Quick Answer

Yes, business insurance for freelancers is usually necessary once contracts, client proof requests, or delivery risk are in play. A practical baseline is professional liability plus general liability, with cyber or workers’ compensation added when your work model changes. Treat the Certificate of Insurance (COI) as an operational requirement for kickoff readiness, not an afterthought. Make quote decisions only after coverage limits, deductible terms, and exclusions are normalized.

Start Here If You Want Coverage Without Overbuying#

Make one decision first: buy coverage that matches your real exposure and the proof your contracts require, not the cheapest result on a quote page. The goal is practical and immediate: decide what to bind now, what can wait, and what documentation must be ready before kickoff.

In many client engagements, especially IT-services work, you may be asked for a Certificate of Insurance (COI) before work starts. Treat that as contract readiness, not a universal legal rule. A low premium that fails a client proof check can cost more in disruption than it saves in price.

Before you request quotes, build a one-page prep note. Include three fields: services you deliver right now, contract promises you are already signing, and proof items clients have requested in recent onboarding. That single page keeps quote shopping tied to your real risk, and it helps you reject policies that look affordable but do not match your actual commitments.

Use this filter when comparing options:

- Buy now when your current services or signed agreements create active exposure and clear proof expectations.

- Defer when a risk depends on changes that are not active yet.

- Reject options that cannot support COI or contract-proof requests when they arise.

You may also see bundled products such as a Business Owner's Policy (BOP). A bundle can be efficient, but it is not one-size-fits-all and should match your service mix and contract demands.

Keep continuity in view. Coverage lapses can interrupt contracts and may increase future pricing at renewal. If you use quote marketplaces, rankings may reflect commercial partnerships, so make your final call on coverage fit.

Key Terms You Need Before Comparing Policies#

Before you compare price, lock down the definitions so you are evaluating like-for-like coverage. Business insurance is a set of policies, not one product, and each policy handles a different risk.

| Term | What it means | What to check |

|---|---|---|

| Business insurance | Multiple policy types chosen based on exposure | Confirm which policy types are included in each quote |

| Professional liability insurance (E&O) | Also called Errors and Omissions insurance; used for negligence or service-error claims, including related legal and settlement costs | Verify this coverage is explicitly listed in the quote |

| General liability insurance | Covers third-party injury or property-damage incidents and related claim costs | Confirm what incidents and costs are included |

| Coverage limit | Maximum payout available for a claim | Compare quotes at similar limit structures, including per-loss and aggregate |

| Policy deductible | A core quote cost variable reviewed alongside premiums and fees | Compare deductible impact alongside premium and fees |

| Policy exclusion | What the policy does not cover | Review exclusions directly to catch likely gaps |

| Certificate of Insurance (COI) | Proof your business has insurance coverage | Confirm how and when a certificate can be issued after purchase |

Three terms usually drive comparisons in practice: limits, deductibles, and exclusions. A cheaper premium can still be a worse deal if exclusions remove protection you actually need.

Use one clean comparison order: align limits first, then compare deductibles, exclusions, and fees. If limits are not aligned, the rest of the comparison is harder to interpret. Treat COI readiness as part of selection, not cleanup, because certificates are issued after purchase and timing can matter when proof is requested quickly.

When two quotes look similar, do one extra check before deciding. Confirm they define what is covered in similar ways and apply comparable exclusions. If those details are unclear, treat the quote as incomplete and keep comparing.

The Minimum Coverage Most Freelancers Should Start With#

Start with coverage that protects the services you sell today, then add policies when your risk profile changes. A common starting point for freelancers is a Business Owner's Policy (BOP), which can be expanded as exposure grows.

| Policy | Article note | Reported price example |

|---|---|---|

| Business Owner's Policy (BOP) | A common starting point that can be expanded as exposure grows | around $1,687 per year |

| Standalone general liability | Addresses third-party bodily injury and property damage claims | $810 |

| Workers' compensation | Review options and local treatment for owners and contractors before onboarding; confirm role classification | $1,032 |

Professional liability addresses allegations of negligence, errors, or omissions tied to your work, including legal fees and settlements. General liability addresses third-party bodily injury and property damage claims. If you prefer separate policies instead of a bundle, compare each policy's fit to your actual services.

Without coverage, you may need to fund claim costs yourself, so the cheapest option is not always the safest. One carrier reports customer averages around $1,687 per year for a BOP, $810 for standalone general liability, and $1,032 for workers' compensation. Treat these as carrier snapshots, not market-wide benchmarks, and use trigger-based timing to decide what to bind now versus later.

- Start with the coverage that matches your current services and delivery risks.

- Evaluate add-ons as exposure changes.

- Review workers' compensation options and local treatment for owners and contractors before onboarding.

If you are deciding between separate policies and a bundle, compare in two passes. First compare coverage fit for your real services. Then compare price using the same limits, deductible, and core exclusions. This order keeps a lower sticker price from hiding a weaker policy shape.

Workers' comp has one critical checkpoint: classification. Independent contractors are generally not covered by a hiring company's workers' comp policy, and misclassification can create legal problems. Confirm role classification before contracts are signed and keep that record with your insurance documents.

If you want a deeper dive, read When Should a Freelancer Upgrade from Sole Proprietor to an LLC?.

Match Real Risks to the Right Policy#

Map each risk to the policy built for that event, not just the policy you already carry. That habit can reduce avoidable coverage gaps.

| Real scenario | Policy to evaluate first | Why it fits | Practical checkpoint |

|---|---|---|---|

| A client says your advice or deliverable caused financial loss | Professional liability insurance (Errors and omissions, E&O) | This is a professional-services allegation tied to client loss | Keep signed scope, revisions, and approvals |

| Someone is injured or property is damaged during your on-site work | General liability insurance | General liability is built for accident-based third-party injury or damage claims | Keep incident notes, photos, and witness details |

| You work in client data environments and a breach or missed deadline turns into a legal threat | Cyber liability plus E&O review | Data and service failures can trigger claims from more than one angle | Keep an incident timeline, actions taken, and client communications |

A common failure mode is assuming standard E&O covers every communications or content-related claim. Some policies exclude media-related acts, so treat that as an open risk until the wording is clear in writing.

When your service model changes, update this risk map before you take on new commitments. Different roles create different liabilities, and yesterday's policy mix can become mismatched quickly.

A practical way to keep this current is a short risk map in your client file. Include four fields: event, first policy to check, evidence you would need, and owner for each document. Update those fields when your services change, and keep proof of coverage ready because many clients ask for it before signing.

What Clients and Contracts Actually Require#

Commercial requirements often matter as much as legal minimums. Many clients ask for proof of insurance before hiring, including for remote work, so treat coverage evidence as a deal requirement, not just a legal checkbox.

Legal minimums and contract terms are separate tests. Requirements can vary by jurisdiction, and in some places (including parts of the EU) specific insurance types are mandated.

Liability and indemnification language can create expectations your policy may not fully cover. Do not assume Professional liability or E&O automatically matches every promise in your agreement.

Use this pre-signature check before you accept terms:

- Confirm insurance requirements tied to the deal's jurisdiction and contract.

- Compare each Liability clause and Indemnification clause against your active policy wording.

- Share current proof of insurance during onboarding.

- If contract promises seem to exceed your coverage, renegotiate before kickoff.

A useful review order is simple: read liability language first, then indemnification promises, then insurance requirements and document requests. That sequence helps you spot mismatch early, while terms are still negotiable, instead of after signature when options are narrower.

Entity choice still matters, but it does not replace insurance. Uncovered claims can still leave you paying directly out of pocket. If you need a clause-by-clause method, review Limiting Your Risk: How to Use Liability and Indemnification Clauses.

How to Read a Policy So It Pays When You Need It#

Read your policy as a working document, not a formality. You want to confirm what the policy says, what your contracts require, and what records you will need if a dispute appears.

Start by capturing policy basics from the declarations and policy documents in one place. If a term is unclear, request written clarification and keep it in your policy file.

Next, compare limits and deductibles against the commitments you sign. There is no universal perfect setup, but there is a clear bad one: terms you could not absorb without disrupting your business.

Then review exclusions against how you actually deliver work. General liability and professional liability address different risks, so confirm your wording still fits your services and client expectations.

Treat documentation and notice requirements as part of coverage readiness. Keep signed scopes, approvals, change records, incident notes, and key client communications organized from day one.

Use this pre-signature and pre-renewal checklist each time:

- Record policy type, policy period, and key declared fields on a one-page summary.

- Record limits and deductibles with practical cash-impact notes.

- Flag exclusions that may conflict with contract promises or service scope.

- Confirm documentation and notice responsibilities.

- Keep your Certificate of Insurance (COI) available when requested.

- Save carrier or broker clarifications as written attachments.

One practical reading method is a three-pass review. Pass one captures declarations and basic terms. Pass two checks exclusions against your real services. Pass three checks conditions, notice expectations, and required records so you know what to keep if a claim develops.

If you take public-sector work, add a clause check before signature. FAR Part 52 organizes solicitation provisions and contract clauses, so compare contract clause language against your policy documents before you commit.

Cost Reality and Budget Tradeoffs#

Make budget decisions claim-first, not quote-first. Fund the coverage most likely to matter in a real loss, then optimize price.

Public quote pages are useful for orientation, not final selection. They are rarely apples to apples because quotes can differ on coverage type, term structure, deductible, limits, and exclusions. Some comparison content is also affiliate monetized, so treat rankings as a starting point.

Use published prices as rough signals only. Examples like about $17 per month, around $5 for a short gig, or annual ranges such as $810 to $1,687 reflect different products and assumptions. They are not one standard benchmark.

The key tradeoff is claim usability versus premium savings. A lower premium can be the worse value if claims handling is weaker or exclusions miss your main exposure. Deductible choices work the same way: a $0 deductible often costs more upfront, while a higher deductible can create cash pressure when a claim hits.

If cash is tight, prioritize by downside risk. Start with the coverages tied most directly to your current service mix, then add lower-priority coverage when revenue or risk changes justify it.

Use a one-page normalization check before choosing:

- Record coverage type and term dates for each quote.

- Match limit and deductible structure before comparing price.

- Log major exclusions tied to your service mix.

- Confirm proof-of-insurance turnaround, including COI access.

- Note insurer financial-strength signals, such as AM Best rating, when available.

Add one budget checkpoint before binding: can you fund the deductible without disrupting core obligations if a claim lands at a bad time? If not, the premium savings may be too expensive in practice.

Re-shop when your risk profile changes, not only at renewal. Changes in service mix, client requirements, or heavier data exposure can change what deserves budget first.

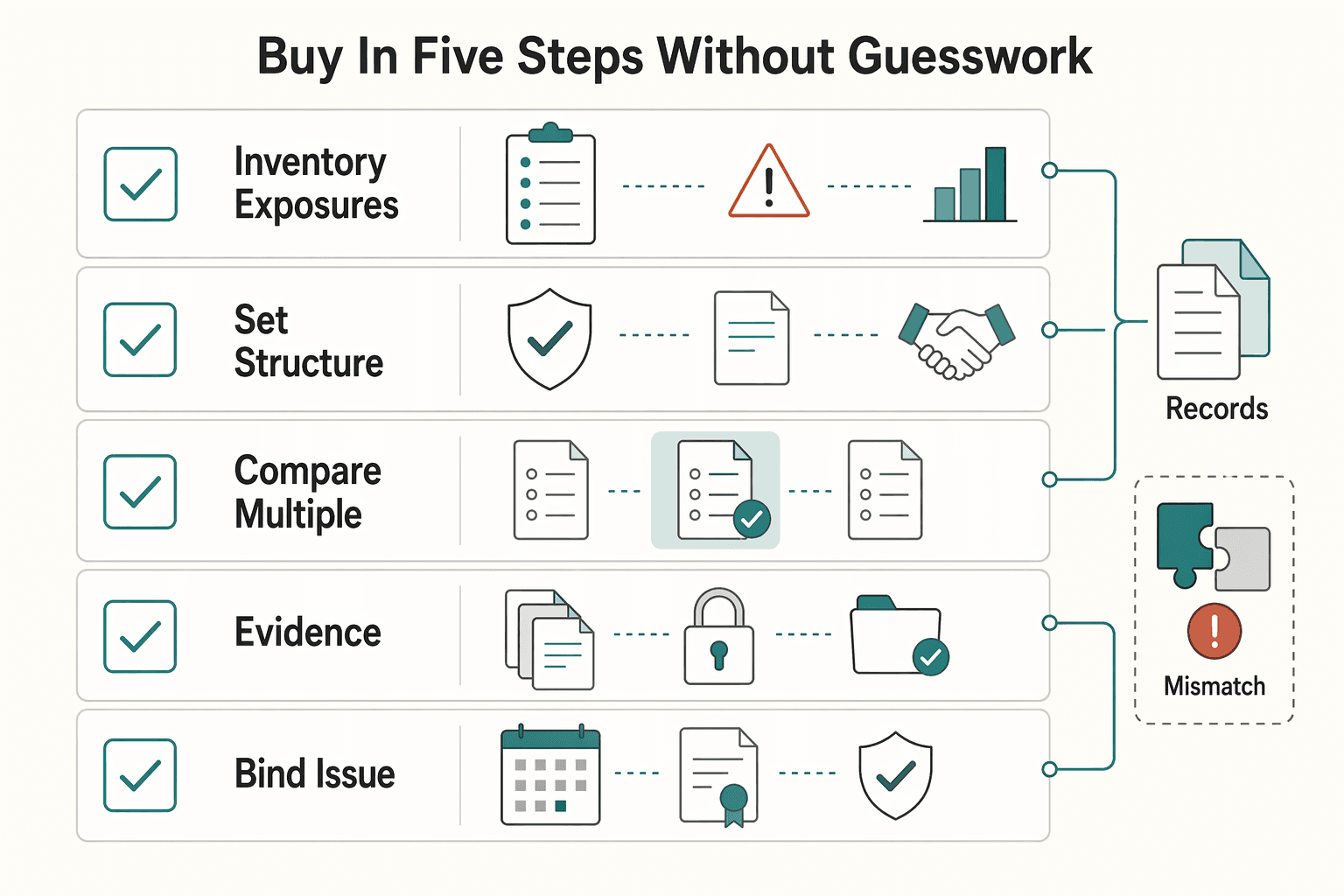

Buy in Five Steps Without Guesswork#

Use a fixed five-step process so you compare like-for-like and bind coverage you can actually use.

| Step | Primary action | Key check |

|---|---|---|

| Step 1 | Inventory exposures and contract promises first | List each service, the core risks tied to it, and the promise language in every Liability clause and Indemnification clause |

| Step 2 | Set your structure before requesting quotes | Choose target limits and a Policy deductible you can realistically pay, and set payment preference early |

| Step 3 | Compare multiple offers on one normalized sheet | Confirm coverage type, term dates, limits, and deductible before comparing price |

| Step 4 | Validate claims and policy documents in writing | Confirm which documents you will receive and when; pause until you receive written confirmation if key answers are unclear or verbal only |

| Step 5 | Bind and issue a client-ready COI immediately | Bind only after named insured details are accurate, then request a Certificate of Insurance (COI) with correct holder information |

- Step 1: Inventory exposures and contract promises first.

List each service you provide, the core risks tied to it, and the promise language in every Liability clause and Indemnification clause. Keep one sheet with client name, contract name, and renewal timing. If you want a clause refresher, review Limiting Your Risk: How to Use Liability and Indemnification Clauses. Include a short note on which promise creates the highest downside so you know where to spend review time first.

- Step 2: Set your structure before requesting quotes.

Choose target limits and a Policy deductible you can realistically pay if a claim happens. Higher deductibles can reduce premium, but only if you can cover that amount without strain. Set payment preference early, since annual payment may reduce total cost versus monthly installments. Lock this structure before shopping so each quote answers the same question.

- Step 3: Compare multiple offers on one normalized sheet.

Collect offers from providers or marketplaces using the same inputs for each quote. If NEXT appears as ERGO NEXT Insurance, track it as one provider name. Confirm coverage type, term dates, limits, and deductible before comparing price. Treat displayed online prices as estimates, and confirm final price and payment terms before ranking options. If one quote is missing exclusions or document timing, flag it and request detail before ranking options.

- Step 4: Validate claims and policy documents in writing.

Before binding, confirm which documents you will receive and when. Ask each provider the same questions so your comparison stays consistent. If key answers are unclear or verbal only, pause until you receive written confirmation. Save those confirmations with your quote sheet so future renewals start from clear records.

- Step 5: Bind and issue a client-ready COI immediately.

Bind only after named insured details are accurate, then request a Certificate of Insurance (COI) with correct holder information. Many clients, especially larger companies, ask for a COI before work starts. Save the COI and core policy documents together so renewals are easier. A clean file at bind time can cut follow-up back and forth during onboarding.

One avoidable breakdown is spreading these five steps across email threads with no single owner. Assign one owner for the quote sheet, one owner for contract checks, and one owner for final files, even if all three owners are you.

Before you bind coverage, you can tighten the contract language tied to liability and indemnity exposure with the Freelance Contract Generator.

Set Up a COI and Evidence Pack for Client Onboarding#

Create one client-ready insurance file before kickoff, with the COI first. Onboarding can stall when proof of insurance is missing.

Your anchor document is the Certificate of Insurance (COI). It confirms active coverage and shows key details clients may review: coverage types, policy limits, and effective dates. Put it first, then attach supporting documents when requested.

At minimum, a lean evidence pack can include:

- Current Certificate of Insurance (COI) for the active policy period.

- A simple version label such as insurer, policy period, and file date.

Before you send it, run a quick verification check: coverage types, effective dates, and policy limits match the client's stated requirements. If anything is off, request a corrected COI before submission.

Do one final send check before submission. The file name should make version and policy period obvious at a glance, and your archive should follow the same naming pattern. Clear naming can make follow-up easier.

When you renew or switch carriers, store prior versions by policy period. That habit can make later verification easier.

Review and Upgrade Coverage as Your Business Changes#

Review coverage when your contracts, services, or delivery model changes, not just at renewal. The core risk is letting insurance stay static while your work evolves.

| Trigger | When it applies | Review action |

|---|---|---|

| Risk profile change | If your services, client mix, or exposures shift | Review whether your policy mix still matches current work |

| Contract change | If a client changes insurance requirements | Recheck coverage limits and deductibles before signing |

| Compliance change | If a contract asks for Additional Insured or Waiver of Subrogation language | Confirm those endorsements before kickoff |

| Service change | If you begin handling sensitive data or software systems | Review whether current coverage still fits |

Freelance risk profiles vary, so your policy mix should reflect what you do now, who you serve, and what contracts require. A short review now is easier than fixing a mismatch after a claim.

Use these trigger checks when scope changes:

- Risk profile change: if your services, client mix, or exposures shift, review whether your policy mix still matches current work.

- Contract change: if a client changes insurance requirements, recheck coverage limits and deductibles before signing.

- Compliance change: if a contract asks for Additional Insured or Waiver of Subrogation language, confirm those endorsements before kickoff.

- Service change: if you begin handling sensitive data or software systems, review whether current coverage still fits.

Anchor updates to the contract terms you accept, so policy settings and endorsements match what you are agreeing to.

A simple habit keeps this manageable: log each scope change with date, what changed, which policy it affects, and next review date. This can make renewal easier and help you explain decisions if a claim question appears later.

Keep general liability in scope even for home-based work. Third-party injury and property-damage claims can still arise, and the financial burden can land on you even when fault is disputed.

Common Mistakes That Leave Freelancers Unprotected#

Protection gaps often come from execution details, not just from whether insurance exists. A common pattern is a mismatch between your coverage, your contracts, and the proof package a client expects.

-

1) Single-policy blind spot. Relying only on general liability can leave a gap when your work depends on professional judgment. General liability covers third-party injury and property damage, while professional liability addresses service-related malpractice, errors, and negligence.

-

2) State rules treated as universal. Insurance requirements are not one-size-fits-all: laws vary by state, and businesses with employees have federal requirements such as workers' compensation, unemployment, and disability insurance.

-

3) Policy terms reviewed too late. A policy can look complete until a claim falls outside what it covers. Review key terms before signing and compare them with contract obligations so you can adjust coverage or contract language early.

-

4) COI handling treated as a formality. A Certificate of Insurance (COI) is often part of a structured procurement review, not just an attachment. Follow the required submission and approval process, and submit the specified form when needed, such as ACORD 25 (2016/03).

-

5) LLC overconfidence. A Limited Liability Company (LLC) can help separate personal and business assets, but that protection has limits. If your team or service risk changes, reassess coverage.

Use this list as a monthly self-audit. If any item gets a "yes," create one corrective task with an owner and due date. Small fixes made early are easier than rebuilding coverage and contract files after a problem appears.

Your Next 30 Days to Get Properly Covered#

Use the next month to lock in a usable baseline. You do not need a perfect setup now, but you do need coverage and core documents ready when needed.

- Decide your starter stack based on current exposure.

General liability can cover common third-party accidents, and professional liability is another policy type to evaluate. If cyber risk is relevant to your work, include cyber insurance in the same comparison round. If hiring could happen soon, ask about workers' compensation early so you are not rushing later.

- Compare quotes on matched assumptions.

Use one application to collect multiple carrier options, then compare them side by side on the same assumptions. Some flows return real-time options from 30+ insurers, but that only helps when the quotes are truly comparable.

- Run one requirements check before your next signature.

Review the insurance requirements in your agreement and compare them with your draft policy details and COI process. If requirements look broader than what your policy appears to cover, pause and clarify before signing.

- Close the month with clean documentation and one annual review date.

Confirm your COI is available when coverage is bound, and verify your policy and client paperwork use the same business name. Save a compact file for each client with the COI, policy summary, and signed agreement. Then set one annual reminder to review limits, deductibles, exclusions, and business details.

If you want a clear timeline, split the month into four checkpoints. Week one sets policy structure, week two normalizes quote comparisons, week three checks agreement requirements and COI readiness, and week four finalizes files and review reminders. The sequence is simple, and it keeps decisions from slipping into last-minute pressure.

As you implement your 30-day plan, keep your operations consistent from invoicing to payment with Gruv for Freelancers.

Frequently Asked Questions

Do freelancers really need business insurance if they work from home?

Yes. Home-based work still carries business risk, and homeowner endorsements for business activity can be limited. Ask your insurance agent to confirm exactly what your home policy does and does not cover. If the answer is vague, request written clarification before assuming your home policy fills business gaps.

What insurance matters most first for a solo freelancer?

If your income depends on advice and deliverables, start with professional liability and general liability. Professional liability addresses service-related errors or negligence, while general liability covers third-party injury or property-damage claims. That pairing addresses both service-related and third-party injury/property-damage risks.

Is errors and omissions insurance the same thing as professional liability insurance?

In many freelancer contexts, these terms refer to the same core protection for negligence, errors, or incomplete work. Policy wording can still differ by insurer. Review coverage forms and exclusions before treating quotes as equivalent.

When does workers’ compensation insurance apply to freelancers?

Requirements can vary by jurisdiction and business setup, so avoid assumptions about when coverage applies. Confirm local requirements with a licensed advisor before deciding workers’ compensation is optional.

What does a Certificate of Insurance do, and when will clients ask for one?

A Certificate of Insurance (COI) is a document clients may request to confirm your coverage details. Whether a client asks depends on their contract and risk requirements. Some also ask to be listed as additional insured to extend liability coverage for claims tied to your work.

How should freelancers think about insurance costs when quote examples vary so much?

Treat public examples as directional, not decision-ready. Compare offers only after limits, deductibles, exclusions, and bundles are aligned. One 2020 survey cited that more than 40% of independent contractors said lacking insurance caused money or legal issues.

Does forming an LLC mean I can reduce or skip liability coverage?

No. An LLC can separate personal and business assets, but it does not shield you from every liability type, including service-related mistakes and client disputes. Keep liability coverage active after formation and keep policy details aligned with your legal entity. Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers is a useful companion.

Watch

Do Freelancers Need Business Insurance?

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- federalregister.gov/documents/2024/04/03/2024-06551/short-term-l...trusted

- ogs.ny.gov/insurance-requirementstrusted

- sba.gov/business-guide/launch-your-business/get-busi...trusted

- atlasinsurance.com/understanding-business-insurance-for-freelan...external

- buildbunker.com/2024/11/07/from-quotes-to-coverage-a-step-by...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Freelance Liability Clauses That Limit Risk Without Stalling the Deal

Start with one written freelance contract, then negotiate liability-related terms from that same text. That keeps payment, scope, and risk terms tied to the same deal. If you skip that step, both sides are more exposed to misunderstandings and avoidable disputes.

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

When Should a Freelancer Upgrade from Sole Proprietor to an LLC?

Forming an LLC is usually an operations decision before it is a tax decision. If you are weighing a move from sole proprietor status to an LLC, start with exposure, contract risk, and how money moves through the business. Treat federal tax treatment as a separate choice, and verify it through IRS guidance instead of assumptions.