Quick Answer

Start by matching policy type to your move pattern: trip-based plans for defined travel windows, broader international cover for longer stays or repeated country changes. For digital nomad health insurance, the fastest path is to verify certificate wording, emergency procedures, and claim-document requirements before payment, then buy the option that can issue visa-ready documents quickly. If pre-existing-condition or evacuation language is vague, pause and remove that option.

Start Here if You Are Moving in the Next 90 Days#

If your move date is close, treat this as a decision-first comparison, not a search for a single "best" provider. Under a 90-day clock, the real risk is not missing the perfect option. It is buying a plan that looks fine on a landing page, then discovering the certificate is too thin for visa review or the claims language is too vague once you are already abroad.

The fastest way to avoid that rework is to sort by use case and document clarity first, then compare price within a smaller set. This guide follows that order. First decide what type of coverage belongs on your shortlist. Then test the policy details that actually change what happens in the real world. Only after that should premium break a tie.

Focus on three things: required paperwork, long-stay reality, and contract language risk. Many nomads spend significant parts of the year abroad, so their needs are not the same as someone taking a few short trips. Travel insurance can help with nonrefundable reservations and emergency medical events during travel, but that does not make it a long-stay healthcare solution by default.

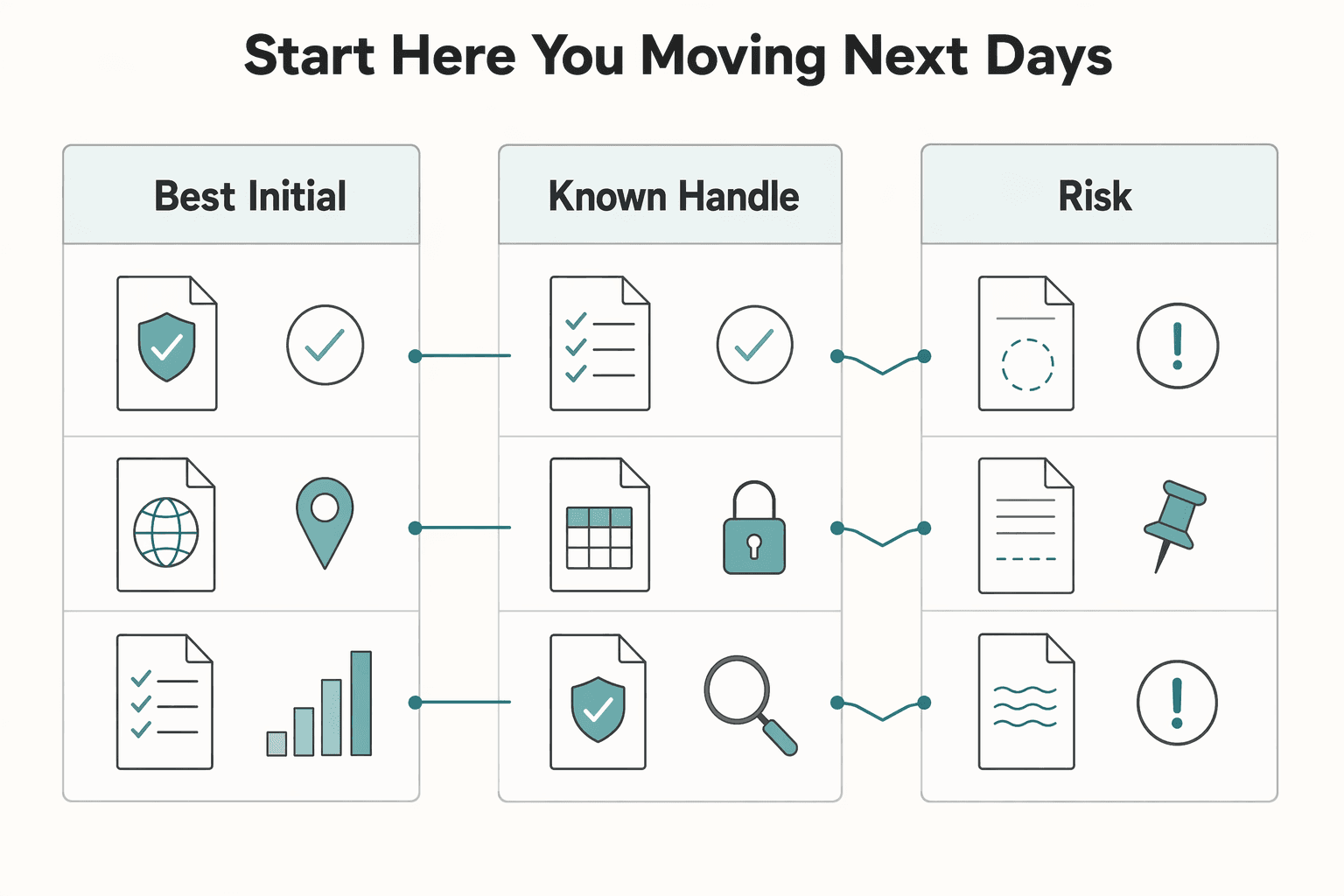

| Decision lens | Travel insurance | International health insurance | Country-tied domestic coverage |

|---|---|---|---|

| Best initial fit | Shorter, trip-based plans | Repeated moves or longer stays abroad | People living most of the year in one country |

| What it is known to handle | Trip costs and emergency medical events during travel | Longer-stay health coverage needs | Local eligibility where residency rules are met |

| Main risk before purchase | Assuming trip cover equals long-stay health cover | Assuming one policy setup fits every travel pattern | Ineligibility if you are not spending most of your time there as a tax resident |

Use the table as a triage tool. You are choosing the right lane first, not the right logo. If you already know you need ongoing care across borders, do not spend a week comparing trip-first plans that were never built for that use case. If you mainly need emergency support for a defined trip, do not assume a broader international policy will automatically be better on documents or day-to-day practicality. Country-tied coverage can make sense when you truly live most of the year in one place, but it becomes risky if the policy assumes a residency or tax-residency setup you do not actually meet.

Build one shortlist this week and keep it tight. Start with 3 to 5 options you can buy now. That is enough contrast to make a decision without drifting into endless research. Cut that list to two finalists only after document checks.

A tight shortlist also makes verification cleaner. When you compare too many providers at once, it becomes easy to mix up which certificate said what, which support reply came from which insurer, and which exclusions still need confirmation. A short list lets you track unresolved points line by line instead of relying on vague impressions.

Use this verification checklist before payment:

- Confirm the policy certificate language matches the documents you need to submit. Strong benefits do not help if the certificate is too generic for review.

- Confirm what the policy says about emergency medical care while abroad, including how it defines the emergency and what happens after the first visit.

- Confirm whether mid-trip extension is possible if dates slip. Move timelines slip often, and this is an easy detail to miss.

- Confirm cancellation limits so you do not assume non-covered reasons are valid.

- Confirm who to call first during an emergency and what records you must keep. Claims trouble often starts with missed admin steps, not the medical event itself.

When you do that check, read like a reviewer, not a shopper. Ask yourself whether a third party could understand the coverage from the certificate alone, whether the emergency process is clear without a phone call, and whether the wording answers your actual use case instead of a generic one. If you have to fill in the blanks yourself, the file is probably not ready.

Then run a one-week purchase timeline:

- Day 1: Build your shortlist and remove options that cannot issue documents quickly or answer basic wording questions.

- Day 2 to 3: Read the certificate wording and coverage summary line by line. Mark vague clauses instead of telling yourself they are probably fine.

- Day 4: Send one clarification email per finalist and keep written replies in the same folder as the certificate.

- Day 5: Buy the best documented option, not the lowest headline premium.

- Day 6 to 7: Assemble your required documents and do a final cross-check before submission so the file you send matches the policy you think you bought.

That final cross-check matters. A common problem is not that the policy is wrong, but that the submission pack does not clearly show the parts a reviewer needs to see. Put the certificate, benefits summary, receipt, and any written clarifications together before you submit anything. If a provider gave an important answer by email, save it with the rest of the pack so you are not hunting for it later.

If one key clause is vague, stop there. A common failure mode is buying first, then learning the paperwork language is too thin for document review or claims handling. Once you filter on that basis, the comparison in the next section becomes much more useful.

At-a-Glance Comparison Table for the Top Nomad Options#

Use this table as a screening tool, not a winner board. It is intentionally conservative because the available material does not support treating plan-level benefits as confirmed when they are not. That may feel less satisfying than a ranked list, but it is more useful when you are about to spend money.

| Provider | Multi-country coverage | Hospital stays | Prescription medications | Medical evacuation | Repatriation coverage | Pre-existing conditions | Best fit profile | What is still unknown until policy wording review | Confidence label |

|---|---|---|---|---|---|---|---|---|---|

| SafetyWing | Needs direct plan verification | Needs direct plan verification | Needs direct plan verification | Needs direct plan verification | Needs direct plan verification | Needs direct plan verification | Candidate for people planning repeated country moves | Exact inclusions and exclusions, claim documentation, reimbursement timelines, and activity-related coverage terms | needs direct plan verification |

| Genki | Needs direct plan verification | Needs direct plan verification | Needs direct plan verification | Needs direct plan verification | Needs direct plan verification | Needs direct plan verification | Candidate for long-stay remote workers comparing nomad-focused options | Exact coverage triggers, exclusions, required claim proof, reimbursement timelines, and emergency-evacuation wording | needs direct plan verification |

| World Nomads | Needs direct plan verification | Needs direct plan verification | Needs direct plan verification | Needs direct plan verification | Needs direct plan verification | Needs direct plan verification | Candidate for travelers blending mobility with activity-related risk | Country-by-country scope, exclusions, documentation burden, reimbursement timelines, and pre-existing-condition treatment | needs direct plan verification |

| Cigna Global | Needs direct plan verification | Needs direct plan verification | Needs direct plan verification | Needs direct plan verification | Needs direct plan verification | Needs direct plan verification | Candidate for readers evaluating broader international health insurance paths | Plan-level differences, exclusions, claim evidence requirements, reimbursement timelines, and evacuation/repatriation wording | needs direct plan verification |

| Insured Nomads | Needs direct plan verification | Needs direct plan verification | Needs direct plan verification | Needs direct plan verification | Needs direct plan verification | Needs direct plan verification | Candidate for mobile professionals wanting one policy across locations | Scope boundaries, exclusions, claim documentation, reimbursement timelines, and emergency transport terms | needs direct plan verification |

In practice, the rightmost columns matter most. "Best fit profile" is only a starting hypothesis based on how each option is framed in current material. "What is still unknown" is the real work list. If an option cannot answer those questions clearly in writing, it is not ready for purchase, no matter how familiar the brand sounds.

That is why the table leans so heavily on verification. It keeps you from importing assumptions from category, brand recognition, or community chatter into plan features that still need proof. If you are buying on a deadline, this filter is faster than undoing a weak purchase later.

One omission is worth noting. Blue Cross and IMG are often mentioned, but fit for nomad-style international coverage is unclear from current material. A provider can be widely discussed and still be a weak fit for this specific use case if the available material does not establish how cross-border care, paperwork, and claims actually work.

The safest way to use the table is to turn each unknown into a yes, no, or unresolved item in your notes. Do not leave anything sitting in the middle as a hunch. If you cannot verify hospital handling, refill rules, evacuation steps, or pre-existing-condition treatment from policy wording, keep the cell functionally blank in your own notes and treat the issue as open. That discipline matters because buyers often slide from "probably included" to "included" without noticing they did it.

Keep only two finalists after written verification of what is included and excluded, especially pre-existing conditions, emergency evacuation, activity-related coverage, required claim documentation, and reimbursement timelines. If replies stay vague, remove that option before payment. Vague answers are not just a research inconvenience. They are an early warning about how hard claims or document review may be later. For broader context, read The Best Travel Insurance for Digital Nomads.

Travel Insurance and International Health Insurance Are Not Interchangeable#

Get the category right before you compare brands. Travel insurance, international health insurance, and expat insurance overlap just enough to confuse buyers, but not enough to treat them as substitutes.

Travel insurance is trip-based and can combine emergency medical cover with travel-related benefits. International private medical insurance is built for people living or working abroad for longer periods, including six months or more. Expat insurance is a subset of international coverage for people living abroad long term.

The overlap is real, which is why people get tripped up. Both categories can mention medical events abroad. The problem is that the use case is different. A plan that works well for a defined trip can be a poor fit once the situation becomes follow-up care, planned care, or a stay that no longer behaves like travel.

The most common mistake is assuming trip-based cover provides the same protection as international medical cover. It may not, especially for care that is not urgent. Some travel policies may decline treatment that can wait until you return home. That gap matters when an emergency turns into follow-up care, or when you need clearer proof of coverage for a longer stay abroad.

A simple way to think about it is this: the first medical event is not always the full event. An initial emergency visit may be straightforward, but what happens after that can determine whether the policy actually fits your move. If the likely next step is observation, follow-up, prescription management, or care that no longer counts as urgent, category fit becomes the real issue.

Use this rule before you buy:

- If you have a defined short trip and a clear return date, start with travel insurance and verify the emergency terms. A clear return date makes the limits and assumptions easier to judge.

- If you expect six months or more abroad, ongoing care, or repeated country moves, start with international health coverage options. The longer and less fixed the stay, the more continuity matters.

- If you plan to live abroad long term in one place, evaluate expat-focused options alongside local eligibility requirements. Local rules can matter as much as the policy itself.

Before you pay, ask each finalist in writing what they classify as emergency care, how non-emergency care is handled abroad, and what claim documents are required. Keep those replies with your policy certificate and benefits summary so you are not relying on memory later.

That written exchange does two jobs. It shows how the provider frames your use case, and it gives you a record of what was said before purchase. If the answer comes back broad, indirect, or full of marketing language, that is useful information too. It tells you the point still needs policy-level proof.

The failure mode to avoid is simple: picking a trip-first plan for convenience, then finding follow-up care is treated as deferrable until you return home. For U.S. readers, do not assume Medicare fills that gap abroad; it generally does not, except limited border-related emergencies. Once you know which category belongs on your shortlist, the next decision is which coverage details actually change the outcome.

The Coverage Criteria That Actually Change Your Outcome#

Price is a weak sorting tool until you deal with the terms that change access to care, transport, and reimbursement. The simplest way to compare plans is to use a must-have, nice-to-have, and deal-breaker filter before you look at premium. For cross-border living, treat unclear wording as unconfirmed until the policy text says otherwise.

Must-haves keep a plan on the list. Deal-breakers remove it even if everything else looks attractive. That sounds strict, but it is the only way to keep the shortlist honest.

| Criterion | Priority | Why it changes outcomes | What to verify in policy wording |

|---|---|---|---|

| Multi-country coverage | Must-have | Nomad healthcare needs are ongoing and cross-border, not a single fixed trip | Country scope, renewal continuity, and whether coverage ends after short windows (for example, 90-day limits) |

| Hospital stays | Must-have | Inpatient events are where costs and claim risk escalate fastest | Admission terms, exclusions, and required claim documents |

| Prescription medications | Must-have | Ongoing care can fail if refills are not workable across borders | Refill rules abroad, formulary limits, and submission requirements |

| Medical evacuation | Deal-breaker if unclear | Transfer support is high impact in emergencies | Trigger conditions, authorization steps, and who coordinates transport |

| Repatriation coverage | Deal-breaker if unclear | Return transport responsibilities can become complex fast | Covered events, limits, and approval requirements |

The easiest comparison mistake is treating those rows as labels instead of processes. A provider can mention hospital cover, prescriptions, evacuation, or repatriation without giving you the details that determine whether you can actually use them. The words matter, but the path matters just as much. Who authorizes what, what counts as eligible, what documents must be submitted, and when approval is required are the parts that shape the real outcome.

Dental treatment and mental health treatment need a separate checkpoint. They are easy to assume and expensive to guess at. Do not treat either as included until scope, limits, and exclusions are explicit in the contract language. If an item is critical and the wording relies on broad labels without process detail, treat that as a real gap.

Pre-existing conditions deserve the same discipline. Marketing copy is not your answer. The decision lives in exclusions, waiting logic, and eligibility terms. If those terms are not provided before purchase, remove that option. If the provider gives you only a verbal explanation, ask for it in writing and save it with the rest of your file.

Claims friction deserves its own checkpoint too, because a valid medical event can still turn into a messy reimbursement experience if the admin path is vague. For emergency care outside your home country, verify:

- the exact evidence required to file

- submission windows and reimbursement timing

- whether pre-authorization is required for hospitalization or transfer

Save those confirmations with your policy certificate and benefits summary. They are boring details right up until you need them. That is why a clean-looking quote is not enough to make the call.

A practical way to review this is to ask every finalist the same questions in the same format. Ask each one to point you to the language covering emergency care, hospitalization, prescriptions, evacuation, repatriation, and pre-existing conditions. Then compare not just the answers, but the precision of the answers. One provider may respond with contract wording and another with a sales summary. Those are not equal levels of confidence.

One reported case described a $2,100 out-of-pocket bill after an international illness when domestic U.S. coverage did not apply abroad and no travel policy was active. Use it as a process warning, not a drama point: if a criterion is unclear in writing, do not assume it is there. That filter makes the provider notes easier to read, because it keeps the focus on what is documented and what still needs proof.

Provider-by-Provider Notes with What We Know and What We Still Need to Verify#

This is where many comparison pieces drift into guesswork. It is better to be direct about what the current excerpts do and do not establish. The notes below are useful because they keep uncertainty visible instead of smoothing it over.

| Provider | What we can say from current excerpts | Likely strengths | Likely limits | Verify before purchase | Usually for |

|---|---|---|---|---|---|

| SafetyWing | One comparison source lists Remote Health at $206/month and positions it as comprehensive global health coverage at home or abroad. | May suit people who want one cross-border health policy. | That price is a dated snapshot and not enough to judge current value or fit. | Written terms for pre-existing conditions and repatriation coverage, plus waiting logic and current pricing structure. | Long-stay professionals who want continuity across countries. |

| Genki | Available excerpts still do not confirm plan-level terms. | Candidate to keep in comparison only after policy text is provided. | No confirmed detail here on pricing structure, exclusions, waiting periods, or network constraints. | Exact wording for pre-existing conditions and repatriation coverage before purchase. | Mobile professionals planning repeated border moves. |

| World Nomads | Excerpts indicate broad country eligibility, mid-trip extension, Nationwide underwriting, COVID-related claims without a pandemic exclusion, and no cancellation for fear of travel. | Practical for travel-led profiles that need flexibility during active trips. | Travel insurance can have time-out-of-country limits, and cancellation flexibility is not unlimited. | Whether your plan variant supports long-stay needs, plus written pre-existing conditions and repatriation coverage terms. | Short-term travelers or mixed travel with defined return windows. |

| Cigna Global | Current material does not confirm plan specifics. | Candidate for long-stay comparison once policy wording is in hand. | No confirmed detail here on network design, exclusions, waiting periods, or pricing structure. | Plan language for pre-existing conditions and repatriation coverage, including emergency-claim evidence requirements. | Ongoing-care profiles comparing long-term international options. |

| Insured Nomads | Available excerpts do not confirm plan specifics. | Candidate for multi-country comparison once terms are documented. | No confirmed detail here on pricing structure, exclusions, waiting periods, or network limits. | Policy certificate wording for pre-existing conditions and repatriation coverage, plus emergency approval process. | Mobile professionals balancing travel and longer stays. |

Read these rows as screening notes, not endorsements. SafetyWing is the only row with a dated price anchor in the current excerpts. World Nomads is one of the few rows where the excerpts state several travel-related features. The rest still depend on actual plan wording before they can be judged fairly. That unevenness is useful because it shows where certainty exists and where it does not.

Notice what is missing. Outside one dated price reference, the available material does not give enough plan-level detail to treat any of these rows as a finished answer. That does not mean the providers are equal. It means the responsible next step is written verification, not speculation.

The biggest practical gap across this shortlist is the same one buyers often try to skip: pricing structure, exclusions, waiting periods, and network constraints are still not fully established in the available excerpts. That is why the shortlist should stay short. Keep finalists only after both providers return clear written terms for pre-existing conditions and repatriation coverage.

When you contact providers, keep the questions narrow. Ask for the policy certificate, benefits summary, and written wording on the specific issues that matter to your move. If the response is fast but generic, that is not the same thing as clarity. If the response points you to the exact wording, that is a stronger sign even before you get to premium.

If one provider gives you crisp contract language and the other gives you general sales language, the clearer provider is usually the safer choice even before price enters the discussion. That is the real value of this section. It stops the comparison from turning into a guessing contest. Given that level of uncertainty, the sensible next step is to choose the provider type that fits your situation first, then test individual providers inside that lane.

Which Provider Type Fits Your Situation#

Start with your situation, not with brand reputation. Move pattern, care needs, and visa timing matter more than a logo. This table is not telling you what to buy. It shows you where to begin so you do not spend a week comparing unlike products and end up back where you started.

| Situation | Better starting point | Why this can fit | Verify before payment |

|---|---|---|---|

| Healthy remote worker changing countries often | Travel insurance first | Travel-focused plans are commonly built for disruptions and emergencies, including delays, document loss, emergency treatment, and repatriation | Trip length limits, renewal terms, repatriation wording, and eligibility across frequent country changes |

| Long-stay relocation with planned care | International health insurance first | Longer stays often need broader ongoing medical handling than trip-focused cover | How hospital care, prescriptions, follow-up care, and cross-border claims are handled in writing |

| Known pre-existing conditions | The plan with the clearest underwriting language | A lower premium is less useful if exclusions or waiting terms limit real use | Exact exclusions, waiting terms, acceptance criteria, and claim review requirements |

| Visa-led move on a deadline | The option with the fastest clear documentation | Visa processes often depend on document readiness as much as coverage | Certificate wording, issuance timeline, and whether documents match your visa checklist |

The tradeoff is straightforward. Travel-focused cover often aligns with disruption and emergency risk during active movement. Broader international cover is the better starting point when the move includes ongoing care, planned care, or a long stay that stops feeling like a trip. Many bad purchases happen when people choose the simpler-looking category and only later discover the follow-up care gap.

Use this as the working rule: pick trip-focused cover for defined travel risk, and start with broader international cover when your move includes ongoing care needs. In both cases, confirm repatriation and medical terms in writing before you commit.

Treat pre-existing conditions as a separate gate, not a detail to check at the end. Do not rank final options until each provider gives written terms for exclusions, waiting periods, and required claim documents. A lower premium does not offset unclear underwriting language.

For visa-led timelines, request the certificate sample and required claims paperwork early, then compare them against official country guidance before purchase. This is one of the few steps that can save both time and a repurchase. Once the move is visa-based, the document work becomes the real schedule.

It helps to picture the difference between a travel-led move and a care-led move. In a travel-led move, the main question is usually whether the plan can support you during movement and respond clearly in an emergency. In a care-led move, the main question is usually whether treatment can continue without the policy treating your life abroad as an edge case. That contrast is already present in the categories above; the goal is to make sure your shortlist reflects it.

Timeline and Document Checklist for a Visa-Based Move#

For a visa-based move, sequencing matters as much as the policy itself. A plan can be fine on coverage and still fail the process if the certificate is vague or the file is incomplete.

Start early and work in stages. A practical relocation model uses an 8 to 12 month runway. If you have less time, keep the same order and compress the timeline instead of skipping steps. Each stage depends on the last one, so rushing the wrong step usually creates more work later.

In practice, the insurance task is half coverage review and half document assembly. The mistake is treating those as separate jobs. For a visa move, they are the same job, because the policy only helps if the certificate and supporting papers actually satisfy the file.

| Stage | Main action | Verification checkpoint | Evidence to store |

|---|---|---|---|

| Week 1: Shortlist | Shortlist plans that fit your stay and care needs | Confirm the plan type fits your move pattern | Comparison notes and rejection reasons |

| Week 2: Wording review | Review certificate and coverage language before purchase | Check clarity on what is covered, excluded, and how to use emergency support | Marked policy wording and written clarifications |

| Week 3: Purchase | Buy only after wording passes your checklist | Confirm issue timing and document delivery format | Receipt and final policy certificate |

| Week 4: Visa pack build | Assemble visa-ready insurance documents | Match your file to official visa guidance for your target country | Policy certificate, coverage summary, emergency contact process, and proof of medical evacuation and repatriation coverage where required |

| Week 5: Submission | Submit your Digital Nomad Visa file | Run one final checklist pass against official government requirements | Full packet copy and submission confirmation |

This sequence works because it blocks false confidence. Shortlisting without deciding the plan type creates noise. Buying before wording review creates rework. Building the visa pack before you know exactly what the certificate says creates a file that looks complete but may still fail review.

A practical way to run the process is to create one folder per finalist and keep the same documents in each one: certificate sample, benefits summary, any clarifying emails, pricing information, and your own notes on open questions. That makes the final comparison much easier because you are not switching between tabs and trying to remember which provider answered which point. It also gives you a clean record if you need to explain why you chose one option over another.

Use the Global Digital Nomad Visa Index to identify your destination, then validate every document against official government guidance before submission. If there is a conflict, follow the government source and request revised insurer wording in writing. The government checklist is the final authority for the file you submit, while the insurer wording is the final authority for what you actually bought. You need both to line up.

When you build the visa pack, read it from the outside in. Do not ask only whether you have the documents. Ask whether someone unfamiliar with your situation could see the insured person, the policy dates, the type of coverage, and any required transport language without guessing. A technically complete pack can still create friction if the key details are buried or expressed too generally.

A common failure mode is buying first, then discovering the certificate language is too vague for review. Missing documents can cause delays or legal consequences, so treat document readiness as a gate before payment, not an afterthought. If you are behind schedule, compress shopping time, not verification. If you need a quick way to organize the next step, browse Gruv tools.

Red Flags That Cause Delays, Denials, or Bad Surprises#

Most bad surprises announce themselves early. People just talk themselves past the warning signs because the provider feels familiar, the premium looks good, or a community thread sounds confident. Until the contract language and certificate text confirm it, treat it as unverified.

A useful example is brand affiliation. A Blue Cross affiliation can be legitimate as a licensed partnership, but that still does not guarantee the claims experience people expect from traditional BCBS plans. Brand familiarity is not a substitute for contract review, especially when the move depends on specific certificate language and cross-border claims handling.

| Red flag | What it looks like | What to verify before paying | Decision rule |

|---|---|---|---|

| Community anecdote bias | Reddit or comparison threads promote providers (for example Cigna Global, Blue Cross, or IMG) without policy excerpts | Full policy text, exclusions, and certificate wording for your visa file | If you cannot trace the claim to policy wording, ignore the recommendation |

| Default-inclusion assumptions | You assume pre-existing conditions, mental health treatment, or dental treatment are included | Explicit inclusion or exclusion language in the policy and certificate | If wording is unclear, treat it as not covered until confirmed in writing |

| Premium-only decision | You choose by monthly price and skip wording-level checks | Exclusions, claims steps, and cross-border access process | If coverage and claims language are weaker, the lower premium is a false economy |

| Ambiguous evacuation language | Certificate uses broad terms like "emergency transport" without clear scope | Clear written wording for medical evacuation and repatriation coverage | If evacuation or repatriation wording is ambiguous, do not finalize purchase |

The pattern behind all four red flags is the same. People treat indirect signals as proof and only read the policy when there is already a problem. Reverse that order. If a provider cannot answer a direct question with direct wording, treat the issue as unresolved and pause the purchase.

Community discussion can still be useful, but only as a prompt for what to verify. It can help you notice recurring problem areas such as certificate acceptance, claims friction, or confusion around repatriation. What it cannot do is replace the policy text for your exact plan and route. Use those discussions as a question list, not as evidence.

Default assumptions are especially risky because they feel efficient. Buyers often think they are saving time by filling in likely answers for mental health, dental, or pre-existing conditions, then plan to clean it up later. In practice, later is when the application is due or the claim has already started. If an item matters to you, resolve it before purchase or treat it as a non-feature.

The common failure pattern here is buying first, then discovering the wording is too vague for review. Keep a hard stop before payment: if treatment scope or certificate clarity is still unresolved, pause and get written clarification. You do not need perfect certainty. You do need enough written clarity to know what you are buying and whether the certificate will stand up to review.

Make the Decision and Lock Your Next Step#

At this point, the decision should feel narrower than it did at the start. You are not trying to identify the best plan in the abstract. You are choosing the option that fits your movement pattern, can produce usable proof of coverage, and gives you a claims path you can actually follow.

Use your two finalists for one last pass. If your needs are mostly trip-focused, a travel-first option may fit. If you expect ongoing care across countries, broader international coverage may fit better. If both still look close, let document readiness and claims clarity break the tie. Those are the parts most likely to matter under a deadline.

| Final gate | What to confirm | Why it changes the decision |

|---|---|---|

| Residence setup | Your country of residence is entered correctly and matches your legal status | Some providers tie displayed information to residence context, including repatriation context for ongoing care |

| Visa document readiness | You can show your policy PDF, membership card, and proof of coverage quickly | Faster document access helps at visa review and clinic intake |

| Claims practicality | You know the claim path: clinic selection, receipt capture, insurer submission | If the process is unclear, reimbursement can become harder to manage |

| Pre-departure checks | You reviewed current government travel advice before departure | Official travel conditions can change before you leave |

Keep one evidence pack in cloud storage and on your phone: policy PDF, membership card, coverage hotline, and any written clarifications. If details around residence context, proof-of-coverage access, or claim submission are still unclear, pause before finalizing.

Before you click buy, ask one last plain-language question: if you had to use this policy in the first week abroad, would you know what to do without searching through old emails? If the answer is no, the problem may not be the coverage itself. It may be that the documentation and process are still too muddy to trust under pressure.

Your next step is simple: buy the clearer option or wait until the missing wording arrives. A short delay before purchase is usually easier to fix than a weak decision after submission or after a claim.

When your checklist is clear, take the next action and complete your filing flow. If you still need filing order, use How to Apply for a Digital Nomad Visa: A Step-by-Step Walkthrough with your insurance packet open beside it.

Frequently Asked Questions

What is the difference between digital nomad Travel insurance and International health insurance?

Travel insurance is usually trip based and focused on unexpected events during travel, not long-term healthcare. International health insurance is designed to follow you across countries for ongoing medical needs. If your move includes long stays or repeat care, start with international coverage and add trip-focused protection only for specific gaps.

What should digital nomad health insurance include at minimum?

At minimum, confirm cross-border medical coverage, emergency handling, and proof-of-insurance documents for visa use. You also need explicit wording for exclusions, claim steps, and how care is handled when you change countries. If a core item appears only in marketing copy, treat it as unconfirmed.

Does digital nomad insurance usually cover Pre-existing conditions?

Do not assume it does. Pre-existing or chronic conditions can involve exclusions, waiting periods, or other terms after disclosure. If you have a known condition, get written confirmation of how related claims are assessed before payment.

Which providers are most commonly compared for digital nomads?

Provider comparisons vary by route, visa context, and care profile. SafetyWing is one option with two tiers (Essential and Complete). Use any shortlist as a starting point, not a conclusion. Final selection should still come from policy wording, visa-document readiness, and claims clarity for your route and care profile.

What should I verify before buying a plan for a Digital Nomad Visa move?

Verify that the insurer can issue visa-ready proof of insurance and that certificate language matches your target country requirements. Confirm emergency procedures, exclusions, and claim documentation before payment. A useful final step is comparing your document pack against official visa guidance for your destination.

What is still unknown until I read full policy wording?

Critical details remain open until you read the contract: exact exclusions, limits, claim evidence requirements, and how ambiguous terms are interpreted. Even when a provider publishes clear tiers, such as SafetyWing Essential versus Complete, you still need the exact wording for your situation. If a term affects treatment access or visa acceptance and is not explicit in writing, do not finalize.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 5 external sources outside the trusted-domain allowlist.

- localsinsider.com/travel-insights/digital-nomad-health-insuran...external

- nomadsembassy.com/best-digital-nomad-health-insuranceexternal

- travlfi.com/blog/guide-to-digital-nomad-health-insurance...external

- twoticketsanywhere.com/digital-nomad-health-insuranceexternal

- worldnomads.com/ca-en/travel-insurance/whats-covered/digital...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Best Travel Insurance for Digital Nomads in 2026

The **best travel insurance for digital nomads** in 2026 is not the plan that tops a roundup. It is the one that clears your paperwork and still works when your route changes. For long stays, keep the order simple: paperwork first, continuity second, price third. Eligibility is part of that first check, because a cheap plan you cannot actually use is not a bargain.

How to Apply for a Digital Nomad Visa: A Step-by-Step Walkthrough

Use a country-specific sequence, not a generic checklist. If you want fewer surprises, use this order. Core requirements often overlap, but each country can add its own rules, and some filing locations add extra instructions. Stale guidance is a common source of delay.

The 2026 Global Digital Nomad Visa Index for 50+ Countries

Start with legal fit, not lifestyle filters. The practical order is simple: choose a route you can actually document, then decide where you want to live. That single change cuts a lot of wasted comparison work and stops you from falling in love with places that were never a real filing option.