Quick Answer

Start by treating a feie audit as a records-and-calculation review tied to your filed Form 2555. Confirm notice scope, tax year, and deadline, then build a bucketed evidence map for eligibility, income sourcing, tax home facts, and computation support. Keep one qualification lane throughout your file and reconcile any mismatch before sending. If your day count is near the edge or your numbers do not tie cleanly, get professional review before you respond.

You got an FEIE audit notice and need a calm first move#

Treat the notice as a proof and calculation review, not a character judgment. Your job is to slow the process down, read the scope carefully, and respond with records that match what you already filed on Form 2555. You are not trying to guess what the IRS is thinking. You are trying to prove eligibility, support the numbers, and avoid creating new problems in the process.

In many cases, the notice feels broader than the actual task. The practical job is usually to turn the request into a short list of proof questions tied to the filed return: how you qualified, what income the form covers, what period the claim covers, and how the Form 2555 math was built. That framing matters. It keeps you from sending a long personal narrative when the reviewer is really looking for support tied to a few filed positions.

Start from one baseline and keep it in view throughout your response. U.S. citizens and resident aliens abroad are still subject to U.S. income tax laws. According to the IRS FEIE overview and the Form 2555 page, the exclusion can reduce taxable income when you qualify, but excluded income is still reported on the return. Form 2555 is where the exclusion and any housing exclusion or deduction are figured, so many examiner questions trace back to that form.

Use these terms the same way throughout your response.

- Physical Presence Test: physically present in a foreign country or countries for at least 330 full days in a 12-month period.

- Bona Fide Residence Test: bona fide resident of a foreign country or countries for an uninterrupted period that includes an entire tax year.

- Foreign tax home: your tax home must be in a foreign country to claim FEIE-related benefits.

- U.S. abode: a term that may come up in FEIE reviews; if it is central in your case, address it carefully using your specific facts.

Make one early decision before you write anything substantive: pick your qualification lane, then test whether your records actually support it. If day counts are close to the threshold, or your residence story conflicts with travel records, stop there and get tax audit help before you send a partial response. A rushed answer built on shaky support is much harder to fix later.

It also helps to freeze the filed position before you start improving anything. Pull the exact return, the exact Form 2555, and the worksheets or notes used at filing. Then test those materials for consistency. If you rebuild from memory before you know what was actually filed, it becomes much harder to tell the difference between a missing record and a changed assumption.

Do not try to pull a limit number from memory or from random snippets online. IRS materials can differ by year, and even materials for the same year can conflict. Anchor your response to the return year under review and the records behind the filed Form 2555, then confirm details in the Form 2555 instructions. For a deeper dive, read Common and Costly Mistakes to Avoid When Claiming the FEIE and FEIE vs Foreign Tax Credit.

Once you have the filed position pinned down, the next step is to think like the reviewer. That makes the notice easier to answer and keeps the response focused on what actually needs to be proved.

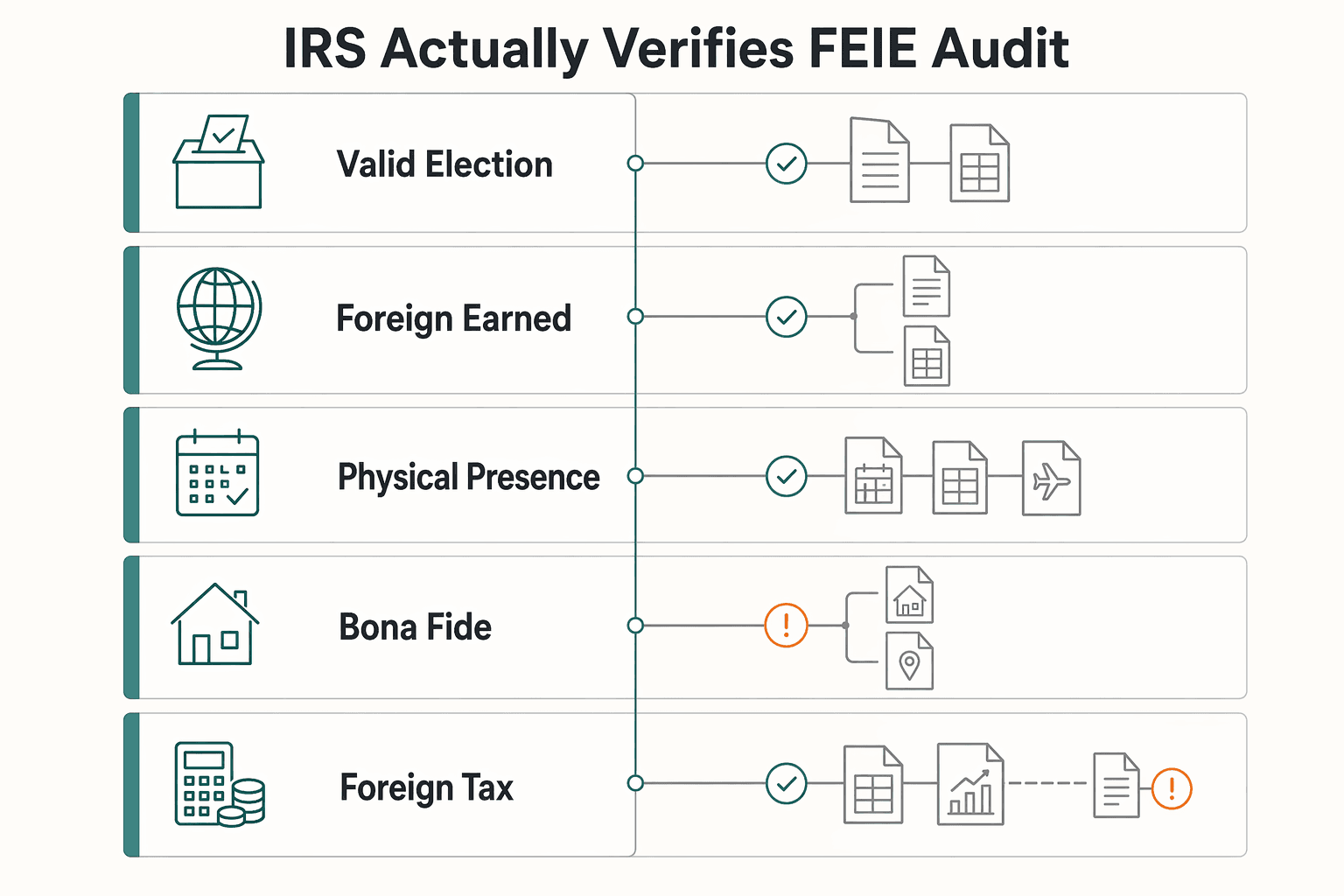

What the IRS actually verifies in an FEIE audit#

This review is usually narrower than it first appears. The IRS is checking whether your Form 2555 election, eligibility, tax home or abode position, and exclusion calculations all match your records. The cleanest response follows the same sequence the examiner is likely using.

| Verification area | What the IRS verifies |

|---|---|

| Valid election | The return shows a valid election for each exclusion item claimed |

| Foreign earned income | The excluded amount qualifies as foreign earned income |

| Physical Presence Test | Your records show you met the Physical Presence Test, if that is your qualification path |

| Bona Fide Residence Test | Your records show you met the Bona Fide Residence Test, if that is your qualification path |

| Foreign tax home / U.S. abode | Your records establish a foreign tax home and support a non-U.S. abode position |

| FEIE computation | The FEIE computation matches filed figures and worksheet inputs, if claimed |

| Housing exclusion or deduction | The housing exclusion or deduction computation matches filed figures, if claimed |

INT-P-222 (an LB&I Process Unit, Foreign Earned Income Exclusion - Audit Techniques) gives practical examiner guidance, not binding law. It explicitly says it is not an official pronouncement of law, so use it to structure your packet, then anchor legal positions to the filed return and the IRS instructions for the year at issue. It does not decide your case. However, it shows the review lens. Even when your facts need explanation, the packet still has to answer the same verification questions in an organized way.

In practice, the review breaks into seven verification buckets:

- You made a valid election for each exclusion item claimed.

- The excluded amount qualifies as foreign earned income.

- Your records show you met the Physical Presence Test, if that is your qualification path.

- Your records show you met the Bona Fide Residence Test, if that is your qualification path.

- Your records establish a foreign tax home and support a non-U.S. abode position.

- The FEIE computation matches the filed numbers, if claimed.

- The housing exclusion or housing deduction computation matches the filed numbers, if claimed.

In our experience, most weak responses fail because they send plenty of documents without showing which question each document answers. A stronger packet maps each bucket to the relevant Form 2555 line, then to the supporting record, then to the computation behind the filed number. Qualification buckets should point to day-count or residence records. Tax home or abode should point to location and tie facts. Computation buckets should point to the exact worksheet inputs used on the filed return.

Those buckets also depend on each other. Qualification determines the period you are defending. That period drives any day-based adjustment and part-year calculation. If housing was claimed, that computation affects the remaining FEIE room. A response that makes those links visible is much easier to review than one that assumes the examiner will reconstruct the whole chain from scattered attachments.

That is why a line-by-line evidence map matters so much. The reviewer should be able to move from the notice to the relevant Form 2555 line, then to the support, then to the calculation file, without guessing why a document is there. If one record supports more than one point, cross-reference it in the map rather than hoping the overlap will be obvious.

Keep the process guidance in perspective. INT-P-222 shows a last update date of 08/11/20. It is still useful for response structure, but year-specific facts should be checked against the return under review and the IRS FEIE computation guidance for that year. That guidance is published by the IRS for annual use.

With that review sequence in mind, the first 72 hours are less about defending yourself and more about getting control of the file.

First 72 hours after the notice#

In the first 72 hours, resist the urge to draft a big explanation. Your best move is to get control of the facts, the notice, and the records before you explain anything.

| Tracker | Fields to log |

|---|---|

| IRS requests | request text; related bucket; due date; status |

| Documents sent | filename; tax year; date sent; request answered |

| Open issues | missing record; owner; target date; escalation note |

Triage the notice in order. Confirm the scope, list the tax year or years under review, and capture the response deadline shown on the notice. Then pause new edits to any prior Form 2555 workpapers until your facts and filed numbers are reconciled. That pause matters. It prevents a messy situation where internal files start drifting away from what was actually filed.

Keep one response log with three trackers:

IRS requests: request text, related bucket, due date, statusDocuments sent: filename, tax year, date sent, request answeredOpen issues: missing record, owner, target date, escalation note

It sounds simple, but one log solves several common problems at once. It shows what the IRS actually asked for, prevents duplicate or inconsistent replies, and makes it obvious where the real risk sits. Additionally, if you end up needing help, that log lets a professional step in quickly without first sorting through your inbox. A companion process in this IRS response checklist can help you keep the same order.

Your first pass should be administrative and factual, not argumentative. Save the exact notice. Compare the notice language to the filed return before you write any explanation. Then reconcile the few items that drive nearly everything else in the file: the qualification period, the tax home position, and the income totals used in the Form 2555 computation.

Before replying, run one practical checkpoint against the filed return: can you support qualification, income sourcing, and the computations with records? If you are using the Physical Presence Test, make sure your date records support the 330 full days in a 12-month period. For the math, confirm that Form 2555 does not exclude or deduct more than foreign earned income for the year.

If a record is missing, flag the gap directly in your response log and work it as a separate problem. Do not try to solve a missing record with a broader narrative. In these cases, a short, well-mapped reply is usually easier to review than a long explanation that mixes qualification facts, tax home facts, and calculation points into one block of text.

If support is weak in more than one core area, escalate early to a tax professional. The same is true when you can tell the documents exist but the story does not line up cleanly with the filed numbers. In practice, that is often the point where the problem shifts from collection to strategy.

Before you mail or upload anything, read the packet in the order the reviewer will see it: cover index, request-by-request answer, attachments, computation file. That final read is where simple but expensive misalignment usually shows up, such as a narrative using one qualifying period while the worksheet uses another, or an attachment that is helpful but not clearly tied to any request.

Once the notice is under control, the real work begins. You need an evidence pack that mirrors the filed form, not a general archive of your life abroad.

Build the evidence pack that matches Form 2555#

The strongest packet is a Form 2555 reconciliation file. Every filed position should tie to a proof trail and a computation trail, or be flagged internally before you reply. If you cannot trace a line item that way, the packet is not ready yet.

Start with a line-by-line map, then collect files to match it. This is reconciliation, not document accumulation. A solid evidence pack usually has two clear components: a proof file and a math file. The proof file shows why the claim was available and what period and income it covers. The math file shows how the filed numbers were reached from that period. Keeping those roles separate makes the response easier to test and harder to misunderstand. We recommend building this from a Form 2555 documentation checklist.

A practical map can be as simple as this:

- Form line or worksheet input.

- What that line asserts.

- Supporting record.

- Tax year and date span covered.

- Assumption used in the computation file.

That map does more than organize paperwork. It forces you to identify where a number comes from, what period it belongs to, and whether it depends on a spreadsheet assumption rather than a direct figure from a source document. Many response problems begin when a filing assumption was reasonable at the time but was never stated anywhere in the file.

Keep qualification proof aligned to the lane you filed.

- Physical Presence Test: support at least 330 full days in a 12-month period.

- Bona Fide Residence Test: support uninterrupted foreign residence that includes an entire tax year.

From there, sort the packet into a qualification set, a tax-home or abode set, an income set, and a computation set, then connect them through the line-by-line map. That structure keeps the reply from turning into a general document dump. It also makes it easier for you to see where the claim is strong, where it is weak, and where one document is doing work for more than one part of the filing.

Make the map practical rather than formal. For each line or input, note what the record shows, what period it covers, and whether the filed figure depends on a judgment call or assumption. If one travel record supports both the qualifying period and the tax home narrative, note that cross-reference directly. If payroll records support foreign earned income but only for part of the year, make that limitation visible instead of letting the reviewer discover it by accident.

Use a separate computation file to show sequence, inputs, and assumptions. For part-year qualification, show how the maximum exclusion was adjusted for qualifying days. Keep one hard check in view: exclusion and deduction totals cannot exceed foreign earned income for the year. For example, if you claimed housing, show that order clearly because the housing amount affects the remaining FEIE room.

Labeling matters more than people expect. A smaller packet with clear file names and a simple map usually outperforms a larger packet that forces the reviewer to guess what each attachment proves. You are not trying to overwhelm the file with volume. You are trying to remove uncertainty.

Where support is incomplete, say so in your internal working file before you send anything. Missing support is easier to manage when isolated and named. It becomes much harder when it is buried in a packet that looks complete but is not. The same is true for part-year qualification. Your file should make it obvious which dates qualify, which dates do not, and how that boundary feeds the filed calculation.

If you claimed a foreign housing exclusion, compute it first and then show the reduced FEIE capacity in the same file. If housing workpapers sit somewhere else, bring them next to the FEIE math and label the order clearly. The reviewer should not have to infer that housing was figured first and that the FEIE amount was reduced afterward.

Timestamped transaction exports can support income timing and traceability, but they are optional support, not a requirement. What usually matters more is whether your evidence is mapped and whether the packet answers the IRS request directly. Related: Qualifying for the FEIE: Physical Presence and Bona Fide Residence Tests and How to Prepare for an IRS Audit.

At this stage, one thing becomes clear: the center of the file is not the document set itself. It is the qualification lane you are defending, because that lane determines both the story and the period used in the math.

Pick your qualification lane and defend it cleanly#

Consistency wins here. The strongest response is a single, provable story across your Section 911 narrative, Form 2555, and supporting records.

The two lanes are different proof jobs. The Physical Presence Test is day-count heavy: at least 330 full days in foreign countries during a 12-consecutive-month period. The Bona Fide Residence Test is facts-and-continuity heavy: uninterrupted foreign residence that includes an entire tax year. In both lanes, your tax home must be in a foreign country.

| Qualification lane | Core proof point | Typical burden | Usually easier for |

|---|---|---|---|

| Physical Presence Test | At least 330 full days in foreign countries during a 12-consecutive-month period | Precise day counts and travel reconciliation | Frequent-country-hopping consultant with clean travel records |

| Bona Fide Residence Test | Uninterrupted foreign residence including an entire tax year | Residence facts and consistency over time | Long-stay resident operator with stable long-term ties abroad |

| Borderline or mixed facts | Some records support each lane but one lane is not fully coherent | Higher risk unless you reconcile one primary lane before replying | Taxpayer with mixed travel and residence facts needing strategy review |

The best lane is not the one that sounds stronger in the abstract. It is the one your filed Form 2555, your dates, and your tax home position already support most cleanly. That sounds obvious, but many bad responses come from trying to improve the story instead of defending the filed one.

Use a conservative rule when facts are close. If your day count is near the 330-day edge, or your residence timeline looks mixed, get professional review before you respond. Borderline facts are exactly where loose wording or a casual assumption can do the most damage.

Do not try to make the reply sound safer by blending both lanes unless the filed return and the records truly support that approach. Mixing them can weaken the packet because the proof standards are different. A reviewer reading a Physical Presence Test story will expect precise day-count support. A reviewer reading a Bona Fide Residence Test story will expect continuity and consistent foreign residence facts. If your response drifts back and forth between them, you create doubt where none needed to exist.

If you filed using the Physical Presence Test, lead with the qualifying period and the day-count support, then make sure the computation file uses that exact same period. If you filed using the Bona Fide Residence Test, lead with continuity and consistency, then make sure the rest of the packet does not tell a mixed residence story. In either case, avoid loose language in the response letter that sounds different from the lane you are defending.

Before sending anything, run this checkpoint:

- The same lane appears in your Section 911 narrative, Form 2555 entries, and supporting file set.

- Dates in your narrative match dates in your records.

- Your tax home position does not conflict with the rest of the file.

- Computation assumptions use the same qualification period you are defending.

If any item fails, pause and reconcile before replying. Consequently, that pause is usually cheaper than trying to explain away inconsistency after the file has already widened.

Once the lane is settled, the next job is to spot the avoidable inconsistencies that turn a manageable review into a longer and more expensive one.

Red flags that turn manageable reviews into expensive problems#

What drives cost and delay in these cases is usually not one isolated line item. It is ambiguity across forms, calculations, and narrative.

The first red flag is unclear FEIE versus FTC handling in your file. Tax software and preparers should build Form 1116 by income category, and each Form 1116 should have only one category box checked. If your support file does not clearly separate how income was handled, expect the review to get slower and broader. In contrast, a clean Form 1116 category workflow keeps the split reviewable.

A common version of this problem is support that answers the wrong question. A packet may show that foreign income existed and still leave unclear how that income was handled between Form 2555 and any Form 1116 work. When the reviewer has to reverse-engineer that split, the review usually expands because the file no longer looks controlled.

The second red flag is computation drift between workpapers and filed numbers. On Form 2555, housing is figured first and reduces the FEIE room, and you cannot exclude or deduct more than foreign earned income for the year. If spreadsheet assumptions changed after filing but the filed values did not, resolve that before you respond.

This type of drift is especially costly because it can make it look like the facts changed when the real issue is that a worksheet changed. Read every number in the response letter against the filed return and the attached workpapers. If you use revised calculations internally to test the filing, keep those clearly separated from what was actually filed so the packet does not blur the line between review and amendment.

The third red flag is a tax home narrative conflict. Section 911 treatment requires your tax home to be in a foreign country. If that position conflicts with other facts in the file, follow-up requests usually widen quickly because the reviewer now has reason to question the foundation of the claim rather than one specific number.

Use this pre-send checkpoint to catch the most expensive issues before they leave your hands:

- Tie each key Form 2555 line to one worksheet cell and one source document.

- Recompute housing before FEIE and confirm the final exclusion or deduction does not exceed foreign earned income.

- If Form 1116 is included, keep documentation separated by income category.

- Confirm response-letter numbers and period assumptions match the filed return.

If any checkpoint fails, reconcile first. A short delay with aligned records is usually cheaper than extended back-and-forth with a reviewer who now has to guess which facts, periods, or worksheets control. That is the real theme across these red flags: ambiguity compounds.

Because the IRS reads a return as a whole, it is also worth checking nearby filings for contradictions before a narrow review turns into a broader conversation.

Related compliance items that can widen the audit conversation#

Keep this part narrow, but do not ignore it. A review focused on Form 2555 can widen when related filings conflict, even if the original notice says nothing about them.

Taxpayers use Form 2555 to figure the foreign earned income exclusion and housing exclusion or deduction. Related international filings are separate, so the practical move is to keep dates, income figures, and residency or tax-home facts aligned across the full tax-year record. You do not need a giant side analysis here. You need a consistency sweep, and our team usually starts that sweep with this expat filing checklist.

The audit logic is straightforward. According to IRS worldwide-income rules, U.S. taxpayers abroad are still taxed on worldwide income, so the IRS is not only testing whether one FEIE line item looks plausible. It is testing whether the filings for that year tell one coherent story.

That means the reply itself should stay narrow, but it should not contradict the broader return. Review related filings just far enough to confirm that the same year tells the same story everywhere. If dates, income totals, or residency language diverge, fix that before the IRS is the first party to notice.

Use this pre-response check:

- Confirm dates, residence facts, and tax-home narrative are consistent across Form 2555 and related filings.

- Reconcile foreign income totals so return values do not conflict across forms.

- Keep a brief year-specific note on why each related filing was or was not required.

- Review self-employment lines separately each year, including Schedule SE treatment.

That year-specific note is more useful than it sounds. It forces discipline. It makes you state why a related filing appears, why it does not, and whether the same foreign income and residence facts were carried through consistently. The note can stay internal, but it often prevents rushed explanations later.

Self-employment is a common gap because it tends to get folded into the general file and then overlooked. FEIE may reduce income tax exposure, but it does not automatically resolve Schedule SE exposure. Keep that review separate enough that it stays visible.

Once you have done that consistency sweep, the remaining questions are usually practical. The FAQ below addresses the ones that come up most often.

Close the loop with a decision-first response#

Your goal is a response the IRS can verify quickly from your filed return, Form 2555, and supporting records. Most friction comes from gaps between your facts, your Form 2555 entries, and the documents behind them.

Start with eligibility, then show proof. Your file should support foreign earned income, a foreign tax home, and one qualifying path: the Physical Presence Test or the Bona Fide Residence Test. Keep each claim tied to records in your evidence map, and keep the dates and periods consistent from the narrative through the calculations.

Then confirm the computation story. Form 2555 is the claim document used to figure the exclusion and housing amount, and excluded income is still reported on the U.S. return. One common failure point is treating excluded income as though it does not need to be reported at all.

A decision-first response is short on drama and strong on mapping. Lead with the year under review, the qualification lane claimed, the requests being answered, and the attachments that support each point. Then let the records do the work. If something is still being reconciled, identify the gap clearly rather than trying to cover it with extra narrative.

Use this final execution checklist:

- Triage the notice: scope, tax year, deadline.

- Build the evidence map: each key Form 2555 line tied to support.

- Keep one qualification lane across all documents and narrative responses.

- Validate computations against filed values and the year-specific limits used in the return.

- Escalate when facts are borderline or records conflict.

Your response does not need to sound expansive. It needs to sound settled. That means the dates match, the qualification story matches, the computation file matches the filed return, and every attachment has an obvious reason to be there.

Clarity is usually worth more than speed. A brief pause to reconcile dates, day counts, income classification, and file support often reduces follow-up rounds later.

If you want cleaner records before the next cycle, review How to Prepare for an IRS Audit, the freelancer year-end tax prep checklist, and our FEIE planning checklist. If you want to pressure-test the numbers, try the FEIE calculator. If you need a second set of eyes on your facts, talk to Gruv.

Frequently Asked Questions

What does an FEIE audit usually check first?

There is no single first document in every case. Initial review commonly focuses on whether you qualify for FEIE, whether Form 2555 calculations are consistent, and whether the income was reported on the return. If you use the Physical Presence Test, qualifying day counts and the day-based maximum excludable amount are common checks.

What documents should I gather before replying to the IRS?

Start with the filed return, Form 2555, and the worksheets behind each key number. Add records supporting foreign earned income, foreign tax home position, and any qualifying day calculation for the 12 consecutive month window. Keep an index that ties each return line to one supporting document.

Can I claim FEIE and Foreign Tax Credit on the same income?

Do not assume that answer. If Form 1116 is involved, keep category separation clear and get the interaction reviewed before filing or responding.

What should I do if I am close to the Physical Presence Test threshold?

Recompute qualifying days before sending anything. The threshold is at least 330 full days in a 12 consecutive month period, and part year qualification requires a day-based adjustment of the maximum exclusion. If your count is close, get a second review of dates and assumptions.

When should I hire a tax professional instead of responding on my own?

Consider professional help when records do not reconcile across forms, when day counts are borderline, or when FEIE and credit treatment is unclear. Also escalate when you cannot produce a clear link from Form 2555 values to source records.

Does an FEIE audit mean I will also be audited for FBAR or FATCA?

Not automatically. Confirm with a qualified adviser whether an FEIE audit could also prompt FBAR or FATCA review in your situation.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Common FEIE Mistakes That Break Form 2555 Claims

Treat FEIE as a compliance decision, not a shortcut. It can reduce U.S. federal income tax only when you qualify and file correctly, and the bigger mistakes usually start when someone jumps straight to the tax savings before confirming the facts that make the claim possible.

Qualifying for the FEIE with Physical Presence or Bona Fide Residence

Start with one principle: choose the FEIE path you can prove, then keep every filing detail consistent with that choice. If you are weighing the Physical Presence Test for FEIE, treat it as a documentation job first and an optimization question second.

How to Prepare for an IRS Audit

Treat an IRS audit as a records check, not a contest. Your job is to show, item by item, how what you filed ties back to the records behind it.