Quick Answer

Freelancers can lower taxable income by claiming ordinary, necessary expenses they can document and tie to work, then reporting them on Schedule C. Start with categories that leave a clear paper trail - like software, professional fees, home office or rent, and vehicle or travel with logs - keeping receipts, payment proofs, and a one-sentence business purpose for each item.

Top 10 Tax Deductions for Freelancers (and who should actually use them)#

If you report business income on Schedule C (Form 1040) for work you do with continuity, regularity, and a real profit motive, these ten categories are the right place to start. The practical rule is simple: claim only what you can prove quickly with records created near the time you spent the money. When the paper trail is thin, the deduction is weak, even if the expense felt business related.

This guide is for people filing as self-employed on Schedule C. It is not a playbook for W-2 employee expense claims or a SALT strategy guide. The point is to help you choose the deductions that are easiest to defend, then decide whether higher-judgment items are worth the extra effort.

A useful first pass is to sort expenses into three buckets: clear fit with strong records, possible fit with incomplete records, and weak fit with no reliable business link. Start with the strongest group. Clean up the middle group while the details are still fresh. In most cases, skip the weakest group. That order keeps filing manageable and keeps marginal expenses from turning into big year-end arguments.

Here are the ten categories and the situations where they usually make sense:

- Home office deduction: Use this when you have a clearly defined area in your home used exclusively and regularly for business. It is strongest when the space boundaries and allocation method are easy to reproduce. Keep dated photos, a simple floor sketch, allocation notes, and supporting statements.

- Rent expense deduction: Use this when you pay for a separate office or coworking space for business use. This is often easier to explain because the paper trail is clean and recurring. Keep the signed lease, monthly invoices, and payment confirmations.

- Vehicle expense deduction: Use this when driving is directly tied to client work, site visits, or required business tasks. This category fails most often when logs are rebuilt long after the fact. Keep contemporaneous mileage or trip logs with date, destination, and business purpose, plus related receipts.

- Travel expense deduction: Use this for overnight trips connected to a client engagement or clear revenue activity. Strong claims include purpose notes that link each trip to work delivered. Keep itineraries, agendas, receipts, and proof of payment.

- Health insurance deduction for the self-employed: Use this when you pay your own premiums and can show complete policy and payment records. Keep policy documents, monthly statements, and matching payment proof.

- Retirement savings deduction: Use this when contributions are made to a suitable self-employed plan and tracked consistently. Keep custodian confirmations, contribution records, and year-end statements.

- Software expense deduction: Use this for subscriptions and licenses directly tied to delivering client work. These are easier to substantiate when invoices show the product, term, and account identity. Keep vendor invoices and payment records.

- Professional fees deduction: Use this for legal, accounting, and tax services that are ordinary and necessary for your trade. Keep engagement letters, detailed invoices, and proof of payment.

- Start-up costs deduction: Use this for eligible costs incurred before an active trade or business begins. This category depends on a clear timeline. Keep early invoices, legal filings, and a short record of your start date and first paid work.

- Employee wages deduction: Use this when you pay employees for work tied directly to business activity. Keep employment agreements, payroll records, time or duty records, and payment proofs.

The best filing plans are not built around every possible write-off. They are built around the categories that match how you actually work and come with clean proof. Start there, then decide whether anything more judgment-heavy is worth claiming. If cash flow is the next problem after deductions, pair this with your quarterly tax planning so your filing and payment rhythm stays aligned.

If you want a deeper explanation of year-round tax set-aside decisions, read How Much Should a Freelancer Save for Taxes? A Simple Formula.

Decide What Qualifies and Prove It (rules + evidence pack)#

Documentation decides this more often than tax theory does. A cost belongs on your return only when all three conditions are true: it is ordinary and necessary for your trade, it is tied to business activity, and you can show records that map to your Schedule C categories.

The mistake is treating this as a filing-season exercise. If you make the classification and recordkeeping decision at the time of purchase, year-end becomes a review process instead of a reconstruction project. That is the difference between a clean return and one built from memory, inbox searches, and guesswork.

Use this sequence to keep decisions consistent through the year:

- Write the business purpose when the expense happens. Use one sentence that names who the expense served, what work it enabled, and when it occurred. Many otherwise valid claims weaken because the purpose note gets added months later and turns vague.

- Run the ordinary-and-necessary test. Ask whether this cost is standard in your field and needed to deliver paid work. If the answer is yes, keep moving. If it is unclear, write down your reasoning now instead of assuming the context will be obvious later.

- Build the evidence pack for each transaction. Keep the invoice or contract, proof of payment, and a dated record tied to the ledger entry. Each item should still make sense if someone looks at it on its own.

- Document mixed-use allocations. For shared costs, save the method, not just the final percentage. An allocation note often makes the difference between a defensible deduction and a rough guess.

- Map categories to Schedule C early. Keep your book categories aligned with how you plan to report. This cuts down on year-end recoding and makes tie-out work much faster.

- Reconcile quarterly. Pull bank statements, mileage logs, travel records, and digital receipts, then compare totals to your books. Vendor filters usually catch missed software and professional fee entries.

- Add entity context once and stay consistent. If you are a sole proprietor, single-member LLC, partnership, or independent contractor, keep your ordinary-and-necessary rationale consistent in wording and categorization. Do not assume Schedule C treatment outside sole proprietor filings.

- Run a red-flag sample before filing. Pick ten transactions and check the purpose note, payment proof, date, and category label. Fix weak entries before return prep.

Keep each category folder in the same order: purpose note, invoice or contract, payment confirmation, and any allocation sheet. Label files with the date first so they sort themselves. When you standardize the folder order, you spend less time hunting for documents and more time checking whether the claim actually holds up.

The practical bar is straightforward. If you cannot explain the expense in one sentence and produce the evidence pack quickly, either skip it or rebuild the documentation before you file. The goal is not to claim everything you might be able to argue. The goal is to claim what you can defend without scrambling.

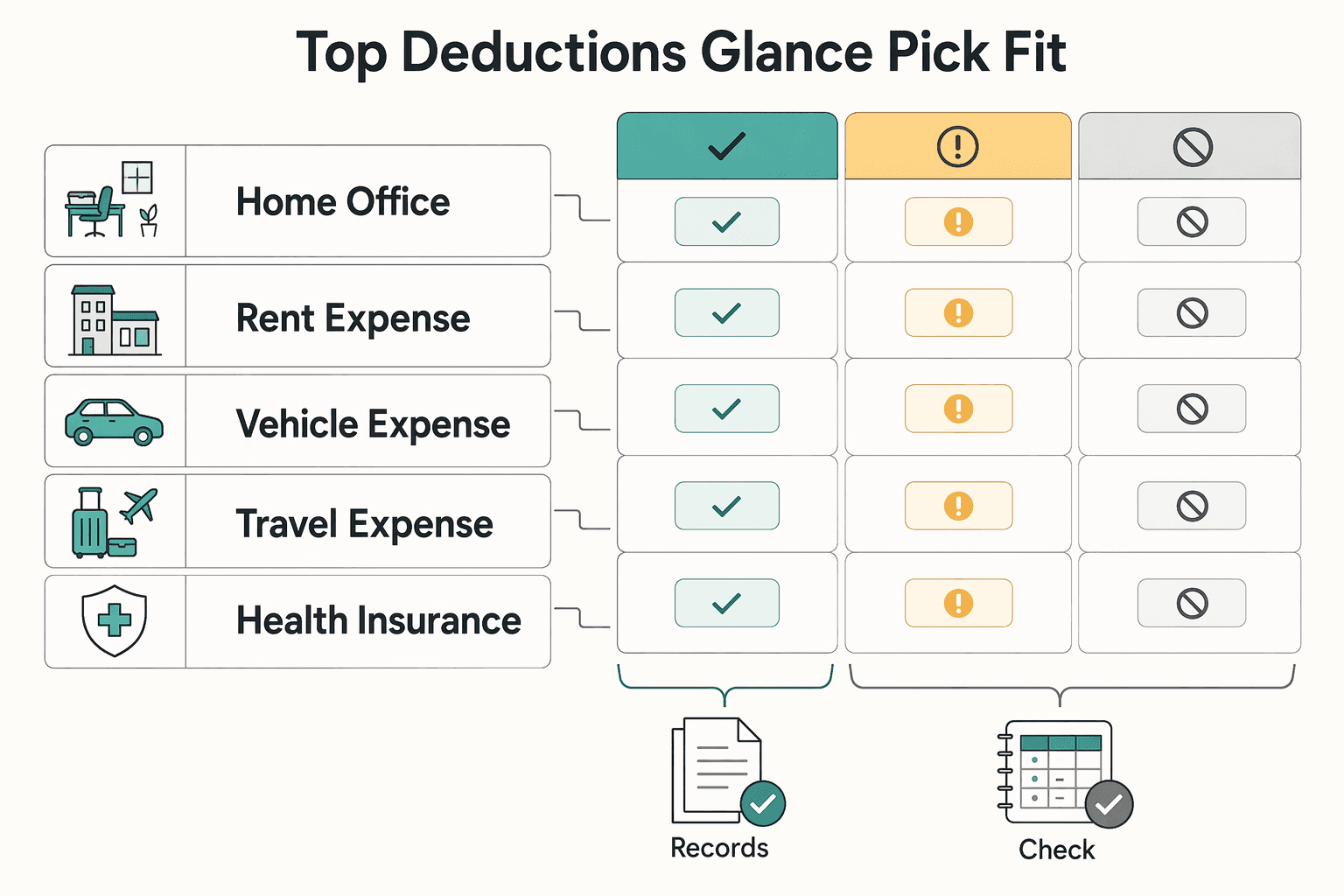

The Top 10 Deductions at a Glance (pick by fit, not hype)#

Use this table as a filter, not a shopping list. The strongest deduction is the one that matches how you actually operate and has a clean evidence trail. If you file on Schedule C (Form 1040), start with categories that tie directly to paid work and reconcile cleanly with your books.

| Item | Best for | Key pros | Key cons/risks | Evidence to keep |

|---|---|---|---|---|

| Home office deduction | Dedicated workspace at home | Clear link to business activity | Mixed-use space misclassification | Dated photos, floor notes, allocation record |

| Rent expense deduction | Separate office or coworking | Straightforward monthly trail | Higher fixed overhead | Lease, invoices, payment proof |

| Vehicle expense deduction | Client travel and site visits | Direct support for field work | Weak logs, personal-use overlap | Trip log, purpose notes, receipts |

| Travel expense deduction | Overnight business trips | Strong project tie when documented | Commuting confusion | Itinerary, agenda, receipts |

| Health insurance deduction for the self-employed | Paying your own premiums | Often material and documentable | Eligibility nuances | Policy, premium statements, payment proof |

| Retirement savings deduction | Taxable income reduction plus savings | Long-term benefit | Plan and timing tradeoffs | Contribution confirmations, statements |

| Software expense deduction | Service delivery tools | Easy recurring documentation | Subscription sprawl | Vendor invoices, payment records |

| Professional fees deduction | Legal, accounting, tax support | Compliance and execution support | Timing can be lumpy | Engagement letters, invoices, payment proof |

| Start-up costs deduction | Pre-launch business spending | Potential early relief | Classification mistakes near start date | Early invoices, legal filings, start timeline |

| Employee wages deduction | Paying staff tied to delivery | Capacity and continuity | Payroll complexity | Employment records, payroll proof, duty records |

A fast way to use the table is to mark each category one of three ways: ready now, needs cleanup, or skip for now. Ready now means you already have the documentation. Needs cleanup means the claim likely fits, but the records still need work this quarter. Skip for now means the expense depends too much on memory or has no clear business link.

Before filing, do one verification pass across every category you plan to claim: confirm the receipt or contract, proof of payment, and a one-line business purpose. Then sample entries to make sure dates, payees, and amounts match the ledger and the Schedule C category you plan to use. The usual misses are predictable: mixed-use space with no allocation support, weak vehicle logs, and totals that do not tie back to the books.

Two categories deserve an early decision because they shape your recordkeeping all year: where you work and how you track driving.

Home Office or Rent: Choose One You Can Defend#

Workspace claims get easier once you stop trying to support two competing stories. Use home office when part of your home is used exclusively and regularly for business. Use rent when your day-to-day work is anchored in a separate paid office or coworking space.

Most trouble starts when you try to keep both narratives alive without a real change in facts. Pick the category that reflects how the work actually happens, support it with records, and stay consistent through the year. If your setup truly changed, document when it changed and split the records by period.

For home office claims, choose one method and keep your documents aligned with that choice:

- Simplified method: per-square-foot calculation at $5 per square foot, up to 300 square feet, with simpler records and no Form 8829.

- Regular method: business-use percentage applied to eligible home costs such as mortgage interest, utilities, insurance, repairs, and depreciation, supported by records that show how you calculated the percentage.

The practical test is simple: could another reviewer recreate the deduction from your file without extra explanation? If yes, the claim is usually in decent shape. If not, fix the support before you file. That matters most for home office claims, where mixed use and rough square-footage guesses tend to cause problems.

Use this checkpoint before you close the year:

- Decision rule: home office fits when the business area is clearly bounded and used exclusively and regularly; rent fits when work is primarily done in a separate paid location.

- Evidence pack: for home office, keep dated photos, a floor sketch, allocation math, and supporting statements; for rent, keep the lease, invoices, and payment confirmations.

- Red flags: mixed-use rooms, rough square-footage estimates, and allocations that cannot be recreated from source records.

- Verification step: tie annual totals to your ledger and to the Schedule C label you intend to use.

If one option is fully documented and the other is not, take the one with the cleaner file and move on. You do not get extra credit for choosing the harder position. For a deeper walkthrough on documenting workspace claims, see The Complete Guide to the Home Office Deduction.

Once your workspace story is settled, the next category that demands discipline is driving.

Vehicle Expenses: Pick One Method and Stick to It#

This category lives or dies on the log, not the math. Pick one calculation approach, apply it consistently through the year, and document each business drive when it happens. Late reconstruction is the common failure mode, and it usually shows up in the same places: missing purposes, personal and business trips blended together, and totals that cannot be tied back to anything reliable.

What makes a vehicle claim defensible is consistency, not volume. A smaller number of well-documented trips is stronger than a large annual total built from memory. If you want this deduction to survive a second look, the record has to explain each drive in plain language.

A practical process looks like this:

- Set a method policy at the start of the year. Write a short note on your chosen approach and keep it with your tax records. Consistency matters more than trying to optimize every quarter.

- Log each business trip contemporaneously. Record the date, destination, and a one-line purpose tied to client work or delivery activity. If you cannot explain the trip quickly, treat it as nonbusiness until you can.

- Separate vehicle from other travel categories. Keep local driving records distinct from overnight travel records. Store itineraries and bookings in a different folder so the categories do not blur at filing time.

- Keep corroborating records. Save receipts and invoices that support your chosen approach, and export calendar or CRM entries monthly to back up trip timing and purpose.

- Run a quarterly tie-out. Compare logged business drives to the vehicle total in your ledger. Spot-check entries against calendar events and client work records, then fix gaps immediately.

- Watch the predictable breakdowns. Problems usually come from mixed personal and business use with no notes, logs written weeks later, or category drift where nonvehicle costs end up in vehicle totals.

- Align with Schedule C reporting. Use a book category label that mirrors the line you plan to use. Before filing, confirm the annual total can be traced to verified entries and stored records.

A simple month-end routine keeps this under control: export the log, look for missing purposes, match a sample to your calendar, and archive the files in one folder. Small monthly fixes are much easier than one large year-end repair.

If driving is central to how you serve clients, tight logging pays for itself. If business driving is occasional, keep the process light and only claim what you can support without guesswork.

Health Insurance and Retirement: Reduce Taxable Income, Keep Proof#

These two deductions are often useful, but they are only as strong as the payment trail behind them. Treat them as recordkeeping first, tax strategy second. You should be able to show what was paid, when it was paid, and where each number lands in your books.

For health insurance, keep the policy, premium statements, and matching bank or card records in one folder by tax year. Reconcile the ledger category quarterly so the running total matches what you actually paid. Small monthly gaps are easier to fix in real time than at year-end, especially if a plan changes or a payment posts in an unexpected way.

For retirement contributions, keep custodian statements, contribution confirmations, and a short log with the date, amount, and account. Make contributions on a cadence you can actually maintain, then reconcile your log to the custodian year-to-date total each quarter so bank debits, books, and statements stay aligned.

A one-page tracking sheet is usually enough for both categories:

- year-to-date premium total

- year-to-date retirement contribution total

- document locations

- date of last tie-out

- open gaps to resolve

A few simple habits prevent most cleanup work: use one clearly labeled payment account where possible, save monthly statements as they arrive, add short ledger memos that reference the policy or account, and request missing confirmations right away instead of reconstructing them later.

These records often drift when cash flow changes. If your income drops or timing shifts, update contribution plans and premium tracking in the same week. Keep a copy of the current-year Schedule C instructions in the same folder as these records, then reconcile again before year-end so the totals still make sense on paper.

After the recurring deductions are in order, the next judgment calls usually come down to timing and classification.

Start-Up Costs and Professional Fees: Get Relief Without Overreach#

Timing does most of the work here. If a cost happened before your active trade or business began, evaluate it as start-up. If it supports ongoing operations, treat it as a professional fee. The clean move is to make that classification explicit and keep a timeline another reviewer could follow without extra explanation.

Once the timeline is clear, most of the confusion fades. For start-up costs, keep a dated record that shows your adopted start date and first paid engagement. Each invoice in this category should fit that timeline. Treatment can vary, so do not rely on assumptions. Keep the reasoning attached to the record while the details are still easy to verify.

For professional fees, focus on ongoing legal, accounting, and tax services tied to an operating business. Save engagement letters, detailed invoices, and payment confirmations, then map the ledger category to the line you plan to use on Schedule C. This is a place where clear labeling in the books saves a lot of cleanup later.

Gray-area items near launch are where you can lose clarity. Handle them with a short memo that states the invoice date, business purpose, and why you classified the item as start-up or professional fees. File that memo next to the invoice so the logic is easy to revisit if you need it later.

These periodic checks usually catch the problem spots before filing:

- quarter-end review of the start-up folder to confirm each item predates active operations

- quarterly reconciliation of professional fees to bank or card statements

- sample review of vendor, amount, date, and purpose notes before filing

- one-page index showing where documents for each category are stored

Common errors tend to repeat:

- retainers paid before launch booked as current professional fees

- legal or tax bills paid through mixed personal and business accounts

- catch-all expense buckets that hide the details

The fixes are straightforward. Move pre-launch retainers back into start-up review and annotate the timeline. Shift legal and tax payments to one payment path and label them on the payment date. Split broad expense buckets into separate start-up and professional fee categories, then review them monthly so the distinction stays visible.

If launch timing changed during the year, update the timeline immediately and note the reason. A dated note is often enough to explain why similar invoices fall on different sides of the line.

Once you begin paying other people, the focus shifts from expense timing to worker classification.

Paying People: Employees vs. Contractors Without Guesswork#

Decide the role before the first payment goes out. That one choice determines tax handling, recordkeeping, and how cleanly your totals roll up at year-end. If classification stays fuzzy, everything after that gets harder.

For employees, the payer withholds and deposits income, Social Security, and Medicare taxes, and pays unemployment tax on wages. For independent contractors, the payer generally does not withhold or pay taxes on payments for services. Keep those payment streams separate from day one so the books do not turn into a cleanup project later.

This usually slips when your business is growing fast and payment execution starts moving faster than documentation. The fix is simple: require the role decision and the engagement documents before the first payment. That gives you a clean record from the start instead of a retroactive explanation months later.

Use this structure to keep the file clear:

- Employees: keep job descriptions, time or deliverable records, payroll summaries, and payment confirmations that match bank debits. Run a quarterly check on total wages and sample entries for date, amount, and business purpose.

- Independent contractors: keep signed contracts or statements of work, dated invoices, and payment confirmations tied to each engagement. Reconcile contractor totals quarterly and sample payments against scope and invoice dates.

- Classification memo: when hiring for the first time or changing a role, write a short memo on the service, degree of direction and control, and why the role is treated as employee or contractor. Store it with contracts and payment records.

- Schedule C tie-out: maintain separate ledger categories and a simple index of document locations for each payee. Before Q2 and Q4 close, compare category totals to statements and correct gaps immediately.

Most year-end problems come from a few avoidable habits: paying without contracts or scope notes, mixing personal and business accounts for labor payments, and using one broad labor category that hides the difference between employees and contractors. Those issues are easy to create and annoying to unwind.

The fixes are equally predictable. Get an engagement document signed. Route payments through one labeled account. Split the chart of accounts so employee and contractor totals can be tested quickly. When a worker's role evolves, do not leave the old classification on autopilot. Add a dated memo for the change, update records prospectively, and keep pre-change and post-change records easy to separate.

Clean classification plus contemporaneous records makes filing much less stressful. For every person you pay, keep the engagement record, payment proof, and category total that ties to your reporting roll-up.

The Takeaway: Pick Defensible Deductions, Prove Them Once#

The goal is not to chase every possible expense. It is to claim the deductions you can explain clearly and prove quickly. Keep categories aligned with Schedule C (Form 1040), and make sure the totals reconcile to statements and ledger entries before you file.

Use extra care where judgment is higher. Vehicle and travel categories are common trouble spots, so keep mileage logs, purpose notes, itineraries, and receipts current. Use Publication 463 when classifying car and travel costs, and use the current-year mileage rules for your filing year rather than relying on an old rate.

Business status matters too. A true trade or business reflects a profit motive plus continuity and regularity. If an expense looks personal or disconnected from paid work, pause before claiming it.

Use this checklist:

- write the purpose at purchase time

- store the invoice or contract with payment proof

- reconcile category totals quarterly

- keep vehicle and overnight travel records separate

- map categories to Schedule C labels early

- tag edge cases such as pre-start costs with a short note

Run that process on a steady cadence: clean records monthly, reconcile quarterly, and do a targeted red-flag sample before filing. When boundary decisions come up, such as a first hire, a role reclassification, or unusual travel, verify the rule before filing and save your reasoning with the records. Clear documentation now makes future review much faster and much less stressful. If your next gap after deductions is cash planning, pair this process with your quarterly estimated tax routine.

Frequently Asked Questions

What expenses actually count as freelancer tax deductions?

Costs for your trade that clearly tie to business activity qualify. Write a one-line business purpose for each expense, then keep an invoice or contract, proof of payment, and a dated record you can trace into your year-end totals. If you cannot explain how the cost helped deliver client work, do not claim it. For official guidance, consult the IRS self-employed individuals tax center.

Who qualifies to claim self-employed deductions?

If you are a business owner or contractor who provides services to other businesses, you are generally considered self-employed and may claim business expenses. Payers generally do not withhold or pay taxes on payments to independent contractors, so you report income and deductions yourself. Keep a short classification note and your contracts so the status is clear.

How do I claim deductions on my return?

Report your business income and expenses on your federal return and keep your records organized so they reconcile to your totals. Maintain category totals that match bank or card statements and keep your evidence pack attached to each entry. Avoid guessing line mechanics. Focus on clean documentation and totals that tie out.

Can I deduct my health insurance as a freelancer?

Eligibility for a self-paid health insurance deduction depends on current IRS rules. Keep the policy, premium statements, and payment proofs together, labeled to the tax year. Verify requirements in official guidance before claiming, and track this alongside other items so you can see the combined impact on taxable income.

What’s the rule of thumb for start-up costs?

You can choose to deduct up to $5,000 of business start-up costs now and claim the remaining cost over 15 years. Document the business start date and keep invoices or legal filings showing when activity began. If an expense predates an active trade or business, decide whether it belongs in start-up costs versus current professional fees and note your position.

Are vehicle expenses deductible for client work?

Whether vehicle expenses are deductible depends on business purpose and current rules. Keep a contemporaneous trip log with dates, destinations, and purpose notes, plus related receipts. Choose a method and stick to it. Verify eligibility against current IRS guidance and rely on your log and evidence.

What changed recently with SALT and should I care?

This section does not include change details or limits. Verify current rules before filing, and document SALT decisions clearly on the personal-return side. Tip: For eligibility and record examples on workspace claims, see The Complete Guide to the Home Office Deduction.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Quarterly Estimated Taxes for Freelancers Without Guesswork

Use this as your start-of-quarter routine: separate the tax tracks, verify the facts, then calculate and pay. That replaces stale assumptions with a routine that cuts surprise balances. At the start of each quarter, define two things first:

How Much Should a Freelancer Save for Taxes? A Monthly Reserve Rule and Quarterly True-Ups

Use one monthly reserve rule, then adjust it with your actual filings and estimated-payment results. If you are asking **how much to save for taxes freelancer** income creates, the practical answer is not one fixed percentage. It is a repeatable process: move money monthly, check it quarterly, and correct course before a shortfall turns into a problem.

Home Office Deduction Rules for Freelancers With Multiple Homes

For globally mobile freelancers, this deduction is a compliance decision before it becomes a tax-saving tactic. The practical rule is simple: claim it only when your facts clearly pass the IRS tests and your records can support that position from worksheet to filed return. If the facts are mixed, stop before you calculate and get a focused review.