Quick Answer

A freelancer should save using a monthly reserve rule and adjust it quarterly against actual net income, Schedule SE estimates, and estimated tax payments, not rely on one fixed percentage. Keep self-employment tax separate from income tax, move the reserve as payments arrive, and use prior filings plus current IRS guidance to reset the rate when your numbers drift.

Start here and stop guessing your freelancer tax savings rate#

Use one monthly reserve rule, then adjust it with your actual filings and estimated-payment results. If you are asking how much to save for taxes freelancer income creates, the practical answer is not one fixed percentage. It is a repeatable process: move money monthly, check it quarterly, and correct course before a shortfall turns into a problem.

This guide is about setting aside money for freelance taxes. It is not legal advice for every jurisdiction or a full cross-border residency guide. The goal is simple: leave with a monthly transfer rule, a quarterly review habit, and clear triggers for when to bring in a tax professional.

Step 1 Commit to a monthly transfer rule#

Start with consistency, not perfect precision. Move money into a tax reserve every month, or whenever client payments land if that is easier to follow. Reserve tax money before it starts to feel spendable.

Treat your starting rate as provisional. If you have last year's return, use it as a reality check. If you do not, use a conservative placeholder and plan to adjust after your first quarterly review.

Step 2 Anchor the method to what the IRS actually taxes#

Keep self-employment tax separate from your full tax picture. The IRS defines self-employment tax as Social Security and Medicare taxes, with a stated rate of 15.3% made up of 12.4% Social Security and 2.9% Medicare. The IRS also says this does not include other taxes you may owe, such as income tax.

Use filing documents to check whether your reserve method makes sense. Self-employment tax is calculated on Schedule SE. If you have a prior return, compare it with your current setup to see whether your reserve rule is in range.

For 2024, the first $168,600 of combined wages, tips, and net earnings is subject to the Social Security portion. Do not assume an older threshold still applies. Check current IRS guidance before you lock in a number.

Step 3 Define the quarterly checkpoint and escalation rules#

A monthly reserve rule only works if you correct it during the year. Freelancers usually do not have employer withholding, so estimated tax payments matter. Those payment amounts can change as earnings and deductions change.

At each checkpoint, compare year-to-date net income, money reserved, and what you expect to pay next. If the gap is widening, update your transfer rule now. Waiting until filing season can mean penalties or a bill that is much larger than expected.

Who this method is for and what it does not solve#

Use this method when you need a practical reserve system for uneven freelance income, not a full cross-border tax decision engine.

Step 1 Identify whether your tax picture is operationally simple enough#

This approach works best when your main problem is cash management, not legal uncertainty. It fits people who work for themselves and want a reliable U.S. reserve habit. The test is simple: can you track business income, estimate what you may owe during the year, and reconcile that to core U.S. filing documents like Schedule SE?

That distinction matters because self-employment tax is narrow, not a catch-all. The IRS defines it as Social Security and Medicare taxes only. If you can map earnings to that calculation and plan for estimated tax payments during the year, this method gives you a workable way to stay ahead. It still helps when income swings month to month.

Step 2 Exclude problems this method does not answer#

A reserve process is useful, but it does not answer everything. It does not determine country-specific tax residency, resolve treaty eligibility, or tell you whether a partnership or other entity structure should change.

A common mistake is treating a savings method as full compliance. Another is waiting until the annual return to pay everything, which can lead to penalties and interest. If your real uncertainty is which country can tax you, or how two systems interact, a reserve rule helps with cash flow but does not settle the legal issue.

Step 3 Escalate when more than one tax system is active#

Once more than one tax system is in play, keep using this process to stay organized, then have your assumptions reviewed by a tax professional. Bring a small evidence pack with year-to-date income totals, reserve transfers, estimated payment records, and the forms you use to compute U.S. self-employment tax.

Also, do not rely only on whether you received a Form 1099. Income may still need to be reported even if no 1099 arrived, so your reserve decisions should follow your own records, not just incoming forms.

What to prepare before you calculate anything#

Set your savings rate only after your records and current IRS checkpoints line up. Otherwise, a percentage turns into a guess.

| Prep item | What to verify | How to use it |

|---|---|---|

| Income, expense, and deposit records | Cross-check what you earned, what you spent on ordinary and necessary business expenses, and what reached your account | Run one monthly reconciliation first and fix mismatched totals before choosing a percentage |

| Prior filings and Schedule SE | Review any prior Schedule SE before setting a new reserve percentage | Use prior filings as context, not as your only source of truth |

| IRS Self-Employed Individuals Tax Center | Confirm current obligations, the quarterly payment process, and annual return filing steps | Use it as a live checkpoint and remember the self-employment tax page is not all-inclusive |

| Gruv transaction and payout exports | Trace dates, amounts, and payout activity clearly enough to explain differences across your records | Treat exports as operational records that support your process, not as a substitute for tax filings |

Step 1 Gather records you can reconcile#

Start with records you can reconcile across income, expenses, and deposits. Confirm what you earned, what you spent on ordinary and necessary business expenses, and what reached your account.

Before you calculate any percentage, run one monthly reconciliation across those records. If totals do not line up, fix that first. A reserve rate built on messy records will drift no matter how careful the math looks.

Step 2 Pull prior filings as reference inputs#

Use prior filings as context, not as your only source of truth. If you have a prior Schedule SE, review it before setting a new reserve percentage.

Keep the definitions straight while you review. Net earnings from self-employment are gross business income minus ordinary and necessary business expenses. Schedule SE is used to figure self-employment tax on those net earnings. Self-employment tax refers to Social Security and Medicare taxes only, not every tax you may owe.

If your self-employment income is low or negative, check whether one of the optional Schedule SE methods may be beneficial.

Step 3 Confirm current IRS obligations before choosing a rate#

Before you choose a percentage, use the IRS Self-Employed Individuals Tax Center as your live checkpoint. Confirm current obligations, the quarterly payment process, and annual return filing steps there.

Do not rely on a single IRS page. The IRS notes that its self-employment tax page is not all-inclusive. Keep one filing threshold in view during prep: you must file an income tax return if your net self-employment earnings were $400 or more.

Step 4 Export an auditable transaction trail#

If you use Gruv where supported, export transaction history and payout trails now so your monthly reconciliation is repeatable. Treat those exports as operational records that support your process, not as a substitute for tax filings.

Your export trail should let you trace dates, amounts, and payout activity clearly enough to explain differences across your records.

Step 1 classify your work correctly before you set a percentage#

Set your savings percentage only after you classify your work status, because that status affects which taxes and forms you need to plan for.

Confirm the IRS category you fit#

Start with the IRS self-employed categories. You are generally in scope if you are:

- carrying on a trade or business as a sole proprietor or independent contractor

- a member of a partnership that carries on a trade or business

- otherwise in business for yourself, including gig work

For self-employment tax purposes, a sole proprietor also includes a single-member LLC that is disregarded for federal income tax purposes. Use the IRS Self-Employed Individuals Tax Center, including its Business structures section, as your checkpoint.

Match that status to the filings behind your set-aside#

Build your reserve from filing reality, not a generic percentage. Schedule SE (Form 1040) is used to figure self-employment tax on net earnings from self-employment. That tax covers Social Security and Medicare taxes only, not every tax you may owe.

The IRS states a 15.3% self-employment tax rate, made up of 12.4% Social Security and 2.9% Medicare. It generally applies that rate to 92.35% of net self-employment earnings. Net earnings are gross business income minus ordinary and necessary business expenses. Review the filing set you expect to use before locking in a rate, and check current Schedule SE instructions for exceptions.

Separate business and personal flows before you trust the math#

Because net earnings are based on business income and business expenses, keep business and personal activity separate in your records so the calculation stays usable.

Recheck when your classification changes#

If your classification changes during the year, revisit your setup. That includes shifts such as independent contractor work, joining a partnership, or operating through a disregarded single-member LLC.

Keep the IRS threshold in view as well. You usually must pay self-employment tax if net self-employment earnings are $400 or more, with exceptions in some cases.

Step 2 choose a starting rate that you will adjust, not worship#

Use a starter rate as a working estimate, not a rule. There is no universal freelancer percentage because self-employment tax is only one layer of what you may owe.

The IRS states that self-employment tax is 15.3% made up of 12.4% Social Security + 2.9% Medicare, and it is generally applied to 92.35% of net self-employment earnings. The same guidance also says self-employment tax covers Social Security and Medicare only, not your entire tax bill. So a flat percentage can feel adequate in your account and still leave you short.

Start from verifiable tax math#

If you filed before, use your prior Schedule SE (Form 1040) as the baseline for the self-employment-tax layer. If you have no prior return, treat your first rate as provisional and plan to adjust it after your first review checkpoint.

Also, do not hard-code old limits into your method. IRS guidance shown here includes $168,600 for 2024 as the Social Security taxed cap on combined wages, tips, and net earnings, and that amount changes by year.

Pick an operating method you will actually maintain#

Choose the simpler method if that is what you will consistently follow. More detail helps only if your bookkeeping supports it. Your income pattern should drive how cautious you are.

| Approach | What it looks like | Pros | Failure mode | Usually suits |

|---|---|---|---|---|

| One blended set-aside bucket | One transfer from each client payment into one tax account | Simple, fast to start, low admin | Can hide whether the shortfall is in self-employment tax or another tax layer | New freelancers or anyone building saving discipline first |

| Split tax buckets | Separate reserves for self-employment tax and other tax obligations | Better visibility and faster course-correction | More admin; weak bookkeeping can make the split unreliable | Freelancers with steady operations and regular bookkeeping |

Use income pattern as the decision rule#

Your income pattern should drive the choice.

- If income is volatile, start with a more conservative rate and tighten it through regular reviews.

- If income is stable, calibrate faster using prior return data.

- If your business changed materially this year, treat last year's rate as stale and recalculate.

Set one review trigger now#

At each review checkpoint, compare your year-to-date reserve with your current net-earnings view and a fresh Schedule SE estimate. If your reserve is not clearly covering the self-employment-tax layer, increase transfers before discretionary draws.

Use current IRS instructions when you true up. For example, the IRS posted a correction to the 2025 Instructions for Schedule SE on 20-FEB-2026, which is a useful reminder that fixed percentages need review.

Step 3 split your monthly set-aside into tax buckets#

If you want fewer surprises, split the reserve. At minimum for this method, keep one bucket for self-employment tax and one for income tax so you can see which part is drifting.

Open two distinct tax buckets#

At minimum, track these two buckets:

- Self-employment tax bucket

- Income tax bucket

Use separate accounts or separate bookkeeping categories, but make each balance and transfer visible every month. These two buckets help you separate federal self-employment tax from income tax, but they may not cover every tax obligation.

Size the self-employment bucket from actual components#

Base this bucket on IRS components, not a round-number guess. Self-employment tax is 15.3% made up of 12.4% Social Security + 2.9% Medicare, and it is generally figured on 92.35% of net earnings from self-employment.

Use your current net earnings estimate each month, then check that method against Schedule SE (Form 1040). Keep two points in view: Medicare applies to all net earnings, and the Social Security portion has an annual earnings base that changes by year. The IRS example shown here is $168,600 for 2024.

Reserve buckets before cash is treated as spendable#

The order matters more than the tool you use. Keep it fixed:

- Receive payment

- Update your current net-earnings estimate

- Transfer amounts into both tax buckets immediately

- Use the remainder as operating cash after those transfers

That sequence keeps tax reserves from quietly turning into general spending money.

Treat missed transfers as a hard internal control point#

If you miss a month, catch up before owner draws. That is your internal control, not an IRS timing rule.

Rebuild that month's net-earnings estimate, calculate the missed amounts for both buckets, and transfer the catch-up first. Split buckets make this easier because you can see exactly which reserve is behind.

Step 4 run a quarterly true-up before each payment window#

Quarterly true-ups are where this process turns into a reliable system. Use current year-to-date data, not memory, and correct drift before it compounds.

Step 1 build a simple quarterly checkpoint table#

Keep one table for the year and update it before each payment window.

| Quarter check | YTD net income estimate | Tax reserved so far | Expected quarterly estimated tax payments YTD | Variance |

|---|---|---|---|---|

| Q1 true-up | $___ | $___ | $___ | $___ |

| Q2 true-up | $___ | $___ | $___ | $___ |

| Q3 true-up | $___ | $___ | $___ | $___ |

| Q4 true-up | $___ | $___ | $___ | $___ |

Use net income, not gross billings. For self-employment tax, the working base is net earnings from self-employment, which means gross business income minus ordinary and necessary business expenses. Tie every number in the table to a source document before you move on.

Step 2 reconcile against current-year numbers, not last-year memory#

If income or expenses changed, rerun your reserve math from updated year-to-date net income. That is the practical way to answer the savings question when revenue is uneven.

For the self-employment side, check your Schedule SE estimate inputs. The total is 15.3%, made up of 12.4% Social Security and 2.9% Medicare, and it is generally applied to 92.35% of net earnings from self-employment. A blended reserve can drift because Social Security has a maximum earnings base while Medicare does not share that same cap.

Write a one-sentence reason for each adjustment next to the quarter row so you can explain later why you changed course.

Step 3 review the filing artifacts that support your numbers#

Use the same supporting documents each cycle and keep them with the quarter checkpoint:

- Updated Schedule C working numbers

Current working view of income and deductible business expenses, aligned to your books.

- Schedule SE estimate inputs

The worksheet you used to estimate self-employment tax.

- Payment confirmations

Confirmation IDs, PDFs, or bank proof for estimated tax payments.

As a control, verify that you are using current Schedule SE instructions. The IRS posted a correction to the 2025 Schedule SE instructions on 20-FEB-2026, which is a reminder that guidance can change.

Step 4 reset the monthly formula if variance keeps repeating#

If variance keeps repeating across quarters, treat that as your signal to reset the monthly transfer formula. This is a control rule, not an IRS rule.

If you are repeatedly short, increase transfers or move money into tax buckets faster after each payment. If you are repeatedly over-reserved, lower transfers only when your updated Schedule C and Schedule SE working numbers support that change. This is what keeps your monthly process reliable for real quarterly estimated taxes.

How deductions should change your savings target#

Deductions should refine your reserve, not give you a reason to lower it too early. Save a little high until expenses are documented and categorized.

Step 1 treat deductions as a later adjustment, not an early assumption#

Start from current net business income and save conservatively, then adjust after the deduction is supported in your bookkeeping. Deductions can reduce taxable income, but planned write-offs do not help if they are not yet recorded.

If a deduction is real but not documented, leave your reserve alone. Once it is documented and reflected in your books, then adjust.

Step 2 prioritize deductions that map cleanly to Schedule C#

Prioritize expenses you can track clearly and report cleanly on Schedule C. Self-employed deductions are ordinary and necessary business expenses, and Schedule C is where those deductions are reported on a personal return.

In practice, start with categories that have a clear paper trail and business purpose, such as software, supplies, professional fees, and, where applicable, home office. The checkpoint is simple: can you tie the amount in your books to supporting records?

Step 3 adjust reserves only after the deduction is supported in your books#

Set one control rule and stick to it. Do not reduce reserves until the deduction is recorded, categorized, and traceable to supporting records.

Deductions may reduce what you owe, including self-employment tax, but only after they are reflected in your books. Better deduction tracking can save money, but it also demands stronger record-keeping. Follow this sequence consistently: book it, verify it, then lower the reserve.

Cross-border realities that break one-size-fits-all freelancer advice#

Cross-border facts can change what you must file and when, even if your freelance income looks the same. If you changed countries mid-year or hold foreign financial accounts, treat your reserve plan as something an advisor should review before you finalize it.

Step 1 add a cross-border status check before you trust your savings rate#

Start with a one-page timeline showing where you lived and worked during the year, when any move happened, and which foreign accounts you opened or kept. The goal is not to solve every cross-border rule yourself. It is to spot escalation triggers early.

If that timeline shows a mid-year move or foreign accounts, do not treat this as a normal DIY-only case. U.S. reporting scope and timing can shift even when the business itself looks unchanged.

Step 2 screen for U.S. foreign asset reporting before year-end#

If you are a U.S. taxpayer with foreign financial assets, screen FATCA/Form 8938 early. Certain U.S. taxpayers must report specified foreign financial assets on Form 8938 when thresholds are met.

Form 8938 is attached to your annual return and filed by that return's due date, including extensions. Not every account is reportable on Form 8938, and the thresholds are not one-size-fits-all. IRS baseline language starts at $50,000, with higher thresholds for some joint filers and taxpayers residing abroad. Use current IRS instructions for your exact case.

Step 3 separate Form 8938 from FBAR and gather an evidence pack#

Do not collapse Form 8938 and FBAR into one task. These can be separate obligations, so evaluate both.

Build a compact verification pack before filing:

- foreign accounts or assets that may be reportable

- records showing account ownership, institution details, and values used for threshold checks

- your move timeline and expected U.S. filing status

The risk here is missing a reporting obligation even when your return otherwise looks straightforward. The IRS warns of serious penalties for not reporting required foreign financial assets. Also note that if you do not have to file a U.S. income tax return for the year, Form 8938 is not required for that year. That is another reason to get a reviewed decision before you finalize reserves.

When to bring in a tax professional right away#

Once your situation no longer fits a straightforward DIY self-employment return, bring in a tax professional early. IRS self-employed guidance includes considering a tax professional, and the goal is to get a reviewed plan before errors affect your reserve, quarterly payments, and annual filing.

Step 1 escalate when your case goes beyond basic self-employment tax guidance#

Treat the basic self-employment tax page as a starting point, not a complete checklist. IRS self-employment tax guidance is explicitly limited to Social Security and Medicare and is not all-inclusive for every business situation.

If you lived outside the U.S., count that as an added complexity signal. The Schedule SE instructions include a dedicated section for U.S. citizens or resident aliens living outside the United States.

Step 2 verify your records can support Schedule SE#

Before you adjust your savings rate again, do one hard check: can your records cleanly support your net-earnings inputs for Schedule SE? If not, get a professional review before filing.

Schedule SE is used to calculate self-employment tax on net earnings, and you usually must pay self-employment tax when net earnings from self-employment are $400 or more. If your records do not reconcile to those inputs, your reserve math is not reliable yet.

Step 3 ask for a scoped review first#

Start with a narrow brief and ask the professional to confirm:

- your set-aside method for income tax and self-employment tax

- your quarterly payment cadence

- your actual filing obligations, including any special forms tied to your facts

Share a compact evidence pack with current bookkeeping, prior Schedule SE work, and your move timeline if relevant. You should leave with a clear yes or no on your reserve method, a corrected quarterly plan, and a concrete list of forms you need to file.

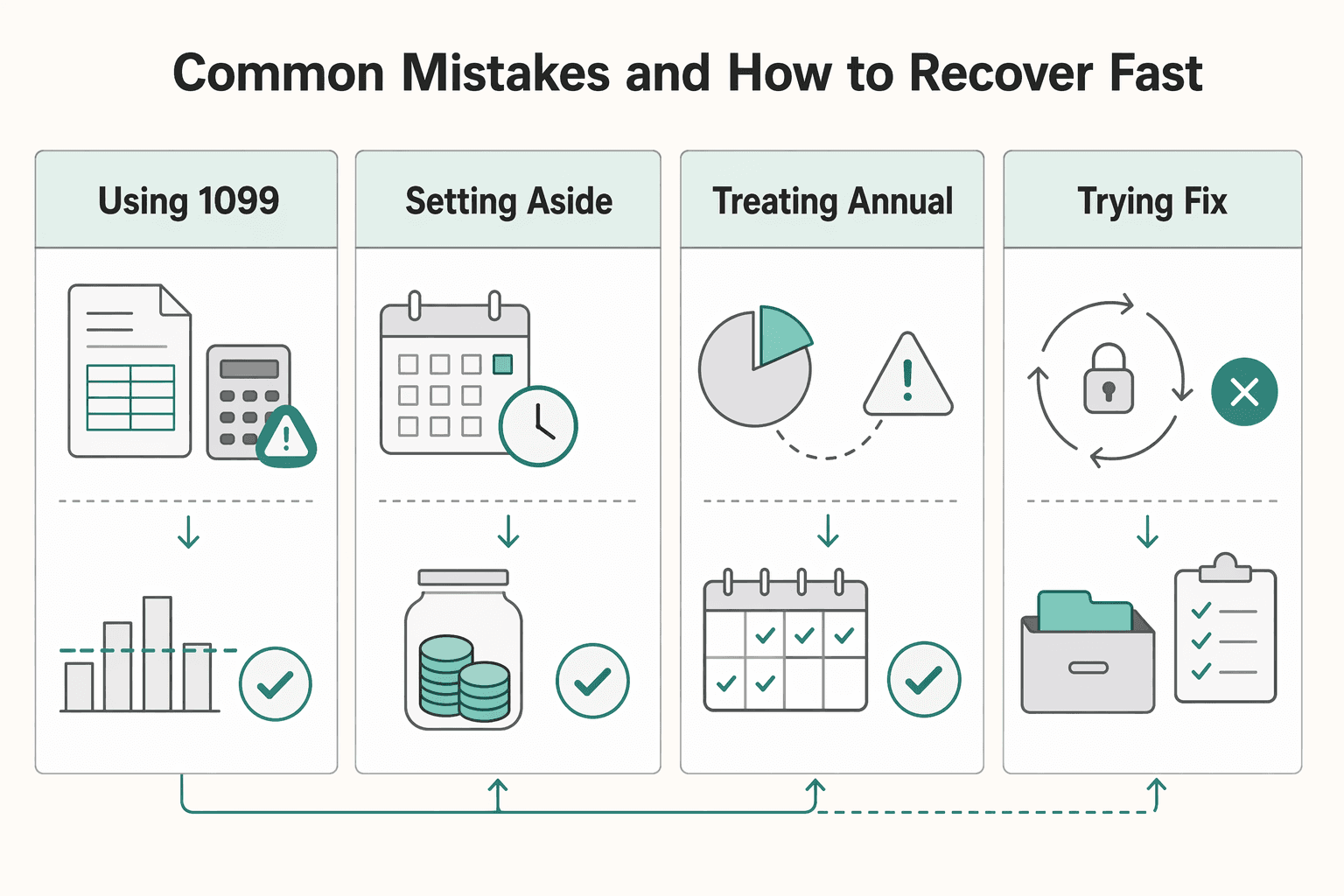

Common mistakes and how to recover fast#

Most problems here come from process drift, not lack of effort. The usual issues are using the wrong number, setting money aside too late, or repeating a method that already failed.

| Mistake | What the article says | Recovery |

|---|---|---|

| Using 1099 totals as the tax base | A 1099 reports income, but it does not by itself determine total tax owed | Rebuild your year-to-date view from your own records and reconcile what you were paid against what you recorded |

| Setting aside tax cash from leftovers | Freelance income usually comes without withholding, so the set-aside has to happen when payment arrives | Make the tax transfer first on every client receipt, then run the rest of your cash flow |

| Treating the annual return as paperwork only | Your annual return is feedback, not just paperwork | Compare what you set aside during the year with what you actually owed, then adjust your monthly or per-payment transfer logic for next year |

| Trying to fix a late tax issue with a small percentage tweak | A late tax issue is usually a review-now problem, not a tweak-the-percentage problem | Stop guessing, gather complete records, get targeted compliance advice, and tighten your quarterly estimated taxes process |

Step 1 recalculate from business records, not 1099 totals#

Form 1099 totals are not your full tax base by themselves. A payer may issue a 1099 when payments from one source reach $600 or more, but you still need complete income and expense records to calculate correctly.

Recovery is simple in concept, even if it takes work. Rebuild your year-to-date view from your own records, then reconcile what you were paid against what you recorded. Include income even if no 1099 was issued, and keep documented business expenses in the same working file.

Step 2 transfer tax cash first, not from leftovers#

If you wait to see what cash is left, you increase the chance of a bill you cannot comfortably pay. Freelance income usually comes without withholding, so the set-aside has to happen when payment arrives.

Recovery: make the tax transfer first on every client receipt, then run the rest of your cash flow. If you are unsure about the amount, a third of freelance income is a common rule of thumb to start with, then refine it from real results.

Step 3 use your annual return as a reset signal#

Your annual return is feedback, not just paperwork. Freelancers still file annually in addition to making periodic payments, so use that result to improve your reserve method.

Recovery: compare what you set aside during the year with what you actually owed, then adjust your monthly or per-payment transfer logic for next year.

Step 4 escalate quickly if a tax issue appears late#

A late tax issue is usually a review-now problem, not a tweak-the-percentage problem. The fastest recovery path is to stop guessing, gather complete records, and get targeted compliance advice.

If your payment rhythm is still inconsistent, tighten your quarterly estimated taxes process at the same time.

Copy and paste checklist for monthly and quarterly tax control#

Use this as an evidence-first checklist. Each action should leave a record you can verify later.

Run your monthly close

- Classify income, post records, log anomalies, and save support in the same order each month.

- Work from your own invoices, payout reports, bank activity, and expense receipts, not only one statement or form.

- Tag unusual items right away, such as refunds, chargebacks, mixed personal spending, or payments posted to the wrong account, while the trail is still easy to fix.

Do a quarterly reality check

- Compare year-to-date bookkeeping against the records you plan to rely on for your annual return.

- If records are drifting from your current numbers, correct entries now instead of waiting for year-end.

- Archive each quarterly reconciliation note with that quarter's bookkeeping file.

Reconcile annual return inputs and cross-border filings

- Reconcile your books to the inputs you will use on your annual return.

- If you hold foreign accounts or other specified foreign financial assets, review Form 8938 early.

- Form 8938 is attached to your annual return and follows that return's due date, including extensions.

- Filing Form 8938 does not replace a separate FBAR (FinCEN Form 114) filing when FBAR is otherwise required.

- Confirm whether any foreign deposit or custodial accounts were closed during the tax year, because Form 8938 asks this directly.

- Keep in mind that the IRS notes serious penalties for failing to report foreign financial assets, and that higher Form 8938 thresholds can apply to joint filers and certain taxpayers living abroad.

- If you are not required to file a U.S. income tax return for the year, Form 8938 is not required.

Archive your full documentation packet

- Keep your tax packet together: bookkeeping files, payment confirmations, statements, invoices, and filed forms.

- If you use Gruv where supported, export transaction history and audit trails and store them with the same packet.

- Treat Gruv exports as supporting records, not substitutes for your core tax documents.

Build a low-stress tax habit you can actually keep#

A low-stress tax routine comes from a simple rhythm. Move money regularly, review it on a recurring cadence, escalate early when things get more complex, and keep clean records all year.

Step 1. Automate the first move after every payment

When client money hits, transfer the tax reserve before treating any of it as spendable cash. With 1099 income, no one is withholding taxes for you, so delay usually turns your reserve into whatever is left.

Many freelancers keep separate buckets for self-employment tax and income tax. The self-employment piece covers Social Security and Medicare, and one commonly cited figure is 15.3%, so separate buckets can make drift easier to spot.

Your regular checkpoint is simple: every payment should have a matching reserve transfer and a matching record entry.

Step 2. Run a regular true-up against your actual books

Regular reviews are where planning turns into accuracy. Compare year-to-date income minus documented business expenses with what you have actually reserved and paid.

Do not use 1099-NEC totals as your only checkpoint. Income still has to be reported and taxed even if no 1099 is issued, so reconcile invoices, payout records, deposits, and bookkeeping, including clients below the typical $600 1099-NEC threshold.

Step 3. Set escalation rules before complexity gets quiet

Decide in advance when to stop doing this alone. Escalate if your records stop mapping cleanly, if you repeatedly under-save, or if major gaps between booked income and your documents are hard to explain.

That guardrail helps you avoid a common failure mode. Quiet under-saving can turn into a large bill plus penalties at tax time.

Step 4. Keep an evidence pack that improves every year

Keep one organized file with invoices, payout reports, bank statements, expense support, tax payment confirmations, and any 1099-NEC forms you receive. That makes your numbers easier to defend and your reserve method easier to refine each year.

Use one practical test. Can someone follow your records from deposits to net income without guessing? If not, fix the records before you change the percentage.

Frequently Asked Questions

How much should a freelancer save for taxes each month?

There is no universal monthly percentage. Use a working reserve that covers both self-employment tax and income tax, then adjust it against year-to-date records and quarterly reviews. The self-employment tax layer is 15.3%, generally applied to 92.35% of net earnings, but that is not your full tax bill.

Do I save one percentage for everything or separate self-employment tax and income tax?

Separate buckets are usually easier to track. Self-employment tax covers Social Security and Medicare only, not your full tax bill. A combined bucket can look healthy while still leaving you under-reserved on income tax.

Who is treated as self-employed for tax purposes?

For this purpose, the IRS generally includes sole proprietors, including independent contractors, partners, and others in business for themselves. A sole proprietor can also include a single-member LLC that is disregarded for federal income tax purposes. If that is your status, Schedule SE is part of the filing reality behind your set-aside.

Does income reported on Form 1099-NEC or Form 1099-MISC automatically determine what I owe?

No. A 1099 reports income, but it does not by itself determine total tax owed. Build your set-aside from net business income using your own records, not 1099 totals alone.

Can deductions like the home office deduction lower how much I should set aside?

Potentially. Deductible business expenses can reduce net earnings, but the article recommends keeping your reserve conservative until the deduction is recorded, categorized, and supported in your books. Follow the same sequence each time: book it, verify it, then lower the reserve.

What is the practical role of Schedule C and Schedule SE in my savings calculation?

Schedule C is where deductible business expenses are reported, so it helps you determine net earnings. Schedule SE is used to calculate self-employment tax on those net earnings. It also matters for future benefits because the Social Security Administration uses Schedule SE information to figure benefits.

When should a globally mobile freelancer stop DIY and hire a tax professional?

When your filing situation is no longer straightforward or your records do not cleanly support your calculations, stop treating it as a DIY-only case. Mid-year country moves, foreign accounts, or more than one tax system are escalation signals in this guide. A scoped professional review can validate your reserve method, quarterly plan, and filing obligations.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 5 external sources outside the trusted-domain allowlist.

- irs.gov/businesses/small-businesses-self-employed/se...trusted

- irs.gov/taxtopics/tc554trusted

- ssa.gov/international/CoC_link.htmltrusted

- blog.turbotax.intuit.com/self-employed/wait-i-have-to-pay-taxes-four-...external

- collective.com/blog/tax-tips/a-freelancers-guide-to-getting...external

- gusto.com/resources/articles/taxes/self-employment-tax...external

- hrblock.com/tax-center/small-business/self-employed/tax-...external

- hrblock.com/tax-center/small-business/self-employed/self...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Quarterly Estimated Taxes for Freelancers Without Guesswork

Use this as your start-of-quarter routine: separate the tax tracks, verify the facts, then calculate and pay. That replaces stale assumptions with a routine that cuts surprise balances. At the start of each quarter, define two things first:

Freelance Financial Management That Protects Cashflow First

Stabilize cash timing first. Perfect budgeting can wait. When payments arrive unevenly, the immediate win is a repeatable way to see what came in, what needs to be set aside, and what is actually safe to spend this week.

Top 10 Tax Deductions for Freelancers

If you report business income on Schedule C (Form 1040) for work you do with continuity, regularity, and a real profit motive, these ten categories are the right place to start. The practical rule is simple: claim only what you can prove quickly with records created near the time you spent the money. When the paper trail is thin, the deduction is weak, even if the expense felt business related.