Quick Answer

Payoneer is not clearly the best platform for marketplace freelancers here. It is presented as a workable cashflow rail only after you verify your own account setup, fees, FX, withdrawal behavior, and review risk. The recommended approach is to run one end-to-end test, track net landed value per invoice, and keep a tested backup rail active.

Treat Payoneer as a cashflow rail, not just a payout app#

Treat Payoneer, and every alternative, as a cashflow rail, not an app. The outcome you want is boring and measurable: money moves from approved work to usable bank funds on time, at a cost you can explain, with backup options ready before anything breaks.

If your income comes from marketplaces, direct international clients, or both, you are not just choosing a payment button. You are choosing a process: how clients pay, how funds are verified, how conversion happens, how withdrawals land, and how quickly you can explain the payment flow if questions come up.

Use that lens throughout this article. Build a get-paid system that stays stable when fees show up, timing slips, or account reviews land at the worst moment. In one freelancer report on Upwork, platform fees were over $5,000 for a year and described as a tradeoff for operational support like contracts, payments, and dispute handling.

Cashflow rail means the full path from "client approved payment" to "cash available in your bank." Reported account-risk cases show why backup rails matter: one Stripe Connect account was deactivated with an opaque reason and later reactivated after escalations, and one Payoneer closure report says reactivation may be unavailable even if fund withdrawal is still possible.

Use this playbook for any rail, including Payoneer, Stripe Connect setups, or marketplace-native payouts:

- Decide fit quickly with a risk scorecard.

- Model true cost per invoice from receive to withdraw.

- Run preventable risk controls so reviews do not derail your month.

- Keep one backup rail active so a single issue does not become a cashflow event.

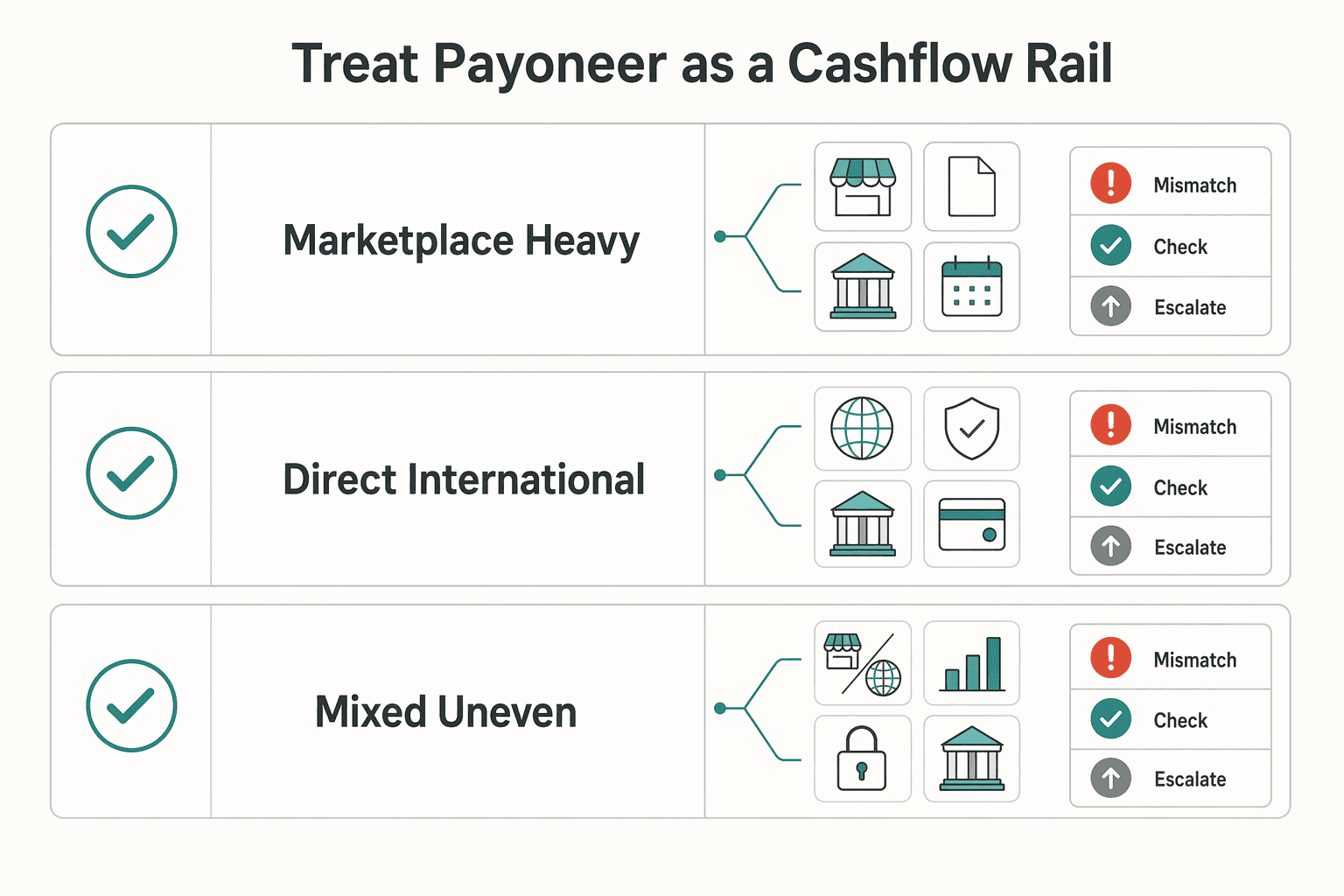

| Your situation | What you need most | What to evaluate first |

|---|---|---|

| Marketplace-heavy income | Predictable payout path | Native payout flow vs added external steps |

| Direct international clients | Transparent invoice-to-bank route | Conversion method and withdrawal economics |

| Mixed and uneven months | Operational resilience | Backup rail readiness and cash buffer rules |

If you apply only one principle from this piece, use this one: pick rails with controls first, then volume.

The selection criteria: a 10-minute risk scorecard (so you don't bet rent money on the wrong rail)#

If a payout rail cannot pass these five risk checks with your own evidence, keep it in test only and send primary volume elsewhere.

Score each category 1-5 (1 = low risk in your setup, 5 = high risk). You are not trying to pick a favorite. You are trying to pick the rail that stays predictable when money is due.

| Risk category | Tight definition | Test-only signal | Evidence to promote toward primary |

|---|---|---|---|

| Fee risk | Non-FX charges that reduce net payout (receive, transfer, withdrawal, card, fixed fees) | You cannot explain net amount from invoice to bank credit | Two reconciled payments where quoted fees match provider activity and final bank credit |

| FX risk | Conversion loss from rate or spread and corridor routing | You cannot benchmark quote-time FX against a live reference | Logged quote-time rate vs benchmark, plus effective conversion cost by corridor |

| Hold/compliance risk | Delay risk from identity, activity, or source-of-funds review | Profile or documents are incomplete, or payment narrative is inconsistent | Verified profile plus ready evidence pack (invoice, contract or SOW, delivery proof) |

| Speed risk | Time from payer action to usable bank funds in normal flow | No end-to-end timing proof in your own process | One test payment and one normal payment with full timing log (send to bank credit) |

| Payer-behavior risk | Risk that the payer causes failures (wrong details, missing refs, late method changes) | Repeated instruction misses or payment-detail errors | At least one clean payment using reusable invoice instructions |

Keep these categories separate when you diagnose problems: fixed charges are fee risk, weak conversion is FX risk, review requests are compliance risk, and late payer action is speed plus payer-behavior risk.

Use explicit pricing as your benchmark#

Use a comparison rail to calibrate transparency, even if you do not choose it. Wise's U.S. pricing flow shows a clear model: live mid-market rate plus upfront fee, quote-time rate-lock display (Rate guaranteed (15h)), a listed 6.11 USD receive fee for USD wire or Swift, and regulator-standardized fee disclosure links.

That does not prove lowest cost for every country or account type. It does give you a verification standard: if you cannot reproduce landed net from visible inputs, keep the rail in test only. For side-by-side provider tradeoffs, see Stripe vs. PayPal vs. Wise: The 2025 Battle for Best Freelancer Payments.

One practical trigger to watch: Wise states discounts begin at 25,000 USD monthly volume and reset monthly. If you are near that level, route timing may change whether you qualify before the monthly reset.

Promotion and fallback triggers#

Promote a rail from test only to primary only after:

| Decision | Trigger | Action |

|---|---|---|

| Promote to primary | One small end-to-end test payment reconciles cleanly | Promote from test only to primary |

| Promote to primary | One normal payment reconciles cleanly | Promote from test only to primary |

| Promote to primary | You can match quote or fee view, invoice, provider activity, and bank credit without gaps | Promote from test only to primary |

| Route to backup rail | Repeated quote-to-net variance you cannot explain | Route volume to a backup rail |

| Route to backup rail | Repeated timing misses vs your normal window | Route volume to a backup rail |

| Route to backup rail | New document-review friction on previously stable flow | Route volume to a backup rail |

| Route to backup rail | Repeated payer instruction failures | Route volume to a backup rail |

If those first three checks pass, you can promote. If the failure patterns at the bottom start repeating, route volume to your backup rail.

For FX-heavy work, review each corridor separately. Wise also warns that additional Swift fees may apply on some routes to EUR outside SEPA. If FX leakage is your main risk, see How to Get Paid in Multiple Currencies Without Losing Your Shirt.

Best-fit traits and mismatch traits#

| Workflow profile | Best fit traits | Mismatch traits |

|---|---|---|

| Marketplace-heavy income | Standardized payout path with minimal extra handoffs | Added conversion or withdrawal steps with no timing or cost improvement |

| Direct international clients | Clients can follow bank-transfer style instructions and use consistent invoice references | Clients insist on incompatible methods or repeatedly submit incomplete details |

| Mixed marketplace + direct income | Clear separation of payment flows plus a live backup rail | One rail carries mixed, hard-to-explain patterns without clean documentation |

Any Payoneer-specific fee, FX, withdrawal, or review-policy detail should be confirmed in current official pricing or support materials before you rely on it. Treat unresolved policy details as pending official/provider verification.

The end-to-end Payoneer workflow (what actually happens from "send payment request" to "money in your bank")#

Once a rail clears the scorecard, the next job is mapping the actual flow. A usable rail is a sequence of states, each with a checkpoint and one clear action if the flow stalls.

Exact Payoneer statuses, checkpoints, and timelines are account- and route-specific, so treat this as an operating model rather than an official policy map.

Think in two layers:

- The money layer: how funds enter, move, and exit.

- The proof layer: invoice, contract or SOW, delivery evidence, and whatever a verification request asks for.

If you can move money but cannot produce proof quickly, the rail is not resilient.

1) Getting paid: choose the "entry point"#

Start by choosing how funds enter the system. No single Payoneer entry path applies to every account—routes vary by region and setup, so confirm the exact route in your account before you brief a client.

This is where many preventable mistakes start. If your client instructions are vague, every downstream step gets slower. Send one payment-instruction format and use it every time.

A practical way to cut errors is to standardize what you send. Keep the message short and treat it like a checklist, not a conversation. For example, always include:

- The invoice ID they should reference.

- The exact payment details you want them to use, copied directly, not retyped.

- A single sentence on what to do if their bank asks for additional details: reply to you before improvising.

You are not trying to control the client. You are trying to prevent an avoidable support loop caused by missing references.

2) Track the payment request status (don't guess)#

When you use a payment request flow, monitor whatever status indicators and verification prompts your account provides. If a request stalls, clear requested information or documents first.

Run the same sequence every time: check status, then check verification prompts, then reply with exact file names and references. Guessing adds delay.

Keep the routine simple:

- One source of truth: check the same two places first: current status, then verification prompts.

- One naming system: upload files that match what you say you uploaded.

- One response format: answer with a short chain that matches the transaction: client, service, invoice, delivery, reference.

The point is not to write a persuasive story. It is to make it easy for someone to close the loop without asking three follow-up questions.

3) Move money out: "Withdraw to bank" + timing realities#

Set expectations with clients, and with yourself, in business days. In one referenced withdrawal flow example, which is not an official Payoneer policy source, processing includes four validation phases: risk scoring (0-2 hours), payment validation (2-8 hours), content compliance (8-24 hours), and manual review for flagged cases (36+ hours). First-time withdrawals can also trigger extended review (24-48 hours). The same example also reports lower fraud attempts with stricter scrutiny for legitimate users.

| Phase | Timing | Context |

|---|---|---|

| Risk scoring | 0-2 hours | From one referenced withdrawal flow example; not an official Payoneer policy source |

| Payment validation | 2-8 hours | From one referenced withdrawal flow example; not an official Payoneer policy source |

| Content compliance | 8-24 hours | From one referenced withdrawal flow example; not an official Payoneer policy source |

| Manual review for flagged cases | 36+ hours | From one referenced withdrawal flow example; not an official Payoneer policy source |

| First-time withdrawals | 24-48 hours | Can trigger extended review in the same example |

Use that as a delay-risk model, not as a Payoneer SLA.

Withdrawals are also where people confuse "initiated" with "landed." Treat them as two operating checkpoints:

- Checkpoint 1: withdrawal initiated successfully. You have a reference, and the withdrawal is no longer just a plan.

- Checkpoint 2: funds landed in the bank and match your expected net result.

If you run payroll or fixed bills, build your buffer around the second checkpoint, not the first.

4) Track fee and net-arrival differences (especially on wires)#

The number on your dashboard may not exactly match what lands. Payoneer's exact fees, FX spread, and withdrawal charges vary by account and corridor—treat any shortfall as a route variable to track and verify directly with your providers.

If a withdrawal arrives short, capture the difference immediately and tag it in your cost sheet. Small deductions become a major margin leak when they repeat.

The discipline here is simple: never label a short arrival as "random." Treat it as a property of that route until proven otherwise. Then you can decide whether to reprice, reroute, or accept it.

5) Reconcile like a grown-up (even if you're solo)#

Use your account records and accounting system as part of a monthly close rhythm. The standard is simple: for any payment, you can show who paid, why they paid, what was charged, and what landed in the bank without digging through old chats.

| Operating stage | Checkpoint | No-surprises action |

|---|---|---|

| Receive | Funds reflected in account balance | Record payer, amount, purpose, invoice ID |

| Status follow-up | An update or request is visible in account | If stalled, clear outstanding verification asks first |

| Withdraw follow-up | Transfer marked initiated | Plan for business-day timing and follow-up window |

| Reconcile | Records match books | Tie statements and ledger entries to invoice-level evidence |

For a step-by-step walkthrough, see The CEO's Weekly Review: A 3-Part Framework for Global Freelancers.

The short list (2026): payout rails for marketplace freelancers-where Payoneer wins, where it doesn't#

Pick the rail based on the failure mode you can tolerate, not the branding. Use the same five decision criteria for every option: cost visibility, payout reliability, dispute or hold exposure, marketplace fit, and reconciliation burden.

A simple way to narrow the list is by revenue mix:

- If you are marketplace-only, keep the native payout path as your baseline and only add another rail after a landed-bank comparison.

- If you are mixed marketplace plus direct clients, keep Payoneer in scope only after you verify that one account actually reduces admin across both flows.

- If you are direct-client-heavy, benchmark Payoneer against rails with clearer published cost mechanics before making any rail your default.

| Rail | Cost visibility | Payout reliability | Dispute / hold exposure | Marketplace fit | Reconciliation burden |

|---|---|---|---|---|---|

| Payoneer | Current fee detail pending official/provider verification. | Account- and route-specific. Verify current status views, withdrawal path, and bank-landing behavior in your account. | Treat verification or compliance requests as possible and keep documentation ready. | Current eligibility detail pending official/provider verification. | Medium. Track receive, convert, and withdraw as separate events when applicable |

| Wise | High. Wise says pricing starts from 0.57%, uses the live mid-market rate, and charges a separate upfront fee | Quotes can show Rate guaranteed (15h) and an expected arrival date (example shown: Should arrive by Monday, April 6) | Route exceptions still matter | Current marketplace eligibility detail pending official/provider verification. | Low to medium. Fee visibility and standardized documentation support invoice-level matching |

| PayPal | Medium. Confirm whether a payment is domestic or international, then check the current fee document | Policy-document driven. Recheck the current fee page and policy updates before relying on prior numbers | Current dispute or limitation detail pending official/provider verification. | Current marketplace eligibility detail pending official/provider verification. | Medium. Save the printable fee document and tie receipts to invoice and market classification |

| Native marketplace payout | Current fee detail pending official/provider verification. | Current payout-timing detail pending official/provider verification. | Current policy exposure detail pending official/provider verification. | Highest for marketplace-only workflows | Low to medium, depending on platform exports and reporting |

Payoneer#

For Payoneer, route availability and operational stability are account-specific, so treat fit as unconfirmed until you verify your own setup. The main risk is uncertainty if you rely on stale fee or eligibility assumptions.

Control action: verify the exact route in your account, then run one small end-to-end live cycle to your bank before using it for critical cashflow. Keep one proof pack per payment: invoice, contract or SOW, delivery evidence, and transaction reference. If you need more context on multi-currency routing decisions, use The Best Multi-Currency Accounts for Digital Nomads and Freelancers and How to Get Paid in Multiple Currencies Without Losing Your Shirt.

Wise#

Wise can be a clean benchmark when cost visibility is your top priority. Wise states it uses the live mid-market rate with a separate upfront fee, shows send pricing from 0.57%, and notes discounts after 25,000 USD monthly transfer volume.

The main risk is assuming every corridor behaves the same. Wise explicitly notes that additional Swift fees may apply when transferring any currency to euros outside SEPA. Control action: save the quote, including arrival estimate and rate window, then compare quoted net versus landed net. For direct-client-heavy setups, use the broader comparison in Stripe vs. PayPal vs. Wise.

PayPal#

PayPal can be simple to start, but classification discipline matters. PayPal distinguishes domestic (same market) and international (different markets) transactions, and that distinction changes how you should validate fees.

The main risk is policy drift if you rely on memory. PayPal provides a printable fee document and policy-update notices, and this pack shows Last Updated: February 19, 2026 on the consumer fees page. Control action: save the current fee document when pricing work, label each receipt as domestic or international, and reconcile to that label.

Native marketplace payout#

If your work is fully marketplace-based, native payout is your baseline until real landed-bank comparisons prove another rail is better. That keeps your first decision simple and avoids adding moving parts too early.

The main risk is platform dependency on payout options and rules. Control action: treat native payout as control, then test any external rail against it using actual landed results and reconciliation effort, not interface convenience alone.

The true-cost model: calculate what Payoneer really costs per invoice (receive → convert → withdraw)#

Use invoice-level landed value, not remembered fees. Separate visible charges, FX spread, transfer deductions, and final bank arrival, then assign a route action: keep, monitor, or reroute.

If you blend cost types together, you cannot tell whether the problem sits in receive, conversion, or withdrawal.

The worksheet that makes the decision obvious#

Keep one row per invoice or payout event. If one client pays three times, log three rows. You are looking for repeated corridor behavior, not a yearly average that hides weak routes.

| Field | What to record | Why it matters |

|---|---|---|

| Invoice ID and corridor | Client, invoice amount, source currency, destination currency, withdrawal country or bank | Keeps comparisons on the same route |

| Explicit receive fee | Any fee shown at receipt. If unavailable, record that the current fee detail is pending official/provider verification. | Separates visible charges from hidden cost |

| Benchmark rate | Your reference rate captured with the same method every time | Gives a neutral FX anchor |

| Effective conversion rate | Rate implied by the actual conversion result | Shows what you actually received |

| FX spread estimate | Gap between benchmark rate and effective rate | Captures exchange-rate loss |

| Explicit withdrawal fee | Any fee shown when moving funds out. If unavailable, record that the current fee trigger is pending official/provider verification. | Completes provider-side fee tracking |

| Transfer deduction | Any shortfall between expected withdrawal and bank arrival. If unclear, record that the current deduction range is pending official/provider verification. | Flags intermediary or route leakage |

| Net landed value | What reached your bank after every step | This is the decision number |

| Route action | Keep, monitor, or reroute | Turns repeated outcomes into decisions |

| Evidence link | Folder, note, or file path to invoice, transaction, quote, and bank proof | Makes later verification fast |

1. Record explicit fees as one layer only#

Start with charges shown as fees: receive, conversion if displayed, and withdrawal. Do not treat this as full cost unless you also test FX and bank-arrival outcomes.

This is where undercounting starts. Wise is useful as a comparison discipline because its pricing outputs separate components, including fixed-fee examples like 6.11 USD for receiving USD wire and Swift payments and 2.39 EUR for receiving EUR Swift payments, plus quote lines such as Our fee and Total included fees. You are not importing those numbers into Payoneer. You are copying the structure so costs do not disappear into one vague fee bucket.

What this changes: if visible fees look small but net landed value is weak, the loss is elsewhere.

2. Measure FX spread with one fixed protocol#

FX checks are only reliable when the method never changes: same corridor, same timestamp method, same evidence source.

A clean benchmark is Wise's published live mid-market rate, and its quote can show Rate guaranteed (15h). Capture the benchmark at the same decision point each time, then keep that timing rule constant. For broader benchmark context, use Stripe vs. PayPal vs. Wise.

What this changes: you stop mistaking inconsistent measurement for real spread differences.

3. Treat transfer deductions as a separate failure mode#

A short bank arrival is not always FX. If provider-side figures look normal but landed funds are low, log it as a transfer-deduction issue in its own field.

This can show up on cross-border corridors. Wise explicitly notes that additional Swift fees may apply for transfers to EUR outside SEPA. That does not prove the same behavior for Payoneer, but it confirms that corridor-specific deductions can exist. Record the shortfall until verified.

What this changes: you can distinguish weak conversion from post-withdrawal leakage.

4. Set route action from repeated outcomes, not one bad invoice#

Use route action as a pattern decision:

- Keep: repeated invoices on the same corridor land consistently and admin effort stays manageable.

- Monitor: results are close to alternatives, one payout is odd, or evidence is incomplete.

- Reroute: the same corridor or client segment repeatedly lands short, needs repeated follow-up, or repeatedly loses margin through receive → convert → withdraw.

One anomaly is noise. A repeated corridor pattern is a routing decision. If the same corridor keeps landing in monitor or reroute, compare options in Stripe vs. PayPal vs. Wise and review corridor setup choices in How to Get Paid in Multiple Currencies Without Losing Your Shirt.

What this changes: decisions come from repeatable outcomes, not memory.

5. Save the evidence pack the same day

Your model is only trustworthy if each number is provable later. Save invoice, contract or SOW, delivery proof, transaction reference, benchmark capture, and bank-arrival proof in one folder, then attach that link to the worksheet row the same day.

For benchmark artifacts, prefer repeatable evidence. Wise offers a regulator's standardized format, which gives you a consistent checkpoint instead of relying only on ad hoc screenshots. If you use PayPal for side checks, remember this consumer fee page is scoped to US accounts and shows Last Updated: February 19, 2026.

What this changes: when margin drops, you can quickly tell whether the cause was visible fees, FX, or deductions.

Before you switch rails, run your own corridor math with the payment fee comparison tool.

Holds & freezes: the prevention checklist + the "funds stuck" escalation path (no panic, just execution)#

When funds get stuck, treat it as an execution problem, not a mystery. Identify the status, submit one complete evidence packet, and keep every follow-up traceable.

One caution here: the authoritative material is investor or SEC reporting, not support-policy documentation. The labels below are working labels, not official Payoneer policy definitions.

1. Use working labels so you choose the right path#

| Working label | Working meaning | First move |

|---|---|---|

| Review | Extra checks may be in progress and more information may be requested | Confirm the exact request scope before uploading anything |

| Hold | A payment event or funds appear paused pending verification | Map the payment to one invoice, one client, one proof set |

| Limitation | Some account actions appear restricted until an issue is cleared | Stop partial replies and answer the stated request directly |

| Freeze | Access or movement appears blocked and urgency is high | Build the full evidence packet immediately and preserve all reference IDs |

A common operational risk is not just the pause itself. It can be mismatched files, answering the wrong question, or opening multiple threads that break the payment trail.

2. Run four pre-invoice gates you can control#

- Identity consistency

Keep account details aligned with documents you may need later: name, address, banking details. Fix mismatches before sending volume.

- Document quality

Keep clean, readable files with full edges visible. If the reviewer would need interpretation, the file is not ready.

- Transaction narrative clarity

Map each payment to one client, one invoice ID, one service description, and one date range. If work is mixed, separate the paperwork so the chain is obvious.

- Backup-rail readiness

A backup rail is only real if it has been tested. One low-confidence but practical checkpoint from the provided Q&A source is to test receiving a small payment after setup. Keep that route active and documented. If needed, use how to get paid in multiple currencies as a control path.

A cautious takeaway from the non-authoritative Q&A source: unverified accounts may face longer approval and temporary holds. Treat verification readiness as a front-loaded control.

3. Build one evidence packet with four parts#

Official packet requirements vary by case. Use this as a working template:

| Packet part | What to include |

|---|---|

| Payment intent | Who is paying, for what, and why now |

| Service proof | Contract, SOW, proposal, or equivalent agreement |

| Delivery proof | Acceptance email, milestone confirmation, delivered work, or similar completion record |

| Transaction traceability | Invoice ID, amount, currency, payer name, reference or transaction ID, and bank-arrival trail if funds moved |

If a request is policy-specific, mark the current requirement as pending official/provider verification instead of guessing current rules.

4. Run the escalation playbook in order#

- Verify request scope

Read the request carefully and list exactly what is being asked.

- Submit one complete packet

Avoid drip-feeding unless the request explicitly requires staged uploads.

- Confirm submission mapping

State payment date, amount, invoice ID, payer, and attached file names in the same message.

- Log follow-up actions

Save ticket IDs, upload confirmations, screenshots, and timestamps with the invoice evidence.

This is how you keep control under pressure: one coherent payment story, one complete submission, and a verifiable action trail.

Marketplace decision trees (Upwork/Fiverr): when Payoneer helps, when it adds double-fees, and when to stay native#

For marketplace income, use marketplace logic first and optimization second. Add an external rail only when your own account-level test shows it improves net payout or payout reliability.

Fee tables, eligibility rules, and payout-timing guarantees for Payoneer, Upwork, and Fiverr are account-specific and change over time, so treat this as a practical decision framework rather than platform policy.

Working terms for this section, not official platform labels:

- Native payout: the payout method inside the marketplace flow.

- External rail: an added payment path outside that default marketplace flow.

- Double-fee risk: possible costs stacking across multiple layers, for example platform fees plus rail, conversion, or bank-arrival layers.

Decision Tree A#

If you work only on-platform, default to native unless a simple pass-or-fail check in your own account suggests the external rail is better.

- Eligibility check (pass/fail)

Confirm the method is visible, selectable, and fully configured in your live account settings. If not, stop.

- Fee-layer visibility check (pass/fail)

Map every visible deduction layer from marketplace to final bank arrival. If any layer is unclear, treat it as a no-go for switching.

- Reliability check (pass/fail)

Compare one completed payout path end to end: landed amount, currency, and arrival date. If outcomes are similar, stay native and avoid extra operational complexity.

On Fiverr-style work, one user report described outcomes as mixed and said issues often start with unclear requirements and unresponsive buyers. The same report emphasized clarifying missing requirements early in an order. When order clarity is weak, adding another rail may not fix the root problem.

Decision Tree B#

If you are moving from marketplace work to direct clients, keep flows separate until traceability is clean.

Use a strict traceability rule on every payment: keep invoice ID, payer, and payment reference together. If one is missing, do not consolidate records yet.

Keep marketplace funds tied to marketplace order trails, and direct-client funds tied to your own invoice trails. Consolidate only after each payment is landed, matched, and logged cleanly.

Decision Tree C#

If you pay a small team or subcontractors, decide based on control quality, not brand preference.

Proceed only when all four controls are in place as internal controls, not stated platform mandates:

- Documented workflow from client receipt to contractor payout.

- Role ownership for receipt confirmation and release approval.

- Payout-condition language in agreements, with a clear trigger for release.

- Audit trail quality that links client invoice, service proof, delivery proof, and outgoing payout record.

If one control is weak, keep the flow simpler until the control is fixed.

Quick go or no-go gate before switching:

- Method is active in your live account.

- Fee layers are visible enough to model.

- One test payout is recorded end to end.

- A fallback payout method is still active.

If you need deeper cost modeling before changing rails, use How to Get Paid in Multiple Currencies Without Losing Your Shirt and Stripe vs. PayPal vs. Wise: The 2025 Battle for Best Freelancer Payments.

Setup that helps prevent surprises: country coverage verification + Day-1 config + pre-flight test transfer#

Setup should work as risk control, not generic onboarding. Eligibility and flow details are account-specific—verify them in current provider docs or support, complete one end-to-end test, and keep documentation retrieval-ready before you route meaningful volume.

- Coverage verification

Check fit first: confirm current country, currency, and card rules directly in official provider materials before you switch rails. If any point is unclear, mark it Confirm current eligibility before switching and keep your fallback rail active. For account-strategy pressure testing, use How to Get Paid in Multiple Currencies Without Losing Your Shirt.

- Day-1 configuration

Treat Day 1 as internal control setup, not assumed platform policy. Define the alerts, folders, and file naming convention your team will use consistently, such as ClientName_InvoiceID_PaymentReference_DocumentType, so payment questions are traceable quickly.

- Pre-flight test transfer

Use one small transfer as a go-or-no-go gate before real volume. Run your full receive-to-withdraw path, log step dates and amount deltas in your own records, then update your true-cost model before scaling. Treat results as account-specific validation, not a universal timing or fee rule. If you need to validate backup-rail options at the same time, use Stripe vs. PayPal vs. Wise: The 2025 Battle for Best Freelancer Payments.

- Documentation readiness

Maintain a live evidence pack by client and invoice so each payment is easy to explain. Where IP transfer or confidentiality applies, keep the General Agreement, Non-Disclosure Agreement, and Employee Confidentiality Contract together, plus any signed confirmation of services rendered when your agreement ties transfer timing to that document. If payment records and paperwork do not map cleanly, resolution slows down and risk rises.

Reconciliation & tax admin: keep your books audit-ready without becoming a finance team#

After your test transfer works, make reconciliation boring and repeatable. Here, audit-ready means you can explain each payment from invoice to bank deposit quickly, without hunting through old messages or guessing at amount differences.

- Run a minimum monthly close

- Practical every-cycle baseline: save payout activity or statements where available, match each receipt to an invoice ID, record whether it came from a direct client or marketplace, and log fee or FX-conversion context. * Can usually defer one cycle: optional tags, extra reporting splits, and naming cleanups. * Treat as an immediate cleanup trigger: backlog rolls into a second close cycle, or you cannot explain a deposit quickly.

- Use one memo standard for every transaction

Every line should answer three questions: which invoice, who paid, and what changed the amount. If conversion drag keeps showing up, revisit How to Get Paid in Multiple Currencies Without Losing Your Shirt. If a payout rail creates messy narratives or stacked fees, compare options with Stripe vs. PayPal vs. Wise: The 2026 Battle for Best Freelancer Payments.

| Transaction | Book label | Memo standard |

|---|---|---|

| Payment received | Client receipt | `InvoiceID |

| Fee charged | Payment fee | `InvoiceID |

| Currency conversion | FX conversion | `InvoiceID |

- Keep one evidence bundle per client

A practical minimum bundle is invoice, contract or SOW, delivery proof, and the payout record tied to the bank deposit. If records and payment references do not map cleanly, month-end often turns into reconstruction work.

- Keep a hard boundary on tax and legal interpretation

Bookkeeping supports recordkeeping; it is not, by itself, a tax determination. Verify current filing requirements with a qualified professional. When you review rules online, treat unofficial pages as a starting point only and verify against official legal editions. FederalRegister.gov states its web version is informational and not the official legal edition, and it points readers to the corresponding official PDF on govinfo.gov.

Switching and alternatives: how to leave Payoneer (or add a backup rail) without unnecessarily disrupting cashflow#

Do not close a working rail out of frustration alone. Demote it first, and only route away when your own records repeatedly show weaker net outcomes, repeated timing friction, or support overhead that no longer justifies the convenience.

Your receive → convert → withdraw records are the decision system. When those records are clean, switching stays operational instead of emotional.

1. Define the roles before you change anything#

A backup is not "I can set it up later." It is already available.

| Term | Working meaning | Operational test |

|---|---|---|

| Primary rail | Your default route for normal payouts | Current invoices, client instructions, or platform settings point here |

| Backup rail | An alternate route kept available alongside the primary | Already configured and ready to receive payouts |

| Tested backup | A backup validated before you need it | Checked in a test environment where available |

| Cutover | The planned switch from one active route to another | Done on a defined date with updated instructions and a fallback path |

Some payout setups support multiple methods in one integration. Nuvei, for example, describes choosing payout methods and supporting rails like ACH, Visa Direct, Mastercard Send, and Payoneer. The practical point is simple: configure and verify before disruption, not after.

2. Run the cutover sequence in order#

- Verify payout setup by channel.

Check each marketplace, client portal, or billing tool separately. Save confirmation after each change. If a sandbox or test environment exists, use it before the next live payout.

- Confirm legal-name consistency.

Match the payout account legal name with contracts, invoices, and platform records. If you use a brand name, keep the underlying legal entity or personal legal name clear where funds are received.

- Update payment instructions before the next cycle.

Update templates, invoice notes, proposals, and "how to pay me" docs before billing starts. Avoid mid-cycle changes unless the current route is already failing.

- Send one clear cutover message with fallback instructions.

Include one effective date, one default method, and one fallback method if AP cannot update in time. Ask for confirmation that your vendor or payment record was updated.

3. Demote before close#

Use this rule: route away when repeated internal evidence shows the rail is now a weaker default. Look for repeat patterns in one or more of these areas:

- Worse net result across receive → convert → withdraw

- Timing misses against your expected payout window

- Support loops that consume more time than the rail saves

Use the same cost framework from earlier sections, not headline fee claims. For side-by-side rail selection, use Stripe vs. PayPal vs. Wise: The 2026 Battle for Best Freelancer Payments. If conversion drag is the core problem, use How to Get Paid in Multiple Currencies Without Losing Your Shirt.

4. Plan for single-rail failure#

Do not assume account age prevents disruption. One public anecdote about a Stripe Connect account describes a deactivation labeled "Other" and about a week of templated responses before restoration. That is not a market-wide statistic, but it is a plausible failure mode to plan for.

Keep one backup rail live and re-test it periodically. If the primary starts failing, route new invoices to the backup and let in-flight payments clear on the old route unless they are already broken. This approach helps reduce the chance of creating your own cashflow gap.

Bottom line: Payoneer is a solid rail when you run it with controls-here's your safe default next step#

Payoneer-specific superiority is unverified. What is clear is that payment and tax compliance pressure is tightening, so the system you run matters more than any single platform: controls, cost visibility, and fallback capacity.

Your safe default plan (next couple of days)#

Treat this like a short implementation sprint. You are not deciding forever. You are building a baseline system you can trust.

- Run the risk scorecard and write clear go-or-no-go triggers for fees, verification friction, and timing dependency.

- Execute one small end-to-end test through receive, convert if needed, and withdraw, then log timing and net outcome.

- Build your verification packet once and keep it ready in organized folders.

- Document the security and verification steps your chosen rail requires before you depend on it.

- Confirm inactivity, review, or closure conditions up front so policy checks do not surprise you later.

Your two non-negotiables (the "operator upgrade")#

These are the controls that separate "I hope it works" from "I know how this behaves."

- Keep one backup rail live and tested, not just created.

- Maintain a true-cost lens that separates explicit fees from exchange-rate effects on every meaningful invoice corridor.

Those two controls can do more for resilience than any single platform tweak.

When you're scaling volume or complexity#

As volume grows, shift from tool-level decisions to policy-level decisions: traceability standards, document gates, reconciliation cadence, and clear escalation paths.

The evidence indicates stricter payment and tax compliance frameworks as the gig economy expands, with examples like Spain's 2026 reporting change where payments are reportable regardless of amount after the prior EUR 3,000 threshold was removed. Build your workflow for that level of transparency. If you do, scaling feels like repetition, not firefighting.

If you want a cleaner setup for invoicing, balances, and compliant payouts, review Gruv for freelancers.

Frequently Asked Questions

Is Payoneer legit, and is it operationally safe for freelancers?

Payoneer is a regulated fintech used by millions of freelancers globally, but operational safety depends on your account setup and documentation quality. Support carries real risk: Payoneer's help search is AI-powered, warns results may be inaccurate, and can return no results. Keep a tested backup rail and clean invoice-to-payout records.

Can Payoneer hold your account, and is that the same as closure?

Holds and closures are different: a review or hold typically means funds are paused pending verification, while closure may block reactivation even if withdrawal remains possible. Treat the distinction as unconfirmed until you get an account-specific answer through signed-in support. Capture the current status, avoid sending new payouts there until clarified, and route new payments through your tested backup rail.

What should I do first if a payment is under review or support is unclear?

Start signed in and use account-specific support first. Help search is AI-powered, warns results may be inaccurate, and says not to share personal or confidential information. Submit short question-format requests with non-sensitive checkpoints only, then escalate through signed-in support if search is not resolving the issue.

What does "Source of Funds" mean, and what evidence should I keep ready?

Source of Funds requirements vary by account, payment type, and jurisdiction—Payoneer doesn't publish a universal checklist. Keep a consistent evidence chain: payer identity, service agreement, invoice, delivery proof, and payout record. One organized client folder is usually enough to respond quickly if asked.

How should I think about fees, FX, timing, bookkeeping, and tax?

Use one method across every rail: receive, convert, and withdraw. Judge performance by net landed value, not headline pricing alone, and compare rails with a true-cost model. Plan timing around bank business days and keep provider timing marked for verification in your own setup. Use platform data for bookkeeping support, and confirm tax treatment with a qualified professional in your filing jurisdiction.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- epubl.ktu.edu/object/elaba:235034466/235034466.pdftrusted

- federalregister.gov/documents/2021/01/07/2020-29274/independent-...trusted

- oecd.org/content/dam/oecd/en/topics/policy-issues/con...trusted

- paypal.com/us/digital-wallet/paypal-consumer-feestrusted

- sec.gov/Archives/edgar/data/1858257/0000950123210118...trusted

- sec.gov/Archives/edgar/data/1845815/0001558370250018...trusted

- thedocs.worldbank.org/en/doc/072814bbbb56aebd4db387154c3df3a5-0460...trusted

- wise.com/us/pricing/send-moneytrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Stripe vs PayPal vs Wise for Freelancers in 2026

Cashflow reliability matters more than brand familiarity. If money arrives later than expected, gets reduced by fees, or loses value during conversion, margin disappears even when the client technically paid on time.

The Best Multi-Currency Accounts for Digital Nomads and Freelancers

This shortlist is for cash flow decisions, not brand popularity. It is for freelancers, creators, and lean teams in the United States who need a cross-border payment setup that still works when real work hits: invoices go out, money lands, conversions happen on your timing, and urgent payouts do not depend on luck.

How to Get Paid in Multiple Currencies Without Forced FX

If you want to **get paid in multiple currencies** while protecting margin, separate collection from conversion. Receive the client's currency first, then decide if, when, and where to convert it.