Quick Answer

Start by filtering each option through legal stay, likely tax residency, and home-country filing duties, then keep only countries you can support with records. For U.S. persons, that includes ongoing IRS reporting, claiming FEIE on Form 2555 when eligible, and using Form 1116 for foreign tax credit treatment where relevant. The safer pick is usually the jurisdiction with clear renewal terms, workable admin load, and evidence you can produce quickly.

Choosing among tax-friendly countries for nomads is easier when you use a three-part fit test: legal stay, likely residency status, and home-country filing duties. The goal is not to chase a move-now, pay-nothing fantasy. It is to reduce guesswork and avoid expensive surprises.

Low-tax marketing can be accurate, but immigration permission and tax treatment are separate decisions. A Digital Nomad Visa is usually a temporary remote-work permit, often around 12 months with extension options, and some places rely on long tourist stays instead of a dedicated nomad visa. Entry rights alone do not settle your tax position.

For globally mobile freelancers and consultants, the usual problem is mixed signals: easy entry, unclear residency triggers, and unfinished filing duties at home. U.S. persons should assume worldwide income reporting still applies and that IRS filing, FBAR, and FATCA can remain in scope while abroad. If your plan starts with moving first and sorting filings later, fix that assumption before you shortlist anything.

This is not a ranked best-countries list. Rankings hide the practical friction that decides whether a move stays low-stress after the first few months. Zero-tax locations can reduce local income tax, but living costs may be higher. Territorial approaches can look attractive, but foreign-income treatment and residency conditions still need a line-by-line check.

Use this sequence before you compare destinations:

- Confirm your legal stay path and timeline, including visa duration and renewal terms.

- Map likely residency exposure in each option, using published day counts as screening inputs, not final legal thresholds.

- Reconcile home-country obligations for the same tax year, including worldwide income reporting where relevant.

- Keep basic documentation from day one in case you need to support immigration or tax compliance.

That order matters because each later decision depends on the one before it. If the stay path is weak, there is no point optimizing for tax. If the residency picture is unclear, there is no point signing a lease or changing banking routines. And if home-country filing duties are still unresolved, any "tax-friendly" label is incomplete by definition.

One early check prevents a lot of rework: compare your intended stay against visa validity before signing a long lease. Tourist permission can range from a couple of weeks to a year, so mismatches happen fast. If the stay plan and the legal-stay window already conflict, the shortlist is wrong before the tax analysis even starts.

What tax-friendly means for nomads#

The useful definition is narrower than most marketing copy. For nomads, tax-friendly means your visa status, residency position, and filing duties can all be defended at the same time. If one of those three is weak, the plan is fragile no matter how good the headline rate looks.

Tax residency is where a country treats you as taxable under its rules. A Digital Nomad Visa is immigration permission, not an automatic tax outcome. Keep those as separate checks, because visa approval alone does not confirm the result you expect.

For U.S. citizens and resident aliens, zero-tax headlines are incomplete because worldwide income taxation still applies. Moving abroad does not automatically remove U.S. filing duties.

Relief tools can reduce double-tax pressure, but they are not automatic. FEIE applies to qualifying foreign earned income from services performed in a foreign country, and you still report that income on your U.S. return and claim FEIE on Form 2555. Under the physical presence test, qualification is time-based: 330 full days in foreign countries during any 12 consecutive months, so long as your tax home is in a foreign country. A full day is 24 consecutive hours from midnight to midnight. Miss the threshold and the test fails, regardless of reason.

The Foreign Tax Credit is separate and is claimed on Form 1116. Filing is category-specific, with one income-category box per Form 1116.

Three recurring myths are worth clearing out early:

| Myth | Reality | Practical check |

|---|---|---|

| Visa approved means tax settled | Visa status and residency status are separate legal checks | Validate your likely position before committing to long stays |

| Zero-tax country means zero U.S. filing | U.S. persons can still have U.S. filing obligations on worldwide income | Map filing obligations before relocation |

| FEIE means no return | FEIE is claimed on Form 2555, and excluded income is still reported | Track your full days abroad against the 330-day, 12-month test |

Think of visa approval, residency status, and filing mechanics as three separate approvals. If one is still unclear, pause there and resolve it before you compare countries. That pause is not lost time. It is the point where you stop treating a destination as a lifestyle idea and start treating it as a compliance setup that has to survive year-end review.

If you want a country-specific example, read this Georgia-focused guide.

Set your baseline before comparing countries#

For U.S. filers, this step saves the most backtracking. If you cannot map what you may need to file, comparing visa and tax headlines is premature.

Start with three checks: U.S. return status, FATCA reporting through Form 8938, and FBAR filing through FinCEN Form 114. Form 8938 is attached to your annual return and is due with that return, including extensions. If you do not have to file an income tax return for the year, you do not file Form 8938. If you do file, confirm whether your specified foreign financial assets exceed the threshold that applies to your filing profile. Thresholds are higher in some cases, including joint filers and taxpayers residing abroad.

| Baseline check | What to verify now | Why this matters before shortlisting |

|---|---|---|

| IRS return filing | Whether you are required to file a U.S. income tax return | It determines whether Form 8938 can apply |

| FATCA and Form 8938 | Whether your specified foreign financial assets exceed your applicable threshold | Missing this creates year-end surprises |

| FBAR and FinCEN Form 114 | Whether any single account or aggregate maximum account value exceeds $10,000 during the calendar year | FBAR may still be required even if you file Form 8938 |

Treat FBAR math as a hard checkpoint. Value each foreign account separately, convert foreign currency using the Treasury Financial Management Service rate for the last day of the calendar year, and round up to the next whole dollar. For example, $15,265.25 becomes $15,266.

Then document your income profile on one page: salary-like compensation, client-invoice freelance income, and business profits. That one page keeps your records cleaner before you start comparing jurisdictions, because you can test each option against the same real income mix instead of a vague idea of how you earn. It also gives you a simple control document when facts change midyear. If a client mix shifts, payouts move, or a business profit stream starts to matter more than service income, update the page so every later country comparison uses the same current baseline.

This is also the right moment to decide what records you will keep as standard practice. If you wait until year-end, you will end up rebuilding account values, payment flows, and travel dates from fragments. If you decide now what statements, confirmations, and exports belong in your file, your later analysis gets faster and cleaner.

If your plan is still "move first, sort filings later," stop and rework it around current U.S. filing and reporting duties. The decision rule is simple: do not shortlist countries until you can name the forms you may need, the thresholds you must monitor, and the records you will keep. Once that baseline is clear, separate immigration approval from tax status before you go any further.

Separate visa approval from tax residency status#

This is where otherwise solid plans break. A visa confirms your right to enter and stay under a program. It does not, by itself, confirm where and how you will be taxed.

A Digital Nomad Visa is generally a temporary permit for remote work while living abroad. Program length varies: some are around 12 months with possible extension, while others are often in the 6 to 12 month range, sometimes longer. That matters because your tax-year plan can easily outlast the permission that got you into the country.

Across labels such as Remote Work Visa, Golden Visa, Freelance Permit, and Rentista Visa, do not assume the name tells you the tax result. Your filing position still needs separate validation.

Before you commit, run this checkpoint:

- Confirm the validity window with exact start and end dates.

- Confirm whether renewal is available and how clearly the rules are defined.

- Confirm stay-pattern fit so your planned presence matches the duration you can actually hold.

- Confirm work-permission fit, because tourist status can restrict work activities.

- Keep dated proof of approval terms and validity dates.

A common failure mode is optimizing for easy approval and discovering later that the visa timeline does not support your intended presence. If the permit term is shorter than your tax-year plan, treat that option as high friction unless extension terms are clear. Another common miss is assuming that an approved remote-work route answers local tax questions automatically. It does not. You still need a separate note that explains how you think your tax position works and what facts would cause that view to change.

Once you have separated entry rights from tax status, you can compare destination lanes on the right terms.

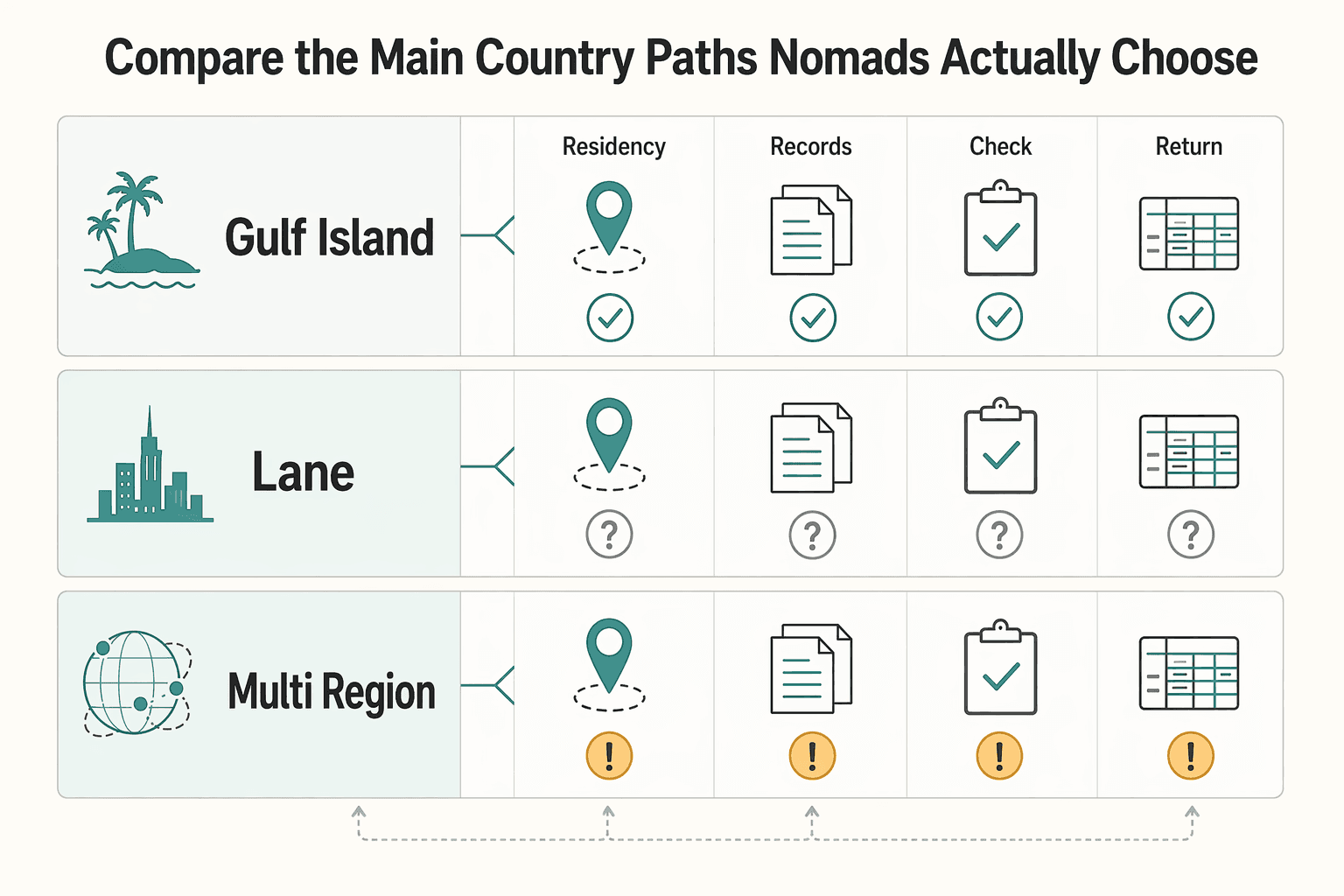

Compare the main country paths nomads actually choose#

After you separate immigration from tax status, compare country paths by ongoing compliance load, not by branding. The safer choice is usually the one you can explain clearly at filing time with documents ready.

| Common shortlist lane | Example countries in that lane | First checks before keeping it on your list |

|---|---|---|

| Gulf and island lane | United Arab Emirates (UAE), Qatar, Bahrain, Cayman Islands | Confirm legal-stay continuity, renewal evidence, banking onboarding requirements, and filing obligations at home and abroad |

| EU lane | Greece, Spain, Italy | Confirm VAT handling for cross-border sales, local return obligations, and whether your filing calendar is realistic |

| Multi-region alternative lane | Estonia, Costa Rica, Georgia, Panama | Confirm residency-process clarity, documentation burden, account setup practicality, and renewal predictability |

Use one scoring lens across all lanes so you compare like for like. Start with admin load and documentation demands, then mark treaty support, banking practicality, and renewal predictability as unknown until you verify them separately. That keeps early comparisons honest. Too many shortlists collapse because you end up judging one country on marketing and another on paperwork.

For EU-leaning options, VAT is a concrete friction point. Since 1 July 2021, EU cross-border B2C e-commerce VAT rules changed and use an EU-wide EUR 10,000 threshold. If you use One Stop Shop (OSS), you register in one Member State of identification and declare all supplies covered by that scheme through OSS. OSS returns are additional and do not replace your regular VAT return.

Filing cadence matters too: non-Union and Union OSS schemes are quarterly, while the import scheme is monthly. For complex cross-border VAT questions, VAT Cross-border Rulings can provide advance treatment, but requests must be filed in a participating EU country where you are VAT-registered and under that country's national VAT-ruling conditions. Estonia, Spain, and Italy are among participating countries.

The practical takeaway is straightforward: prefer paths where legal status, filing treatment, and documentation demands are all understandable before you move. Any universal ranking falls apart if it skips compliance workload and ongoing friction. Treat personal income-tax rates, day-count thresholds, and definitive rankings as unknown until separately verified.

A useful way to compare these lanes is to ask the same operational questions for each one: What has to be filed, what has to be renewed, what has to be proved, and what happens if timing slips? That framing keeps the comparison grounded in execution rather than marketing language. From here, a scorecard helps you turn a broad comparison into a real decision.

Related: Dubai, UAE: The Ultimate Digital Nomad Guide (2025).

Use a shortlisting scorecard before you commit#

A shortlist becomes useful only when you judge every finalist the same way. Use a weighted scorecard and pick the option you can defend at filing time, not the one with the lowest advertised rate. Set the weights once, score every finalist the same way, then apply red-line rules that can remove a country immediately.

Use five criteria: residency certainty, tax mechanism fit, admin load, cost friction, and audit defensibility. Score each country on how tax treatment and reporting would work for your actual income pattern, because headline rates do not show full compliance risk.

| Criterion | What to verify | Evidence to store | Red-line trigger |

|---|---|---|---|

| Residency certainty | Visa fit for planned presence, including minimum income threshold, duration, and eligibility criteria | One-page country note plus requirement snapshots | Permit timing does not fit your tax-year plan |

| Tax mechanism fit | What income is taxed, under what conditions, and what reporting is required | Tax-mechanism note for your income mix | Core tax treatment or reporting obligations are still unclear |

| Admin load | Required reporting and filing workload for your setup | Reporting checklist and filing calendar | Required reporting cannot be maintained reliably |

| Cost friction | Quality-adjusted cost: internet reliability, coworking access, safety, and healthcare | Scored checklist plus budget assumptions | Low cost but clear productivity drag from weak infrastructure |

| Audit defensibility | Ability to produce dated records for status, income, and filings | Evidence folder map and retention plan | Missing core records needed at filing or review |

Residency certainty and tax-mechanism fit are pass-fail gates. If you cannot explain how income is taxed and reported in plain language, the option is not ready no matter how attractive the tax headline looks.

Timing matters too. A permit that expires in the middle of your planned tax year can create avoidable admin churn, so do not ignore validity dates just because the application path looks simple.

If you are a U.S. citizen, keep home-country exposure explicit for every finalist because relocation does not end filing duties by itself. If FEIE is part of the plan, log the applicable annual limit and verify current guidance before filing.

The scorecard works best when you write short notes beside the numbers. A country that looks strong on cost but weak on documentation should not survive just because the total score still looks decent. The notes are what stop you from talking yourself into a choice that only works on paper. They also make it easier to revisit the shortlist later if rules, timing, or your own income mix changes.

Decision rule: choose the option with fewer irreversible compliance risks. If documentation readiness or infrastructure reliability fails your test, remove that country even if the headline rate looks better.

Before you lock a country, run your finalists through a residency-timing sanity check with the Tax Residency Tracker. Then test the surviving options against dual-residency risk.

Prevent dual-residency collisions and treaty surprises#

A strong shortlist can still fail if your calendar creates two plausible tax homes. Usually this starts as a timing and documentation problem long before it becomes a filing problem, which is why you need to address it before you commit.

A Digital Nomad Visa gives immigration permission to work remotely while living abroad, and some programs market longer stays or local-tax relief. It does not automatically establish foreign tax residency or resolve double-taxation exposure. With many programs running about 6 to 12 months and immigration rules changing quickly, split-year moves can create avoidable ambiguity if you do not map them in advance.

This is the checkpoint that matters most:

- Build a month-by-month presence plan for the next tax year, then test it against visa duration.

- Treat treaty, substance, and exit-tax issues as jurisdiction-specific questions to verify with qualified advice before you move.

- Reconfirm official immigration requirements right before travel.

- Keep proof documents ready for applications or border checks, since decisions can depend on what you can prove on the spot.

The month-by-month plan matters because border stamps, lease dates, renewal timing, and year-end filings all tell parts of the same story. If those pieces do not line up, the problem is rarely fixed by calling the country "tax-friendly." You fix it by reducing ambiguity before the move, not by trying to explain it away after the year closes.

Tax planning only works when the program, your income profile, and your actual movement pattern fit the same story. If your jurisdiction-specific position cannot be explained clearly and supported with records, pause and get professional advice before you move. The only reliable way to defend that plan later is to build the evidence pack before departure.

Build your evidence pack before you relocate#

Once the calendar looks defensible, turn it into paperwork. Your move is only as defensible as the dated records behind it. If you cannot produce a record quickly, treat the claim as weak and fix it before relocation.

Build one evidence pack and keep it current before departure:

| Proof category | What to keep in the file | Why it matters |

|---|---|---|

| Physical presence day log | Entry and exit dates with tickets, stamps, or equivalent records | Supports 330-day counting positions |

| FEIE workpapers (Form 2555) | Eligibility notes, qualifying-day calculations, and Form 2555 support | Supports your FEIE position |

| Foreign housing exclusion workpapers | Housing expense calculations and exclusion ordering notes | Supports housing exclusion and FEIE interaction |

| Foreign Tax Credit workpapers (Form 1116) | Separate Form 1116 support by income category, with country or territory detail where needed | Supports FTC treatment across jurisdictions |

For U.S. filings, build FEIE and related support before you leave, not after the year closes:

- Track physical presence days with precision: 330 full days in any 12 consecutive months, with a full day counted as 24 consecutive hours from midnight to midnight.

- The 330 days do not need to be consecutive, but missing the threshold fails the physical presence test even for personal or employer-driven disruptions.

- Keep FEIE scoped correctly: you still file a U.S. return and report income, then claim FEIE on Form 2555 if eligible.

- Limit FEIE assumptions to foreign earned income from services performed in a foreign country. If qualification is only part-year, adjust by qualifying days.

- For 2026 planning, use the FEIE maximum of $132,900 per qualifying person.

If you claim the Foreign Housing Exclusion, calculate it first because it reduces FEIE available. The general housing expense limitation is 30% of the FEIE maximum, and the stated 2026 housing amount limitation is $39,870.

For the Foreign Tax Credit, prepare Form 1116 by income category, and separate country or territory entries clearly when taxes were paid to more than one jurisdiction.

For Gruv users, keep invoice, payout, and ledger-linked exports organized for reconciliation so cross-border income trails are reviewable without manual reconstruction. A simple structure is enough if it is consistent: keep travel evidence with travel evidence, tax workpapers with tax workpapers, and filing support with filing support. The important part is that your records are contemporaneous and easy to match. When a date in your day log lines up with a ticket, a permit issue date, and the related payment trail, later filing work gets much easier.

With the records in place, the first 90 days become an order-of-operations problem instead of a scramble.

Execute your first 90 days in the right order#

The sequence matters more than speed. In the first 90 days, the conservative move is to secure legal stay and core documentation before changing financial operations. Treat this as an internal control you adapt by country, not a universal legal rule.

| Phase | Priority action | Check before moving on | Common miss |

|---|---|---|---|

| Days 1-15 | Secure legal stay with a status that allows remote work | Confirm permit terms support your real work setup and are not tourist terms that restrict work | Treating entry permission as tax residency |

| Days 15-45 | Complete permit-related steps and any required local registrations | Save dated confirmations, receipts, and issued IDs | Locking long housing before core paperwork is accepted |

| Days 30-60 | If needed, open banking rails that match your current documents | Ensure identity and address records align across account setup documents | Opening accounts with incomplete document trails |

| Days 45-90 | Tune invoicing and payout routines | Match invoice entity, payout destination, and ledger records to issued documentation | Rerouting client payments before paperwork is stable |

Country requirements, income thresholds, and fees can change, so verify official criteria right before each submission. That single habit prevents a lot of avoidable rework.

Before you commit to longer housing in UAE, Greece, Spain, Costa Rica, or any other finalist, run a quick country-fit check:

- Recheck current official visa requirements and fees at application time.

- Confirm work-eligibility language matches your income model, including foreign clients or employers where required.

- Confirm insurance and financial-proof documents are valid for the full intended stay.

- Confirm how that permit path is treated for tax, since outcomes differ by country and visa approval alone does not establish tax residency.

Many digital nomad permits run around 6 to 12 months, often with extensions, and usually include eligibility checks such as remote-income conditions and private health insurance for the full stay.

The hidden risk in this phase is changing too many systems at once. If you reroute client payments, switch account details, and sign long housing before permit and identity records are fully aligned, you create extra points of failure for no real gain. Slow, staged changes are usually easier to document and easier to explain later.

Decision rule: delay optimization moves until identity, address, and tax-profile documentation are fully aligned and dated. If one layer is unresolved, pause and fix it before moving to the next phase. That discipline pays off when you reach year-end filing.

Run a year-end compliance checklist and escalation rules#

Year-end is where earlier shortcuts show up. File only positions you can support with complete records. Reconcile what actually happened before finalizing any filing position, and pause any optimization idea if the documentation trail is incomplete.

| Checklist item | What to verify now | Escalate if |

|---|---|---|

| Form 8938 filing test | Confirm whether you must file an income tax return and whether your specified foreign financial assets exceed the applicable Form 8938 threshold | Return-filing status is unclear, or your threshold test is incomplete |

| FBAR maximum-value test | Calculate each account's maximum value and the aggregate maximum for the calendar year; use periodic statements when they fairly reflect the maximum | Account values conflict, key statements are missing, or totals cannot be determined |

| Filing calendar | Track each return and attachment to its due date, including extensions where allowed | A required filing is not mapped to a filing event |

| Evidence-pack completeness | Confirm you can produce source documents for each filing claim | Core account or tax records are incomplete |

For U.S. foreign-asset reporting reviews, run IRS and FBAR or FATCA checks as separate controls:

- Form 8938 is attached to your annual return and filed by that return's due date, including extensions.

- Filing Form 8938 does not replace FBAR when FBAR is otherwise required.

- If you are not required to file an income tax return for the year, you do not file Form 8938 for that year.

Use thresholds carefully and document your test:

- FBAR is required if a single-account maximum or aggregate maximum exceeds $10,000 during the calendar year.

- Form 8938 reporting can apply when specified foreign financial assets exceed $50,000 in aggregate, with higher thresholds for some joint filers or taxpayers residing abroad.

- For specified domestic entities, the referenced threshold is over $50,000 at year-end or over $75,000 at any time during the tax year.

For account-value support, periodic statements may be used for FBAR maximum-value calculations if they fairly reflect the maximum. Record FBAR values in U.S. dollars and round up to the next whole dollar. If totals cannot be determined, use the FBAR amount unknown marker and treat it as an immediate escalation item.

Talk to a pro now if any of these appear:

- You cannot determine whether Form 8938 applies because return-filing status or threshold inputs are unclear.

- You cannot determine FBAR maximum values and need to file with an amount unknown marker.

- Your Form 8938 and FBAR conclusions conflict.

- Missing source documents for account values, asset ownership, or filing inputs.

One useful habit at year-end is to compare your final filing positions against the plan you made before relocation. If the two no longer match, identify why. Sometimes the explanation is harmless, such as a timing shift. Sometimes it signals a real compliance issue that needs review. Either way, you want that gap noticed before filing, not after.

The broad pattern is simple: clean year-end filing depends on decisions you made much earlier. That is why the checklist belongs at the end of the plan, not just at the end of the year.

Conclusion#

The throughline is simple: this is an execution problem, not a ranking problem. A low headline tax rate only works when your visa path, residency position, and documentation all support the same story.

Country choices are not interchangeable. Residency requirements, visa options, and living costs vary, so similar tax headlines can create very different compliance pressure. Territorial tax treatment can help, but it is not a universal exemption. Panama is often attractive because foreign-sourced income is not taxed, yet it is still not fully tax-free.

Documentation is usually the make-or-break point. The UAE is often presented as 0% personal income tax, but digital-nomad routes still require proof, including non-UAE employment evidence and supporting documents such as a contract, recent bank statements, and in some routes income checks. If your proof is weak, treat that as a decision signal, not a paperwork detail.

The costliest mistake is usually not picking the wrong country from a list. It is letting your facts drift into conflict over time, including the 183-day trap that can trigger unintended residency exposure in a higher-tax jurisdiction. Prevention is easier than cleanup.

Use one practical next move this week:

- Run a shortlist scorecard with residency certainty, visa fit, admin load, cost friction, and audit defensibility.

- Build an evidence pack for each finalist with visa records, contract and income proof, and presence documentation.

- Pick the country with the cleanest compliance path, even if another option advertises a lower rate.

If you want a deeper reality check on zero-tax claims, read Living in a No-Tax Country: Is it Really Tax-Free for a US Citizen?. If you use Gruv, keep invoices, payouts, and ledger-linked records traceable across borders so your income trail stays audit-ready where supported.

When you are ready to operationalize the plan with cleaner documentation and payout workflows, talk with Gruv.

Frequently Asked Questions

Do zero-income-tax countries mean zero tax for me?

No. For U.S. taxpayers, claiming FEIE still means filing a return that reports the income. Whether local tax is due depends on local rules, so zero-income-tax labels are not a personal all-clear.

How many days do I need to establish tax residency?

The IRS 330 full days in a 12-consecutive-month window is a FEIE physical presence test, not a global residency rule. Those days do not have to be consecutive, and each counted day is a full 24 hours from midnight to midnight.

Can I be tax resident in two countries at the same time?

If your facts could support more than one filing position, treat it as a high-risk situation and escalate before filing.

What is the difference between a Digital Nomad Visa and Tax Residency?

A Digital Nomad Visa and tax residency should be evaluated separately. Do not assume visa status alone determines tax residency. Keep permit records and tax records aligned so your filing position matches your documented facts.

How do FEIE and the Foreign Tax Credit differ for US citizens abroad?

FEIE excludes qualifying foreign earned income when eligibility tests are met and the income is reported on a return. The Foreign Tax Credit is handled on Form 1116, using a separate form for each income category. If taxes were paid to more than one foreign country or territory, Form 1116 requires separate country lines or columns.

When should I hire a cross-border tax advisor instead of handling it myself?

Escalate when your day count is close, your records are incomplete, or your facts changed midyear. Get help if you cannot confidently support FEIE eligibility or prepare the required Form 1116 category and country breakdowns. If two filing positions seem plausible and you cannot defend one clearly, involve a professional before filing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Georgia 1% Tax for Entrepreneurs Without Filing Surprises

Treat Georgia's 1% tax path as a compliance question first and a rate discussion second. The goal is a setup you can defend under review, not a shortcut that fails at filing time.

Dubai Digital Nomad Guide 2026 for a Practical Move Plan

If this move works for you, it will work because you sequence decisions well and keep risk reversible until your status is clear. Treat this route as a chain of checkpoints, not one giant yes or no decision made under time pressure.

Is a No-Tax Country Really Tax-Free for a US Citizen?

A no-tax destination can lower local income tax, but it does not end U.S. filing and reporting duties. U.S. citizens abroad are still taxed on worldwide income, and tools like the FEIE or Foreign Tax Credit are tied to filing a U.S. return.