Quick Answer

Start with account separation and a three-lane money setup: Operating, Tax, and Reserve. For freelance financial management, the fastest improvement is tagging each payment when it arrives, then reconciling expected versus actual receipts on a weekly and month-end cadence. Keep an evidence pack per invoice with the invoice copy, payment confirmation, and delay notes. Move tax funds on receipt day, and only increase retirement contributions after reserves are stable.

Start with the outcome you actually need#

Stabilize cash timing first. Perfect budgeting can wait. When payments arrive unevenly, the immediate win is a repeatable way to see what came in, what needs to be set aside, and what is actually safe to spend this week.

For freelancers, creators, and small teams, the job is not fancy budgeting. It is control. Income moves with project volume, pricing, competition, and client behavior, so the first goal is visibility you can use right away. At any point, you should be able to answer three questions without digging through five apps: what has been invoiced, what has been paid, and what part of current cash is already spoken for.

Keep the sequence simple. Protect cash flow first. Then improve tax handling and long-term savings. Add complexity only when your volume justifies it. Reversing that order usually makes planning harder, not easier. Extra tools and extra accounts can create the appearance of order while the real problem, uneven inflows, stays untouched.

A dedicated business account is one of the first checkpoints. Yes, it is one more account to maintain. The tradeoff is still worth it, because income, expenses, and tax prep stop disappearing into personal spending. You do not need a complicated setup on day one. You do need one clean place where business activity stays visible.

Use the same checklist when you add a client and again at month-end:

- Define payment terms before kickoff, including due date and invoice approver.

- Log each invoice with issue date, amount, and expected payment date.

- Confirm receipt, then tag funds by purpose before spending.

- Keep a small support file for each invoice: invoice copy, payment confirmation, and notes on any fee or delay.

- Run a monthly compare step: expected receipts versus actual receipts, with exceptions listed.

- If a client requests onboarding documents before payment, collect them early.

This checklist works in two places. At the start of a client relationship, it keeps missing details from getting buried under delivery work. At month-end, it gives you a clean way to test whether what should have happened is what actually happened. If an invoice is missing, delayed, short-paid, or held, the same checklist shows you where the break occurred.

Keep the exception list practical. It does not need to be a long report. It just needs to show which invoice is off track, what the current blocker is, who needs to act, and what the next step is. That turns "something seems wrong" into a short queue you can clear.

This will not eliminate delays, fees, or country-specific rules. It does give you one operating habit you can run client by client and month by month with fewer surprises. Once that outcome is clear, the next move is to decide how money should flow before you start shopping for software. If you want a quick starting point, try the free invoice generator.

Define your money system before you pick tools#

Tools are rarely the first problem. Most money issues start earlier, when an invoice is created, sent, paid, or misclassified. Set the rules first, then pick software that supports them. A simple spreadsheet works if the rules are clear. An expensive tool will not rescue a messy process.

| Lane | Purpose | Timing |

|---|---|---|

| Operating | Keeps current work and bills moving | Classify immediately when a payment lands |

| Tax | Money you set aside and do not treat as spendable | Classify immediately when a payment lands |

| Reserve | Buffer when a client pays late or a payout gets held | Classify immediately when a payment lands |

When a payment lands, classify it immediately into three lanes: Operating, Tax, and Reserve. Operating keeps current work and bills moving. Tax is money you set aside and do not treat as spendable. Reserve is the buffer that helps when a client pays late or a payout gets held. Then use the monthly close as the point where ledger totals, bank activity, and open invoices line up.

The key is timing. If you wait until the end of the week or the end of the month to decide what a payment was for, that money will often get spent as one mixed balance. Lane assignment works because it happens right after receipt, while the invoice, amount, and purpose are still obvious. That keeps later reviews short and keeps spending decisions tied to actual availability instead of a rough bank balance.

Treat the ledger as your source of truth. Each invoice ID should carry a compact record set: the invoice itself, payment confirmation, payout status, and the related tax record. That keeps follow-up, tax prep, and dispute handling tied to the same record instead of scattered across an inbox, payment platform, and memory.

A common failure mode is invoicing from outdated documents after terms changed. That is one of the easiest ways for avoidable errors to creep in. Keep one current client agreement as the source for invoicing and payment fields so reminders, amount due, and routing details all come from the same place.

Another failure mode is status drift. The invoice was sent, then partly discussed by email, then marked paid in one place but not another, then followed up by someone using old terms. Once status splits across tools, the problem is no longer just bookkeeping. It affects reminders, tax handling, and how confidently you can speak to the client about what is owed.

At close, do four checks before you blame the software:

- Verify each open invoice has one status only: sent, paid, or overdue.

- Match every bank deposit to an invoice ID and lane assignment.

- Confirm lane transfers were recorded when payment was received.

- Flag mismatches between agreement terms and invoice fields before reminders go out.

If you find a mismatch, trace it backward in order. Start with the invoice record. Then check the agreement terms that support it. Then check the deposit or payout trail. Then confirm the lane transfer. That sequence is faster than jumping around between apps because it follows the path the transaction actually took.

The operating rule here is simple: if the books do not reconcile at close, fix the record at the point it was created before you switch software or add automation. Once those rules work on paper, account setup gets much easier. If retirement planning is your next question, read The Best Retirement Plans for Self-Employed Individuals.

Set up accounts and legal separation on day one#

Set this up on day one, not after the first messy month. If personal and business money mix early, every later step gets harder to trust.

If you operate as a sole proprietor, personal and business assets are not legally separate. A single-member LLC can add liability protection, but only when day-to-day records and accounts stay separate in practice. That distinction matters. Filing paperwork is not enough if the money trail says otherwise.

Think of account setup as a control decision, not just a banking choice. Use dedicated business accounts for business activity, keep one traceable record path per invoice ID, and fix any mixed transaction as soon as it happens with a logged correction. Cleanup is always more irritating later than it is on the day the mistake happens.

Use this day-one checklist:

- Route client payments and business expenses through business accounts only.

- Keep personal transactions out of business flows.

- Keep legal names and billing records consistent across your agreements, invoices, and payment profiles.

- Link each invoice ID to its related payment and tax records in one traceable log.

In practice, this means resisting small shortcuts. Paying a business expense from a personal card once, receiving one client payment into a personal account because it feels faster, or using a different legal name in one profile because the form looked informal all create extra cleanup. Each shortcut may seem harmless on its own. Together, they weaken the one thing you need most later: a money trail you can trust without reconstructing it from memory.

If a mixed transaction does happen, correct it immediately and note what happened. Do not leave yourself a vague reminder to sort it out later. A short logged correction is enough if it clearly ties the amount, date, account, and reason back to the original transaction. The important part is that the correction becomes part of the record instead of a private mental note.

Then run a short weekly check to make sure recent invoices, receiving accounts, and records still line up. If one item fails, fix that client batch before the next bill goes out. Once the legal and account boundary is solid, the next place to reduce risk is the client agreement itself. For a deeper walkthrough, see this guide on separating business and personal finances.

Tighten client payment terms before work starts#

Do not wait for a late invoice to learn how a client handles billing. Payment risk is cheaper to prevent before kickoff than to chase after delivery.

For every engagement, use one standard pre-kickoff checklist. Confirm payment timing, invoice routing, approval path, payment method, and any required onboarding documents before work starts. If any of those details are fuzzy, resolve them before you move ahead. A missing approver name or billing inbox looks small at kickoff and expensive a few weeks later.

It also helps to identify the detail most likely to stall payment. Sometimes it is who approves the invoice. Sometimes it is where the invoice must be sent. Sometimes it is a required reference or onboarding record the client expects before its system will release payment. You do not need a long legal review to catch these basics. You need a short checklist answered in writing.

Once billing is live, send invoices with complete details and keep one continuous record from send date through status updates. That creates a clean trail if the client says the invoice went to the wrong inbox, lacked a required reference, or is waiting on approval. It also makes your follow-up more specific and more credible, because you can point to dates, documents, and contacts instead of sending vague payment chasers.

If a client's approval flow is slow or unclear, reduce open exposure early. Break the work into smaller scopes, use clearer billing checkpoints, and keep expectations explicit throughout the project. The point is not to be rigid. It is to make it obvious what is due, when it is due, and who needs to act next.

A useful habit is to treat kickoff answers as billing inputs, not just meeting notes. If the client gives you the approver, billing inbox, or payment method in a call, move it into the same place your invoicing process pulls from. That way the information survives after the project conversation fades and the person who sends the invoice is not relying on memory.

Clear terms reduce avoidable confusion, but they do not replace follow-up. You still need a review rhythm that catches slippage before it becomes a cash problem.

Run a weekly and month-end control routine#

A monthly review by itself is too slow. By the time you notice a missing payment or bad status, the next billing cycle may already be underway.

| Attribute | Weekly | Month-end |

|---|---|---|

| Purpose | Early detection | Reconcile ledger entries so income and expenses match bank or provider records |

| Review | Confirm invoices were sent, statuses are current, and overdue items have a logged next action; compare expected receipts with credited and held funds | Confirm open invoices and their status; compare bank or provider activity to the ledger; review lane transfers and tax-reserve movements |

| Exceptions | Flag any mismatch or unmatched deposit for investigation with an owner and current status | Clear or carry forward exceptions with notes |

| Why it matters | Catch missing payments, bad status, and edge cases while the trail is still easy to follow | Issues that survive the close tend to come back later in reminders, tax prep, or client conversations |

Use two cadences. The weekly pass is for early detection. Confirm that invoices were sent, statuses are current, and overdue items have a logged next action. Compare expected receipts with credited and held funds, then flag any mismatch or unmatched deposit for investigation with an owner and current status. This does not need to be elaborate. A short, disciplined review beats a heroic cleanup weeks later.

The weekly pass also keeps exceptions from hardening into assumptions. An invoice that looked merely slow last week can quietly become overdue if no one updates the record. A deposit that appears to match an invoice by amount can still be wrong if the provider deducted a fee, held part of the payout, or applied the payment to a different reference. Weekly review is where you catch those edge cases while the trail is still easy to follow.

Month-end serves a different purpose. This is where you reconcile ledger entries so income and expenses match bank or provider records. Review transactions, journals, and reports together, then clear open exceptions before new billing starts. If an issue survives the close, it tends to come back later in reminders, tax prep, or client conversations, usually at the least convenient time.

At month-end, work in a fixed order. First confirm open invoices and their status. Then compare bank or provider activity to the ledger. Then review lane transfers and tax-reserve movements. Finally, clear or carry forward exceptions with notes. This makes the close easier to repeat because you are checking the same sequence every month rather than improvising based on what feels urgent.

In both reviews, watch for duplicated retries, stale status assumptions, and deposits that do not map back to an invoice. Those look small, but they are usually where preventable errors first show up. The value of this routine is not just cleaner books. It is quicker decisions because you can see what changed before the month gets away from you.

Once that routine is reliable, setting money aside for taxes stops feeling like guesswork and becomes a simple transfer with a verification step.

Save for taxes with an evidence-first habit#

The safest tax habit is simple: move the money when each payment lands, and keep the supporting records current while the details are still fresh.

| Record | When relevant | Handling note |

|---|---|---|

| 1099 records | Where relevant | Keep current in a live tax record file throughout the year |

| W-8 forms | Where relevant | Keep current in a live tax record file throughout the year |

| W-9 forms | Where relevant | Keep current in a live tax record file throughout the year |

| Deductible expense logs | Throughout the year | Keep current in a live tax record file throughout the year |

| Short jurisdiction notes | For edge cases | Keep them so you can remember why a payment or expense was handled a certain way |

Treat your tax reserve as restricted cash. Transfer a set allocation from each paid invoice into that reserve on receipt day and do not treat it as operating money. In a tight month, that can feel restrictive. It is still far safer than discovering you owe tax on paper without cash set aside to cover it. A reserve only works if you actually leave it alone.

Keep a live tax record file throughout the year. For many freelancers, that means 1099 records, W-8 or W-9 forms where relevant, deductible expense logs, and short jurisdiction notes for edge cases. The goal is not identical paperwork for every situation. It is being able to explain each tax position clearly, with documents attached to the right invoice or transaction. Those records matter most when something changes mid-year and you need to remember why a payment or expense was handled a certain way.

The evidence-first part matters because memory fades faster than people expect. If you wait until filing season to rebuild why a payment was classified a certain way or why an expense was treated as deductible, you are doing the hardest version of the work. If you attach the supporting record while the transaction is fresh, later review becomes a verification exercise instead of a reconstruction exercise.

If you have financial interest in, or signature authority over, foreign financial accounts, track FBAR exposure early. A U.S. person generally must file an FBAR when aggregate foreign account value exceeds $10,000 at any time during the calendar year, and FBAR must be filed electronically through the BSA E-Filing System. For most people with an FBAR obligation, the due date is April 15, 2026, with an automatic extension to October 15. For certain people with signature authority but no financial interest, FinCEN extended the due date to April 15, 2027.

Before you close the books each month, run one verification checkpoint:

- Compare tax reserve balance with booked taxable income assumptions.

- Adjust for open receivables so unpaid invoices are not treated as cash.

- Confirm the record file is complete for the month, including new 1099, W-8, or W-9 records where relevant.

- Flag any foreign account balance that may have crossed the $10,000 FBAR threshold.

If any item fails, log the exception, assign an owner, and resolve it before the next cycle. That discipline matters because retirement planning only becomes real once the tax reserve is consistently funded and the cash is actually there. For a simple allocation method, see How Much Should a Freelancer Save for Taxes? A Simple Formula.

Choose retirement based on income pattern, not hype#

Do not let retirement planning outrun your cash reality. Make this decision only after your tax reserve and emergency buffer are stable enough to survive a weak month.

At that point, compare Solo 401(k) and SEP IRA against how your income actually arrives. A Solo 401(k) allows both employer and employee contributions, which gives you more room to structure deposits across strong and weak months. It also allows traditional pre-tax or Roth contributions. Stated total Solo 401(k) limits are $69,000 for 2024 and $70,000 for 2025, with catch-up contributions for people over 50.

SEP IRA is also a valid option. Neither plan is universally better. The practical rule is simpler than most marketing makes it sound: if your income swings sharply, favor the setup that preserves cash flexibility while still letting you contribute consistently. The plan should fit the way cash moves through your year, not the way a comparison page says it should.

In practice, a steady base contribution works better than ambitious promises. Set an amount you can sustain in weaker months, then add top-ups only after reserve targets are funded. That keeps retirement saving connected to actual cash, not to one unusually good month.

A useful comparison is not just which plan looks bigger on paper, but which contribution rhythm you will still follow after a slow client month, a delayed payout, or an unexpected reserve transfer. The right plan tends to be the one you can keep using without raiding the tax reserve or pretending a temporary cash spike is permanent income.

Use this monthly checkpoint:

- Confirm tax reserve and emergency buffer thresholds before retirement transfers.

- Review recent income variance and adjust contribution size if needed.

- Log each contribution decision with amount, date, and reason.

- Recheck plan fit quarterly, not just at year end.

The red flag is easy to spot: a big commitment after one strong month, followed by a retreat as soon as receivables slow. Emergency savings are often thinner than people assume, so keep contributions steady first and scale only after the buffer stays durable. If clients or accounts cross borders, add compliance timing to that cash picture before you assume funds are really available.

Prepare for cross-border and compliance friction before it happens#

If money crosses borders, assume extra checks, more documents, and slower cash timing. That is normal, not an exception.

Cross-border payments are harder to manage because currency conversion, multiple institutions, and different regulatory jurisdictions can all affect what arrives and when. In practice, funds may land on different days with varying fees, and it can take real time to trace movement across time zones if the record trail is thin. None of that is unusual, which is exactly why you should plan for it instead of treating it as a surprise.

When a client, payer, or payout destination sits outside your home country, plan for KYC, KYB, and AML gates that can affect timing and documentation. Before you sign terms, confirm in writing who the legal payer is and how VAT is handled on invoices and payouts. International payment cycles also raise recurring questions about classification, withholding, and local labor rules, so settle ownership early and keep that answer tied to the client record.

The goal is not to predict every possible issue. It is to remove preventable ambiguity before money moves. If a payout is reviewed, returned, or delayed, the fastest cases to resolve are usually the ones where the invoice, contract or SOW, payer identity, and tax form already match across the record. The slow cases are the ones where the amount is right but the supporting trail is thin.

Treat holds and returns as expected scenarios. Set the response path before you need it:

- Assign one investigation owner and one backup.

- Define the minimum support file: invoice, contract or SOW, payment confirmation, payout status, and required tax form.

- Set a clear decision point for pausing new work if a hold stays unresolved beyond your tolerance window.

- Log each status change with date, amount, provider reference, and next action.

If you use multiple providers, map the full flow from collection to conversion to payout so traceability survives end to end. When visibility breaks at any step, fix tracking before you scale volume. Even a simple flow map is useful if it shows where money entered, where it was converted or routed, and where the final payout should appear. With that layer in place, the recurring questions during monthly operations become much easier to answer.

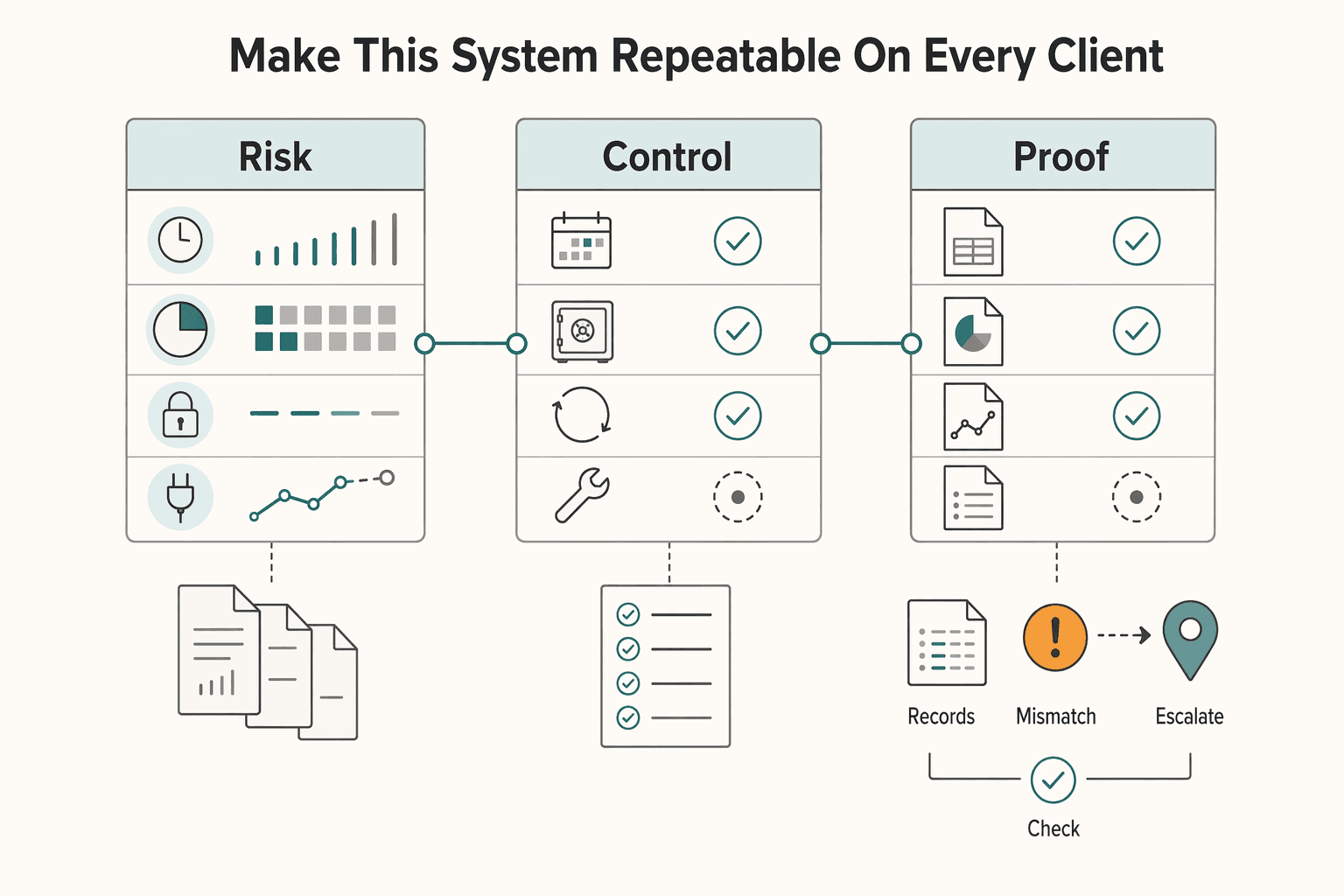

Make this system repeatable on every client#

Repeatability matters more than sophistication. The goal is one operating habit you can run even when work is busy, not a finance setup that only works when you have time to babysit it.

Keep priorities in the same order every time: payment reliability, tax readiness, retirement consistency, then tooling upgrades. Do not add new tools until weekly review issues and month-end exceptions are being documented and cleared in a controlled way. That same sequence, terms, lanes, review, reserve, and exception handling, is what makes the process portable from one client to the next.

Then apply the same rhythm to every client. Before work starts, confirm billing terms, required records, and any program- or market-specific compliance checks. Each week, compare expected and actual receipts, flag overdue invoices, and assign one owner, next action, and due date for every exception. At month-end, reconcile records, clear stale issues, and log any carry-forward risk that still needs attention.

If you work with several clients at once, consistency matters even more than detail. Use the same invoice log fields, the same support-file standard, and the same review sequence across all of them. That way a busy week does not force you to remember different rules for different accounts. Standardization is what keeps the process manageable when volume rises.

Automate repetitive steps only after the basic process is working. Proposal templates, reminders, and routine status updates are good candidates because they remove repetitive work without hiding important exceptions. Keep client, project, and deliverable details in one project management tool so status stays visible and deadlines are easier to protect.

The common failure mode is tool sprawl before process discipline. Start simple: document your current process, fix the weakest checkpoint this week, then layer in tools as volume justifies it.

Frequently Asked Questions

How do freelancers manage irregular income month to month without constantly guessing?

Use a written budget covering operational, marketing, and financial goals, then review it on a fixed monthly date. Move each payment into clear lanes immediately so spending decisions are not made from one mixed balance. Keep a short monthly variance note on what changed and what you will adjust next.

How much should a freelancer set aside for taxes from each payment?

Set a consistent tax allocation rule and transfer that amount as income lands. The exact percentage depends on your facts, so confirm it with a qualified tax professional instead of copying a generic number. If you need a practical method, start with How Much Should a Freelancer Save for Taxes? A Simple Formula.

What is the minimum account structure for freelance financial management?

Keep at least one separate business bank account for inflows and outflows, and consider dedicated tax and reserve balances. Mixing personal and business funds makes income and expense tracking harder. Separation also supports deduction tracking and cleaner record-keeping.

When does Solo 401(k) make more sense than SEP IRA for a freelancer?

Plan choice is case-specific. Review both options with a qualified professional using your current-year cash pattern before deciding.

What should I do first if a client pays late or disputes an invoice?

Verify records before escalating: invoice terms, delivery proof, payment status, and contact history. Then send a short written notice with amount due, supporting documents, and response deadline. If risk keeps growing, pause new work until the account is current.

Which tax documents do freelancers usually need to collect and keep current?

Keep business books that show gross income, deductions, and credits, plus supporting receipts and transaction records. Apply the same standard to electronic and paper records. Maintain any client- or platform-required tax forms and keep them current.

How do compliance checks like KYC or AML affect payout timing?

Payout timing can vary when a payment provider requests additional compliance review. Reduce avoidable delays by keeping legal entity and billing details accurate and maintaining complete records for any hold review. Protect cashflow with reserve coverage.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Much Should a Freelancer Save for Taxes? A Monthly Reserve Rule and Quarterly True-Ups

Use one monthly reserve rule, then adjust it with your actual filings and estimated-payment results. If you are asking **how much to save for taxes freelancer** income creates, the practical answer is not one fixed percentage. It is a repeatable process: move money monthly, check it quarterly, and correct course before a shortfall turns into a problem.

The Best Retirement Plans for Self-Employed Individuals

Start with the plan you can actually fund without squeezing the business. Most bad retirement decisions by a self-employed owner do not start with the wrong tax idea. They start with a plan that looks good on paper, then collides with payroll, uneven collections, or a hiring change six months later.

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.