Quick Answer

Choose eligibility before optimization: in feie vs foreign tax credit, confirm tax home and qualifying status, then compare both paths using the same inputs. FEIE is computed on Form 2555 and can leave residual U.S. tax when income sits above the exclusion cap, while FTC is handled on Form 1116 by income category. The safer filing posture is the one you can document end to end with travel logs, allocation notes, and reconciled Form 1040 workpapers.

FEIE vs FTC for high-earning expats who want one correct decision#

Start with compliance, then optimize tax. If you are a globally mobile freelancer or consultant filing Form 1040, first confirm what you can actually claim and support, then compare the tax result.

For high earners, that order matters more than it first appears. A rough comparison can look decisive until you draft Form 2555, confirm the qualifying test, and separate income into the buckets that matter for Form 1116. The better choice is usually the one you can support from source records without changing the story later.

You are still under U.S. income tax rules while living abroad. FEIE applies only when you have foreign earned income, a foreign tax home, and qualifying status under an IRS test. FTC is claimed on Form 1116, and it must be handled by income category.

| Decision point | FEIE | FTC |

|---|---|---|

| Primary filing anchor | Form 2555 attached to Form 1040 | Form 1116 attached to Form 1040 |

| Core mechanism | Excludes qualifying foreign earned income | Uses Form 1116 calculations with separate income-category treatment |

| First eligibility gate | Foreign tax home plus qualifying status tests | Foreign taxes with category-by-category treatment on Form 1116 |

| Common high-earner friction | Income above the annual exclusion cap remains exposed | Category-by-category treatment can add filing complexity |

| Frequent filing error | Treating excluded income as not reportable | Combining income categories on one Form 1116 |

One practical checkpoint prevents a lot of bad calls: verify FEIE qualification before you run side-by-side math. If you are relying on physical presence, document the 330 full days in a 12-month period before you depend on exclusion numbers. That tells you whether FEIE is available at all, whether the exclusion may be reduced for part-year qualification, and whether the return will still need FTC work for income outside the exclusion.

For 2026 planning, the listed FEIE amount is $132,900 per qualifying person. The exclusion is not unlimited, and excluded income is still reported on the return. If income is materially above that level, FEIE alone can still leave residual U.S. federal income tax exposure. At that point, the question is no longer just exclusion or credit. It becomes a return-construction problem: what can be excluded, what remains exposed, and whether Form 1116 still needs category-by-category work.

Choose the filing posture you can defend with records and repeat next year. Keep travel logs, tax home support, draft Form 2555 logic, and any Form 1116 category notes before filing. A short dated memo stating which test you used, how you mapped earned versus passive income, and why you chose the final path can make next year's filing much easier to update. If you want a quick next step, try the FEIE calculator. For related state exposure, see Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

FEIE and FTC at a glance before you choose#

Use this table as triage, then confirm eligibility before you model tax outcomes.

| Decision criteria | FEIE | FTC |

|---|---|---|

| Core mechanism | Excludes eligible foreign earned income from U.S. taxable income | Credits eligible foreign taxes against U.S. liability |

| Primary filing anchor | Form 2555 on Form 1040 | Form 1116 on Form 1040 |

| Income fit | Best for earned income that meets FEIE rules | Can apply by income category, including passive category income, when foreign tax exists |

| Key constraint | You must meet FEIE qualification requirements before claiming it | Form 1116 must be handled by income category, with country-level separation where required |

| Typical high-earner tension | Income above FEIE limits can leave residual U.S. tax exposure | Benefit depends on foreign tax profile and how usable the credit is |

The table is a starting point, not the decision by itself. Before you compare outcomes, know whether the return is mostly foreign earned income, whether passive income is present, and whether foreign taxes were paid in more than one country. Those facts determine how much work Form 2555 and Form 1116 will actually require.

Eligibility comes first, not optimization. FEIE requires foreign earned income, a foreign tax home, and qualifying status under a listed test. If you are using the Physical Presence Test, keep records that support 330 full days in 12 consecutive months. If that foundation is unclear, any later tax comparison is just a rough draft.

The tradeoff many filers miss is coordination. FEIE can simplify one part of the return, while FTC still depends on clean category and country-level tracking. Form 1116 is prepared by income category, and taxes tied to more than one country or territory must be separated accordingly. In practice, that means building one clean income map before you run numbers: what may go to Form 2555, what must stay outside it, and how foreign tax records will support Form 1116 later.

A good operator habit is to draft both paths from documents, not estimates. Build a working Form 2555, prepare preliminary Form 1116 splits, and keep the country-level tax support with the file. Excluded income is still reported on the U.S. return, so the cleanest choice is the one that keeps reporting, qualification, and category treatment consistent. If your income mix or allocation logic is still fuzzy at this stage, slow down. It is far easier to fix assumptions while they are visible than after the return is assembled.

Eligibility gates you must clear before comparing tax savings#

Do not compare savings until you clear eligibility. The right order is tax home, qualifying test, then filing setup. If any one of those pieces is weak, a side-by-side tax comparison can push you toward a position you cannot defend.

First comes tax home. For FEIE, your tax home must be in a foreign country. U.S. citizens and resident aliens abroad are still taxed on worldwide income, so you still file a U.S. return and report the income, then use Form 2555 to figure the exclusion. It is a common mistake to jump straight to day counts because the travel log feels concrete. In practice, the tax home story and the qualifying test work together, and the form logic depends on both.

Next comes qualifying status. You must meet either the Bona Fide Residence Test or the Physical Presence Test. Under physical presence, you need at least 330 full days in a foreign country or countries during any 12 consecutive months. If your qualifying period covers only part of the year, the maximum exclusion is adjusted by qualifying days. That is where rough planning often goes wrong, because a full-year estimate can make the exclusion look larger than it will actually be on the filed return. For test mechanics, see Qualifying for the FEIE: Physical Presence and Bona Fide Residence Tests.

Do the day-count work before you compare savings. Pick the 12-month period, lay out the travel dates, and make sure the log is consistent with passport or other travel records. If the qualifying period is only part of the year, adjust the FEIE limit first rather than comparing a full-year exclusion estimate to an FTC result. That sequencing step can save a lot of backtracking later.

Only after those gates are clear should you set up the filing side. Draft Form 2555 early enough to expose any bad assumptions, then separate the foreign tax records you expect to use for Form 1116. This is less about form mechanics than about forcing the return into one clean story before you start optimization.

Use this quick verification pass before running tax comparisons:

- Confirm and document facts that support a foreign-country tax home.

- Confirm which test you are using and keep support for either full-year residence or day count.

- Reconcile your day-count log to passport or travel records before final numbers.

- Draft

Form 2555early so assumptions are visible before final filing. - Separate FEIE support documents from the foreign tax records you expect to use later for

Form 1116. - Check current IRS instructions for election timing and any late-election path.

The practical takeaway is simple: if records are thin, fix the documentation before you model savings. Treat FEIE as a recurring eligibility check as your travel pattern and income facts change year to year. An early Form 2555 draft often shows whether the real issue is qualification, dates, or income classification. For broader context, review The Ultimate Digital Nomad Tax Survival Guide for 2025.

Where FEIE helps high earners and where it can hurt#

FEIE works best when most of your income is foreign earned income and your goal is to reduce U.S. taxable income through exclusion. When the return has that shape and the qualification file is clean, FEIE gives you a direct line from facts to filing.

Where it gets weaker is just as important. The exclusion loses some of its value as income rises above the annual cap or the return includes more than earned income. FEIE cannot exceed your foreign earned income for the year, and mixed earned plus passive income usually means you still need category-based FTC work on Form 1116 rather than relying on exclusion alone. For high earners, the issue is not that FEIE stops helping once income rises. The issue is that it often stops being the whole answer.

The cap is the main decision lever here. IRS materials show conflicting 2025 figures, so verify filing-year instructions before you rely on a single 2025 number. For 2026, the listed maximum is $132,900 per qualifying person, so if expected earned income is materially above that, compare an FEIE-first approach with an FTC-led approach before filing. A quick estimate can make the exclusion look complete when it is only partial.

Housing can also change the result. If you claim a foreign housing exclusion, it reduces the foreign earned income available for FEIE, which can lower the value of the exclusion compared with a headline estimate. That is why experienced preparers do not rely on the top-line FEIE amount until the Form 2555 draft is complete.

A good modeling pass usually looks like this:

- Draft

Form 2555using expected earned income and any housing exclusion. - Separate earned and passive income early, then prepare

Form 1116by the relevant income category. - Pressure-test a case where earned income lands above FEIE coverage.

- Keep a short assumptions file so next year is an update, not a rebuild.

The point of that exercise is not to overcomplicate the return. It is to see the edges clearly. Identify total foreign earned income, reflect any housing exclusion, compare likely FEIE coverage to the annual cap, and note what remains outside the exclusion. Then check whether passive income or other categories still require Form 1116 work. That side-by-side view is what high earners need before they finalize the return.

If expected annual earned income materially exceeds likely FEIE coverage, treat FEIE as one component of the return and run a full FTC comparison before you decide. If the housing numbers or qualification period change late in preparation, rerun the Form 2555 draft instead of assuming the earlier answer still holds.

Where FTC helps and where it falls short#

FTC often fits better when foreign taxes are recurring and the return spans more than one income category, including passive category income. It can become the more natural filing path when the return already demands category discipline.

Its strength is structure. Form 1116 requires a separate form for each income category, only one category box per form, and separate country lines when taxes were paid to more than one country or U.S. territory. That adds setup work, but it also gives you a cleaner way to handle mixed-income and multi-country returns. When the records are well sorted, the form follows the file instead of forcing you to improvise late in the process.

That means the work starts with the records, not the software. Sort your foreign tax payment records before you begin form prep. Group them by income category, then separate country lines where required, so the draft Form 1116 mirrors the source documents. This is one of those boring setup steps that pays off later, because it keeps the final return reviewable.

Where FTC falls short is coordination. If FEIE and FTC are handled without a category-by-category review, it becomes easy to map income inconsistently across the return. Keep the baseline clear: U.S. taxpayers abroad are taxed on worldwide income, and excluded foreign earned income is still reported on the U.S. return. If one worksheet treats an item one way and the final Form 1116 treats it another way, the return gets harder to review and harder to defend.

For that reason, an FTC-led draft often works well when foreign tax burden is high and recurring. Build the credit side first, then test whether FEIE improves the outcome. That order can make the comparison cleaner because you see the full credit structure before any FEIE allocation changes the income pool.

Can you combine FEIE and FTC without creating filing risk#

Yes, but only if the return tells one consistent story. The same foreign earned income cannot be treated as both excluded and creditable.

The safest way to handle both is as one filing sequence, not as two separate calculations you try to reconcile at the end. Settle the FEIE piece first, freeze the income map, and then determine what remains for Form 1116 by income category. If the income buckets keep moving as you work across the forms, filing risk rises fast.

Use a clean preparation order:

| Coordination point | Clean approach | Filing-risk pattern |

|---|---|---|

| Form flow | Finish Form 2555, reflect it on Form 1040, then draft Form 1116 | Build Form 1116 first and backfill FEIE later |

| Income mapping | Keep excluded earned income separate from income used for credit calculations | Reuse one income pool for both outcomes |

| Documentation | Keep dated allocation logic by income stream/category | No written logic, only spreadsheet edits |

That sequence matters because coordination mistakes usually start upstream. If Form 1116 is built before FEIE allocation is settled, later changes to day count, housing figures, or income classification can ripple through the return. When that happens, rerun the full sequence instead of patching only one form. Partial fixes are where inconsistent treatment sneaks in.

Use two pre-filing checks before you sign off:

- Confirm the

Form 2555exclusion does not exceed foreign earned income for the year. - Confirm each

Form 1116has one category selection and ties to a clearly documented income bucket.

Those checks work best as a written reconciliation, not just a mental review. Compare the income used on Form 2555 against the income buckets feeding each Form 1116, and make sure the file explains why an item was excluded, credited, or left outside both.

Red flags that often lead to amendments include overlapping treatment where excluded income is also treated as creditable, undocumented allocation logic across earned, housing, and other buckets, and unsupported assumptions that all foreign taxes paid remain usable after FEIE is applied. If coordination depends on technical elections or relief requests under Treasury Regulation § 301.9100-3, involve a qualified tax professional early. If you cannot explain the allocation without reopening multiple spreadsheets, the file is not ready.

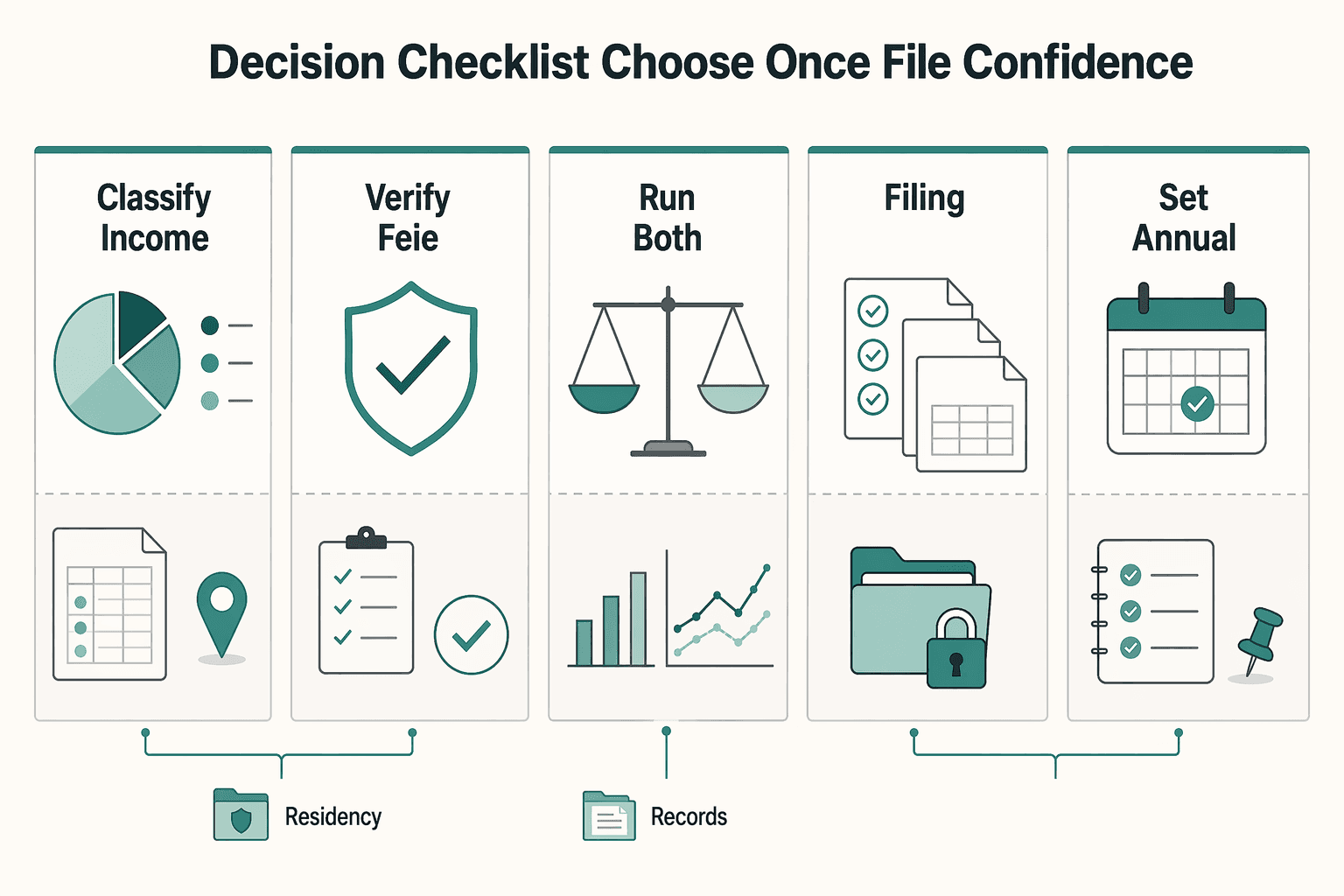

Decision checklist to choose once and file with confidence#

Choose your position in a fixed order, document each call, and file one consistent story across Form 1040, Form 2555, and Form 1116.

| Step | What to do | What to keep |

|---|---|---|

| 1. Classify income | Split foreign earned income from passive income, then mark what is potentially excludable vs creditable. | Income map tied to payer records and account statements. |

| 2. Verify FEIE eligibility first | Confirm your tax home is in a foreign country and that you meet a qualifying test (Bona Fide Residence Test or Physical Presence Test) before running optimization. | Residency evidence and a travel-day log. |

| 3. Run both paths with one assumption set | Compare FEIE-first and FTC-first outcomes for U.S. federal income tax using the same dates and inputs. | Side-by-side worksheet with assumptions clearly dated. |

| 4. Confirm election timing and filing language | Check filing language and timing requirements, including cases that reference Section 1.911-7(a)(2)(i)(D). | A short filing memo stating the chosen path and why. |

| 5. Set annual re-check triggers | Re-run this checklist after residency moves, income-mix changes, or jurisdiction changes. | Year-end review checklist and change log. |

Read that checklist as a sequence, not a menu. Step 1 controls the rest of the return. If income is not classified cleanly at the start, the exclusion math and the Form 1116 category handling can drift in different directions. Step 2 comes before optimization because no comparison matters if FEIE qualification is weak or only partly supported. Step 3 only has decision value when the inputs are truly the same across both paths: same dates, same income totals, same assumptions file.

Step 4 is where technical issues tend to surface. If filing language, election timing, or a relief question appears, pause before you finalize the numbers. This is also where a short memo earns its keep. It does not need to read like a legal brief. It just needs to state what you chose, what facts support it, and what would force you to revisit the position.

Step 5 keeps next year from turning into a rebuild. A short change log for moves, income-mix changes, or jurisdiction changes makes the next review much faster because you are updating a known file rather than rediscovering the facts.

Two controls prevent a lot of late-stage errors. First, if FEIE qualification applies only for part of the year, adjust the exclusion by qualifying days before you compare outcomes. Second, for FTC, keep Form 1116 handling strict by using a separate form per category and checking only one category box on each form. Put those controls into your final review, not after filing. If Step 4 raises technical election or relief issues, escalate before the return goes out.

Keep an audit-ready tax file so your choice survives scrutiny#

Once you choose a filing path, documentation quality becomes the main risk. Your file should let a reviewer trace each major number from source records to Form 1040 in one pass.

The goal is practical, not academic. A good file should answer three questions without guesswork: why you qualified, how you calculated the return, and where each major figure came from. Organize the file in that order so it mirrors the way the return was built. When the file and the return follow the same logic, review gets easier and mistakes are easier to catch.

Keep one minimum evidence pack: records that support your foreign tax home position, travel logs, foreign tax payment records, filed Form 2555 with workpapers, final Form 1040 workpapers, and FBAR filing artifacts, including the FinCEN electronic filing confirmation. FEIE still requires filing a return that reports the income, so the records have to support both qualification and reporting. If you rely on physical presence, keep a day-count log that supports the 330 full days in a 12-month period.

Arrange your file so qualification records come first, then income and foreign tax records, then workpapers, then final filed forms and confirmations. That sequence sounds simple, but it matters. If the records are scattered, you will spend review time hunting for support instead of checking whether the treatment is actually consistent.

| File component | What it supports | Quick check |

|---|---|---|

| Tax home and residency records | Foreign tax home position | Dates and location history align to the return year |

| Travel log | Physical presence test | Day count ties to passport/travel records |

| Foreign tax payment records | Cross-border tax treatment inputs | Payment date and taxing authority are clear |

Form 2555 + workpapers | FEIE and housing computations | Inputs tie back to income records |

Form 1040 workpapers | Final return assembly | Totals reconcile to the filed return |

| FBAR records | Account-reporting compliance trail | Submission copy and FinCEN e-filing confirmation are saved |

Use the quick-check column before submission, not after. If dates do not align, if a tax payment record does not clearly identify the foreign authority, or if a Form 2555 input cannot be tied back to income records, stop and fix the file before you file the return.

Run this evidence audit before final review:

- Can a reviewer trace foreign earned income from payer records to

Form 2555? - Can the travel log be tied to passport or other travel records?

- Are foreign tax payment records clearly matched to the country lines and category treatment you used?

- Is there a short memo explaining the assumptions behind the filed forms?

Certain red flags usually mean rework is still needed. A return figure that cannot be tied to a source record is one. Another is withholding that is documented, but it is unclear whether it went to a foreign tax authority or the U.S. Treasury. A third is saving filed forms without the short memo that explains what you did and why.

That memo does not need to be long. Its job is to explain the filing story in plain English: what test you used, what income was treated as earned or passive, and why the final choice was FEIE-first, FTC-led, or coordinated. Run one last evidence audit before filing. If a second reviewer cannot follow the path from records to forms cleanly, fix that gap first.

Make the choice once and execute it correctly#

The right choice is the one you can prove end to end: eligible, documented, and cleanly filed. In practice, one correct decision means one coherent story from qualification through final forms.

Start with eligibility before any math. FEIE requires foreign earned income, a foreign tax home, and a return that reports that income. If you are using the Physical Presence path, confirm the 330-day test before you finalize Form 2555.

Then compare FEIE and FTC using one shared input set. Keep income, dates, and assumptions identical across both paths. After that, run a coordination check so Form 2555 and each Form 1116 category stay consistent. The comparison only has value when the inputs are stable and the preparation order is clear.

Use this filing sequence:

- Confirm eligibility facts and supporting records.

- Run the FEIE and FTC comparison with matched assumptions.

- Reconcile forms and income categories in one review pass.

- File only when the documentation is complete and traceable.

If records are incomplete, pause and fix them before deciding. If technical interpretation questions remain, escalate before filing. Do not wait until submission to discover that the day count, tax home file, or Form 1116 categories do not line up.

Complete the checklist now, attach your evidence pack to the draft return, and resolve edge cases before submission.

Frequently Asked Questions

Can I use FEIE and FTC in the same tax year?

This section does not establish FEIE-FTC coordination mechanics. What is supported: FEIE requires qualifying status with foreign earned income, a foreign tax home, and a filed U.S. return reporting that income. FTC is handled on Form 1116 by income category. If you cannot map income and taxes cleanly across forms, escalate.

When is FEIE usually less useful for high-earning freelancers and consultants?

FEIE is capped by an annual inflation-adjusted limit, so its value can narrow when income sits well above the exclusion. The 2025 figures shown conflict. Verify current-year numbers before modeling.

What form do I file to claim FEIE?

If you qualify, use Form 2555 to figure FEIE and any housing exclusion or deduction, and file a U.S. tax return reporting the income.

Does choosing FEIE lock me into that approach for future years?

Confirm current IRS election and change rules before filing.

What is the safest first-pass choice if I am unsure between FEIE and FTC?

Start with eligibility. Confirm foreign earned income, foreign tax home, and qualification tests such as physical presence (330 full days in 12 consecutive months), then compare outcomes using the same income inputs.

Do FBAR and FATCA filings change the FEIE vs FTC decision?

Confirm FBAR and FATCA obligations separately from your FEIE vs FTC decision.

When should I stop self-filing and hire a cross-border tax professional?

Escalate when facts are hard to document or income-category mapping is unclear on Form 1116. Escalate when qualification questions cannot be resolved before filing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Qualifying for the FEIE with Physical Presence or Bona Fide Residence

Start with one principle: choose the FEIE path you can prove, then keep every filing detail consistent with that choice. If you are weighing the Physical Presence Test for FEIE, treat it as a documentation job first and an optimization question second.

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.