. If a number is not freshly verified, do not use it for non-refundable decisions.

| Cost category | Known | Unknown | Verify now |

|---|---|---|---|

| Visa application | Confirm with the relevant authority | Exact amount for your case and filing location | Current route details on GOV.UK on action day |

| Healthcare surcharge | Confirm with the relevant authority | Exact total for you and any dependants | Latest surcharge guidance before payment |

| Ecctis | Confirm with the relevant authority | Exact fee and add-on costs | Current pricing and options before purchase |

| Relocation cash buffer | Planning line for date movement and rebooking risk | Appropriate buffer size for your situation | Your runway target, then recheck before committing dates |

| Dependant-related costs | Planning line for additional applicants | Total cost until each person is confirmed | Current dependant guidance and sequencing before submission |

| Post-arrival tax admin | First-time online filers must register before using filing services; a National Insurance number is needed to register; existing accounts may need reactivation; and recordkeeping is required | Whether and when those steps apply depends on your income and filing circumstances | Current HMRC guidance before filing, payment, and notification deadlines |

For each line, keep a log with amount, last verified date, and proof record. A blank verification date means the number is not decision-ready.

Separate planning confidence from spending confidence. You can keep planning with unknown figures, but you should not lock in non-refundable costs until the critical unknowns are verified and documented.

Keep HMRC dates on a separate track from visa timing. 5 October 2025 and 31 January are tax anchors, not visa fee deadlines.

When you review your budget, test two outcomes: expected timing and delayed timing. If delayed timing breaks your cash position, pause and adjust before you submit. That is a planning decision, not a policy decision.

Plan Dependants Early to Avoid Splitting the Family Timeline#

Plan family sequencing early, but treat dependant rules as unconfirmed in this section until you verify them on live GOV.UK visa pages for your case.

For each person, track two lines:

Legal definition to verifyEvidence on hand versus missing

Think through two common sequencing options before you book anything:

| Sequencing option | Practical effect | Verification before booking |

|---|---|---|

Main applicant and dependants move on one timeline (if allowed) | This may keep one planning window for travel, housing, and setup, but it creates more documentation pressure at once. | Verify on GOV.UK that this sequence is valid and that each person's records are complete. |

Main applicant moves first, dependants follow (if allowed) | One person can establish logistics first, but the family timeline may split. | Verify on GOV.UK that this sequence is valid before booking dates. |

Keep one sheet per person with passport name, date of birth, relationship label used across forms, issue date, expiry date, and last-verified date. Any conflict should pause submission until corrected.

Treat family documentation like one shared package, even if applications are not submitted together. A mismatch in one person's records may force edits across multiple forms and timelines.

If you are targeting London or Scotland, test practical constraints early, but verify details directly with local providers. For city-level setup checks, use London, UK: A Guide for Expats and Remote Workers:

- Confirm school admissions timing directly with schools or local authorities.

- Confirm lease timing directly with landlords or agents.

- Confirm childcare availability directly with providers.

If location is still open, compare setup realities before you choose.

Keep tax administration in the same project plan but separate from visa assumptions. If sole-trader income may exceed £1,000 in a tax year, plan Self Assessment from first income: you need a National Insurance number to register, first-time filers must register before filing online, filing without reactivating an existing account may delay processing, keep records such as bank statements or receipts, tell HMRC by 5 October for the previous tax year, and pay your tax bill by 31 January.

Avoid the Mistakes That Most Often Delay HPI Moves#

Delays often start with submitting before key checks are complete. Keep visa assumptions clearly marked for same-day GOV.UK verification.

Common red flags:

- Filing a Self Assessment return for the first time without registering first.

- Filing without reactivating an existing Self Assessment account when reactivation is needed.

- Treating HMRC tax guidance as if it confirms HPI visa rules.

- Not keeping records such as bank statements or receipts ready before filing.

Another recurring issue is mixing timelines. HMRC tax dates are specific to Self Assessment and should stay in your tax plan.

Before you pay, run one pre-submit audit:

- If you are filing Self Assessment for the first time, confirm registration is complete before using the online filing service.

- If you had a Self Assessment account before, check whether it needs reactivation before filing.

- If sole-trader income may exceed

£1,000in a tax year, keep tax steps separate from your visa checklist. - Keep records such as bank statements or receipts so you can complete returns correctly.

- Keep HMRC dates such as

5 October 2025and31 Januaryin your tax timeline only.

If any item fails, pause and fix it before submission. A short delay now is usually lower risk than correcting preventable errors later.

Before final submit, do one last pass with fresh eyes or a second reviewer. The objective is simple: catch contradictions and separate confirmed tax steps from unverified visa assumptions.

Decide Your Exit Path Before Your HPI Clock Starts#

Choose your likely next route early, then review it at fixed checkpoints. That prevents last-minute route changes and keeps evidence-building aligned with your likely path. Exact visa-route eligibility and timing are not established here, so treat them as items to verify in current official guidance.

| Direction after arrival | Evidence to build early | Verification gate |

|---|---|---|

| Employer-led route | Dated role-search notes, job descriptions, contract drafts, and later employment records aligned with your application history | Confirm current route criteria on GOV.UK and log the date checked |

| Independent income track while assessing future options | Invoices, bank statements, receipts, and a clear income log from first payment | If income may exceed £1,000 in a tax year, prepare HMRC registration steps |

| Hold position while deciding | Passport and identity consistency across records, plus one dated document folder | Revalidate official guidance before committing |

Use three checkpoints:

- Early checkpoint: pick one primary path and one backup, then log the pages you relied on.

- Mid checkpoint: test whether your document trail still supports the path you picked.

- Final checkpoint: make the route call only after a fresh rules check and full consistency review.

Keep tax compliance on a separate track so filing issues do not consume time needed for other actions. First-time online filers must register before using filing services, and existing accounts may need reactivation to avoid delays. If you lived abroad as a non-resident, do not assume the standard online filing service applies.

Use dates correctly. HMRC anchors such as the 5 October notification deadline for the relevant tax year, 31 January for payment, the tax-year window 6 April to 5 April, and filing availability on or after 6 April are tax milestones, not immigration milestones.

Business structure choices also affect risk and documentation. GOV.UK set-up-business guidance notes that sole traders are personally responsible for business debts, while limited company owners are responsible up to their investment. Once relocation timing is clearer, connect this plan with Understanding the UK's Statutory Residence Test (SRT).

Use one test at each checkpoint: can you support your chosen path with current documents and current rule checks, or are you still relying on assumptions that are not yet verified? If it is the second case, keep building evidence before you commit.

Set Up Your First 90 Days in the UK With Compliance in Mind#

Use the first 90 days to create a dated record trail you can rely on later. Keep tax administration tasks on a separate timeline so key deadlines and follow-ups stay visible.

| Task | What to keep or review |

|---|---|

| GOV.UK pages | Keep a last checked date for each GOV.UK page you rely on. |

| Identity sheet | Maintain one identity sheet with exact name spelling, date format, and current address. |

| Self Assessment readiness | Track National Insurance number readiness and any Self Assessment registration or reactivation tasks. |

| Monthly records | Keep monthly folders for statements, receipts, invoices, and payout records. |

| Income trigger review | If income may exceed £1,000 in a tax year, review sole-trader registration criteria promptly. |

In week one, standardize identity details across your records and create a simple folder structure for dated documents. Practical setup timing can vary, so keep important dates logged as you go.

For work readiness, decide early whether Self Assessment may apply. If you are filing online for the first time, register before using the service. A National Insurance number is needed for registration, and older accounts may need reactivation before filing.

If you work with clients, keep payment records clean from the first invoice. Save invoices, bank statements, and receipts in monthly folders, and keep a simple payout trail linking invoice date, amount, currency, and receiving account entry.

Use this lightweight checklist during the first 90 days:

- Keep a

last checkeddate for each GOV.UK page you rely on. - Maintain one identity sheet with exact name spelling, date format, and current address.

- Track National Insurance number readiness and any Self Assessment registration or reactivation tasks.

- Keep monthly folders for statements, receipts, invoices, and payout records.

- If income may exceed

£1,000in a tax year, review sole-trader registration criteria promptly.

Use deadlines as planning anchors only. In the cited guidance, 5 October 2025 is a notification date for the referenced prior tax year, filing can start on or after 6 April after year end, and payment is due by 31 January.

Choose business structure deliberately in this period. GOV.UK notes that sole trader status is simpler to set up and keep records for, while personal responsibility for business debts remains with the sole trader. Limited company owners are responsible for business debts up to their financial investment.

Keep a recurring review habit during this period. At each review, update what changed, what is still pending, and what needs a fresh official check. That simple rhythm protects you from stale assumptions and keeps your records usable if plans shift.

Final Decision Checklist Before You Apply#

Use this as a strict go or no-go check. Submit only when live policy checks are complete and your records are internally consistent.

| Final check | What to confirm |

|---|---|

| Official guidance is live-verified | Confirm current route wording on GOV.UK, then log the date checked. |

| Identity details are consistent | Confirm names and dates match across your records and account details. |

| Self Assessment access is ready if relevant | First-time online filers must register first, and existing accounts may need reactivation. |

| Tax triggers are understood | If sole-trader income is more than £1,000 in a tax year, registration may be required and late registration may lead to penalties. |

| Required tax records are in place | Keep bank statements or receipts organized, and keep your National Insurance number ready for registration. |

| Key tax dates are tracked | Keep 5 October and 31 January in a dedicated tax timeline. |

Route-specific criteria, document sufficiency, filing-path mechanics, and current fee amounts are unconfirmed. Treat each of those as a same-day GOV.UK check and record when you verified it.

Run the same checks in order:

- Official guidance is live-verified: confirm current route wording on GOV.UK, then log the date checked.

- Identity details are consistent: confirm names and dates match across your records and account details.

- Self Assessment access is ready if relevant: first-time online filers must register first, and existing accounts may need reactivation.

- Tax triggers are understood: if sole-trader income is more than

£1,000in a tax year, registration may be required and late registration may lead to penalties. - Required tax records are in place: keep bank statements or receipts organized, and keep your National Insurance number ready for registration.

- Key tax dates are tracked: keep

5 Octoberand31 Januaryin a dedicated tax timeline.

Treat every line as pass or fail. If a line fails, fix it before you submit. Do not convert partial confidence into paid action.

Final rule before submission: every checklist item needs an owner, a document, and a verification date.

As you finalize your move plan, start tracking day-count risk early with the tax residency tracker. If your first destination city is not final yet, keep one parallel setup track using London, UK: A Guide for Expats and Remote Workers.

Frequently Asked Questions

Can I get a UK HPI visa without a job offer?

Job-offer requirements are unverified. Check the live GOV.UK route criteria before you act on this answer.

How long does the HPI visa last if I have a Doctor of Philosophy (PhD)?

Visa length, including any PhD-specific duration, is unconfirmed. Confirm the current policy page before setting your timeline.

Can I extend the High Potential Individual (HPI) visa?

Extension rules for the HPI route are unconfirmed. Verify current options on GOV.UK before relying on any deadline.

Do I need Ecctis for every HPI application?

Ecctis requirements are unconfirmed. Check current GOV.UK application guidance for your case.

How long do decisions usually take inside and outside the UK?

Decision timelines are unconfirmed. Check live GOV.UK processing guidance and record the date you verified it.

Can my partner and children apply as dependants?

Dependant eligibility and requirements are unconfirmed. Verify current GOV.UK guidance before submitting.

How should I verify current fees and savings requirements safely on GOV.UK?

Use a same-day check and treat every requirement as live until you confirm it. Review current HPI guidance, then verify fees and any financial requirements on GOV.UK for your route, and record the date checked in your file. Keep tax and visa tracks separate: dates like 5 October 2025 and 31 January are HMRC Self Assessment milestones, not visa fee deadlines.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- gov.uk/register-for-self-assessmentexternal

- gov.uk/set-up-businessexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

London, UK: A Guide for Expats and Remote Workers

Get two calls right early and the rest of the move gets easier: how you'll be in the UK, and where you'll work when conditions are less than ideal. Make those decisions before you lock dates or prepay a long stay. If you book first and sort the basics later, admin and work reliability usually collide in your first week.

Understanding the UK's Statutory Residence Test (SRT)

Treat SRT like ops, not folklore. You want a repeatable workflow you can run monthly so your tax-year answer is boring, documented, and easy to defend.

The 2026 Global Digital Nomad Visa Index for 50+ Countries

Start with legal fit, not lifestyle filters. The practical order is simple: choose a route you can actually document, then decide where you want to live. That single change cuts a lot of wasted comparison work and stops you from falling in love with places that were never a real filing option.