Quick Answer

Start by treating taxes in portugal for nomads as a filing-position exercise, not a visa exercise. Draft a short residency memo, test it against your travel, housing, contract, invoice, and address records, and label each assumption as confirmed, assumed, or missing. Use day-count and habitual-home checks as checkpoints, then keep NHR and IFICI in a provisional bucket until eligibility is verified. If two countries could claim you or your records conflict, escalate before filing.

Start Here With the Decision You Actually Need to Make#

Your first decision is not optimization. It is whether you can defend a provisional Portugal filing position with documents, then keep every later choice consistent with that position. Do not mix these terms:

| Term | Meaning in this article |

|---|---|

| Tax residency | Your working view of which country may treat you as resident for tax purposes, pending official or professional confirmation. |

| Immigration status | Your legal permission to enter, stay, or work in a country. |

| Habitual home (plain-language use here) | Where your day-to-day life looks settled in practice. |

A visa can support your story, but do not treat visa status alone as your filing position.

Before you start#

If you are using the D8 Digital Nomad Visa, treat it as an immigration checkpoint, not a tax shortcut. The D8 is commonly described as having been introduced in 2022 for non-EU applicants who meet minimum income and employment requirements. A third-party 2026 index also describes it as renewable for up to 5 years and potentially leading to permanent residency, but that remains third-party summary material, not Portuguese tax-authority guidance. For visa process context, use current government instructions and, if useful, this Portugal Digital Nomad (D8) Visa: A Complete Guide.

Step 1#

Write your residency position before you optimize anything. Draft a 5 to 6 line memo: where you currently think you may be resident this year, why, and which records support that view. Start with facts, such as presence, housing, work pattern, and payer setup, not regime names. Expected outcome: you can explain your base position without relying on NHR, IFICI, or tax-rate assumptions.

Step 2#

Run an evidence-first intake check. Use records you can produce later, not memory.

| Document category | What to collect now | Status |

|---|---|---|

| Travel records | Flight confirmations, passport stamps, border logs, calendar entries | Confirmed / Assumed / Missing |

| Housing records | Lease, hotel invoices, utility bills, rent transfers, host letters | Confirmed / Assumed / Missing |

| Work and income records | Contracts, client statements, invoices, payroll records, payment receipts | Confirmed / Assumed / Missing |

| Identity and immigration records | Passport, visa approval, residence card if issued, application receipts | Confirmed / Assumed / Missing |

| Address trail | Bank address, platform profiles, invoicing address, insurance address | Confirmed / Assumed / Missing |

| Personal ties | Family location, school records, memberships, storage, local subscriptions | Confirmed / Assumed / Missing |

Quick consistency test: your travel, housing, and invoice records should tell the same story.

Step 3#

Label each key point as confirmed, assumed, or missing.

- Confirmed: you have the document now.

- Assumed: you believe it is true but cannot evidence it yet.

- Missing: you know it matters and still lack support.

If your conclusion depends on a residency test or day-count rule, mark the threshold as not yet verified until current authority is in the file.

Step 4#

Treat special regimes as unverified until you can prove eligibility under current official guidance. That includes legacy NHR discussions and current IFICI discussions. Until eligibility is documented for your exact facts, model your position without regime benefits.

Escalate early when the file is not clean. Talk to a Portugal-focused professional if any of these apply:

- Two countries could plausibly claim you.

- Records conflict across leases, invoices, banks, or immigration files.

- Your result depends on an unverified threshold or regime.

- You cannot reconcile your memo and documents in 15 minutes.

Expected outcome: one provisional position, one evidence table, and one short list of items still needing confirmation. If you want a deeper dive, read Lisbon, Portugal: The Ultimate Digital Nomad Guide (2026).

Build the Mental Model Before You Pick a Tax Position#

Once you have a provisional file, make sure you are using the right boxes. Start from evidence, not identity. You are not taxed as a lifestyle label or a visa label, and "tax-friendly" headlines are not a filing position. Build your position from records you can defend: travel pattern, housing continuity, contracts, address trail, and how income is actually administered.

Step 1#

Use core terms as working tools. These labels help you decide what to verify:

- Tax-friendly: a relative label that depends on your facts and how you make money.

- Territorial tax system: commonly means income earned outside the jurisdiction is treated differently from local income.

- Flat tax: a single rate can look simple, but simplicity can come with tradeoffs like fewer deductions, credits, or social-service offsets.

These are working labels, not guarantees. If your records are incomplete or conflicting, your file is still incomplete.

Step 2#

Keep immigration, tax status, and regime eligibility in separate boxes.

| Box | What it answers | What it does not answer | Evidence to check |

|---|---|---|---|

| Immigration status | Can you legally enter, stay, or work? | Your final tax treatment | Visa approval, residence card, application receipts |

| Tax status | What filing position fits your facts? | Whether a visa or headline makes it favorable | Travel log, lease, address trail, contracts |

| Regime eligibility | Whether a special regime may apply | Your base residency position | Eligibility records, application evidence, current rules |

For visa process context, see Portugal Digital Nomad (D8) Visa: A Complete Guide. Keep the guardrail in place: D8 approval can support your file, but it does not settle tax treatment by itself. If your plan depends on repeated tourist-visa stays, treat re-entry and continuity as unresolved risk.

Step 3#

Write a one-paragraph position, then pressure-test it. Draft five to six sentences on where you think you are taxable, why, and which documents support each point. Test every sentence against three lanes: contracts, address history, and income administration.

Mark each point as confirmed, assumed, or unresolved. If invoices, bank address, and housing records point to different bases, stop optimizing and fix that conflict first. If your work has shifted into local business activity, re-check your assumptions before relying on generic "tax-friendly" framing.

For a step-by-step walkthrough, see Taxes in Colombia for Foreigners and Remote Workers.

Use a Residency Decision Sequence Instead of Guessing#

Use a sequence, because a favorable guess is not a method. Choose the filing position you can defend from records, not the one that looks most attractive. In a fragmented tax environment, reproducible records matter more than assumptions.

Step 1. Count presence#

Start with presence because it is the easiest part to reproduce later, but do not stop there. Build your count from source records, not memory, and document your method. Reconstruct the year using travel and stay evidence, then test it against the threshold you have currently verified with qualified local advice.

Use this pass/fail screen:

- Pass: Your count is below your verified trigger, your period is clearly defined, and another reviewer could reproduce the same result from your records.

- Fail: Your count meets the trigger, is close enough that missing days could change the result, or your method cannot be reproduced from underlying records.

If you rely on summary tools, keep the primary records behind them. Summaries can be incomplete or inaccurate.

Step 2. Test ties#

The day count gets you to exposure. Your other records tell you whether the file is internally consistent. Treat this as an operational consistency test, not a legal ruling.

Use this pass/fail screen:

- Pass: Records for the same period, for example housing, contracts or invoices, and tax administration records, are internally consistent.

- Fail: Those records repeatedly point in different directions, or their dates cannot be reconciled.

Period matching is non-negotiable. If one record set updates months after another, your file is not coherent yet.

| Signal observed | Provisional position | Evidence required | Escalate or proceed |

|---|---|---|---|

| Count meets or exceeds your verified threshold | Residency risk is elevated | Day-count method, underlying travel/stay records, covered period | Escalate for jurisdiction-specific review before filing |

| Count below threshold, but records repeatedly cluster in one jurisdiction | Residency risk may still be elevated | Address trail across housing, contracts, invoices, and tax administration records | Escalate if you cannot reconcile why records cluster there |

| Count below threshold and records consistently point elsewhere | Lower residency risk, still subject to review | Complete count file and consistent period-matched records | Proceed with a dated memo and recheck before filing |

| Mid-year move or conflicting records across travel, contracts, and billing | Unresolved fact pattern | Move timeline, address changes, contract or invoice update trail | Escalate before filing |

Step 3. Run a conflict check for edge cases#

For mid-year moves or multiple addresses, compare dates across three lanes: travel, contracts, and billing or admin records. Mark the exact date your living pattern changed, then verify when each lane changed. If the dates do not reconcile, do not average or smooth them into a story. Keep the conflict open and escalate.

Step 4. Write the assumptions memo#

Close with a short memo you can defend later. Include, at minimum:

- Counting method used

- Source documents used

- Unresolved conflicts

- Next review point (a real date)

Escalate when facts do not reconcile across the two screens. If presence points one way and record consistency points another, you do not have a defensible filing position yet.

Need the full breakdown? Read Taxes in Italy for Expats and Freelancers.

Classify Your Work Setup Because Tax Treatment Follows Facts#

This part should be built from your records, not just the label in an app, the payment origin, or shorthand people use in conversation.

Step 1. Gather the records that describe day-to-day reality#

Build one file with your contract, scope documents, invoices, payment records, work-direction messages, approval trail, and where you physically worked during the period. Your test is simple: if another reviewer reads the same file, can they follow your reasoning without guessing?

Keep the same source discipline here. Recency markers, for example a page dated December 10, 2025, can help with tracking, but promotional content, for example a 5% code page, is not a legal classification authority.

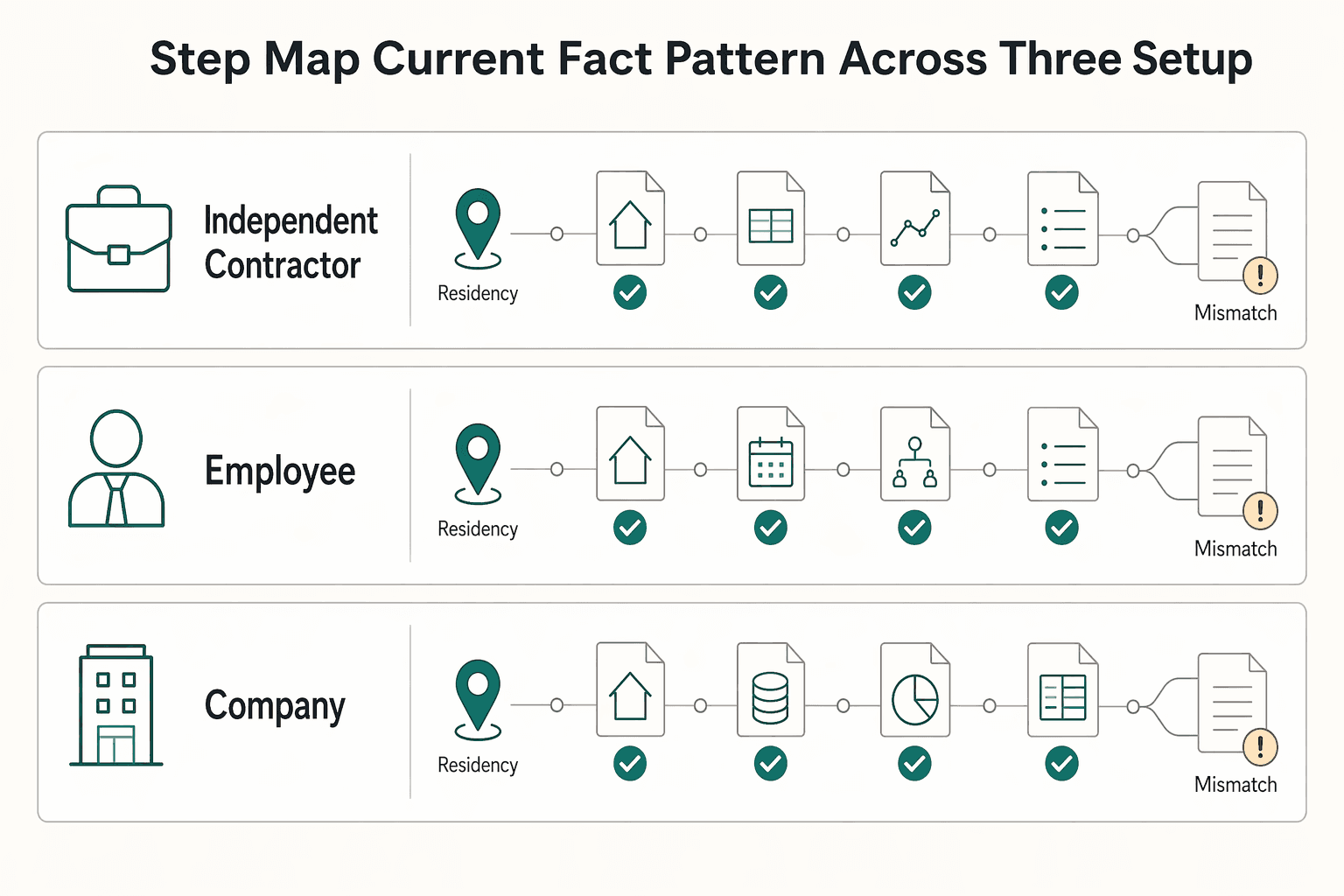

Step 2. Map your current fact pattern across the three setup paths#

Specific Portugal legal tests for contractor vs employee vs company are not established here, so use this table as a documentation checklist, not as a legal rulebook.

| Setup path | Contract terms | Control and supervision | Commercial risk | Invoicing/payment trail | Where work is performed | Mismatch flag |

|---|---|---|---|---|---|---|

| Independent contractor | What the signed documents say about scope and deliverables | What your records show about who directs daily execution | What your records show about who carries business downside | Whether invoicing and payment records align with this path | Whether location records are complete and consistent | Flag if records point to a different path or are incomplete |

| Employee | What the signed documents say about role and relationship | What your records show about day-to-day direction | What your records show about who bears business downside | Whether pay records align with this path | Whether location records are complete and consistent | Flag if records point to a different path or are incomplete |

| Company | What the signed documents say about entity-to-entity engagement | What your records show about operational control in practice | What your records show about where risk sits in practice | Whether entity records and money trail align with this path | Whether location records are complete and consistent | Flag if records point to a different path or are incomplete |

Step 3. Run a consistency check before filing#

If the documents say one setup but your day-to-day records show another, pause and resolve the conflict before submission. Update the documents or adjust your filing assumption so everything matches the same fact pattern.

Escalate when control, invoicing, and work pattern give mixed signals, or when your decision depends on a legal threshold you have not independently verified.

Related reading: Taxes in Mexico for Expats Without Guesswork.

Understand NHR Legacy Claims and the IFICI Conversation Without Overclaiming#

This is where a lot of files drift. Treat both a legacy NHR path and an IFICI path as provisional until you can verify each required check from current, accessible material and your own records.

The material behind this article supports broad context on UN-level tax-rule negotiations and a convention tracker, and it shows that some candidate sources may be inaccessible. It does not verify Portugal-specific NHR or IFICI legal criteria.

Use legacy NHR claim and IFICI claim as working labels only, not legal conclusions. Unverified means at least one required check is still pending, based on memory, carried over from prior years, or tied to a source you cannot access.

Use this sequence in order:

- Identify the exact claim path you are using now.

- Test each required check against accessible primary material and your records.

- Mark every check as

ConfirmedorPending. - Defer claim-dependent planning until key checks are confirmed.

| Claim path | What you can safely say now | What evidence supports it | What makes it unsafe to claim | Escalation trigger |

|---|---|---|---|---|

| Legacy NHR claim | The label is under review and not yet confirmed | Accessible primary authority text plus your own records, logged check by check as Confirmed/Pending | Prior-year assumptions copied forward, summaries without primary text, or unresolved checks | You cannot validate the basis from accessible material, or your records conflict |

| IFICI claim | The label is under review and not yet confirmed | Accessible primary authority text plus your own records, logged check by check as Confirmed/Pending | Using the label as settled before checks are complete, relying on secondary summaries, or treating pending items as final | Any key check remains pending near filing, or records point in different directions |

| No regime claim yet | Your base filing position does not rely on unverified regime assumptions | Records that align with your current filing narrative | Building planning around a regime before verification | Cross-border overlap, conflicting records, or unresolved filing narrative |

If a source is inaccessible, treat it as unusable until you can review it. Keep a one-page checklist memo and update it as checks are completed:

- Filing year: not yet recorded

- Current claim path: not yet selected

- Current authority reviewed: not yet verified

- Required check 1: not yet identified

Status: pending until verified

- Required check 2: not yet identified

Status: pending until verified

- Facts that support the claim: not yet mapped to documents

- Facts that conflict with the claim: not yet mapped to documents

- Decision if any key check stays pending by filing cutoff: defer the claim or escalate

Pause and get Portugal-focused advice if your facts are cross-border, your records are inconsistent across residency, work, and income files, or your current position depends on assumptions carried over from prior years.

Related reading: Taxes in Germany for Freelancers and Expats.

Handle Foreign Income, VAT, and Social Charges as Separate Risk Buckets#

Keep these in separate lanes from the start. One lane does not prove another.

Foreign-source income is income you are treating as arising outside Portugal for income-tax analysis. This lane answers whether Portugal can tax that income in your position and whether treaty or regime review is needed. Tax residency is separate from residence-permit status, and residency is often described as triggered by 183 days or more in a calendar year or by habitual-home facts. Once triggered, Portugal may tax worldwide income, subject to exemptions, special regimes, and treaties.

VAT is a separate lane for what you invoice. This lane checks whether your VAT treatment matches the facts you can document.

Social security is your coverage lane for work earnings. This lane answers which country's system applies and what proof you need if an exemption applies elsewhere.

| Bucket | Primary question | Key documents | Common wrong shortcut | When to escalate |

|---|---|---|---|---|

| Foreign-source income | If you are tax resident in Portugal, how is this income treated, and do you need treaty or regime analysis? | Contracts, invoices, payment records, travel log, housing records, residency memo, current authority reviewed | "Client is abroad, so Portugal cannot tax it" or "my permit decides tax residency" | Two countries may tax the same income, or residency facts conflict with contract and payment facts |

| VAT | Does your invoice treatment match the real service and client facts you are relying on? | Invoices, service descriptions, client records, current authority reviewed | "If income is foreign-source, VAT is solved" | You cannot document the facts behind your VAT treatment, or authority is missing |

| Social security | Which country covers these earnings, and do you have proof for any exemption? | Work agreement, work-location history, payroll records (if any), Certificate of Coverage (if applicable) | "Income-tax treaty analysis settles social charges" | The same earnings may be exposed in two countries, or coverage proof is unclear |

Build three short memos, one for each bucket, and mark every item as confirmed, assumed, or missing authority.

- State the filing year and bucket name.

- Write the exact question for that bucket.

- List documents and current authority reviewed.

- Mark each conclusion as

confirmed,assumed, ormissing authority. - Note what fact changes would change the answer.

- Set a review trigger for contract, work-location, or travel-pattern changes.

Keep Totalization and Certificate of Coverage in the social-security lane only. Totalization agreements are designed to reduce dual Social Security taxation and help split-country careers. For the U.S., they cover Social Security and Medicare taxes, and the U.S.-Portugal agreement is listed as in force from August 1, 1989. If U.S. coverage applies, a Certificate of Coverage is proof of exemption from the other country's Social Security taxes, and employers or self-employed individuals can request certificates online. Use that as social-security evidence only.

Run income-tax treaty relief analysis separately, and if timing or eligibility is unclear, mark the processing timeline as pending until verified. Reopen all three lanes when facts change. If travel days, housing pattern, or contract terms move, re-check each memo before filing and escalate early if key items remain assumed or missing authority.

You might also find this useful: Taxes in Estonia for E-Residents and Nomads.

Build a Tax Evidence Pack You Can Defend#

Once your position is plausible, make it traceable. Build your evidence pack so a reviewer can follow your residency and work-structure position from documents, not from explanations. Keep residency, income, VAT, and social-charge analysis in separate lanes, but make sure the underlying facts stay consistent across all of them.

If your time in Portugal is approaching more than 183 days in the calendar year, or you may have habitual residence there on December 31st, prepare your file as if resident treatment and filing obligations may need to be defended. Tax residency treatment is not automatic in the cited guidance; if your position relies on Portuguese tax registration and a Portuguese address, include that record set as well. Inconsistency across documents is a cited failure point, even when you otherwise have enough paperwork.

Step 1. Build the matrix before collecting more files#

Use a compact matrix to define what each document proves and how you will cross-check it. This is an operating format, not a legal requirement.

| Document type | What it proves | Key fields to capture | Cross-check source |

|---|---|---|---|

| Passport or government ID, plus Portuguese tax registration record if relevant | Identity and, when relevant, registration tied to a Portuguese address | Full legal name, ID number, registration date, address shown | Lease, utility bill, bank profile, invoices |

| Housing records | Address history and whether Portugal functioned as a stable home base | Address, occupant name, start and end dates, payment proof | Tax registration record, travel log, utility bills |

| Employment agreement or client contract | Work setup and who engaged you | Legal names of parties, start date, scope, billing address | Payslips or invoices, platform statements, bank inflows |

| Invoices or payslips | Income earned for a specific period | Date, period covered, seller or employer details, client or employee details, amount, currency | Contract, bank payment record |

| Bank or payout records | That funds moved and from whom | Payer name, amount, value date, payment reference | Invoice number, payslip date, platform payout report |

| Travel log and work-location records | Day count and where work was performed during the period claimed | Entry and exit dates, city or country, timestamps if available | Passport stamps, flight records, calendar, coworking receipts, housing records |

If you work through a platform, keep platform statements as supporting evidence, not as a substitute for showing who paid you and for which period. Platform work can sit under different legal statuses, so the platform label alone may not be enough.

Step 2. Tie each claim into a chain of proof#

For each key fact, build a proof chain instead of relying on a single document:

- Contract or employment agreement -> invoice or payslip -> bank inflow or platform payout

- Work-period claim -> calendar or time log -> work-location evidence -> housing and travel record

- Portuguese address claim -> lease or utility record -> payment receipt -> tax registration address (if relevant)

Be strict with identity and timing fields. Names, dates, and addresses should align across the contract, invoice or payslip, payment record, and location evidence for the same period.

Step 3. Reconcile on a fixed rhythm and log discrepancies#

A good file is maintained, not rebuilt at the deadline. Run the same checklist on a schedule, and tag each item as collected, reconciled, gap found, or resolved.

- Monthly: collect new contracts, invoices or payslips, bank records, housing receipts, and travel updates.

- Quarterly: reconcile names, addresses, dates, service periods, currencies, and amounts across the proof chain.

- When mismatches appear: mark

gap foundand open a dated discrepancy log. - After correction: save the corrected record or explanation note, then mark

resolved.

Your discrepancy log should capture: date found, issue, affected documents, correction made, and date resolved.

Step 4. Escalate when the file still does not align#

If identity fields, addresses, timelines, tax narrative, and income narrative still conflict after reconciliation, pause your filing assumptions and get Portugal-focused tax review. Escalate early when two countries may both treat you as resident, or when your day count and housing pattern do not match billing and payment records. When documents cannot be made consistent, review is safer than improvisation.

Turn your notes into a repeatable record before filing with the Tax Residency Tracker.

Know the Red Flags That Mean Talk to a Pro Now#

If your filing position depends on unresolved assumptions, stop and escalate. Once you are filing on guesses, the process stops being self-serve.

| Red flag | What you see | What to do next |

|---|---|---|

| Cross-country timeline unclear | Your timeline, housing pattern, work location, or year-end living facts are incomplete or conflicting across countries. | Pause assumptions and escalate with a clean timeline, including travel dates, housing dates, and where work was physically performed. |

| Key documentation unverified | Required document checkpoints are still open, such as proof of accommodation for a full year, criminal record checks from every country lived in, or whether documents need translation and an Apostille. | Mark each item as verified vs unverified, then escalate with the gaps clearly listed. |

| Process timing uncertain | Timing-sensitive steps are unresolved, such as short visa-validity windows (for example, 4 months) or appointments that are hard to obtain (for example, AIMA). | Document each timing risk and current status before you escalate. |

| Records are incoherent | Contracts, invoices, payment records, address history, and travel logs do not align on names, dates, or locations. | Stop optimization, repair the record set, or escalate if it cannot be reconciled cleanly. |

Separate the assumptions before you ask for help#

Keep each assumption explicit instead of letting one unresolved point carry the rest. If your position only works when multiple unverified assumptions are all true, you are out of self-serve territory and into professional-review territory.

Red flag when your cross-country timeline is still unclear#

What you see: your timeline, housing pattern, work location, or year-end living facts are incomplete or conflicting across countries. Why it is risky: unclear facts make your filing position assumption-driven instead of record-driven. What you do next: pause assumptions and escalate with a clean timeline, including travel dates, housing dates, and where work was physically performed.

Red flag when key documentation is still unverified#

What you see: required document checkpoints are still open, such as proof of accommodation for a full year, criminal record checks from every country lived in, or whether documents need translation and an Apostille. Why it is risky: unresolved document assumptions can stall your process and weaken your filing position. What you do next: mark each item as verified vs unverified, then escalate with the gaps clearly listed.

Red flag when process timing is uncertain#

What you see: timing-sensitive steps are unresolved, such as short visa-validity windows (for example, 4 months) or appointments that are hard to obtain (for example, AIMA). Why it is risky: timing uncertainty increases deadline-error risk, including avoidable late-filing penalties where applicable. What you do next: document each timing risk and current status before you escalate.

Red flag when records are incoherent#

What you see: contracts, invoices, payment records, address history, and travel logs do not align on names, dates, or locations. Why it is risky: incoherent records turn basic compliance into a reconstruction exercise and increase timing-error risk, including avoidable late-filing penalties where applicable. What you do next: stop optimization, repair the record set, or escalate if it cannot be reconciled cleanly.

Triage checklist before contacting a pro#

Before you call, make it easy for someone else to see the problem. Prepare a compact pack:

- One-page timeline for the year: travel dates, housing periods, and year-end living facts

- Work-location summary: where services were physically performed

- Document status note: NIF status, full-year accommodation evidence, criminal record checks by country lived in, and translation/Apostille status

- Process-risk note: appointment constraints and short validity windows that affect your timeline

- Evidence-gap list: mismatches and missing documents

Final quality check: if names, dates, and addresses do not match across at least one full pay period and one travel period, state that plainly before you escalate.

This pairs well with our guide on Portugal NHR for US Consultants in 2026 and the W-2 vs Unipessoal LDA Choice.

What to Do in the Next 30 Days#

Your job over the next month is simple: set a defensible provisional filing position, back it with reconciled records, and escalate anything unresolved before you file. Open one dated memo and label every material point as confirmed, assumed, or unproven. Keep NHR and IFICI status provisional unless eligibility is verified. If your position depends on either regime and you have not verified eligibility, it stays unproven.

| Step | What to do | Verification point |

|---|---|---|

| Set your provisional residency position | Write a one-page position using one or both of the two core tests: more than 183 days in a relevant 12-month period, and whether you maintained a home there as habitual residence. State the filing consequence clearly. | A third party can read this page and state your provisional status, your reasoning, and what still needs proof. |

| Build and reconcile your evidence pack | Collect dated records for travel, housing, work location, income flow, and regime assumptions. Run one hard reconciliation test on one full pay period or invoice cycle. | Each material memo claim has supporting evidence, or it is downgraded to assumed or unproven. |

| Run a conflict check | Look for contradictions in day count, habitual-residence facts, work-location records, invoice narrative, and AT address or status records. | Your residency narrative, evidence pack, and intended filing treatment all align. |

| Escalate if risk is still live | Escalate to a Portugal-focused advisor if dual-claim residency risk, unresolved NHR or IFICI assumptions, or mismatched records remain. | Send a tight pack: one-page memo, lived and worked timeline, conflict list, and key supporting and contradicting documents. |

Step 1. Set your provisional residency position#

Write a one-page position using one or both of the two core tests: whether you were in Portugal for more than 183 days in a relevant 12-month period, and whether you maintained a home there as habitual residence.

Then write the filing consequence clearly:

- Residents are generally taxed on worldwide income.

- Non-residents are generally taxed on Portugal-source income.

Also note whether a residency-relevant address or status change must be reported to AT within 60 days. Verification point: a third party can read this page and state your provisional status, your reasoning, and what still needs proof.

Step 2. Build and reconcile your evidence pack#

Match documents to claims, not the other way around. Collect dated records for travel, housing, work location, income flow, and regime assumptions.

Typical pack:

- Travel log plus tickets or border records

- Lease or housing dates

- Contracts

- Invoices or payroll records

- Bank inflows

- Work-location calendar

- NHR legacy application or supporting documents (if relevant)

- IFICI eligibility notes, including unresolved five-year non-residency and qualifying-activity checks

Run one hard reconciliation test: pick one full pay period or invoice cycle and match the calendar, travel, work-location, and bank records. Verification point: each material memo claim has supporting evidence, or it is downgraded to assumed or unproven.

Step 3. Run a conflict check#

Before you file, look for contradictions:

- Day count points to residence, but filing logic treats you as non-resident

- Housing facts suggest habitual residence, but your memo ignores it

- Work-location records conflict with the invoice narrative

- AT address or status records lag behind your current facts

Do not use NHR or IFICI assumptions to cover unresolved residency facts. If records conflict, stop and resolve them. Verification point: your residency narrative, evidence pack, and intended filing treatment all align.

Step 4. Escalate if risk is still live#

Escalate to a Portugal-focused advisor if any of these remain:

- Dual-claim residency risk

- Unresolved NHR or IFICI assumptions

- Mismatched records

Send a tight pack: one-page memo, lived and worked timeline, conflict list, and key supporting and contradicting documents.

Ready-to-file gate#

- One coherent residency narrative based on the >183-day test, habitual-residence test, or both.

- One reconciled evidence pack with no major mismatch across travel, housing, work location, and income records.

- One written filing plan stating what you will file, what remains provisional, and what must be updated with AT.

If any gate fails, you are not ready. Portugal's IRS filing window is 1 April to 30 June for online filing, but deadline pressure is not a reason to treat unproven facts as confirmed.

Related: 183-Day Rule Explained: Stop the Tax Myths Before They Cost You.

If your facts still point to multi-country exposure, talk to Gruv to confirm a safe operational setup.

Frequently Asked Questions

Does being a "digital nomad" change your tax status in Portugal?

Do not treat the label alone as a tax conclusion. Start by documenting your facts: where you lived, where you worked, your legal setup, and what records you can prove.

What should you test first if you think Portugal might treat you as tax resident?

Start with separate tracks: the residency-rule details you still need to verify under current Portugal law, and your actual living/work-location facts for the year. Keep Portugal day-count thresholds and habitual-residence test details explicitly unverified until confirmed.

Is day count the only thing that matters?

Verify your count against a travel log that matches tickets, border records, and housing dates, and treat unresolved residency-rule checks as open items until verified.

Does your D8 visa automatically make you Portuguese tax resident?

Do not use visa status alone as proof of tax residency. Keep immigration documents and tax analysis in separate files, and use Portugal Digital Nomad (D8) Visa: A Complete Guide for immigration planning only.

Does it matter where you physically performed the work if your client or employer is abroad?

It can matter in sourcing analysis. For example, California guidance ties source income to where services were physically performed. Keep a dated work-location log and reconcile at least one full pay or invoice period to your calendar, travel records, and bank inflows. Do not assume California sourcing rules determine Portugal filing outcomes.

What does each tool actually determine?

Use this split before filing so you do not mix separate decisions. | Tool or question | What this determines | What this does not determine | |---|---|---| | Tax residency analysis | Whether residency may be claimed under the rules you verified | Social-security coverage, VAT outcome, or regime eligibility by itself | | Treaty relief position | Whether double-tax relief may be available under treaty analysis | Social-security assignment or VAT treatment | | VAT analysis | Whether VAT obligations may exist under the rules you verified | Income-tax residency | | Social-security analysis and Certificate of Coverage | Which country's social-security coverage applies, and whether contributions may be exempt in the other country | Income-tax residency or VAT treatment | If one tool is being used to answer another tool's question, pause and correct that before you file.

Does a Certificate of Coverage decide your income-tax or VAT treatment?

No. A Certificate of Coverage is social-security evidence, not an income-tax residency decision and not a VAT ruling. For U.S. coordination, Portugal appears on the SSA agreement list, with entry into force shown as August 1, 1989, and if coverage is assigned to the United States, SSA issues the certificate.

Can you assume foreign income is exempt because of NHR or IFICI?

No. Keep any NHR or IFICI outcome provisional until eligibility is verified for your exact facts. If your filing position changes materially depending on that assumption, escalate before filing.

When should you stop DIY planning and talk to a pro?

Escalate when two countries could plausibly claim you, your records conflict, or your NHR or IFICI assumption is still unresolved. Bring a compact pack: one-page timeline, work-location summary, regime-assumption note, evidence-gap list, and a social-security note showing whether a Certificate of Coverage was requested, by whom, and when.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- europarl.europa.eu/RegData/etudes/STUD/2025/774671/EPRS_STU(202...trusted

- ftb.ca.gov/file/personal/residency-status/part-year-and...trusted

- info.portaldasfinancas.gov.pt/en/tax-information/getting-started-in-portug...trusted

- oecd.org/content/dam/oecd/en/publications/reports/202...trusted

- oecd.org/content/dam/oecd/en/publications/reports/202...trusted

- registrar.northwestern.edu/documents/registration/catalog-archive/2017-...trusted

- ssa.gov/international/CoC_link.htmltrusted

- ssa.gov/international/agreements_overview.htmltrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Portugal Digital Nomad Visa Decisions That Prevent D8 Delays

Start with verification, not paperwork. In this research set, some material is useful only as EU VAT context, not as D8 instruction, and mixing those categories is one of the fastest ways to build the wrong plan. We use the same separation rule in [Global Digital Nomad Visa Index](/blog/global-digital-nomad-visa-index) comparisons.

Lisbon Digital Nomad Guide 2026 for Long-Stay Move Sequencing

Lisbon can still work well for remote professionals in 2026, but the smoother moves usually come from sequencing decisions well, not from moving fast. This is an execution guide, not a lifestyle brochure. The point is to help you avoid paying for the wrong apartment, booking the wrong timeline, or building your first month around assumptions that collapse on arrival.

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.