Quick Answer

Start by separating visa choice from tax residency. For thailand tax for digital nomads, the practical move is to pick a residency path early, track calendar-year presence and remittances every month, and escalate once your facts become mixed. DTV flexibility can change your position during the year, so rely on dated records and written advice instead of end-of-year estimates.

Most Thailand tax mistakes happen before you file#

The most expensive mistakes here happen before anyone opens a tax return. People pick a visa, assume the tax answer comes with it, then try to rebuild the year from scraps after the fact. By then, the damage is usually not one dramatic error. It is a pile of small gaps: an unverified day count, a transfer with no clear purpose note, invoices that do not line up cleanly with payments, and assumptions nobody wrote down when the facts were still fresh.

A lower-risk approach is simpler than most online advice makes it sound. Decide early which direction the year is likely to take, track the few facts that actually matter every month, and escalate as soon as the story starts drifting. That gives you two chances to stay out of trouble: once when you plan the year, and again while you still have time to adjust it.

The key point is that tax exposure follows residency, income type, and remittance behavior. It does not follow whatever label the internet attaches to a visa. "Digital nomad visa" gets used loosely online, but a common route, the Destination Thailand Visa (DTV), is still immigration permission first. It is not a tax conclusion by itself.

Timing is where the risk jumps. DTV is described as a five-year, multiple-entry option launched in July 2024. It also allows stays of up to 180 days per entry, plus a possible 180-day extension. One excerpt says that staying more than 180 days in Thailand in a calendar year on DTV can make you a Thai tax resident. That is the kind of trigger to plan around early, not something to estimate from memory in December.

This article is a decision guide, not a loophole hunt. If your plan depends on probably staying under a threshold, the risk is already higher than it needs to be. One of the most common failure modes is late reconstruction of travel, invoices, and remittances after the dates no longer line up. The thread running through everything below is simple: choose your posture early, test it regularly, and do not assume uncertainty can be cleaned up later.

By the end, you will have:

- A clear fork for choosing a non-resident path or a resident-prep path early in the year.

- A monthly checklist with day-count verification and remittance tracking.

- Clear escalation points for when DIY no longer makes sense.

Keep the working standard simple: decide early, document continuously, and get written advice before uncertainty turns into a bigger problem.

Start with the terms that actually change your tax bill#

Start narrow. You do not need every visa-blog term or social media label. You need the handful of terms that change the answer: tax residency, calendar-year day count, and how remitted foreign-source income is treated.

Tax residency and non-resident status are not interchangeable under Thai income tax. Pick the status you are currently relying on and write down the fact that would force you to revisit it before year-end. That note can be brief, but it should tie your plan to a real trigger instead of a vague intention. If another entry, extension, or longer stay would change the analysis, say that now rather than arguing with yourself later.

The first hard checkpoint is your calendar-year day count. In DTV-focused guidance, staying more than 180 days in a calendar year is described as triggering Thai tax residency. DTV is also described as allowing up to 180 days per entry with a possible additional 180-day extension. That combination is exactly why people drift into trouble. The problem is usually not that they never heard the rule. It is that they assumed they still had room and never verified it against the calendar.

Use one monthly verification routine:

- Update your day-count ledger for the current calendar year.

- Reconcile it with travel evidence you could produce later.

- Flag risk early if your plan depends on a narrow margin under the threshold.

It sounds basic, but it does real work. The useful question each month is not what you remember. It is what you could prove if you had to show your file to someone else.

The other term to pin down early is remittance treatment. The practical point is straightforward: once residency is established, remitted foreign-source income enters the tax discussion. Document transfers into Thailand as they happen, with the purpose and the linked invoice or note that explains them.

Keep VAT questions in a separate lane from your personal residency analysis. Mixing those topics too early usually makes the overall picture harder to read. If your facts include uncertain status, mixed personal and business transfers, or a stay length that keeps changing, that is the point to get written professional advice.

Once you pin these terms down, the next decision is more strategic: which path you are actually building the year around.

Decide your path before you book flights#

Do not let the itinerary lock in before you choose your tax posture. The cleanest plans start with a fork, not a visa search.

If your stay pattern is predictable and genuinely supports a non-resident position, run a lean plan and protect your margin. Keep the day count well controlled, keep proof clean, and treat any unexpected extra time in country as a live risk, not a small inconvenience. If your stay pattern is uncertain, the safer move is the resident-prep path. Document the year as if residency could apply, so you are not scrambling later to explain payments, transfers, and where work was performed. In practice, that means tighter remittance tracking and a clearer map between work, invoices, and payments from the start.

This is less about predicting the year perfectly and more about deciding which mistakes you are unwilling to make. A non-resident path fails when you drift over a line you were only half tracking. A resident-prep path costs more effort up front, but it usually leaves you with a file that still works if plans change.

Plan visas and tax in parallel. For extended stays, you will need a Thai visa, and longer-stay options can reduce constant reapplication. What they do not do is settle your tax status for you. That answer still turns on days, income flow, and what money moved into Thailand.

A practical quarterly checkpoint keeps this from turning into a year-end cleanup exercise:

- Day-count review: keep a running day log and reconcile it with travel records.

- Income-flow review: track where work was performed and how invoices were paid.

- Remittance review: record transfers into Thailand with the purpose and supporting documents.

Quarterly is frequent enough to catch drift while you can still change travel plans or tighten the file. If your whole position depends on probably staying under a threshold, treat that as a warning sign, not a plan. That becomes easier to act on once you separate immigration permission from tax liability.

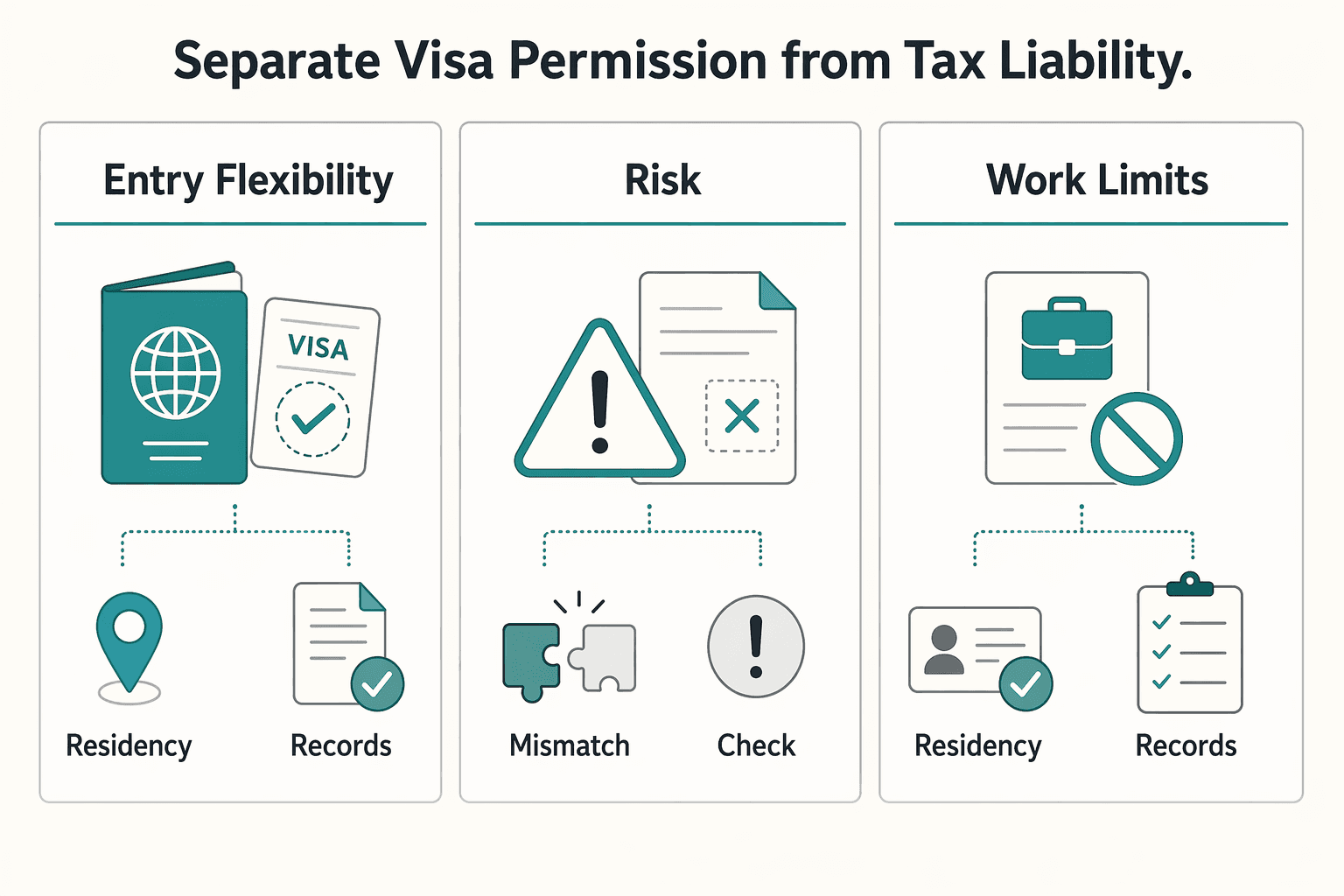

Separate visa permission from tax liability#

A visa can solve an immigration problem without solving a tax problem. Missing that distinction is what turns a manageable year into a messy one.

| Factor | Practical point | Impact |

|---|---|---|

| Entry flexibility | A visa that makes extra time in country easy | It can also make it easy to miss the tax impact until late in the year |

| Stay structure | The route naturally pushes you toward longer in-country stretches | Residency risk rises with it |

| Work limits | Assumed work permissions may not hold for your visa type | It is a separate issue you do not want tangled into the tax file |

Whether you are looking at DTV, the loose "digital nomad visa" label people use online, or the Thailand Long-Term Resident (LTR) Visa, treat them as immigration routes first. The tax risk comes from your actual stay pattern, not the name on the permission. That is why visa research and tax planning have to sit side by side.

DTV is a good example. It is described as a five-year, multiple-entry visa with up to 180 days per entry and a possible additional 180-day extension. One advisory source says more than 180 days in a calendar year on DTV makes you a Thai tax resident, while another says stays over six months may lead to residency and filing obligations. Read both as risk signals. Do not treat either one as a substitute for looking at your own facts.

Before you choose a route, check three things that tend to change the analysis in practice. First, entry flexibility. A visa that makes extra time in country easy can also make it easy to miss the tax impact until late in the year. Second, stay structure. If the route naturally pushes you toward longer in-country stretches, residency risk rises with it. Third, work limits. If you are assuming work permissions that may not hold for your visa type, that is a separate issue you do not want tangled into the tax file.

A good operating rule is simple: if your visa plan makes a longer timeline in Thailand likely, run Thai income tax analysis early. Then recheck quarterly against cumulative days in Thailand, income and payment flow, and remittances into Thailand. This keeps the tax answer tied to facts instead of wishful labeling.

The common failure mode is convenience-driven extensions with weak records. A stay gets extended, another entry gets used, and nobody updates the file until the year is already fixed. This is why a quarterly evidence pack matters. Keep travel records, extension documents, invoice logs, and remittance notes together. If the facts no longer support a non-resident position, escalate before your next booking cycle rather than after it.

If you are comparing longer-stay routes, Thailand's Long-Term Resident (LTR) Visa for Professionals is a useful companion read.

Once visa and tax are separated, the next question is how to handle the parts of the picture that still feel unsettled.

Handle post-2024 uncertainty without guesswork#

Post-2024 uncertainty is real, but it does not justify guesswork. The right response is a position you can support from your file.

DTV launched in July 2024 and is presented as a flexible long-stay option, with up to 180 days per entry and a possible additional 180-day extension. That flexibility can change your fact pattern during the year. A file that looked fine earlier can stop matching the facts by year-end if the stay runs longer, the transfer pattern changes, or home-country assumptions start doing more work than the records can support. The answer is not to sound more certain. It is to be more precise about what you know, what you do not know, and what needs evidence now.

Use a simple knowns-versus-unknowns table to force that discipline:

| Topic | What is known from your file | What is still unclear | Action now |

|---|---|---|---|

| Time in Thailand | Entry dates, exits, extensions, total days | Whether your current pattern changes residency analysis | Reconcile travel records monthly and before year-end |

| Income profile | Client country, invoice dates, payment accounts | Which inflows become relevant if facts shift | Tag each payment by source and purpose |

| Remittances into Thailand | Transfer dates, amounts, destination account | How later reinterpretation could affect treatment | Keep bank proofs and invoice links for each transfer |

| Home-country overlay | Filing status and major elections | Whether relief assumptions still hold | Get written cross-border advice before filing season |

The value of this exercise is simple: it separates what is in the file from what is only in your head. If a key item stays in the unclear column month after month, that is usually a sign you need advice, not more optimism.

There is also a real tradeoff here. A more aggressive interpretation may reduce tax now, but it can increase audit and penalty risk later if guidance tightens or your facts drift. For most people in this situation, a defensible answer is better than a clever one. You can still make reasonable choices. Choose a position you can support, not one that only works if nobody asks follow-up questions.

Before year-end, run one formal review of residency, remittance patterns, and supporting documents. If an important conclusion rests on memory, missing bank proofs, or undocumented assumptions, treat that as an escalation point. The review is there to expose weak spots while you can still fix them, not after the year is already locked.

It only helps if the underlying file is being maintained throughout the year, which is where a monthly documentation habit earns its keep.

Run your documentation system monthly#

Monthly recordkeeping is what makes the rest of this manageable. Good records are not busywork here. They are what turns a reasonable position into one you can actually defend.

| Folder | What to keep |

|---|---|

| Residency tracker | Day count, entry and exit records, extension records |

| Income tracker | Invoice date, client country, service period, payment account, receipt date |

| Remittance tracker | Transfer date, amount, destination account, linked invoice or purpose note |

| Assumptions log | Current residency view, supporting facts, and escalation triggers |

| Advisor notes | Written questions, answers, and unresolved items |

Keep one evidence pack and update it every month. Do it on a fixed monthly cadence so it stays a maintenance task instead of turning into a reconstruction project. At a minimum, that means a travel log for the calendar-year residency test, contract and invoice mapping, and bank-transfer traces tied to income source. Keep each item dated and cross-referenced so the sequence is easy to follow without extra explanation. You do not need fancy software. You need consistency, clear exports, and a file you can hand over without spending a week decoding your own notes.

A simple folder structure like the one above is enough. The aim is not perfect organization for its own sake. The real test is simpler: can any date, amount, or claim in your plan be tied back to something you can produce later? If not, the file is not finished.

This matters because long-stay flexibility can quietly change the tax picture. DTV is described as a five-year, multiple-entry option with up to 180 days per entry plus one 180-day extension, and one advisory source states that more than 180 days in a calendar year can trigger Thai tax residency for DTV holders. Once residency is established, remittance treatment may become relevant, so your day count and transfer records should never be more than a month out of date.

The main failure mode is reconstructing records after the fact. That is where missing transfers, inconsistent dates, and mixed personal and business movements usually show up. If you use financial tools, prioritize exportable ledgers and clear audit trails so the checklist is provable, not just well-intentioned.

With that file in place, you can handle the next layer with much less stress: double-tax exposure and home-country reporting.

Avoid double taxation and US filing traps#

For Americans, the biggest trap is assuming one U.S. rule solves the whole cross-border picture. FEIE can be useful. It is not a complete answer.

U.S. citizens and resident aliens abroad are still taxed on worldwide income, so foreign earnings still have to be reported on a U.S. return. Treat FEIE as a filing position you may qualify for, not an automatic outcome. You need foreign earned income, a foreign tax home, and a qualifying test, for example physical presence for 330 full days in a 12-month period. If you qualify, use Form 2555 to calculate the exclusion and housing adjustment. The provided IRS excerpts conflict on the 2025 FEIE cap, so confirm the current filing-year amount before you file.

The sequencing matters. First, get clear on what happened in Thailand: your day count, the residency posture you can support, and how transfers into Thailand are documented. Then layer the U.S. analysis on top. If you reverse that order and start with FEIE, it becomes easy to miss how the local facts and the U.S. filing position interact.

Double-tax relief also needs separate lanes. Treaty positions, exclusions or credits, and country-specific filing obligations outside Thailand each need their own analysis. One should not be assumed from the existence of another, and each depends on its own facts and records. In practice, the common miss is not the calculation itself. It is assuming one filing position covers a different reporting track.

Use this U.S. compliance check before filing:

- FBAR with FinCEN: confirm whether your foreign accounts require filing.

- FATCA and Form 8938: confirm whether this reporting track applies.

- Schedule SE: check for self-employment tax exposure, even if FEIE reduces income tax.

Use a simple guardrail here: if your plan depends on FEIE alone, add a second review for self-employment and information-reporting exposure. A common miss is getting Form 2555 right while overlooking FBAR or Form 8938. That usually happens because one helpful exclusion gets treated as if it answers every filing question.

Once those U.S. layers sit on top of Thai residency and remittance questions, DIY has a much narrower margin for error. That is the point where you should be honest about whether you still have a simple case.

Know when DIY stops and professional advice starts#

DIY works only while the story stays simple. Once your facts can be read in more than one reasonable way across countries, written advice stops being optional.

Use this as the escalation test. Bring in cross-border tax advice when any of the following show up:

- Tax residency is uncertain.

- Income, filing duties, or planning assumptions span multiple jurisdictions at once.

- Business and personal remittances are mixed and not traceable line by line.

- Your stay pattern changes and you cannot cleanly support non-resident status with records.

- You are relying on verbal interpretations instead of written positions.

Act quickly if your time in Thailand drifts from plan. Visa routes like DTV are described as five-year, multiple-entry arrangements with up to 180 days per entry and an additional 180-day extension, so actual travel can change the analysis during the year, not just at filing time. Waiting until the return is due usually means you are asking an adviser to rebuild the facts and solve the issue at the same time.

When you do engage an adviser, ask for a written position summary that covers Thai income tax, foreign-source income remittance treatment, and home-country filing interactions. If treaty relief is part of your plan, request a separate written note on the treaty logic and what would invalidate that position. A short memo with assumptions and supporting evidence is far more useful later than a casual verbal assurance.

You will get better advice if you hand over a clean file. That means the day log, visa and extension records, invoice map, transfer notes, and your current assumptions should already be in one place. For background, see How to Legally Avoid Double Taxation: A Freelancer's Guide to Tax Treaties.

Conclusion#

The low-stress version of this is not complicated, but it does require discipline. Decide your residency direction early, keep the file current, and escalate as soon as the facts change. That sequence matters more than finding the perfect visa blog post or the most optimistic interpretation.

Visa flexibility and tax exposure move on separate tracks. A Destination Thailand Visa can allow long stays, including 180 days per entry plus one 180-day extension, but that permission does not decide tax outcomes on its own. If your time in country starts drifting upward, rerun the residency analysis immediately instead of hoping the year still works.

When the rules feel unsettled, default to positions you can document. That matters most around how remitted foreign-source income is treated and how home-country filing obligations interact with what happened in Thailand. If guidance conflicts, write down the assumption you are relying on and keep the evidence pack current.

A short monthly checklist is enough to keep control practical:

- Reconcile travel logs to entry and exit proof.

- Match income records to remittances and account movement.

- Confirm filing positions still fit both Thailand and home-country obligations.

- Record changes and flag items that need professional review.

For U.S. taxpayers, keep one extra guardrail in view: worldwide income reporting still applies abroad, and FEIE does not erase every filing duty.

When the facts get mixed, act early. Ask for written guidance that states your likely position, the assumptions underneath it, and the documents that support it. If you want to confirm what is supported for your situation, Talk to Gruv.

Frequently Asked Questions

Do digital nomads pay tax in Thailand?

They can. The outcome depends on your facts, especially stay pattern and tax-residency analysis.

What happens if I stay in Thailand long enough to trigger tax residency?

Your exposure to local tax-residency analysis can increase, and compliance usually gets more complex. Recheck travel records and filing assumptions before year-end.

Does a Destination Thailand Visa (DTV) mean I automatically owe Thai tax?

No. DTV is immigration permission, not an automatic tax outcome. Its long-stay structure can increase the chance that your tax position changes during the year.

If I am American, does Foreign Earned Income Exclusion (FEIE) mean I owe zero tax everywhere?

No. U.S. citizens and resident aliens are taxed on worldwide income, and FEIE does not remove return filing and income reporting duties. It applies only if you qualify, and Form 2555 is used to calculate it.

What records should I keep to prove my tax position?

Keep dated travel evidence, income records, and copies of filed forms in one place. If relevant, keep remittance records, a short assumptions note, and written adviser guidance with your file.

When should I stop DIY and hire a tax professional?

Escalate when residency is unclear, jurisdictions multiply, or personal and business transfers are mixed. Hire help quickly when travel diverges from plan or when filing interpretations conflict.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- taxesforexpats.com/country-guides/thailand/thailand-digital-nom...external

- theprofessionalhobo.com/filing-taxes-as-a-digital-nomad-everything-y...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Thailand's Long-Term Resident (LTR) Visa for Professionals

For a long stay in Thailand, the biggest avoidable risk is doing the right steps in the wrong order. Pick the LTR track first, build the evidence pack that matches it second, and verify live official checkpoints right before every submission or payment. That extra day of discipline usually saves far more time than it costs.

Bangkok Digital Nomad Guide for 2026 Long-Stay Moves

This guide is for remote professionals planning a long stay in Thailand. It puts legal and operational decisions first, then lifestyle choices.

How Freelancers Can Legally Avoid Double Taxation With Tax Treaties

Classify the tax problem before you touch a return. If your income is mostly personal service fees across borders, this guide fits. If your issue is C corporation profits and shareholder dividends, you are solving a different problem.