Quick Answer

Start by deciding whether your facts support Dutch resident treatment or non-resident treatment, then map that position to the likely P-form, M-form, or C-form. For netherlands tax for expats, the safer path is to classify income by box before estimating, keep VAT records separate from personal return work, and confirm filing details with Belastingdienst. If your country ties or US obligations are unclear, get coordinated professional review before submitting.

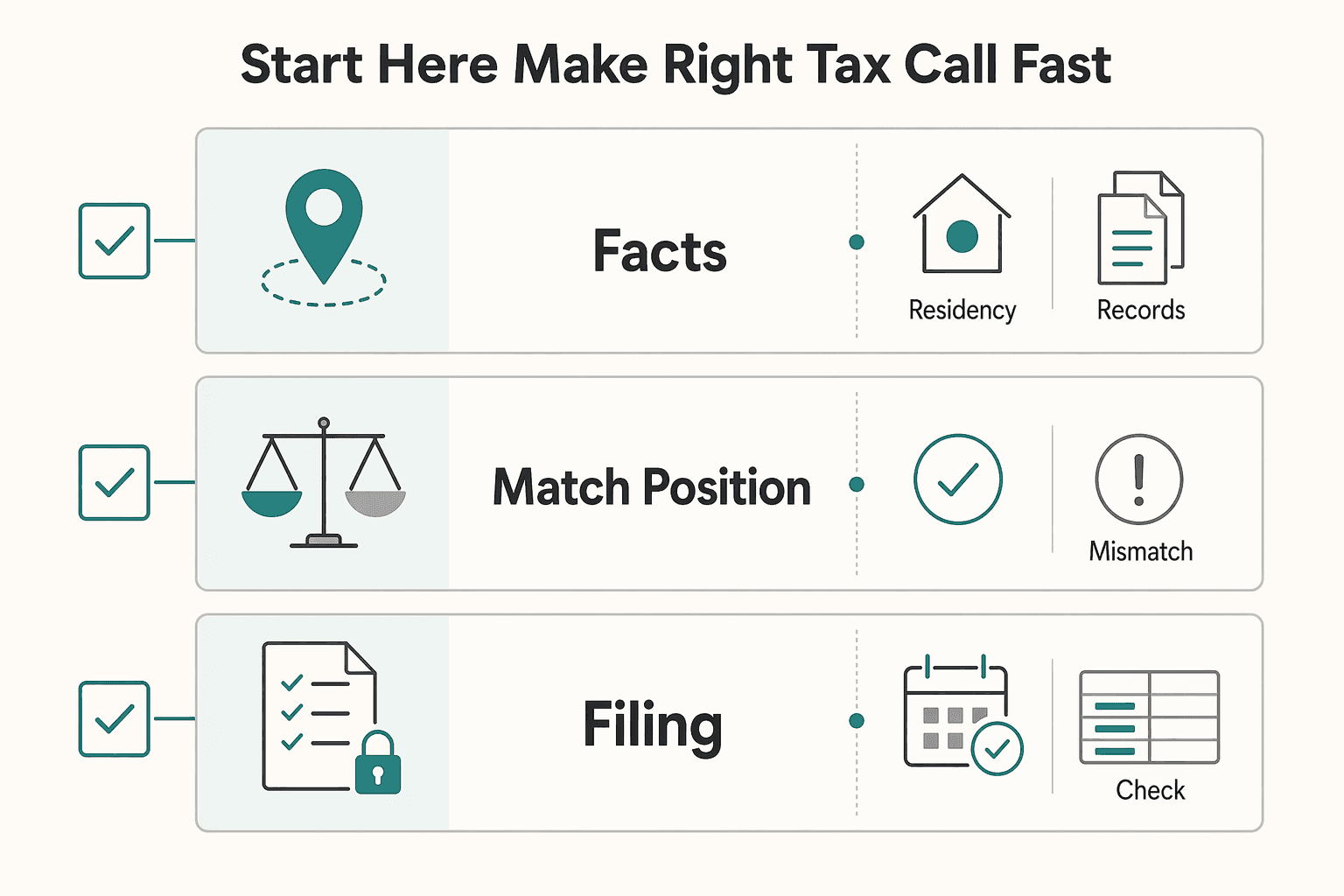

Start Here and Make the Right Tax Call Fast#

Make one decision first: are you filing on a Dutch resident track, or a non-resident track with Dutch income. Once that call is provisional, everything else gets simpler: choose the likely return path and gather the records that support it.

| Return form | Use when |

|---|---|

| P-form | Standard return |

| M-form | If you moved to or from the Netherlands |

| C-form | Non-residents with Dutch income |

This guide is for freelancers and consultants in the Netherlands. It is compliance-first, not tax-hack content. Employee-focused items, including 30% ruling documentation, matter only when they apply to your case.

In one sitting, aim to complete three actions:

- Choose a provisional filing position: resident track or non-resident track, based on your facts.

- Match that position to the likely return type:

P-form(standard return),M-form(if you moved to or from the Netherlands), orC-form(non-residents with Dutch income). - Build a first-pass evidence folder with filing essentials like BSN, DigiD access, and your savings and investments snapshot as of January 1 of the tax year.

Keep two boundaries in view. Form type helps with filing, but it does not prove legal residency status by itself. Freelancer filing logic is also different from payroll logic, so apply employee-style assumptions only when they clearly fit your case.

Before moving on, run one quality check: confirm your documents are complete enough to support each major return line. Missing evidence can undermine a filing even when the calculations look straightforward.

A practical move at this stage is to open a short unresolved-items note. List anything that could change filing position, form choice, or income classification, then assign each item a decision deadline. This keeps open questions from silently rolling into submission week.

Treat date-sensitive details as verification points for the current year. Filing windows are often shown as March 1 to May 1, with postponement requests by May 1, and older pages can be outdated. If your facts are mixed or cross-border and still unclear after this pass, escalate early for professional review.

If you want a deeper dive, read Amsterdam, Netherlands: The Ultimate Digital Nomad Guide (2025).

Define the Tax Terms That Control Your Outcome#

Definitions drive your outcome before rates do. Lock down residency status, income box classification, and VAT versus income tax treatment first. Dutch tax residency is the first term to settle because it controls whether Dutch income tax reaches worldwide income or mainly Dutch-source income.

You already chose a provisional track. Now translate that into filing language: organize the personal Dutch income tax return first. Form choice (P, M, or C) depends on your personal situation, so treat it as a filing detail after you establish the facts.

| Term | Practical meaning | Why it changes your outcome |

|---|---|---|

| Box 1 income | Salary, benefits, pensions, and profit from self-employment | Misclassifying core work income can distort the whole return |

| Box 2 income | Income tied to a substantial interest in a BV (generally at least 5% shares) | This income is treated differently from regular freelance profit |

| Box 3 income | Savings, investments, and certain second homes | Assets here follow different rules than work income |

These boxes are not labels to sort out later. Each has different rules, rates, and deductions, so categorization comes before calculations. If your profile mixes freelance invoices, BV ownership, and investment income, get a classification review early.

VAT is separate from income tax. As a freelancer, VAT reporting can run quarterly, while personal income tax filing follows its own annual cycle. Paying or collecting VAT does not settle your personal income tax position.

One way to reduce rework is to keep two ledgers in parallel from the beginning: one for income-tax box candidates and one for VAT reporting lines. When the same invoice appears in both places, your year-end cross-check is usually faster and cleaner.

Use this checkpoint before moving on:

- Tag each income line as a Box 1, Box 2, or Box 3 candidate before doing calculations.

- Keep a separate VAT ledger for VAT returns, independent from personal income tax totals.

- Keep records for at least seven years so return lines can be traced to invoices, statements, and costs.

Decide Your Residency Status Before You Do Anything Else#

Residency is the first high-impact call because it sets filing scope. Make this call before you build your tax-year plan.

Use this order:

- Gather your facts: permanent home, where you actually work, where close family lives, local registration details, where key bank and assets are held, and intended length of stay.

- Assess Dutch tax residency from the full facts-and-circumstances picture, not one indicator.

- Validate your filing position before you finalize your Belastingaangifte approach, especially if your facts are mixed across countries.

When facts are unclear, use a conservative rule. If your ties strongly point to the Netherlands, plan as resident first. If your ties are split across countries, treat status as unresolved and escalate early for professional review.

A common failure mode is treating Municipal Personal Records Database registration and a BSN as decisive. They are indicators, not a formal residency conclusion. In disputes, broader personal ties, and to a lesser extent economic ties, are reviewed. You may need practical evidence such as utility bills to support your position.

Before taking a non-resident filing position, run a hard check: do your overall facts support non-resident treatment, and have you tested whether Dutch tax still applies to specific Dutch-source income. Non-resident does not automatically mean no Dutch liabilities. If two countries can both claim residency in the same year, treaty analysis may be needed.

In practice, this decision is easier when each key tie has matching records in your folder. For example, if you list living location, include lease or utility support. Keep your evidence consistent across the facts you rely on.

Keep two guardrails in view. A single person staying in the Netherlands for more than one year is generally treated as resident, so long stays need extra caution before a non-resident filing position. Also, qualifying non-resident taxpayer treatment may require 90% or more of income to be subject to Dutch wage and income tax, plus other conditions, so do not assume resident-like benefits apply by default.

Before locking in resident vs non-resident status, run your facts through the Tax Residency Tracker and store the result with your filing evidence.

Separate Employee Expat Rules From Freelancer Reality#

Treat employee expat benefits and freelancer filing mechanics as separate tracks. Mixing them is where planning can break down.

Employee-focused guidance on the 30% ruling and related expat treatment can matter for payroll roles, but it does not automatically carry over to self-employed planning. If you are freelancing, start with residency scope, return preparation, and income classification across Box 1, Box 2, and Box 3.

- If you are on payroll with an employer and think

30% rulingcould apply, verify current-year assumptions before you budget net pay. - If you are a solo freelancer, prioritize residency status and filing mechanics first, then layer in benefit assumptions only after confirmation.

Partial nonresident taxpayer treatment can also be an error point. Do not assume it applies. Build your plan without it first, then include it only if your current-year position is clearly supported.

| Profile | First tax focus | Common planning mistake |

|---|---|---|

| Payroll hire under an employment contract | Check payroll-linked expat assumptions first, then align the annual Dutch income tax return | Assuming payroll benefit logic also covers freelance activity |

| Location-flexible consultant billing multiple countries | Lock residency and filing scope first, then classify income and prepare return evidence | Building around expat-benefit assumptions instead of filing mechanics |

One filing baseline still matters: if you live and work in the Netherlands, you must file a Dutch income tax return. If you are treated as a resident, Box 3 can include worldwide savings and investments above the applicable threshold for the year. For the 2025 tax year, the stated thresholds are €57.684 per person and €115.368 for fiscal partners, measured on January 1, and authorities assess both fictional-return and real-return methods, then apply the more favorable outcome.

Mixed years need extra discipline. If you moved from payroll into freelance work during the same tax year, separate those income streams early and label every assumption by source. That keeps employee-rule references from bleeding into self-employed treatment.

Before locking the plan, verify three points:

- Is your year payroll-only, freelance-only, or mixed.

- Does any partial nonresident assumption have current-year support.

- Does your filing plan still hold if no employee-focused expat benefit applies.

Understand Box 1 Box 2 and Box 3 Without Guessing#

Classify income first, then estimate tax. Dutch personal income tax is split into three boxes, and each box has different rates. Rate-first planning can produce precise numbers on the wrong base.

| Box | What it covers | What to tag before calculations |

|---|---|---|

| Box 1 income | Business and employment income, plus income from home-ownership of a main private residence | Contracts and invoices, bookkeeping totals, and relevant home records |

| Box 2 income | Income and gains from substantial shareholdings | Shareholding records and transaction support |

| Box 3 income | Income from savings and investments | Year-end account statements and investment summaries |

Outdated rate tables can be a failure point. Even with correct classification, old box-rate charts can distort your estimate. This is especially sensitive in Box 3: a new bill was presented on 19 May 2025 and, if enacted, is scheduled for 1 January 2028, with a shift toward taxing actual returns and added complexity that requires careful handling.

Run one hard checkpoint before you finalize estimates: if your income spans multiple boxes or multiple entity structures, pause DIY and get a professional classification review.

Ambiguous lines should stay visible until resolved. If a line item might fit more than one box, do not force it into the nearest category just to finish the draft. Mark it clearly, keep the supporting documents next to it, and resolve classification before rate modeling.

Quick pre-estimate checklist:

- Build one master income list for the year and assign a provisional box to each line.

- Flag uncertain lines instead of forcing a guess.

- Keep rate lookup separate until box assignment is complete.

- Recheck Box 3 assumptions against the current filing-time position.

- Note why each ambiguous line was assigned to a box.

Use the 30 Percent Ruling Facts Without Overplanning Around It#

Treat the 30% ruling as a secondary assumption, not the base of your plan, until you confirm current official Dutch tax-administration guidance for your exact setup.

In this research set, one explicit 30 percent reference is tied to U.S. withholding, not Dutch expat treatment. This pack does not establish Dutch eligibility, percentages, caps, duration, or procedures. Do not copy percentage assumptions across tax regimes. If a source does not clearly map to Dutch tax administration, leave it out of your working model.

Before modeling compensation, run this go or no-go check:

- Confirm current terms directly in official Dutch tax-administration guidance for the relevant tax year.

- Record the publication date and tax year for each rule you rely on.

- Check that your contract setup matches the assumptions in your model.

- Keep policy notes, procedure documents, and related training materials with your tax return working file.

Keep the tradeoff clear: over-optimizing one benefit can hide larger residency and filing risks. If residency status is still unresolved, settle that first and only then optimize compensation details.

If your work arrangement changes, rerun the same check with current official guidance before updating cash-flow expectations.

A useful guardrail is to write one sentence next to each benefit assumption: what document supports it, and what happens if it falls away. If removing that assumption breaks your filing plan, you are still planning too close to the edge.

Build Your Filing Calendar and Form Stack#

Treat filing as a sequence: close records, draft with complete data, then submit.

| Date | Planning point |

|---|---|

| March 1, 2026 | Submissions are typically described as opening |

| April 1, 2026 | Filing before this date is linked to a general target of assessment before July 1, 2026 |

| May 1, 2026 | Standard filing deadline |

Use this order each year so deadline choices are based on finished records: close your books, organize your entries, prepare your Belastingaangifte draft, then submit your Dutch income tax return.

For the 2026 filing season (2025 tax year), use the dates above as planning guidance, not guarantees.

If your filing situation is unclear, confirm the exact return form directly with the Belastingdienst before submission.

If you might need extra time, check current options with the Belastingdienst before the standard due date and log what was confirmed and when.

Keep records organized and resolve missing items early.

Add one timing checkpoint in early April: if key lines or supporting evidence are still unresolved, pause polishing and close those gaps first.

Handle US Overlap Without Double Counting or Missed Filings#

Treat US and Netherlands overlap as one coordinated effort from day one, especially when the same earnings could trigger social security in both countries.

Keep the records separated but the logic aligned. Social security coordination is one question, and income-tax coordination is another. If your year includes both US-side and Dutch-side filing work, build one shared income map, with payer country, contract type, and where contributions were withheld, before anyone finalizes numbers.

Use the US-Netherlands Totalization Agreement when the issue is social security overlap. Totalization agreements are meant to avoid dual social security taxation by assigning coverage to one country and exempting employer and employee social security taxes in the other. The US-Netherlands social security agreement has been in force since November 1, 1990.

Keep income-tax analysis separate from totalization so you do not mix assumptions.

Execution can fail at certificate handling. If you are claiming a totalization-based social-security exemption, the Certificate of Coverage is the proof document, and the SSA provides an online request path for employers and self-employed individuals.

Use this checkpoint list before locking drafts:

- Submit the certificate request early and save confirmation.

- Complete all required fields or the request cannot be transmitted.

- Use the request-status search instead of guessing from silence.

- Allow 90 business days before routine follow-up.

- If a certificate is issued, allow up to two weeks for mailing.

One failure mode is document timing mismatch: one advisor finalizes return assumptions while certificate status is still uncertain. Avoid that by recording certificate status directly in your shared fact pattern and requiring both sides to work from the same version.

If you have mixed-source income and parallel US and Dutch filing work, require one reconciled fact pattern across advisors instead of separate assumptions. If a DAFT move is part of the plan, raise tax and social-security coordination questions early and align planning timing with visa timing; see The Netherlands DAFT Visa for American Entrepreneurs.

Prepare an Audit-Ready Evidence Pack Before Filing Season#

Lock records behind each number before filing. Weak documentation leads to rework, so build one evidence pack per tax year and treat draft figures as provisional until they are supported.

| Document group | What to keep |

|---|---|

| Residency records | Records you rely on for your status position for the year |

| Contracts and invoices | Signed contracts, amendments, and invoices with issue dates and client names |

| Payment evidence | Bank statements plus invoice confirmations, payout records, and reconciliation artifacts exported from Gruv where supported |

| VAT support and unresolved log | Support for how you treated VAT-relevant transactions, plus a short unresolved-items log |

Keep those four document groups together.

Use a line-trace check before submission. For each material line in your return, check amount, date, and counterparty against stored evidence. If support is missing, mark it unresolved and pause filing until clarified.

If the 30% ruling is part of your year, keep a dedicated subfolder with employment start-date evidence and payroll records showing how the allowance was applied. The 30% ruling provides a tax-free allowance of up to 30% for qualifying employees, with 70% still taxed, for up to five years, and mistakes can create financial and compliance problems.

Treat public explainers as orientation, not final authority. If your filing depends on a narrow interpretation, get qualified professional review before locking numbers.

If you are also handling US catch-up, keep those records in a parallel archive instead of mixing them into Dutch folders. The streamlined path described here points to three years of tax returns and six years of FBAR records.

A small process detail can save hours later: use consistent file names that start with date and counterparty, then add a short description. When support is requested for one return line, you can pull the exact document quickly instead of searching through unsorted exports.

Red Flags That Mean You Should Escalate to a Professional#

Escalate before filing if your position is not clearly defensible from your records. The most expensive mistakes here usually come from an unclear position, not a math error.

Use this quick check: if you cannot explain each item in plain language and back it with documents, treat that as a stop signal.

- You cannot clearly explain which country should cover your Social Security for this work period.

- You have U.S.-Netherlands overlap and are still unclear whether totalization rules assign coverage to one country for the same earnings.

- You have not submitted a Certificate of Coverage request even though coverage assignment affects your year.

- You submitted a request but required filing details were incomplete, or you cannot track where it stands in the SSA status flow.

For U.S. overlap, keep scope tight: totalization agreements address Social Security coverage and can prevent dual Social Security taxation on the same earnings. They are not a complete income-tax answer on their own.

If Social Security coverage assignment affects your year, request a Certificate of Coverage early. Employers and self-employed individuals can request online, required fields must be complete before submission, and you can track checkpoints like Received and Completed, with decisions sent by mail or email. SSA asks you to allow 90 business days before follow-up, and mailing can take up to two weeks after issuance. The portal also notes web submissions are not risk-free, so keep copies of what you submitted in your annual evidence pack.

Escalation works best when you bring a clear question set, not just a folder dump. State what you believe, what evidence supports it, and what remains uncertain. That helps a reviewer give a decisive answer instead of charging time to rebuild your case from scratch.

If any red flag remains, book one coordinated professional review and bring one packet: your coverage timeline, submitted Certificate of Coverage details, current SSA status, and any decision notices you have received. For treaty-focused prep before that meeting, see How to Legally Avoid Double Taxation: A Freelancer's Guide to Tax Treaties.

Conclusion and Your Next Compliance Move#

You have enough to build a compliance-first filing plan. Lock down what you can defend with documents before you optimize.

Use this sequence in order:

- Set your year scope and filing clock.

Use the Dutch tax year as the calendar year, ending 31 December, and plan to file personal income tax before 1 May of the following year. If timing is tight, check extension eligibility early, since an extension of up to one year may be possible when conditions are met.

- Confirm your form path before drafting returns.

C/M/P forms apply to different personal situations, so map facts first and choose form path second. If your situation changed during the year, flag it early and escalate for review before final submission.

- Treat 30% facility assumptions as document-dependent.

The 30% facility context here is employee-based and tied to a labor contract with a Dutch employer. The process requires an upfront ruling, includes a labor contract copy, and requires a Dutch address and BSN. If this benefit affects your plan, recheck current-year terms before locking payroll assumptions.

- Compare actual alternatives.

Employers can either apply the 30% ruling or reimburse actual extraterritorial expenses, and reimbursement can be more favorable in some situations. Run both paths with real costs instead of assuming the headline allowance is best.

As a final check, reopen your unresolved-items note from the first section and close every line or escalate it. Once that list is clear, your filing plan should be stable enough to execute without last-minute rewrites.

This week, complete your personal-situation decision memo and your evidence checklist. If any red flag is still open after that pass, book one coordinated professional review before filing.

After you finish the decision memo and evidence checklist, use Gruv Tools for your next compliance tasks.

Frequently Asked Questions

Am I a Dutch tax resident or a non-resident taxpayer?

Dutch tax residents are generally taxed on worldwide income, while non-resident taxpayers are taxed only on specific Netherlands-source income. Residency is determined from all facts and circumstances, not one datapoint. Formal municipal registration alone is not enough. If your ties are mixed and more than one country may treat you as resident, escalate before filing.

What is the normal Dutch tax filing deadline and when can extensions apply?

A commonly listed Dutch return due date is 1 May, and the tax year runs from January 1 to December 31. For residents, Belastingaangifte is identified as the primary filing form. Extensions can apply in certain cases, but they are not automatic. Confirm your timing directly with Belastingdienst.

Do expats in the Netherlands pay tax on worldwide income?

If you are treated as a Dutch tax resident, worldwide income is in scope for Dutch income tax. If you are treated as a non-resident taxpayer, taxation is limited to specific Netherlands-source income. US citizens living abroad still have a US filing obligation. Keep treatment consistent across filings so positions do not conflict.

How should I think about Box 1 Box 2 and Box 3 as a freelancer?

Review Box 1, Box 2, and Box 3 separately before you estimate. Do not rely on one article or one outdated rate table. Some guides include 2024 example rates, but those should not be used as a current-year default without confirmation. If income could reasonably fit more than one box, get a professional review before filing.

How does the 30% ruling change over time, and who should care most?

The Expat Scheme is conditional and not automatic. It applies to paid employment with an employer, and you can apply only if you meet all conditions. Thresholds change by year, including EUR 48,013 in 2026 for the standard specific-expertise threshold and EUR 36,497 for people under 30. Anyone planning around this benefit should recheck current-year criteria before locking payroll assumptions.

If I am a US citizen in the Netherlands, do I still file a US tax return?

Yes. Americans living overseas still have to file a US tax return and report worldwide income. An American living in the Netherlands will probably also need to file a Dutch tax return. If your cross-border position is not clear, get coordinated advice before submission.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- irs.gov/individuals/international-taxpayers/totaliza...trusted

- taxation-customs.ec.europa.eu/system/files/2020-01/tax_policies_in_the_eu_...trusted

- taxpayeradvocate.irs.gov/wp-content/uploads/2024/01/ARC-2023_FullBook...trusted

- aangifte24.com/en/netherlands-tax-for-expats-a-comprehensiv...external

- agn.org/insight/the-netherlands-30-tax-ruling-what-e...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Netherlands DAFT Visa for American Entrepreneurs

**The Netherlands DAFT visa is a residence permit path for U.S. citizens under the Dutch-American Friendship Treaty. It works best when you treat it like an execution problem, not a research hobby.** Your job is not to "learn DAFT." It is to run a sequence that ends in an IND-ready file and a business that already looks real on paper.

Amsterdam Digital Nomad Guide for a 2026 Move

The smartest way to plan this move is simple: get legal clarity first, then start spending. That habit saves more money and stress than any packing checklist or neighborhood deep dive. If you cannot clearly name the legal basis for your stay and the documents that support it, hold off on flights and long housing commitments.

How Freelancers Can Legally Avoid Double Taxation With Tax Treaties

Classify the tax problem before you touch a return. If your income is mostly personal service fees across borders, this guide fits. If your issue is C corporation profits and shareholder dividends, you are solving a different problem.