Quick Answer

Stop margin erosion by locking one formula, building a clean baseline, tracking leakage client by client, tightening contracts and invoicing, and choosing payment rails by net impact instead of habit. Review the same inputs weekly and monthly, include owner labor and payment friction in your model, and fix the biggest repeat leaks before changing rates.

Revenue Can Hold While Margin Slips#

Revenue can hold steady while the business underneath it gets weaker. What comes in matters, but what you keep after the work is delivered is the clearer signal of health.

Set the definitions once and use them the same way every month. Revenue is total client income. Costs are what you spend to deliver the work and run the business. Profit margin is (Revenue - Costs) / Revenue.

This guide follows the order that usually works best in practice. Start with a baseline you can trust. Lock one formula so month-to-month comparisons actually mean something. Then find the leaks in the money flow, protect yourself in the contract before work starts, tighten invoicing and payouts, and review the whole picture on a fixed cadence.

Before you change rates, accept broader scope, or switch tools, do three things first:

- Lock one margin formula and apply it to every client.

- Track income and costs the same way each month so results stay comparable.

- Review margin on a schedule and tie changes to recorded inputs.

That is not administrative busywork. It is how you avoid reacting to noise. If you cannot explain a drop from your own records, clean the inputs first and decide second.

Gather Your Baseline Inputs Before You Change Anything#

Do not change pricing or terms from a blurry baseline. When the starting point is weak, every fix is guesswork, and tracking errors get expensive quickly.

| Input | What to include | Note |

|---|---|---|

| Marketing costs | Pull all marketing costs for the period and break them out by channel in one sheet | Do not include just ad spend |

| Recurring small costs | Include recurring small costs as line items | Do not roll them into miscellaneous totals |

| Revenue attribution | Capture revenue attribution for each customer | See which sales came from which marketing source |

| Customer counts and CAC | Add customer counts by channel and calculate CAC | channel spend / customers generated |

| Unclear entries | Mark missing or unclear entries as provisional | Avoid major pricing or terms changes from provisional rows |

Start with one working spreadsheet for one consistent reporting period. Give each expense category its own column. If you spend to generate work, pull every marketing cost for the period into that sheet, not just ad spend. Small recurring tools and services matter here. If they help you win clients or serve them, they belong in the baseline instead of disappearing into a miscellaneous bucket.

The goal is not a perfect finance system. It is a clean operating view that lets you see what changed, where it changed, and whether the result was real.

Use a simple capture method, but make it complete:

- Pull all marketing costs for the period and break them out by channel in one sheet.

- Include recurring small costs as line items instead of rolling them into miscellaneous totals.

- Capture revenue attribution for each customer so you can see which sales came from which marketing source.

- Add customer counts by channel and calculate CAC for each channel (

channel spend / customers generated). - Mark missing or unclear entries as

provisionaland avoid major pricing or terms changes from provisional rows.

Before you trust the sheet, run two quality checks. First, confirm each channel has complete cost entries for the full period. Second, confirm the sheet includes channel-level costs, customer counts, and CAC so return is measured instead of assumed.

Treat attribution as operating data, not a nice-to-have detail for later. If it is not being captured consistently, add a required intake field such as "How did you hear about us?" so future rows stay usable. A common failure mode is having spend data without clear source attribution for the revenue that followed. Once that happens, you cannot tell whether a weak result came from pricing, channel quality, or missing data.

It also helps to separate confirmed rows from provisional ones as you go rather than trying to clean everything up at the end of the month. That way, when you review the numbers, you already know which conclusions are safe to act on and which still need verification. This is especially useful when you are tempted to make fast pricing changes after a rough period. If the row is provisional, the decision should wait.

This baseline becomes the reference point for everything that follows. If someone asks why you changed pricing, terms, or channel mix, the sheet should show the pattern that forced the decision. Once the baseline is clean, freeze the formula so the trend line starts to mean something.

Set a Margin Formula That Reflects Freelance Reality#

Pick one formula and keep it fixed. If the definition changes month to month, the trend stops being useful and your decisions start chasing the latest story instead of the actual pattern.

Use these core equations:

Gross profit = Revenue - Cost of salesGross margin = (Gross profit / Revenue) x 100

The arithmetic is simple. The harder part is cost-scope discipline. Decide what counts as direct cost and what belongs in overhead, then keep that treatment consistent across reviews. Do not move costs in and out of categories just because one month looks better that way. A clean trend is worth more than a flattering one.

That consistency matters even more when you are comparing clients or deciding whether a service line still works. If your cost definition shifts every time you review the numbers, you are not comparing performance. You are comparing different accounting choices.

Then connect it to pricing. Use your annual business expenses and realistic billable working hours, after non-billable days, to set a minimum workable rate and adjust from there. If you need the full method, use How to Calculate Your Billable Rate as a Freelancer.

A simple example shows why this matters. At $100 billed and $50 costs, gross margin is 50%. If costs rise to $55 and price stays $100, margin drops to 45%. Even if billings move to $105, margin is still about 47.6%, which is below the starting point. More revenue did not solve the problem because cost rose faster than the price did.

That is why margin review should sit alongside pricing decisions, not behind them. If scope grows, delivery gets slower, or payment friction starts eating into the net, the formula should reveal it before the issue becomes a habit.

Use the model as a recurring checkpoint rather than a one-time calculation. When costs or scope change, run the same method before you agree to new terms. If the updated terms push margin below your floor, you have a concrete reason to reprice, reduce scope, or walk away. Once the formula is locked, you can stop debating definitions and start looking for the actual leaks.

Find Where Margin Erosion Actually Happens#

Most erosion is not mysterious. It usually shows up in the same few leaks once you reconcile invoiced amounts to net cash.

The cleanest way to see it is client by client. Build a leakage ledger with one row per client and one period per row. That keeps delivery overruns, payment friction, and documentation failures visible in the same place instead of scattered across email, payment dashboards, and memory.

What matters here is retained value, not just invoice totals. A project can look fine at the top line and still underperform once you account for discounts, fees, revision spillover, and payment trouble after delivery.

Set up the ledger to capture the losses that actually change what you keep:

- Record invoiced amount, discounts, processor fees, refunds, dispute losses, write-offs, late-payment delay, revision overrun, and urgent out-of-scope work.

- Check contract drift before blaming pricing. Mark each overrun as approved, unapproved, or unclear based on what the contract allowed at delivery.

- Audit payment friction by rail from your own records. Track paid timestamp, funds-available timestamp, and net received amount.

- For Wise, test method-specific pricing before deciding. Wise says fees vary by currency and start from

0.57%for sending, shows a fixed6.11 USDfee for receiving USD wire and Swift payments, and says discounts are applied automatically after25,000 USDequivalent sent in a month, whether in one or multiple transfers, with savings for the rest of the month and a reset on the first. - Prioritize fixes by cash impact and repeat frequency, then start with the highest-impact issue first.

- Keep an evidence pack for high-loss clients: invoice history, fee line items, dispute notes, and approval records for extra work.

Add one more field that makes the ledger much more useful: root cause. Use labels such as pricing, term failure, scope drift, payment friction, or documentation gap. Without that, it is easy to reach for a rate increase when the real problem is weak approvals, slow invoicing, or a payment rail that keeps reducing the net.

In practice, root-cause labels also make follow-up cleaner. If the problem is scope drift, the next action belongs in your approval process. If the problem is payment friction, the next action might be a rail change or a contract update. If the problem is documentation, the fix is operational, not commercial. That distinction saves a lot of wasted effort.

Use a simple impact rule so your cleanup time goes where it matters. Rank each leakage type by estimated monthly loss and repeat count, then start with the issue carrying the highest combined burden. This keeps you from spending hours fixing edge cases while a larger recurring loss keeps running every month.

The evidence pack matters more than most people expect. Memory is a weak audit trail, especially after a difficult client cycle. Keep invoice records, fee details, dispute notes, and approval trails together for each high-loss client. If a leakage line is not documented, treat it as provisional until verified. That sounds cautious, but it prevents you from changing policy based on half-remembered frustration.

A common failure mode is treating late payment as separate from margin. Delay still changes retained value because cash arrives later and may become harder to collect. Track delay beside fee and dispute lines so the picture reflects what you actually kept, not just what the invoice said.

There is also a sequencing benefit here. Once the ledger is built, contract changes stop being abstract. You are no longer adding terms because they sound protective. You are adding them because the ledger showed exactly where money kept leaking. That makes the next step much easier.

Lock In Contract Terms That Protect Margin Upfront#

The cheapest leak is the one you prevent before work begins. Clear contract terms do that better than after-the-fact negotiation ever will.

| Clause | Default use | Process link |

|---|---|---|

| Deposit clause | For new clients and large milestones when it fits your risk policy | Map deposit language to kickoff rules |

| Payment terms | Make due dates, accepted methods, and what happens when invoices go unpaid explicit | Map payment terms to reminders and escalation |

| Revision limit clause | Separate revision work and new scope in writing | Map revision limits to change-request approval |

| Pause-work clause | Tie it to missed payments and apply one internal trigger rule consistently | Map pause-work language to clear stop and restart conditions |

| Change-request addendum | Use a standard change-request addendum | Approve and price extra work before it is scheduled |

Use these protections as defaults for new engagements. When one client gets one version and another gets a looser version with no clear reason, enforcement gets inconsistent and your own decisions turn subjective. A standard starting point makes follow-through easier and gives you a cleaner basis for exceptions.

Make these protections part of the default package:

- Include a Deposit clause for new clients and large milestones when it fits your risk policy. If a client declines, document any scope, timeline, or milestone changes before you proceed.

- Make Payment terms explicit with due dates, accepted methods, and what happens when invoices go unpaid.

- Set a clear Revision limit clause so revision work and new scope are separated in writing.

- Add a Pause-work clause tied to missed payments, and apply one internal trigger rule consistently.

- Use a standard change-request addendum so extra work is approved and priced before it is scheduled.

If your terms reference federal rules, verify FederalRegister.gov text against an official Federal Register edition, including the linked govinfo PDF, and do not treat IRS bulletin synopses as authoritative interpretations.

The clause itself is only half the protection. Each one needs a matching operating action. Deposit language should map to kickoff rules. Payment terms should map to reminders and escalation. Revision limits should map to change-request approval. Pause-work language should map to clear stop and restart conditions. If a clause cannot be carried through in the actual process, it will not protect you when the relationship gets tense.

That is where many contracts fail in practice. The wording looks solid, but the team never uses it consistently. A pause-work clause means very little if no one has decided what overdue point triggers the pause, who sends the notice, or what has to happen before work resumes. Good terms need operational legs.

Negotiation usually goes better when you explain the delivery reason behind the clause. Do not argue from principle alone. Show how the term creates predictability for both sides. If a client pushes back on a deposit or revision limit, offer a scoped alternative such as smaller milestones or tighter deliverables instead of dropping the protection entirely. That preserves the business purpose of the clause without turning the conversation into a fight over trust.

Store the signed contract and every addendum in the same place as invoices and delivery records. Fragmented storage creates enforcement drift because no one can quickly confirm which version governs the work. When a question comes up about scope, due dates, or pause rights, the answer should be easy to verify.

Treat exceptions as deliberate decisions too. If you waive a clause for a client, log why, what changed, and what risk you accepted. Otherwise one-off concessions start to look normal, and before long the exception becomes your unofficial default.

Once terms are solid, invoicing has to carry them through cleanly. Good contracts lose value fast when the billing process is slow, vague, or inconsistent.

Rebuild Your Invoicing Workflow to Reduce Delay and Disputes#

Invoice speed and clarity usually matter more than minor wording tweaks. A well-timed, well-structured invoice protects value you already earned and makes the contract enforceable in real life.

Before you bill, confirm three basics are in place: itemized services, clear payment terms, and a due date on the invoice. If one is missing, fix it before sending. Small omissions create review delays, extra questions, and slow payment for no good reason.

Keep the workflow simple and repeatable:

- Issue invoices promptly. Delays in invoicing can delay when payment starts.

- Use itemized line items. Keep each entry specific so clients can see exactly what they are paying for.

- Communicate early. Early communication can reduce payment trouble later.

- Keep records organized. Track invoice history and payment communications in one place.

The practical standard is this: line items should be clear enough that an outsider could map each one to delivered work. Vague descriptions create avoidable review cycles, and every review cycle slows payment. It is almost always cheaper to make the invoice clearer on day one than to explain the same work two or three times after the due date.

Timing matters just as much. A well-written invoice sent late still delays the clock. If you already know the milestone is complete, bill it promptly and keep that timing consistent. Otherwise you create your own cash drag and then misread it as a client issue.

Follow-up needs the same discipline. Use a consistent approach for unpaid invoices instead of improvising tone and timing client by client. Early, calm follow-up sets expectations before a balance turns into a bigger process problem. It also gives you cleaner records if the issue later becomes a dispute about what was sent, when it was sent, and what response you received.

Add two verification checks to every invoice cycle. First, confirm the invoice was sent to the right contact and received when possible. Second, confirm payment status is recorded before follow-up. These checks sound basic, but they prevent a surprising amount of wasted time chasing an invoice that never reached the approver or was already paid through another path.

If a client repeatedly asks for longer terms, treat that as a cash-flow tradeoff and price accordingly. Net 30 is common but can still create a long wait, and Net 60 is often a poor fit when you need faster cash flow. The point is not that one term is always wrong. It is that longer timing has a cost, and your business should recognize that cost instead of absorbing it by default.

Once the invoice is clean and the follow-up pattern is stable, the next decision is the payment rail. That choice affects what you actually keep more than habit usually admits.

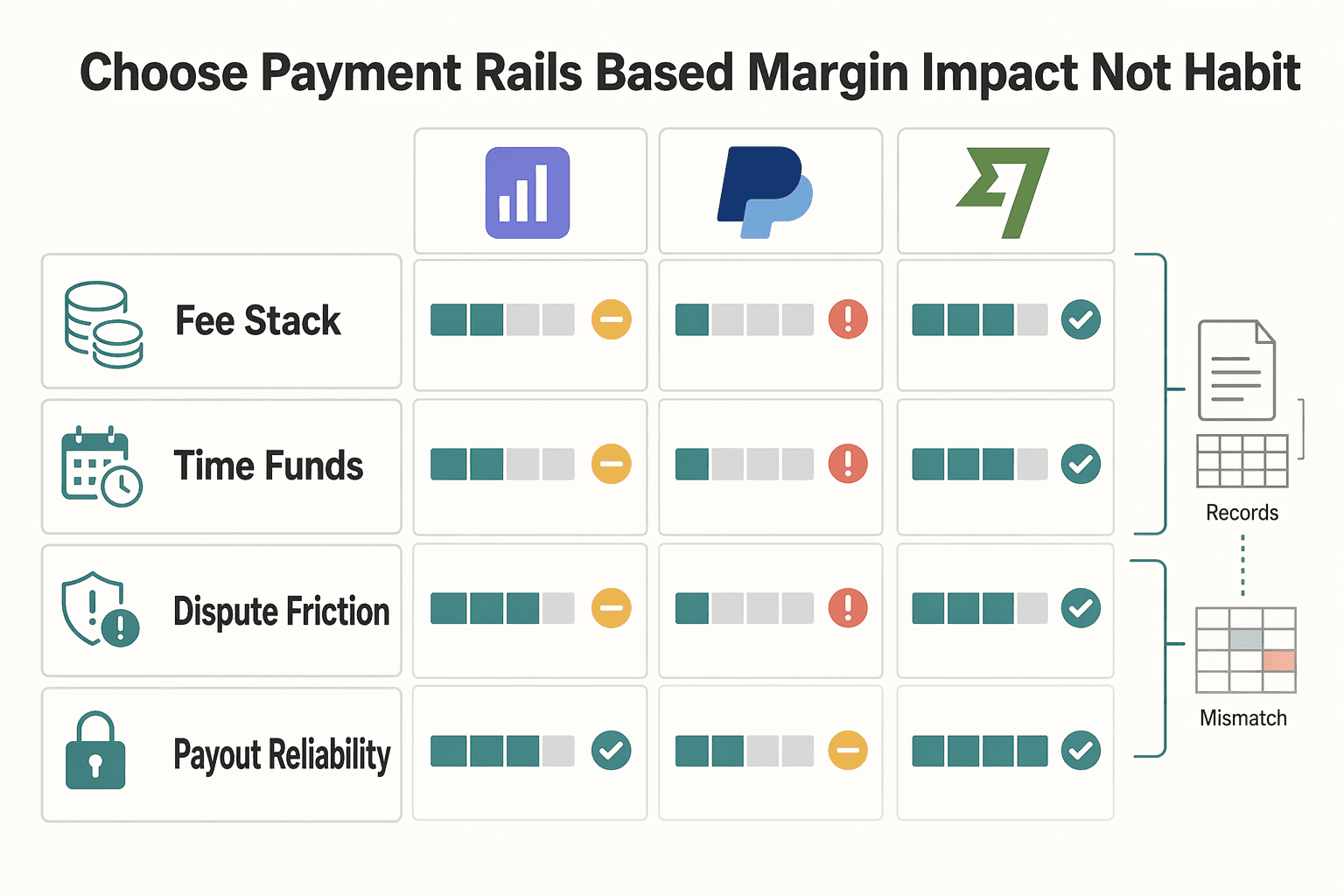

Choose Payment Rails Based on Margin Impact Not Habit#

Habit is a weak reason to pick a payment rail. The better choice is the one that leaves the best net result after fees, timing risk, dispute friction, and payout reliability are counted together.

Use the same scorecard for Stripe, PayPal, and Wise so the comparison stays honest.

| Check | What to compare | What to record |

|---|---|---|

| Fee stack | Processing, receiving, and conversion cost | Net amount received |

| Time to funds | Paid timestamp to usable funds in your process | Delay by rail in your records |

| Dispute friction | Effort and outcome from your own history | Recovered vs lost amount |

| Payout reliability | Holds, reversals, and exceptions in your own records | Exception count and close time |

Then run the comparison with identical scenarios:

- Build one scorecard with identical invoice scenarios across all three rails.

- Stress-test at least one high-ticket case, since fee and delay impact can compound on larger invoices.

- For Wise, test by method because pricing differs by path. Some methods are free, while faster methods can carry fixed fees, including

6.11 USDfor receiving USD wire and Swift payments,2.16 GBPfor GBP Swift, and2.39 EURfor EUR Swift. - If expected send volume may exceed

25,000 USDequivalent in a month, test whether discount eligibility changes the result. - If relevant to your setup, include one-time account costs in first-project math, such as the

31 USDWise Business line item.

Keep the assumptions matched. Invoice size, currency path, and timing need to stay the same across every test. Mixed inputs create false winners and hide long-run cost exposure. This is one of the easiest ways to fool yourself, especially when one rail looks cheaper in a marketing example but behaves differently in your actual client mix.

The high-ticket test is worth doing because small invoices can hide real tradeoffs. Visible fees matter, but predictability matters too. A rail with a slightly higher stated charge can still win if the funds become usable more reliably and exceptions take less time to close in your own records. That is why the scorecard includes both fee stack and time to funds. Margin damage is not only about the percentage charge. It is also about how smoothly the money gets from paid status to usable cash.

Wise especially needs method-specific testing for that reason. A path that looks inexpensive in one case may pick up fixed receiving charges in another. Use the likely client payment method in the model instead of relying on a generic average. And if your volume may cross the 25,000 USD equivalent threshold, check the result both below and above that point so you can see whether the decision still holds when usage changes.

Do not let familiarity make the choice for you. Many freelancers keep using the rail they started with because it is already connected, not because it performs best. That is fine when the difference is small and the process is stable. It is expensive when the rail adds repeat fee drag, delayed availability, or unnecessary exception handling.

Use one operating rule before every new client: if expected rail cost plus timing risk exceeds your margin buffer, reprice or switch rails before onboarding the project. That is easier than absorbing the drag and hoping tighter collections will make up for it later.

For a deeper side-by-side decision checklist, use Stripe vs. PayPal vs. Wise: The 2026 Battle for Best Freelancer Payments.

Before you lock a default rail, run your own fee-and-delay scorecard in this payment fee comparison tool.

Even the best rail decision still needs a clean payout path. If the money gets stuck between paid status and usable cash, the margin problem is only delayed, not solved.

Tighten the Payout Workflow and FX Steps#

Getting paid is not the same as having usable cash. Margin protection is incomplete until each paid invoice can be traced through payout and, where relevant, conversion.

Map the payout path end to end for each invoice. Keep one record that ties invoice details to paid status. If any step is missing, it becomes hard to explain where delays or costs entered the process, and small failures start to look like normal variance.

Use a controlled process:

- Map each stage with clear records. Track the unique invoice number, payment terms, for example due within 30 days, and paid status for every invoice.

- Standardize payment instructions. Include bank account details for direct transfers so clients have a clear payment path.

- Reconcile by invoice ID, not just account totals. Review missing or late payments at the invoice level so issues do not get buried.

- Treat payment failures as delivery risk. Unresolved payments can disrupt kickoff and delivery, so they need fast escalation.

The invoice-level trail is not just for reconciliation. It also shows where delays cluster. If payments regularly miss stated terms, you can adjust terms and cash planning before the problem turns into delivery stress. If funds keep getting held after the paid event, that points to the rail or payout setup rather than the client.

Treat process handoffs as control points. Compare expected timing against actual timing and note where the gap appears. That is usually where friction and extra cost enter the picture, especially in older or multi-step processes. Once you know the stage where delays collect, the fix becomes much more specific.

Exception tracking also needs ownership and closure notes. Unresolved items tend to roll from one cycle into the next until no one can say what is still open. Every exception should have a status, next action, and completion check. Otherwise month-end review becomes a mix of real issues and stale leftovers.

The operating checkpoint is simple: every invoice should have a clear trail from invoice details to paid status and usable cash. If the trail breaks, resolve it before you finalize your cash-flow view. That discipline gives you reliable inputs for a weekly operating rhythm instead of a month-end scramble.

Install Weekly Decision Rules and a Monthly Risk-First Review#

A review cadence only helps if it leads to action. Weekly checks should catch immediate leakage, and the monthly review should deal with structural changes before they become expensive habits.

Keep the weekly pass short and decision-oriented. You are not rewriting strategy every seven days. You are deciding which accounts need intervention now and which can stay on the current path.

Use a fixed operating checklist:

- Run a weekly cash checklist. Review overdue invoices, disputes, pending payouts, and balances across dedicated accounts: income, profit, owner pay, operating expenses, and taxes.

- Use fixed internal trigger rules. Define your own unpaid-exposure limit and the action you will take if a client crosses it.

- Protect profit allocation. Set aside profit before paying expenses, and avoid leaving profit as "whatever is left" at month-end.

- Pressure-test legal and compliance references. Treat checklist or advisor outputs as starting points, not complete legal coverage, and verify legal decisions against official editions.

The point of the weekly pass is speed and consistency. You want a clear answer to a small set of questions: what is overdue, what is disputed, what is pending payout, and which client now needs an intervention under your trigger rules. If that review starts turning into general business reflection, it gets slow and the most urgent items slip.

The monthly review has a different job. It should look for repeated leakage patterns, check whether pricing or terms need updating, and decide which client labels now require a different action. If you use labels, tie each one to a clear next step and deadline so the review produces decisions instead of notes.

Keep the two scopes separate. Weekly work handles current risk. Monthly work handles policy and pattern changes. When you combine them, urgent follow-up usually crowds out the structural fixes that would stop the same problem from returning.

This is also where discipline around records pays off. Tie pricing and term updates to repeated patterns in the data, not to memory or one difficult client. That keeps the business from swinging between overreaction and avoidance. If the pattern is real, it should show up in more than one row and more than one cycle.

With the cadence in place, most remaining damage comes from a short list of habits that keep reopening old leaks. Those are easier to fix once you can name them clearly.

Common Mistakes That Keep Eroding Margin and How to Recover#

Most erosion comes from familiar behaviors, not one dramatic failure. The fix is usually clear once you name the pattern and stop treating it as normal.

- Mistake: Tracking only topline sales.

Revenue can look healthy while costs rise faster underneath it. Recovery: review project and client profitability with a consistent cost structure, and check where rework or overtime is eating into margin. If activity is high but profit is thin, scope or delivery cost is probably out of line with pricing.

- Mistake: Letting invoicing drift.

Delayed, inconsistent, or easy-to-overlook invoicing drags down retained value even when the work itself was priced well. Recovery: set a clear invoicing and follow-up sequence, then apply it the same way each cycle instead of rebuilding the process case by case.

- Mistake: Committing senior pitch time before qualification.

When budget and fit are not qualified early, business development turns into unpaid consulting. That often means expensive senior effort gets spent on low-value opportunities. Recovery: use a qualification gate before assigning senior resources, and reference historical project profitability when deciding what work to pursue.

A frequent secondary mistake is treating the fix as a one-time cleanup. If the checks are not built into the weekly and monthly rhythm, the same leak reopens a few cycles later. This is why cadence matters so much. The repair is rarely hard. Keeping it repaired is the harder part.

Another common failure mode is changing too many processes at once. If pricing and invoicing change in the same window, it becomes much harder to tell what actually improved the result. Stage major changes so impact stays visible and the next decision has a real basis.

In practice, recovery gets easier when you can connect each mistake to a control point. Topline-only tracking is fixed in the baseline and formula. Invoicing drift is fixed in the billing sequence. Unqualified pitch work is fixed in your intake and qualification gate. That kind of mapping makes the response practical instead of motivational.

When these fixes start working together, the business gets quieter in a good way. Pricing decisions get clearer, payment friction drops, and month-end results stop producing avoidable surprises. The questions below cover the judgment calls that usually come up once the process is running.

Conclusion#

Protecting margin is less about chasing a generic benchmark and more about tightening the points where value leaks out. The sequence matters: build a trustworthy baseline, lock one formula, find the real sources of erosion, protect terms before work starts, invoice promptly, choose rails by net impact, reconcile payouts, and review the whole picture on a fixed cadence.

Use the checklist below as an execution order, not a menu. Running it in sequence keeps the decisions connected from contract setup to payout reconciliation. Specific benchmarks and contract-enforcement thresholds are not established here, so treat those as internal policy choices.

- Define one margin formula and include owner labor cost. Use the same formula across clients so trend decisions stay comparable. Document cost scope once and keep it stable through each review cycle.

- Audit leakage before changing prices. Review fee drag, delayed payment, disputes, write-offs, and revision spillover by client. Rank issues by impact and repeat count so you fix the biggest drag first.

- Standardize default contract terms. If you use deposit, payment-term, revision-limit, or pause-work clauses, keep defaults consistent unless you log an exception. Store signed terms and addenda with invoice records so enforcement is straightforward.

- Issue invoices immediately and automate follow-up. Use reminders and escalation triggers tied to your agreement. Keep line items aligned with approved scope to help reduce avoidable disputes.

- Score payment rails by true margin impact. Compare options with your own invoice sizes and outcomes. For Wise, check method-specific pricing with its calculator: some methods are free, faster methods can include fixed fees, and USD wire or Swift receiving is listed at

6.11 USD. - Reconcile payouts and FX outcomes monthly. Match invoice IDs to received amounts, log fee and conversion impact, and keep a monthly audit artifact, for example, Wise's standardized fee-format view. Resolve exceptions before finalizing monthly conclusions.

- Run a weekly risk-first checklist and act on triggers. Track overdue invoices, disputes, pending payouts, and client-level margin trend. Apply trigger rules consistently so action does not depend on mood or memory.

- Reprice, renegotiate, or exit low-margin high-friction clients. Use trend data to decide, then update your floor with this billable rate guide.

If you implement only one change this week, start with baseline quality and invoice timing. Those two moves usually expose the next best decision quickly and make every later improvement easier to measure.

When you finalize your risk-first checklist, convert it into enforceable terms with the freelance contract generator.

Frequently Asked Questions

What is a good freelance profit margin for service businesses?

There is no universal percentage that fits every service business. A better standard is whether your margin trend stays healthy over time after all expenses are included. Benchmarks only help when they use the same formula and cost assumptions you do.

How do I calculate profit margin correctly when I do all the work myself?

Assign a real cost to your own time and include it as an expense. Then calculate profit margin as (Revenue - total expenses) / Revenue x 100, and keep net profit separate as the dollar amount left after expenses. If you also track gross margin, use net sales minus cost of sales divided by net sales.

Why is my margin shrinking even when my revenue is flat or growing?

Margin can shrink when costs are missing from the model, especially owner labor and overhead. It can also fall after delivery because disputes, withheld payment, fee drag, and delays reduce what you actually keep. Scope drift in revisions, urgent requests, or undocumented extras can create the same problem.

Should I optimize rates first or payment terms first?

Start with the bigger leak. If pricing is below your cost floor, fix rates and scope first. If pricing is workable but payment is delayed or inconsistent, tighten payment terms and follow-through first. You can stage both changes, but keep the order explicit.

Are margin benchmarks from calculators and forum posts reliable?

They are useful for comparison, not for final decisions. Different sources often use different formulas, so the percentages are not always directly comparable. Use them to pressure-test your assumptions, then decide from your own trend data.

How do chargebacks, late payments, and write-offs change my true margin?

They can compress true margin because delivery costs are often already spent when payment is delayed, reduced, or lost. Track late payments, chargebacks, write-offs, and dispute losses in the same ledger as regular cost lines. That makes repeat drag by client, terms, or payment rail visible so you can reprice, tighten terms, or exit.

Watch

The Silent Profit Killer in Freelance Businesses

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Calculate a Freelance Rate You Can Actually Get Paid On

A workable rate is not the neat number a calculator produces. It is the number that still works after you account for real billable capacity, non-client time, scope drift, and the gap between sending an invoice and receiving cleared cash. Start with hourly math even if you do not plan to bill hourly, then turn that number into a quote with clear `payment terms`.

Stripe vs PayPal vs Wise for Freelancers in 2026

Cashflow reliability matters more than brand familiarity. If money arrives later than expected, gets reduced by fees, or loses value during conversion, margin disappears even when the client technically paid on time.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.