Quick Answer

Citizenship based taxation means a country can tax its citizens on worldwide income regardless of where they live, while residency-based taxation taxes you based on local tax residency rules. The U.S. is the main example people run into, and the key operational reality is that CBT and RBT can stack-creating two filing and reporting tracks that require consistent documentation, clean income categories, and careful use of tools like FEIE or the Foreign Tax Credit.

You're not choosing between "citizenship" and "residency"-you're managing two tax systems at once#

You're not choosing one tax identity and discarding the other. In cross-border life, you're usually operating two systems at the same time: a status-driven filing layer and a place-driven residency layer. Stop asking which one wins and start running one operating flow that covers exposure, obligations, paperwork, and proof.

This matters because stress rarely starts with one giant bill. It starts with mismatched assumptions, missing records, and a story you cannot defend quickly. You can pay local tax where you live, keep clean books, and still have a second filing track tied to citizenship or similar status. Most problems show up when someone treats one layer as optional, then has to backfill months of facts under deadline pressure.

Use this framing at the start of every planning cycle, especially before you choose FEIE or FTC. Clear facts make forms simpler. Fuzzy facts make every downstream decision more expensive.

| What you're managing | Trigger signal | What it changes for you | What to save (audit-ready) |

|---|---|---|---|

| Status-based exposure | Citizenship, immigration status, or similar legal ties | Possible second filing/reporting lane even while living abroad | Status documents, filing history, account list, income records |

| Local residency exposure | Residency tests and local ties where you live | Where local tax may apply and what local filings are expected | Lease/address proof, tax returns, payment receipts, day-count log |

A practical default looks like this:

- Put both exposures on one page so you can see the full surface area at once.

- Mark each filing item as must file, might file, or needs confirmation. Do not guess.

- Build your evidence pack before deadlines, not after.

- Flag hidden costs early, especially state issues and self-employment compliance.

The goal is boring, defensible execution. Run both layers like an operator.

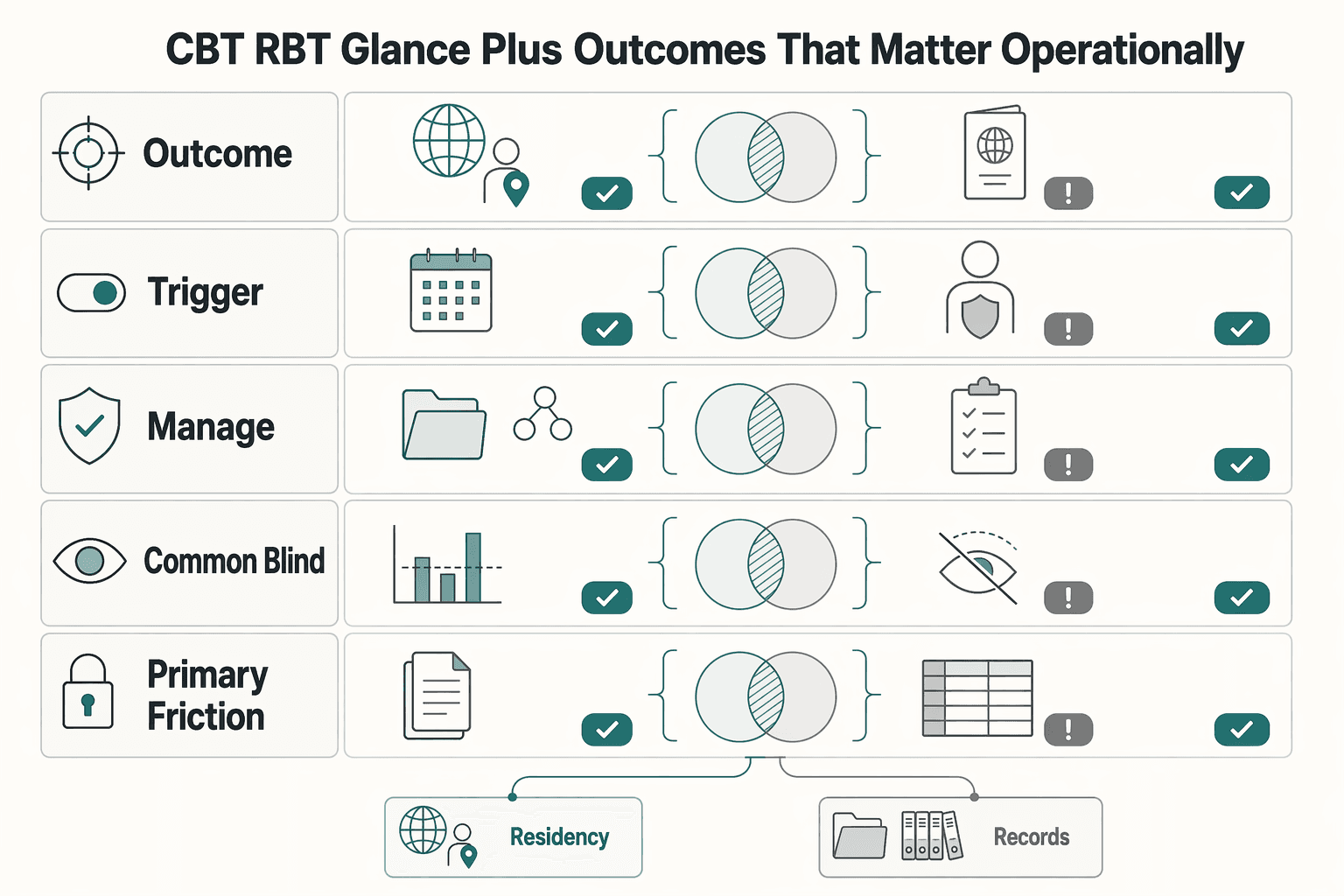

CBT vs RBT at a glance (plus the 3 outcomes that matter operationally)#

CBT and RBT are not two opinions about tax policy. They are two rule systems that can overlap in your real life. Your job is to identify where they stack, then control that stack with documentation and a clear filing story.

| Outcome | Posture | Operational meaning |

|---|---|---|

| Outcome 1 | One-system posture | Status-based filing remains, but local residency does not trigger in a second country |

| Outcome 2 | Two-system posture | Status-based filing continues and local residency also applies; you need one consistent story across two filings |

| Outcome 3 | Multi-system posture | More than one jurisdiction can claim residency, or your facts look like dual residency; this is the highest-friction case and deserves early professional review |

| Criteria | Citizenship-based taxation (CBT) | Residency-based taxation (RBT) |

|---|---|---|

| Trigger | Citizenship or comparable status ties | Local residency tests based on days and ties |

| What you manage | Ongoing filing/reporting track with a home tax authority | Local filing/payment obligations where you are treated as resident |

| Common blind spot | Assuming living abroad removes filing duties | Assuming low days automatically removes residency risk |

| Primary friction | Extra reporting, category tracking, record discipline | Local rules, language, deadlines, advisor dependency |

| Failure pattern | "I moved abroad, so I stop filing" | "I am resident nowhere, so nobody can tax me" |

From an execution standpoint, you are not trying to pick a side. You are trying to sort your year into one of three operational outcomes before you optimize anything:

- Outcome 1 (one-system posture): status-based filing remains, but local residency does not trigger in a second country.

- Outcome 2 (two-system posture): status-based filing continues and local residency also applies. You need one consistent story across two filings.

- Outcome 3 (multi-system posture): more than one jurisdiction can claim residency, or your facts look like dual residency. This is the highest-friction case and deserves early professional review.

One more operator point that saves real money: low tax does not mean low compliance. Many costly problems are reporting problems, not rate problems.

The Two-Layer Model that stops bad decisions#

The Two-Layer Model is deliberately simple. It forces you to separate questions that people routinely blend together. Layer 1 asks whether legal status creates a filing lane. Layer 2 asks where lived facts create residency claims. You make safer decisions only when both layers are visible at once.

| Layer | What triggers it (in practice) | What you decide | What you track to keep decisions safe |

|---|---|---|---|

| Layer 1: Status layer | Legal status with a country, regardless of current address | Whether status creates filing/reporting obligations | Status documents, filing history, account inventory, income categories |

| Layer 2: Place layer | Where you actually live and work, regardless of intent | Where residency claims may arise and when | Day-count log, home-base evidence, work-location trail, local deadlines |

Why this model prevents expensive mistakes#

Most expensive cleanups come from one sentence: "I moved, so I am done." That sentence hides two different systems and leaves gaps in both. The model prevents this by making the overlap explicit from day one.

Once you separate the layers, bad habits get easier to spot and fix. You stop skipping filings because projected tax looks low. You stop treating day-count folklore as legal certainty. You stop waiting until year-end to reconstruct where you were and what you earned. You also get better results from advisors because you show up with facts organized by layer instead of a pile of screenshots and memory.

This model does not remove complexity. It contains complexity so you can execute without improvising under deadline pressure.

Your safe-default system#

Run the same routine each quarter so you're not re-solving the same problem every tax season.

Start by writing down Layer 1 and Layer 2 in plain language. Then keep one source of truth current enough to defend your position quickly.

Here is the system, phrased as actions you can actually take:

- Define Layer 1 in writing. Identify status-based filing exposure and unresolved questions.

- Define Layer 2 in writing. Record where you lived, worked, and kept ties.

- Choose relief tools after classification. Use FEIE or FTC based on facts, not identity.

- Maintain one source of truth. Keep travel logs, category-level income records, and proof of taxes paid in a consistent structure.

- Escalate interpretation questions early. Do not DIY when residency or entity treatment is unclear.

Treat this as risk control, not a one-time setup.

The 10-minute decision flow (your safe-default playbook for 2026 planning)#

Fast decisions come from a prewritten flow, not from last-minute research. The sequence below is short enough to run monthly and strong enough to catch most avoidable mistakes. The goal is not to predict every edge case. The goal is to keep your base position clean so edge cases become obvious early.

| Step | Focus | Deliverable |

|---|---|---|

| Step 1 | Confirm status exposure (no guessing) | A one-line status conclusion plus supporting documents |

| Step 2 | Map physical presence like an operator | A current day-count log and a reconciled calendar |

| Step 3 | Decide where residency claims might come from | A residency-risk map with clear yes, maybe, and no jurisdictions |

| Step 4 | Classify income before choosing tools | An income-category map plus a draft tool direction supported by records |

| Step 5 | Output a minimum viable compliance stack | A dated minimum viable compliance stack you can hand to an advisor in one call |

Step 1 - Confirm status exposure (no guessing)#

Start with a binary question: do you have status that can create a continuing U.S. filing relationship? If yes, treat that as an active input for the year. If no, document why. If uncertain, mark it as needs confirmation and keep moving through the flow.

Do not turn this step into a debate about identity. It is scoping. You are defining whether a status-based filing lane exists so downstream choices stay grounded. Write the result at the top of your working sheet and date it. If facts change mid-year, update the sheet and keep the prior version so your story stays consistent.

Deliverable for Step 1: a one-line status conclusion plus supporting documents.

Step 2 - Map physical presence like an operator#

Build a day-count calendar using entry and exit dates from records you can produce later. Keep it mechanical. For the Physical Presence Test, qualification is based on time abroad, and the threshold is generally 330 full days during any period of 12 consecutive months.

Two execution rules matter here. First, track continuously, not just at year-end. Second, reconcile your log with independent records such as tickets and calendar events. This prevents memory errors from turning into filing errors.

Do not treat day counting as a magic switch. It is one component of eligibility analysis and one component of your broader residency story. Its value is evidentiary. It helps you prove what happened, when it happened, and how your filing position was chosen.

Deliverable for Step 2: a current day-count log and a reconciled calendar.

Step 3 - Decide where residency claims might come from#

Now map residency risk based on lived facts, not intentions. List the places where you had meaningful ties: housing, work pattern, family presence, permits, and recurring activity. Then ask a practical question: which jurisdictions could plausibly claim you as resident on these facts?

If one place is plausible, document it and proceed. If multiple places are plausible, flag this for professional review before you lock in filings. Do not guess your way through dual-claim situations.

This step also prevents story drift. If your lease, visa, bank activity, and client footprint point to one place while your filing story points to another, fix the mismatch now. Consistency across records is what keeps your position durable.

Deliverable for Step 3: a residency-risk map with clear yes, maybe, and no jurisdictions.

Step 4 - Classify income before choosing tools#

Tool choice comes after income classification. Separate earned service income from other categories, then evaluate FEIE and FTC against those categories. This sequence matters because FTC reporting is category-based and generally requires a separate Form 1116 for each category of income.

FEIE is an exclusion for eligible foreign earned income that you claim through a filed return. That means filing remains part of the process even when the exclusion reduces taxable amounts. FTC is a credit mechanism tied to foreign taxes paid and categorized reporting. It is not a one-click offset for everything.

If your bookkeeping does not reflect categories, you are not ready to decide. Fix the bookkeeping first. A clean classification map now saves hours of amendment risk later and makes advisor help cheaper because your inputs are already structured.

Deliverable for Step 4: an income-category map plus a draft tool direction supported by records.

Step 5 - Output a minimum viable compliance stack#

Finish by producing a one-page compliance stack. Keep it short and operational. Include likely filings, timing, evidence requirements, and unresolved questions. The objective is execution clarity, not legal prose.

A useful stack covers:

- Core return posture and expected forms.

- Additional international reporting items that may apply.

- Evidence list by claim type, such as days, income categories, and foreign tax payments.

- Review triggers that force advisor involvement.

When this page exists, the rest of your process becomes routine. Without it, every deadline becomes a fresh interpretation exercise.

Deliverable for Step 5: a dated minimum viable compliance stack you can hand to an advisor in one call.

FEIE vs FTC vs "surprise taxes": what you file, what you owe, and what blindsides freelancers#

Most freelancer confusion starts with solving the wrong problem first. People ask which tool is better, but skip the prior question: what must be filed regardless of tool choice? The clean sequence is obligations first, liability modeling second, optimization third.

Separate "filing obligations" from "tax due"#

Keep these on separate tracks.

Filing obligations describe what must be reported and documented. Tax due describes the computed amount after exclusions, credits, and category rules are applied.

This distinction is where many surprises begin. If you use FEIE, filing still exists because the exclusion is claimed on a filed return that reports the underlying income. If you use FTC, category-specific work still exists because credits are claimed within structured reporting lanes.

This is why "my bill should be low" is not a strategy. The compliance surface can stay large even when liability is modest.

FEIE vs FTC (what they actually do)#

| Tool | Best fit (typical) | What it depends on | What it changes | What it does not automatically solve |

|---|---|---|---|---|

| Foreign Earned Income Exclusion (FEIE) | Foreign earned income with qualifying facts | Meeting a qualifying test such as the Physical Presence Test | Excludes eligible foreign earned income when claimed properly | Does not remove filing duties; income is still reported on a return |

| Foreign Tax Credit (FTC) | Foreign taxes paid with category-aware reporting | Form 1116 process by income category, generally separate per category | Claims credit amounts tied to foreign taxes paid | Does not remove category complexity or record requirements |

Both tools can reduce double-tax pressure in the right fact pattern. Neither tool replaces disciplined records. Choose based on eligibility, income type, and how strong your documentation is.

The operator checklist (5 minutes)#

Before you lock your strategy, run a quick check that focuses on execution, not theory:

- Eligibility proof exists. Your day-count and location records are complete.

- Income categories are clean. Service income and other categories are not blended.

- Foreign tax proof exists where credits are claimed.

- Filing obligations are listed separately from expected tax due.

- Unclear items are flagged for review, not buried inside assumptions.

The point is to choose tools from facts, then keep support files ready for a fast explanation.

The reporting stack that feels like taxation (and the compliance surface you should take seriously)#

Cross-border taxes feel heavy partly because reporting has its own workload. Even when computed tax is manageable, documentation can still be extensive. If you treat paperwork as an afterthought, you create rework and avoidable risk.

Compliance isn't the same thing as liability#

Low liability is not a waiver for reporting. In practical terms, the system still expects clear returns, category logic, and supportable records. When FEIE is part of your position, the return still carries the reporting burden. When FTC is part of your position, category-level documentation still drives correctness.

Treat compliance like production work. Inputs must be complete, the process must be repeatable, and outputs must be explainable. Do this and deadline panic drops because the work is distributed through the year instead of compressed into a scramble.

The reporting stack, in one table#

| Workstream | What you're doing | Common failure point | Safe default |

|---|---|---|---|

| Eligibility proof | Supporting the tests and positions you claim | Trying to reconstruct time and location from memory | Maintain a live travel log and reconcile it monthly |

| Computation | Calculating outcomes by category | Blending categories and losing traceability | Keep category-level ledgers and assumptions |

| Documentation | Producing forms and retaining support files | Missing key records when questions appear | Use one organized evidence register for the full year |

This is intentionally plain. Plain systems survive stress better than clever systems.

Two specifics you can anchor your system to#

First anchor: time-based positions need time-based evidence. If your day count is weak, your position is weak. Keep the log current and tie it to corroborating records.

Second anchor: FTC category discipline is not optional. If you earn through multiple income types, your bookkeeping must mirror those lanes. Clean category data is what keeps Form 1116 work defensible and efficient.

Anchor to these two points and most reporting friction becomes manageable instead of chaotic.

Where double taxation actually happens (it's category-specific, not "everything")#

Double-tax pressure rarely shows up as one giant universal overlap. It usually shows up in categories where systems classify timing, income type, or entity treatment differently. That is why category discipline matters more than slogans about low-tax locations.

When you review your year, use a mismatch lens. Ask where classification might diverge, where timing might diverge, and where your structure might be treated differently across jurisdictions. Then document those points before return prep begins so you are not discovering them inside a form workflow.

| Where mismatches show up | What typically drives the mismatch | Safe default move |

|---|---|---|

| Capital gains | Different recognition timing and definitions | Keep purchase/sale records and year cutoffs precise |

| Retirement or pension flows | Different account treatment and reporting rules | Flag account treatment questions before filing |

| Entity classification | Different views of foreign entities across systems | Treat foreign entities as compliance multipliers from day one |

| Investment wrappers | Product classifications that do not map cleanly across borders | Simplify where possible before changing jurisdictions |

Keep the order straight: classify first, compute second, optimize last. Reverse it and you invite cleanup.

The myths, hidden costs, and failure modes that blow up "simple nomad tax plans"#

Simple narratives are attractive because they lower anxiety. They also hide the details that drive real outcomes. The plans that fail most often optimize for a slogan and underinvest in evidence, categorization, and filing discipline.

| Issue | Main risk | Safe move |

|---|---|---|

| One day-count rule makes you safe | A day count can support specific tests, but it does not shut down every tax question in every jurisdiction | Maintain a coherent home-base story backed by records, then file conservatively until uncertain items are resolved |

| Resident nowhere planning | Visas, leases, banking, and repeated work patterns create facts that authorities can evaluate | Use consistency: stable facts, stable filings, and early escalation when claims overlap |

| State tax inertia | State exposure can persist longer than expected when domicile-related ties remain in place | Assume the question is open until you have a clear position supported by facts |

| Self-employment compliance | If it is ignored, you can produce mismatched estimates, weak records, and year-end surprises | Classify income correctly, map obligations early, and confirm interpretation points before you optimize cash flow decisions |

Myth: "One day-count rule makes you safe."#

A day count can support specific tests, but it does not shut down every tax question in every jurisdiction. Status-based filing may continue while local residency analysis runs on separate criteria. Treat days as data, not as an all-purpose shield.

The safe move is to maintain a coherent home-base story backed by records, then file conservatively until uncertain items are resolved.

Failure mode: "Resident nowhere" planning#

In theory, being resident nowhere sounds efficient. In practice, your footprint still exists. Visas, leases, banking, and repeated work patterns create facts that authorities can evaluate.

When multiple jurisdictions can plausibly claim you, ambiguity becomes the real cost. You lose time, spend more on cleanup, and weaken your position in every review. The remedy is consistency: stable facts, stable filings, and early escalation when claims overlap.

Hidden cost: state tax inertia#

State exposure can persist longer than expected when domicile-related ties remain in place. Travel alone does not always resolve that exposure. If meaningful ties remain, assume the question is open until you have a clear position supported by facts.

This is a common operator trap. People optimize international layers and ignore the domestic layer that still has momentum.

Hidden cost: self-employment compliance#

Self-employment compliance is its own workload and should be scoped early. If you ignore it, you can end up with mismatched estimates, weak records, and year-end surprises that are expensive to unwind.

The better approach is straightforward: classify income correctly, map obligations early, and confirm interpretation points before you optimize cash flow decisions.

Plans fail when they chase cleverness. Plans hold when they prioritize proof.

Your audit-ready evidence pack (plus a quarterly routine that makes tax season boring)#

Your evidence pack is the difference between calm filing and frantic reconstruction. Build it once, maintain it lightly, and let it carry most of the operational load through the year.

The evidence pack (build once, update continuously)#

Keep this pack compact and specific. Each item should support a claim you are likely to make.

| Evidence item | What it supports | Safe default |

|---|---|---|

| Day-count log and travel calendar | Time-based positions and location narrative | Update weekly and reconcile monthly |

| Filed return and FEIE workpapers | Reported income and exclusion calculations | Save final outputs plus calculation inputs |

| FTC category folders | Credit claims by income category | Keep separate folders with assumptions and source records |

| Proof of foreign tax paid | Credit support and reconciliation logic | Store official statements and payment evidence with notes |

If a document does not support a claim, do not clutter the pack. Clarity beats volume.

The quarterly "close" (repeatable, calm)#

Treat this like a simple operational close, not a tax project.

- Reconcile travel logs against tickets and calendar records.

- Export statements while access is easy and file them in one structure.

- Refresh income-category mapping and note any classification changes.

- Snapshot year-to-date figures used in your filing model.

- Write down unresolved questions and assign a decision date.

Quarterly closes convert tax season from emergency work into verification work.

A printable decision checklist#

Use this as a yes-or-no gate before return prep:

- I can produce a complete day-count record for the year.

- If I use FEIE, my return reporting and calculations are documented.

- If I use FTC, income is separated by category and foreign tax proof is filed.

- I can explain where I lived, where I worked, and how income was classified.

- I know which items require professional review before filing.

If any answer is no, fix that item before you optimize anything else.

When to talk to a pro (clear guardrails that prevent expensive mistakes)#

You do not need outside help for every routine step. You do need it when interpretation risk rises or choices become hard to reverse. Engage early, before a filing locks in a weak position and turns clarity into cleanup.

| Trigger | Why it's a pro moment | What to bring to the first call |

|---|---|---|

| Forming or using a foreign company | Classification and reporting complexity expands quickly | Ownership map, payment flows, and operating timeline |

| Holding complex cross-border assets | Category treatment can diverge across systems | Holdings list, statements, and transaction timeline |

| Potential residency claims in more than one country | Conflicting residency positions can drive disputes | Day-count log, lease history, and work-location record |

| Late or missing foreign-account filings | Remediation strategy should be deliberate | Account inventory and filing history by year |

| Considering renunciation | Decision path reaches beyond annual filing mechanics | Long-term residency plan and full financial snapshot |

Two reminders keep this grounded. Treaties can help, but outcomes depend on treaty text and your facts, and many treaties include a saving clause. Also, Form 8938 and FBAR are separate obligations. Filing Form 8938 does not replace FBAR, and FBAR is not filed with the IRS.

The point of hiring help is not outsourcing responsibility. It is buying clarity where ambiguity is expensive.

The safe default: accept the two-layer reality, then run a boring system that helps you stay compliant#

The safest long-term posture is simple: assume a stable status-based layer, assume a variable local residency layer, and run one documentation system that supports both without drama. This is how you stay compliant while keeping decision fatigue low.

In practice, that means you stop hunting for one rule that makes everything disappear. Instead, you maintain one operating rhythm that keeps facts current and filings coherent.

| Layer | What stays true | What you track | Common relief tools |

|---|---|---|---|

| U.S. status layer (CBT) | Status-based exposure can continue while abroad | Filing posture, income categories, reporting checklist | FEIE for eligible foreign earned income, FTC for eligible foreign tax credits |

| Local residency layer (RBT) | Local rules depend on where and how you live | Day counts, residency ties, local tax treatment | Country-specific credits or exclusions under local rules |

If you want a quarterly loop that holds up under stress, keep it tight:

- Confirm status exposure and unresolved questions.

- Update day counts and residency ties.

- Reclassify income categories if business activity changed.

- Refresh reporting checklist items, including FBAR and Form 8938 as separate obligations.

- Close your evidence pack so year-end is verification, not reconstruction.

Boring systems win. The goal is not perfect prediction. The goal is a position that is clear, supportable, and hard to break.

Frequently Asked Questions

What is citizenship-based taxation?

Citizenship-based taxation (CBT) means a country taxes citizens on worldwide income regardless of where they live or earn it. In practical expat tax conversations, the U.S. is the example people run into most.

Which countries have citizenship-based taxation?

Very few countries impose tax on citizens living outside their borders. In most discussions, the examples you'll see referenced include the United States and Eritrea, and sometimes Myanmar.

Do U.S. citizens living abroad have to file U.S. taxes?

Often, yes. The U.S. requires citizens and green card holders to file a U.S. tax return if their income exceeds IRS thresholds.

If I pay tax in another country, do I still owe U.S. tax?

Sometimes. Double-tax risk shows up when both the U.S. and your country of residence tax the same income. The Foreign Tax Credit (FTC) can mitigate that by giving credits for foreign taxes paid.

Can I avoid U.S. taxes by becoming a resident of another country?

Changing residency can change your local tax bill, but it doesn't switch off the U.S. approach of taxing citizens without regard to where they live. Think "two-layer stack," not "pick one country and you're done."

Does spending less than 183 days abroad avoid U.S. tax?

No. Don't build your plan on a day-count myth.

FEIE vs Foreign Tax Credit: which is better for freelancers and consultants?

FEIE and FTC solve different problems. Operator move: model both against your income categories and your foreign taxes paid. Then pick the option your facts support without creating reporting surprises.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Is a No-Tax Country Really Tax-Free for a US Citizen?

A no-tax destination can lower local income tax, but it does not end U.S. filing and reporting duties. U.S. citizens abroad are still taxed on worldwide income, and tools like the FEIE or Foreign Tax Credit are tied to filing a U.S. return.

Renouncing US Citizenship Starts With Form 8854 Readiness

Treat this as a tax-compliance decision first and a consular step second. For freelancers and consultants, the practical sequence is to assess covered expatriate risk, organize and verify your tax file, and only then decide whether to proceed.