Quick Answer

To open a European bank account as a non-resident, start by defining your exact residency scenario and focus on a reliable way to receive EUR via SEPA. Eligibility and onboarding requirements vary by country and institution, and online opening still typically requires ID, proof of address, and source of funds under KYC/AML checks. If you're legally resident in an EU country, you may be entitled to a basic payment account.

You're not trying to "open a bank account." You're trying to get paid from Europe-reliably.#

If euros arrive on time, reconcile cleanly, and remain usable without constant support tickets, you have solved the real problem. The search phrase "open european bank account non resident" usually means one thing in practice: protect cashflow. Start there, not with prestige features.

Think like an operator. You are not shopping for an app. You are designing a payment system that survives normal friction: compliance reviews, payer-side errors, transfer holds, and the occasional provider outage. A sleek interface will not protect revenue. Process will.

A safe default is to build resilience upfront with a simple two-rail setup:

- Rail 1: a dependable euro receiving path. SEPA is designed to make cross-border euro transfers across participating countries work more like domestic transfers.

- Rail 2: a backup way to receive funds. Assume one provider can pause activity, request additional documentation, or reject a transfer. Your backup exists so you can keep billing even when that happens.

Everything below follows one operating thread: define your scenario, pick a receiving rail your clients can execute correctly, then run payment ops with consistent documents and naming so avoidable delays stay avoidable.

The real risks (and the safe defaults)#

Most payment pain clusters into a few predictable failure modes. If you control those early, the rest becomes manageable.

Delays come from messy inputs. You reduce them by standardizing what clients copy and paste. Invoice in EUR when practical, keep payment instructions identical across clients, and enforce a single reference format that maps to your invoice ID.

Fee leakage comes from ignoring the system. Treat costs like a debugging task. Track transfer charges, intermediary deductions, and FX spread, then fix the largest leak first instead of arguing about small line items.

Holds and freezes come from narrative drift. Assume reviews will happen. When your business description, address history, and activity story drift across forms, invoices, and contracts, you create a manual-review magnet.

Safe defaults are intentionally boring. Boring payment operations are usually profitable payment operations.

Expect variation-and confirm eligibility before you apply#

Rules and workflows vary by country and by institution. Confirm eligibility before you spend time on onboarding.

If you are legally resident in an EU country, you have an EU-level right to open a basic payment account for everyday payment functions. Banks also cannot refuse this account only because you live in another EU country. They can still refuse if you do not meet rules on money laundering and terrorist financing, or if your file is incomplete.

That is why this article is risk-first and systems-minded. You will identify your scenario, choose a practical receiving rail, prepare an application-ready document pack, and set up backup coverage before you need it.

"Non-resident" is three different scenarios-pick yours before you do anything else#

"Non-resident" is too vague to be operational. Banks, payment providers, and tax forms need your actual status, not a loose label. If this is unclear, even a complete application can stall because your narrative does not line up.

Define your scenario first. Once that is done, provider choice, document prep, and support conversations get simpler because you can answer the questions reviewers are actually trying to resolve: who you are, where you live, why money is moving, and whether the story is consistent.

Step 1: Pick the scenario that matches your reality#

Use practical buckets before filling any form. These are operator labels, not legal definitions.

| Scenario | Your plain-English situation | What you must answer clearly |

|---|---|---|

| A | You live in the EU/EEA, but not in the account's country | Where you actually live and which address appears consistently in records |

| B | You are not legally resident in the EU | Why you need a European receiving setup and where your legal home base is |

| C | You are legally resident in one EU country and opening in another | Which country you are legally resident in and how you will use the account |

Default rule: treat residency as fact-dependent and document-backed. Keep one consistent record set across contracts, invoices, and onboarding forms.

Before you apply anywhere, write your scenario in one sentence that you can reuse across forms and support conversations. The goal is not clever wording. The goal is consistency.

Step 2: Separate "getting paid" from "having an account"#

Most people do not need "a European account" as the first milestone. They need reliable receipt of EU client payments without repeated rework.

So split the goal into outcomes you can test:

- Receive EUR predictably through a rail clients can execute correctly.

- Handle cross-border and non-EUR cases with clear expectations on timing and fees.

- Reduce compliance back-and-forth with one stable identity and business narrative.

This framing keeps you focused on what moves revenue, not on feature shopping. You can always optimize features later. You cannot retroactively fix a messy payment trail when you need cash now.

Step 3: Get your tax identifiers straight before you scale volume#

Tax friction tends to show up after volume rises. Handle it early, while the system is still small enough to control.

TIN (Taxpayer Identification Number) appears on IRS reporting forms such as Form 8938. Form 8938 is used to report specified foreign financial assets when total value exceeds the applicable threshold. In some cases, certain domestic corporations, partnerships, and trusts may also have filing obligations when asset values exceed specified thresholds.

You do not need complexity here. You need consistency. Keep one canonical record for identity, residency position, and activity description. When these fields drift across systems, manual-review risk increases and your support conversations get longer.

The 2026 reality check: what's feasible (and what's a dead end) for non-residents#

Feasibility is not a branding question. It is a qualification question. Can you receive EUR through SEPA in a setup you can pass with your current residency profile and documentation?

Run this check before you apply. It prevents a common failure loop: multiple long applications, multiple inconsistent narratives, and no working rail at the end.

SEPA exists to make euro payments across participating European countries behave more like domestic transfers. For most operators, confirmed SEPA receiving capability is the key gate. Do not assume that because a provider is popular it will fit your profile or your client workflow.

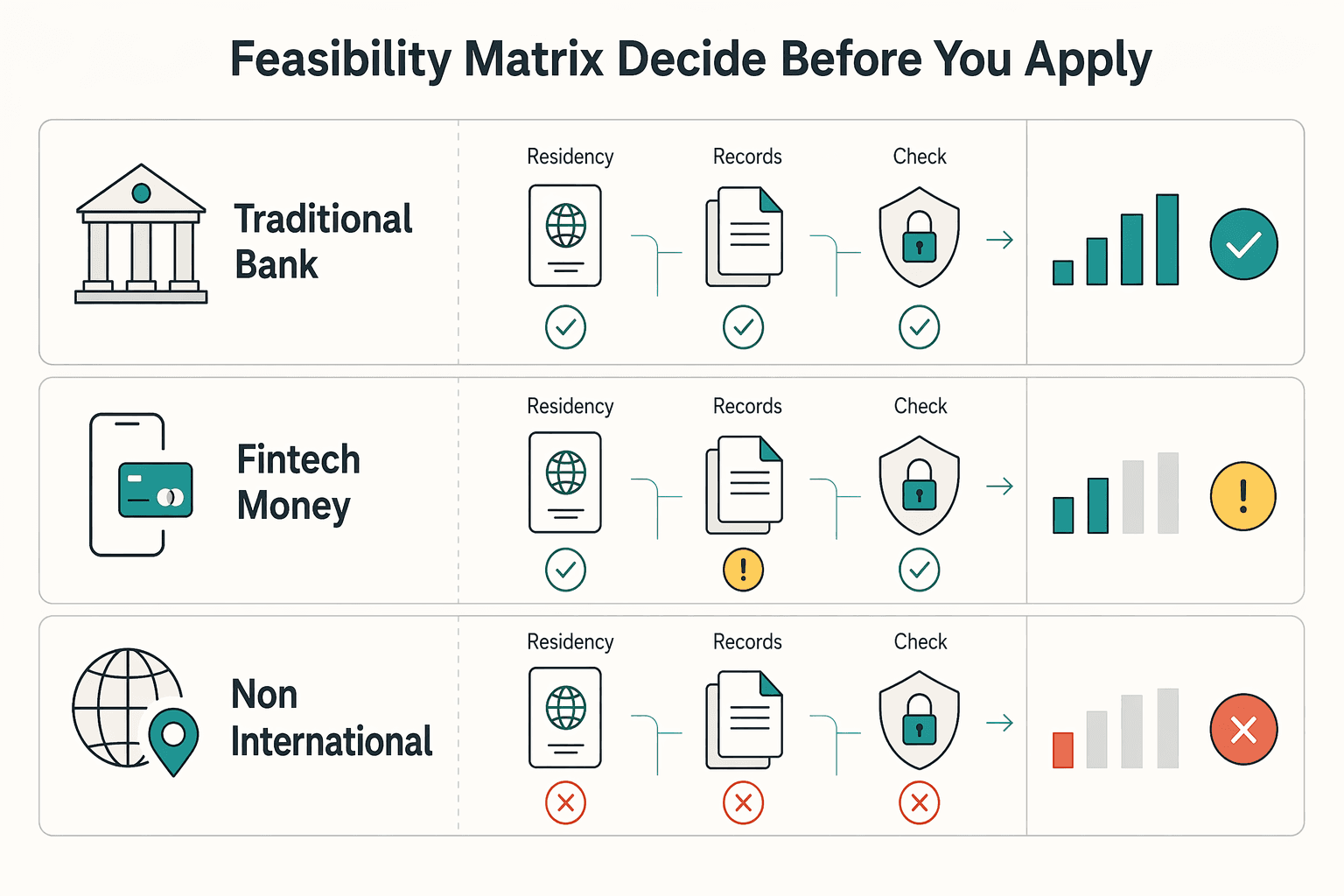

Use a feasibility matrix (decide before you apply)#

Evaluate every option with two tests:

- Can it receive EUR the way your clients actually pay?

- Can you prove what it asks you to prove without hand-waving?

| Option | When it's feasible | What typically creates friction |

|---|---|---|

| Traditional bank account | Bank policy aligns with your residency and documents | Country-level variation in requirements and process |

| EU fintech / e-money account | Remote onboarding is supported and checks can be passed cleanly | Identity and compliance reviews can still be iterative |

| Non-EU or "international" account | Priority is broader global access, not local banking extras | EUR receiving method may not fit payer workflow if SEPA support is limited |

Use this matrix to eliminate weak-fit options before onboarding. Every early "no" saves weeks and reduces the odds you end up with a half-working setup you cannot safely depend on.

Remote opening can be real-but not "no paperwork"#

Remote onboarding changes where work happens, not whether work exists. Expect full verification.

A prepared operator assumes the provider will ask for (and cross-check) basics like:

- Valid ID

- Proof of address

- Source of funds

Expect screening under KYC and AML standards. The advantage is speed through preparation, not speed through shortcuts. If you treat onboarding as paperwork you can improvise, you will pay for it in rework.

Operator rule: every application is a mini audit#

Assume reviewers will compare your forms against invoices and contracts line by line. If your story changes across documents, the review slows down. If names do not match cleanly, the review slows down. If your activity description feels vague or contradictory, the review slows down.

Your job is to make the reviewer's job easy:

- Keep one business description that you can reuse across providers without changing the meaning.

- Keep one beneficiary naming standard (and enforce it on invoices and contracts).

- Keep one explanation of why and how you receive EU payments.

Avoid shotgun applications with different stories. Pre-check fit first with a direct question: can you receive EUR via SEPA in your scenario, and which documents are accepted?

That discipline keeps effort tied to outcomes: predictable deposits, fewer surprises, and less compliance churn.

The cashflow-first decision framework: choose the right "receiving rail" (not the fanciest account)#

Pick the rail that makes payment easiest for the client and most traceable for you. Optimize account extras later.

Once feasibility is confirmed, lock a default route you can place on every invoice. Replacing improvisation with a standard flow is the fastest way to reduce late payments and reconciliation noise.

Start with the job-to-be-done (then map to a rail)#

Start with one payer-side question: what lets this client complete payment correctly on the first attempt?

For most EU clients, the lowest-friction option is the one that matches their existing payable workflow. If you bill in the client's normal currency and route, straight bank transfer tends to run with fewer internal approvals and fewer field-level mistakes. If you bill outside their routine, expect additional checks, delays, and "can you resend details" loops.

Card payments can work, but treat them as a separate operating model with different fees, disputes, and support load. The rail you choose should match how you want to operate when something goes wrong, not just when everything goes right.

Write your "minimum viable getting-paid spec"#

Write the smallest specification that makes payment operations reliable. This becomes your internal standard and client instruction baseline.

At minimum, define:

- Payout identity fields: legal beneficiary name, required account identifiers, and exact reference format.

- Operational visibility fields: where inbound statuses appear and how statements are exported.

- Escalation fields: what evidence packet you send if a transfer is held or returned.

Keep the spec short, but treat it as real. When you are tired, busy, or dealing with a client who "just needs to pay today," the spec prevents you from inventing a one-off process you later regret.

Decide on speed vs. risk (and be honest about tradeoffs)#

Fast settlement is useful, but speed without control can become expensive ambiguity.

A transfer can settle quickly and still trigger review. International routing can work well and still show timeline variance. The right decision is the option that keeps speed acceptable while making incidents easy to trace and resolve.

Use a two-axis lens:

- Speed: how quickly funds are usable when everything works.

- Control: how clearly you can trace, reconcile, and escalate when it does not.

You are not trying to maximize a single axis. You are trying to pick a point where both are acceptable for your business model and your support capacity.

Rule of thumb (freelancers + small teams)#

Prioritize in this order: reliability, traceability, then marginal fee improvement.

For most freelancers and small teams, clean naming discipline and stable instructions create larger gains than chasing small fee differences too early. Once operations are stable, compare provider costs and FX outcomes using your real invoice sizes and your real client mix.

If you run multi-currency flows, keep approved rails short and explicit. The Best Multi-Currency Accounts for Digital Nomads and Freelancers can help you compare the account types before you add another rail. Fewer rails with strong documentation usually beat many rails with weak controls, especially when you are the person who has to untangle exceptions.

The "basic payment account" option: when to use it, how to make it work, and what it won't do#

A basic payment account can be a practical path in some jurisdictions when standard onboarding fails. Use it as a targeted tool, not as a universal workaround.

Rights, eligibility, and provider responsibilities vary by jurisdiction. Treat this as an execution framework, not a guarantee. Your goal is not to win an argument. Your goal is to secure working payment functionality with minimal operational drag.

When this lever actually fits#

This path fits when your situation aligns with everyday access and your immediate need is basic payment functionality.

Use it when you can clearly show local legal residence where applicable and your requirement is straightforward receiving and sending. Skip it when your true need is formal business banking with multi-user controls, advanced workflows, or credit features.

A fit check that keeps you honest:

- Are you solving practical payment access, not premium features?

- Can you document residency and use case without gaps?

- Will this setup support your near-term invoicing flow?

If yes, it can be worth running in parallel with a backup rail so you are not betting cashflow on one outcome.

What it can do (operationally)#

Operationally, this route can turn a blocked "non-resident" conversation into a procedural review path.

In the right scenario, that can mean access to usable receiving details and standard transfer functionality. It can also support pushback when refusal is based only on living in another country rather than on risk, eligibility, or document quality.

Treat it like last-mile access. It can solve immediate receiving constraints when you fit the lane. It is not designed to replicate every business-account capability.

What it won't do (so you don't waste weeks)#

Set expectations before you start. Clear expectations reduce wasted cycles.

| Expectation | Reality to plan for |

|---|---|

| "This guarantees approval." | Banks can still refuse for risk, compliance, eligibility, or policy reasons. |

| "I'll get a full-feature account." | You may receive a limited setup with restricted extras. |

| "It will work as a business account." | The result may be personal-account oriented and not ideal for invoicing operations. |

If you need strong business banking features for operations, do not pretend this lever is the same thing. Use it for access, then build your broader setup around it.

How to make it work without making it a fight#

Run this path with a procedural packet, not a debate mindset.

Include only true, relevant evidence: current contracts or engagement letters, recent invoices or payment confirmations, and local ties such as studies, work assignment, lease, or property link when applicable. Keep the packet short and consistent so it can be reviewed quickly.

If refused, ask for the decision in writing or request a clear explanation in writing. Then ask for the formal complaint path and next escalation step in your jurisdiction. This keeps the process factual and auditable.

Most important, keep cashflow independent from this path by maintaining a working alternative rail while you pursue it.

Your application-ready document pack (and the bank inquiry script that prevents wasted weeks)#

Treat onboarding like an operations launch. A clean document pack and a short pre-check script can remove weeks of avoidable back-and-forth.

By this stage, you should already know your scenario and preferred rail. Now the goal is to submit a package reviewers can verify quickly, without interpretation games.

The standard document stack (built for "no surprises")#

Bring core documents plus one context page that answers predictable compliance questions. You are not trying to bury the reviewer. You are trying to make it easy to say "yes" without chasing you for clarifications.

| Document | Details |

|---|---|

| Primary ID | Government-issued photo ID, plus backup ID if available |

| Proof of address | A document type the provider explicitly accepts in your jurisdiction |

| Tax details | Your TIN if available and a short signed statement of tax residency position |

| Proof of activity | Contract, recent invoice, engagement letter, or portfolio evidence |

| Source-of-funds summary | One page covering what you do, typical inflow range, where clients are located, and usual sending countries |

That one-page summary is where you prevent confusion. Keep it plain-language. It should align with your invoices, your contracts, and your onboarding answers.

Your "single source of truth" naming rule#

Name mismatches are a common trigger for manual review and returned transfers. Fix this before invoice one.

| On your invoice | On the receiving account | Safe default |

|---|---|---|

| Individual name | Individual beneficiary | Match provider records as closely as possible. |

| Company name | Company beneficiary | Invoice and receive under the same legal entity. |

Write the rule once and enforce it across contracts, invoices, onboarding, and support tickets. If you ever change it, treat it like a migration, not a casual edit. Update everything, then run a controlled test payment before you assume the new state is stable.

The pre-application inquiry script (copy/paste)#

Do not start with a full application when a short message can disqualify a provider in minutes.

| Topic | Question |

|---|---|

| Inbound European bank transfers | Do you support inbound European bank transfers for my residency status and account type? |

| Proof of address | Which proof-of-address documents do you accept from my country, and is local registration required? |

| Inbound international transfers | Do you support inbound international transfers, and what fees or limits apply? |

| Held or returned transfers | What are common reasons inbound transfers are held or returned, and what documents clear those cases quickly? |

Send these four questions before applying:

- "Do you support inbound European bank transfers for my residency status and account type?"

- "Which proof-of-address documents do you accept from my country, and is local registration required?"

- "Do you support inbound international transfers, and what fees or limits apply?"

- "What are common reasons inbound transfers are held or returned, and what documents clear those cases quickly?"

Keep the replies. You are building a paper trail that your future self will need when the process shifts midstream.

Safe confirmation protocol#

Keep an evidence trail as you go. Save requirement pages and retain full support transcripts.

Requirements vary by provider and jurisdiction, and they can change. Your archive protects you when a process shifts mid-onboarding. It also speeds escalation because you can reference what you were told and when, without relying on memory.

Treat confirmation as part of the job, not as admin overhead.

Payment ops playbook: reduce avoidable payment friction before it happens#

Once your receiving path is live, consistency is your edge. Payment ops should run like delivery ops: clear inputs, standardized instructions, and fast verification.

Most friction is preventable when controls are applied before money moves. The goal is not perfection. The goal is reducing the volume of avoidable exceptions so you have time to handle the real ones.

The control that beats most chaos: name-match discipline#

Name consistency is the single most effective control in this workflow.

Lock one billing identity per contract. Invoice either as an individual or as a legal entity, and keep that choice stable. Ensure beneficiary details in payer workflows mirror your invoice identity and, where possible, provider records. Minor drift can trigger extra checks, requests for "clarification," or a returned transfer.

Use three operating rules:

- One approved legal name format for invoicing.

- One approved beneficiary name format for receiving.

- No ad hoc client edits unless the change is updated everywhere.

This is boring work. It also prevents the kind of chaos that burns a week.

Client-facing payment instructions (copy/paste template)#

Give clients one strict instruction block they can paste directly. Your goal is to reduce interpretation.

| Field | Template |

|---|---|

| Beneficiary name | Your legal name / legal entity name |

| IBAN | Your IBAN |

| Bank name | Bank name |

| BIC/SWIFT (if asked) | Your BIC |

| Reference (strict format) | INV-1047 | YourBrand |

Add non-negotiables in plain language:

- Do not edit the beneficiary name.

- Do not shorten or rewrite the reference.

- Do not split one invoice into partial payments unless agreed in writing.

Then enforce it. If a client asks "can we tweak the name," treat that as a red flag that their payable process may be about to create work for you.

Verify the route before you depend on it#

Before making any rail your default, run a controlled test and inspect what information survives end to end.

You are checking practical realities: which sender fields are required, which fields are optional, and how payer name and reference appear after receipt. Two providers can both claim support while giving very different inbound visibility.

A setup is not production-ready until it has been test-paid, observed, and reconciled. One clean test payment can save you from discovering a missing reference field on your largest invoice of the quarter.

Reconcile like an operator#

Reconciliation quality determines how quickly you can answer "what happened" and close your books without chaos.

A simple standard works:

- Put the invoice ID in every payment reference.

- Keep a compact evidence packet per payment: invoice, sender confirmation, and receiving-side transaction view.

- Log exceptions immediately so patterns surface early.

The real win is not a neat spreadsheet. The win is speed. When a payment is delayed or disputed, you can respond with facts in one message instead of hunting across inboxes and portals.

Two-rail resilience: your "primary + backup" setup so one freeze is less likely to stop cashflow#

Redundancy is not overengineering. It is cashflow protection.

A two-rail setup reduces the chance that one provider event pauses revenue. The goal is independence, not complexity. You want a primary path you use by default and a backup you can activate quickly without reinventing your instructions.

Pick rails that fail differently#

Choose rails with different failure modes so one issue does not disable both paths.

Your primary rail is usually standard euro credit transfer into your default receiving details. Your backup rail is a second provider path or an alternative method the client can execute quickly.

If clients can send instant transfers, instant payments in Europe are euro-denominated credit transfers that can settle within seconds and run continuously, based on SEPA Instant Credit Transfer (SCT Inst). Settlement can be handled through systems such as TARGET Instant Payment Settlement (TIPS).

| Rail | What it's best for | What to validate upfront |

|---|---|---|

| Standard euro credit transfer (bank transfer) | Predictable invoicing workflows | Reference retention, beneficiary details, who can initiate |

| SEPA Instant (SCT Inst) | Time-sensitive EUR payments | Provider support and sender-side limits |

| Alternate method | Edge cases when transfers are blocked | Sender steps and exportable proof |

Do not overbuild. Pick rails that you can explain to a client payable team in one paragraph.

Choose your backup based on your real risk#

Match backup design to your revenue pattern, not to what sounds sophisticated.

If you invoice high-ticket work, keep backup inside transfer rails where possible so operations stay consistent and auditable. If volume is higher and ticket size is lower, prioritize a backup customers can complete quickly, then tighten fulfillment proof and refund handling so you are not creating a different kind of operational risk.

Ask one blunt question: if your primary rail pauses tomorrow, which backup keeps obligations moving this week?

Where Gruv fits (without wishful thinking)#

If you already use Gruv for payment operations, treat it as an operations layer, not a workaround.

Use it where it improves control surfaces such as traceability, reconciliation workflow, and payment status visibility where enabled. Keep expectations tied to your process design.

Gruv can support execution discipline. It does not replace scenario fit, document quality, or payer instruction clarity. If you want fewer incidents, the upstream work still matters.

The true cost of "getting paid": fees, FX spread, and the operational cost nobody prices in#

Most operators underprice payment friction because they model only visible fees. That misses where margin typically leaks: conversion effects, delays, and time spent on exceptions.

A useful model combines direct charges, conversion outcomes, and internal time spent resolving incidents. The point is not to produce a perfect finance model. The point is to stop making decisions based on incomplete math.

Build a cost model that matches reality#

Start with monthly measurements from your actual transaction mix.

SEPA's mission is payment usability for cross-border euro transfers, not standardized provider pricing. Treat every low-fee claim as unverified until schedules and outcomes match real payments.

Also, do not rely on anecdotes. Qualitative stories can help you spot risk, but they do not price your system. Your own ledger does.

| Cost bucket | What to include | What to record each month |

|---|---|---|

| Account fees | Plan fees and add-ons | Plan name and total fixed fees |

| Transfer fees | Inbound, outbound, and trace charges | Fee by transfer type and count |

| FX conversion | Explicit conversion fee and effective received rate | Converted amount and effective rate |

| Operational overhead | Ticket volume and admin follow-up time | Minutes per incident and frequency |

Once you track this for a few cycles, you will see patterns. Those patterns tell you where to intervene.

Add the hidden costs you can't "negotiate" away#

Published pricing rarely shows time-to-open delays, repeated document requests, or incident response speed. Those are real costs because they delay cash and consume attention.

One missing transfer can consume hours across invoice lookup, beneficiary validation, reference tracing, and follow-up. Track these explicitly:

- Time-to-cash: invoice sent to funds usable.

- Incident handling time: time spent per payment issue.

- Escalation loop count: number of contacts before resolution.

Assign an internal hourly rate to this effort. Once you do, "cheaper" options often look different. A slightly higher visible fee can be the lower-cost option if it reduces exceptions and makes issues resolvable quickly.

Risk controls that reduce avoidable delays#

Reviews cannot be eliminated, but common self-inflicted triggers can.

Increase activity in steps when possible instead of abrupt jumps. Keep client-country mix described accurately during onboarding so pattern shifts are less surprising. Maintain one plain-language business description across forms, invoices, and statements.

These controls are not glamorous. They are high impact because they reduce the incidents that waste the most time.

When a transfer is held or returned: a triage workflow that gets answers (and money) faster#

When funds stall, structure beats urgency theater. Handle it like incident response: classify route, package evidence, ask precise questions, then close with one preventive fix.

This keeps escalation factual and resolution faster. It also reduces the chance you get stuck in support loops where each message asks you for something you already sent.

Step 1: Classify by rail (SEPA vs SWIFT)#

Start by confirming route and currency. Without this, every conversation stays vague.

In this context, payment rails are the infrastructure moving funds between banks and payment service providers. Two common lanes are:

- SEPA for euro-denominated payments across Europe.

- SWIFT as a network used for international transfers through financial institutions.

Use this triage view to align sender and receiver facts quickly.

| What you need to know | Ask the sender | Ask your provider |

|---|---|---|

| Rail + currency | "Was this sent as SEPA (EUR) or via SWIFT?" | "Which rail does this incoming payment route through?" |

| Sender reference | "What reference did you include?" | "What reference fields do you see on your side?" |

| Current status label | "What status do you see right now?" | "What exact status label is this case in?" |

Do not skip this step. If you do, you will spend days arguing about symptoms instead of diagnosing the route.

Step 2: Send one complete context packet#

Do not drip-feed information. Send a complete packet in one message.

Include the invoice or internal reference, beneficiary details you provided to the sender, sender payment confirmation, and your receiving-side view showing non-receipt or in-progress status.

Complete packets reduce loops. They also signal to support that you are prepared, which often changes the quality of the response you get.

Step 3: Escalate with calm, specific questions#

Escalation works best when requests are direct and answerable. Avoid broad asks like "why is this happening." Ask for the next operational move.

- "What do you need from me to progress this case?"

- "Which document formats do you accept?"

- "Can you assign a case number so we track this cleanly?"

- "What is the next operational step?"

These prompts move the conversation from general explanation to concrete action. They also create a written record you can use if you need to escalate further.

Step 4: Prevent recurrence with one system change#

Close each incident with one process improvement. Small fixes compound.

Depending on root cause, that fix may be stricter reference formatting, tighter beneficiary-name controls, or a client pre-brief on rail selection for EUR payments in Europe when available.

If your underlying objective is account access as a non-resident, expect difficulty to vary by provider and profile. Keep legitimacy documentation ready and keep your narrative consistent across every channel. The fastest way to reduce repeats is to treat each incident as feedback on your system, not as a one-off annoyance.

The "get paid from Europe" checklist (safe defaults) + what to do next#

Turn research into a system. Lock your rail, confirm your eligibility lane, and standardize execution before you scale volume.

This is where strategy becomes daily operating discipline.

Safe defaults (grounded)#

- Pick your rail first: SEPA is designed to make cross-border European payments function like domestic transfers. If SEPA is not available for a payer, define the alternate route in advance and do not improvise under deadline.

- Separate rights from outcomes: if legally resident in an EU country, a basic payment account route may be available, and refusal cannot be based only on living in another EU country.

- Assume process variation: onboarding requirements can differ by provider, jurisdiction, and account type. Treat every provider as its own process.

- Run one consistent identity narrative: names, addresses, residency position, and business description should match across systems.

- Maintain backup coverage: one primary rail plus one tested backup lowers single-point cashflow risk.

Execution checklist (operator version)#

- Write your scenario in one line: residency status, payer locations, and invoice currency.

- Choose a primary receiving rail and one backup that fails differently.

- Build a document pack with ID, address proof, tax details, activity proof, and source-of-funds summary.

- Send the pre-application inquiry script before onboarding.

- Publish one client payment instruction template and enforce strict beneficiary and reference formatting.

- Run a controlled test payment and verify what payer and reference data appears on your side.

- Track fees, FX outcome, and time-to-cash each month using real transactions.

- For every incident, run triage and log one preventive system change.

What to do next#

Prioritize reliability and auditability first. A slightly higher visible cost can be cheaper than one delayed invoice plus hours of manual follow-up.

Take three actions now. First, finalize your primary and backup rails for the next 90 days. Second, standardize your client-facing payment instructions into one non-editable template. Third, set a monthly review to track leakage, incident time, and reconciliation quality.

If your goal remains account access as a non-resident, keep that as a means, not the mission. The mission is steady EU cashflow with low operational drag.

Frequently Asked Questions

Can a non-resident open a bank account in Europe?

Sometimes, but treat it as case-by-case, not a guarantee. If you are legally resident in an EU country, you have a defined right to open a basic payment account. If you're not legally resident, focus on "get paid" rails first, then pursue account options that match your situation.

What is a "basic payment account" in the EU, and who is eligible?

A basic payment account covers standard daily transactions like deposits, cash withdrawals, and receiving/carrying out payments. If you are legally resident in an EU country, you are entitled to open one. Banks also can't refuse your application just because you don't live in the country where the bank is established. This right doesn't apply to other types of bank account, like savings accounts.

Can I open a European bank account online without proof of address?

Don't plan your cashflow around skipping documentation. Requirements vary across European banking providers and products, and you should expect verification steps. Build a backup receiving option so your invoicing doesn't depend on a "maybe."

Which documents do I need to open an EU account as a non-resident?

Don't rely on a universal checklist. Providers set their own requirements. What you can anchor on: if you qualify for a basic payment account, eligibility starts with being legally resident in an EU country. Ask the provider for an exact list before you invest time.

What's the best way to get paid by EU clients if I can't open an EU bank account?

Optimize for rails, not prestige. SEPA exists to make cross-border payments in Europe as easy as domestic transfers, so EU receivables can be smoother when your client can send a SEPA transfer. For multi-currency and routing strategy in international finance, use How to Get Paid in Multiple Currencies Without Losing Your Shirt.

Why was my EU bank transfer returned or put on hold?

Start by classifying the situation using what each side can actually see: rail used, currency, reference fields, and the current status label. Cross-border payments can involve multiple parties and checks, which can create delays even when the sender did everything correctly. Ask for the next required action, not a generic explanation.

Do I need an IBAN to invoice EU clients (and how do I handle IBAN discrimination)?

Whether you include an IBAN on an invoice depends on how your client is going to pay-but if they're paying via SEPA bank transfer, they may ask for it. IBAN discrimination means someone can't make or receive a SEPA credit transfer (or pay via SEPA direct debit) from an account located in another Member State. If it happens, file a complaint with the national competent authority where it occurred.

SEPA vs international transfers: which should I use to get paid?

Use SEPA when the sender can initiate a transfer within the SEPA system. If SEPA isn't an option for the payment, ask your provider which international transfer route will be used and what bank details are required. If your goal is "open european bank account non resident," default to the rail that reduces friction for your clients first. Optimize the account later.

Watch

Open a European Bank Account as a Non-Resident

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Best Multi-Currency Accounts for Digital Nomads and Freelancers

This shortlist is for cash flow decisions, not brand popularity. It is for freelancers, creators, and lean teams in the United States who need a cross-border payment setup that still works when real work hits: invoices go out, money lands, conversions happen on your timing, and urgent payouts do not depend on luck.

How to Get Paid in Multiple Currencies Without Forced FX

If you want to **get paid in multiple currencies** while protecting margin, separate collection from conversion. Receive the client's currency first, then decide if, when, and where to convert it.

How US Citizens Can Work Remotely in Europe Without Visa Missteps

Start with legal verification, not logistics: confirm your pathway first, assemble matching paperwork second, and book travel last. That order helps reduce avoidable delays.