Quick Answer

Choose based on file quality and forum clarity, not pressure alone. In collection agency vs small claims, agency-first usually fits when your venue is uncertain or you need immediate outreach with limited owner time, while court fits when your records are complete and you can handle filing and service steps. Before escalating, confirm Governing Law and Jurisdiction terms, send a final demand letter with delivery proof, and set one hard switch deadline.

Collection agency or small claims: pick for take-home, not toughness#

Do not pick the option that sounds toughest. Pick the one most likely to put money in your account with the least avoidable drag.

When freelancers weigh a debt collection agency against small claims, the real tradeoff is usually straightforward. You can delegate the chase and give up part of what is recovered, or you can keep more control and run the court process yourself, knowing that even a win may still leave you with follow-up work before any money actually arrives.

Both paths are formal in their own way. In consumer debt settings, the FTC has described creditors and collectors using both litigation and arbitration, and noted that those systems did not always provide adequate consumer protection at that time. Your unpaid invoice is a different setting, so treat that as a process lesson, not a direct forecast. The narrower point still matters: results depend on current rules, clean procedure, and disciplined evidence, not on which option sounds more serious.

| Decision criterion | Debt collection agency | Small claims court |

|---|---|---|

| Cost shape | Terms depend on the agency agreement and local law, so confirm pricing and obligations before you sign | Costs and procedural requirements depend on local court rules and case steps |

| Owner time load | Day-to-day chasing can be lower, but oversight and document support still matter | You are usually responsible for the procedural steps under applicable court rules |

| Outcome path | Recovery still depends on debtor response, evidence quality, and process execution | The case is rule-driven and can end in a judgment, but requirements vary by jurisdiction |

| Operational risk | Quality and results vary by agency practice and contract terms | Risk centers on filing accuracy, service of process, deadlines, and local rules |

Use that table as the lens for the rest of this piece. Judge both options on the same four things: expected take-home, owner time, collectability, and the amount of process risk you are taking on.

Before you sign with anyone or file anywhere, confirm commencement and service rules where you plan to act. Then verify that any legal text you rely on is current and from an official legal source. A surprising number of filing mistakes come from stale guides and unofficial summaries, not from any weakness in the underlying claim.

This is practical guidance, not legal advice. Filing rules, service mechanics, and enforcement tools vary by location, and those differences often decide whether court is efficient or whether an agency-first escalation is cleaner. With that frame in place, start with a quick comparison, then work through cost, time, leverage, and contract fit.

At a glance comparison for freelancers#

Freelancers usually make the wrong call here for one reason: they compare only the visible fees. That leaves out owner time, venue friction, and the fact that a judgment still is not the same thing as payment. The right first move is to screen for fit, not to chase whichever option looks cheaper on the surface.

Use the table below as a fast filter. It is meant to narrow the field, not make the whole decision for you.

| Criteria | Debt collection agency | Small claims court |

|---|---|---|

| Upfront cash outlay | If your contract uses a contingency fee agreement, upfront spend can be lower; confirm any setup or service fee in writing | Filing and notice or service steps are part of starting the case, and costs vary by court and location |

| Percentage of recovery kept | Under a contingency fee agreement, part of recovered funds goes to the agency | You may keep more of the award, but you carry filing costs and your own process time |

| Owner time | Agency-led outreach can reduce day-to-day follow-up work | You handle filing, records, hearing prep, and follow-up |

| Speed to first action | Depends on agency intake and launch timing | Begins after filing and court processing; defendant notice is a required step |

| Legal leverage | Collection pressure and settlement attempts | A court path for money claims that can end in a judgment |

| Relationship impact | Third-party collection contact can strain the relationship early | A filed claim is formal and can strain the relationship |

| Cross-border practicality | Can be used as an early pressure path when venue is unclear | Cross-border disputes usually need extra venue, notice, and enforcement checks |

| After you win risk | Any agreement still depends on payment compliance | A judgment is not the same as payment; collection can still require separate enforcement steps through local process, for example an enforcement officer where applicable |

| Best fit | Small debt, evasive debtor, unclear venue, limited owner bandwidth | Strong documentation, local court fit, and an owner willing to run procedure |

A quick read of that table usually points to one of two early conclusions. If your records are strong, the amount fits local limits, and the other side is reachable, court may be worth the extra work. If venue is unclear, the balance is modest, or you do not want to spend your week managing service, deadlines, and hearing prep, agency pressure can be the cleaner opening move.

Use local limits and procedure as a gate before you file. For example, New York small claims guidance shows different money limits by court type, up to $5,000 in City Courts and up to $3,000 in Town or Village Courts. The broader lesson is that caps, forms, service rules, and hearing process are jurisdiction-specific. If your amount does not fit the court or your notice process is shaky, the option that looks cheaper can become the expensive one very quickly.

Another practical filter is relationship value. If this is a one-off client who has gone silent, formality may not cost you much. If this is a recurring account, a strategic partner, or a client with a real dispute you may still want to unwind professionally, the opening move matters more. Agency contact can escalate tension early. Filing does too, but it does so in a different way, by moving the dispute into a public, procedural track.

Keep one red flag in mind: treat a judgment as a milestone, not the finish line. Court is often efficient when the claim fits local limits, the defendant is reachable, and your records are clean. If venue, notice, or later enforcement look messy, agency-first pressure may buy you faster information and a cleaner path to settlement before you spend more time on procedure.

If you want the procedural side laid out step by step, read Client Won't Pay? Your Step-by-Step Guide to Collecting Overdue Payments.

What each option actually costs when you include hidden work#

The most common math error is comparing an agency percentage to a filing fee and stopping there. That is not cost analysis. It is just comparing the most visible line items while ignoring the time and friction that actually determine what you keep.

Real cost is what remains after direct spend, your own time, and the drag involved in turning a paper win or a payment promise into money that clears. If you want a decision that holds up in practice, you have to count the work that does not arrive as a neat invoice.

Hidden work shows up differently on each route. On the agency side, it usually means account handoff, clarifying facts, answering questions, reviewing updates, and deciding whether to accept a settlement or payment plan. On the court side, it means filing, service, exhibit prep, hearing time, and follow-up if payment does not arrive after the ruling.

A simple way to think about it is to separate direct spend from indirect spend and refuse to blur them.

| Cost bucket | Debt collection agency | Small claims court |

|---|---|---|

| Direct spend | Contract-based charges tied to your agency agreement and outcome terms | Court-side costs set by local process and rules |

| Indirect spend | Your time for handoff, document support, and update review | Your time for filing steps, evidence prep, hearings, and follow-up collection work |

Indirect spend matters because it does not feel like a bill, even though it behaves like one. Agency use can lower the daily chase, but you still need to support the file, answer questions, and review offers. Court can preserve more of the award, but it also pulls you into deadlines, preparation, and appearances that compete with paid work. A common failure mode is comparing a contingency percentage to filing fees while silently valuing your own hours at zero.

That valuation mistake matters most for freelancers because your time is not overhead in the abstract. It is your sales time, your delivery time, and often your admin time all at once. A route that consumes half a day of court prep and follow-up is not free just because the filing fee looked manageable.

Fee claims in search results often conflict because agreement terms and case details differ. That is not just internet noise. It tells you the economics are driven by contract terms and local procedure, not by generic averages. If you do not have written agency terms and a realistic estimate of local court-side costs, you are still guessing.

Use this net-recovery check before you escalate:

- Set the claimed amount.

- Estimate recovery probability for each path based on response history, documentation quality, and venue fit.

- Subtract direct spend for each path.

- Subtract your time cost, using hours multiplied by your billable rate.

- Reduce for enforcement friction if payment may still require extra follow-up.

- Pick the route with the better expected take-home at an effort level you can actually sustain.

That last clause matters. The better path on paper is not always the better path for you. If the numbers are close, favor the option you can execute cleanly. A slightly smaller theoretical recovery is often better than a larger one that dies in paperwork, delay, or fatigue because you stop paying attention halfway through.

It also helps to separate probability from emotion. Many freelancers overweight the satisfaction of winning in court and underweight the administrative cost of getting there. Others do the opposite and assume outsourcing the problem makes it disappear. Neither instinct is especially useful. The question is narrower: which route gives you the best realistic net result for this claim, with this documentation, against this debtor, in this venue.

Keep one timing checkpoint in your file from the beginning: when the debt became delinquent and whether local rules can add charges after that point. For example, in the cited Oregon court context, case-balance debt can be considered delinquent after 30 days from the court order date, and Oregon law requires a fee on judgments that include money owed to the court. The broader point is not about Oregon alone. Delinquency timing and add-on rules can change the economics, so track that trigger date from the start rather than trying to reconstruct it later.

The decision usually gets easier once you price your own labor honestly. If your billable time is tight and the amount is modest, outsourcing some of the chase may be rational even if it means giving up a percentage of recovery. If the claim is well documented and the amount makes the extra work worthwhile, court may still be the better economic choice. The point is to compare full cost to full cost, not fee to fee.

Time to cash and operational drag#

Fastest to first action is not always fastest to cash. What matters is how many steps sit between today's decision and money that actually clears.

This is where many freelancers misread the choice. Agency outreach can often start sooner because intake and contact attempts are front-loaded. Court is slower to launch because filing, service, hearing preparation, and court scheduling all sit between your decision and any ruling. That extra structure can be worth it when your file is strong and local procedure fits. It becomes pure drag when you are still fixing identity details, notice problems, or proof of acceptance.

| Operational step | Debt collection agency | Small claims court |

|---|---|---|

| First action | Intake account details and begin collection outreach | Start formal case process and manage court steps |

| Main work owner | Agency runs communication cadence and negotiation attempts | Freelancer manages records, filings, deadlines, and appearances |

| Typical drag point | Incomplete account data slows outreach | Process mistakes, weak documentation, or missed dates can delay progress |

| After decision point | Continue negotiation and collection attempts | A judgment may still require follow-through if payment does not arrive |

The practical lesson is simple: do not confuse motion with progress. An agency can contact the debtor quickly, but if your handoff is incomplete, the file stalls. Court can create formal pressure, but if service is wrong or your exhibits are thin, the case drags or weakens before you reach a hearing. In both paths, the slowdowns are usually predictable.

Early negotiation is not a soft option when it is structured well. It can resolve some debts before either side spends heavily on court costs or major collection effort, and it can include partial-payment terms that get money moving sooner. Court can still be the right move, but it shifts more execution onto you. The useful question is whether the extra formality is buying you something concrete, or whether it is simply adding steps before you are back to the same collection problem.

A lot of time-to-cash problems begin before escalation. Missing identity details, old contact information, undocumented acceptance, and sloppy reminder records make every later step harder. That is why a clean file often matters more than your initial choice. If the file is weak, both routes slow down. If the file is strong, either route becomes easier to run.

Before you escalate, run this basic file check:

- Confirm debtor identity details match your contract and invoice records.

- Verify current contact channels for notices and outreach.

- If you already sent a final demand letter, confirm delivery and logging.

- Assemble acceptance evidence, invoice trail, and reminder history in one file.

- Verify any rule summary you rely on is current and from an official source.

This is the boring part, but it is also where a lot of delay gets created or avoided. If identity, contact, or delivery records are weak, tighten the file before adding more process. If the file is complete and you are ready to handle formal steps, court may justify the extra workload.

It also helps to think in terms of waiting points. Agency effort can mean waiting on debtor response and your own approval of settlement options. Court can mean waiting on service, scheduling, a hearing date, and then possible post-judgment follow-up. If cash speed is the deciding factor, map those waiting points honestly instead of assuming the more formal route is automatically stronger.

Once the file is tight, the next question is not just speed. It is leverage. You want to know whether more formality will actually improve your position or just add more tasks.

Legal leverage and where freelancers overestimate it#

Formality helps, but freelancers often overestimate what it buys them. An agency can apply steady pressure. A court can produce a judgment. Neither one turns a reluctant client into cash on its own.

That distinction matters because unpaid invoices create a strong emotional pull toward the option that feels more powerful. In practice, though, a harder tone is not the same as better collectability. The more useful distinction is narrower: agencies are good at persistent outreach, settlement discussion, and payment-plan attempts, while court is good at producing a rule-driven decision on a documented money claim.

| Pressure question | Debt collection agency | Small claims court |

|---|---|---|

| What it can do first | Run persistent outreach, payment-plan talks, and settlement discussion | Start formal adjudication that can end in a legal judgment |

| Where it slows down | No response or factual disputes | Filing, service, hearing timing, and possible post-judgment collection steps |

| Main limit to remember | Pressure alone does not force payment | A judgment does not always produce immediate payment |

The most common overestimate is post-judgment certainty. A ruling in your favor can matter a lot, but it is not the same as money received. Collection may still require additional steps, which adds time and effort after the hearing is over. That is why collectability belongs in the decision before you file, not after you win.

This is also where freelancers sometimes underrate structured settlement efforts. If the client is still responsive and the dispute is really about timing rather than denial, a written payment arrangement may outperform both a rushed filing and an unfocused agency handoff. The key is structure: exact amount due, clear payment dates, and a defined consequence if the arrangement fails. Without that, negotiation turns into drift.

Debtor status can stop progress entirely. If the client enters Chapter 13 bankruptcy, creditors are barred from starting or continuing collection efforts during the repayment period. That period is usually three to five years, and the plan cannot run longer than five years. If that possibility is in play, do not treat every delay as ordinary stalling when the legal ground may have changed underneath the dispute.

There is also a relationship tradeoff that deserves a realistic read. Some freelancers assume agency contact preserves the relationship because it creates distance. Sometimes it does. Other times, it hardens the dispute faster because the client feels pushed before they have been offered a structured chance to resolve it directly. Filing can have the same effect in a different register. Once the claim is formal, the conversation changes from overdue payment to procedural defense.

So before you escalate, run one clean checkpoint: verify whether there is an active bankruptcy filing, confirm your demand and settlement records are complete, and keep one clear contact timeline. If preserving the relationship is still a real business priority, start with a structured payment arrangement and written settlement agreement, then escalate if needed. If the relationship is already broken and your file is court-ready, filing may be cleaner than another round of loose promises and vague deadlines.

The point is not to avoid pressure. It is to use the kind of pressure that matches the actual problem. If the issue is silence and evasion, persistent outreach may be enough to force a response. If the issue is an unresolved money claim with good records and usable venue, court may be worth the lift. If you want the court side in more detail, see A Freelancer's Guide to Small Claims Court.

Contract terms that decide whether court is practical#

Court is efficient only when your contract tells a usable story about where the case belongs and what the client actually agreed to pay. If those clauses are vague, missing, or fighting each other, you can spend your energy arguing about forum and process before anyone reaches the unpaid invoice.

That is why contract review is not busywork here. It is the screen that tells you whether court is a practical next step or whether you should push for settlement or agency pressure first.

Start with three checks before you file: Governing Law, Jurisdiction, and Dispute Resolution. Those terms tell you whether court is available now, whether another forum is specified, and whether some earlier step must happen first. If they conflict or read vaguely, filing can become procedural work before the payment dispute is ever addressed.

Small claims is generally a money-judgment path, not an injunction path, so frame the claim around unpaid amounts you can document. Also confirm filing mechanics early. In the Rule 4 model, the plaintiff is responsible for arranging service of the summons and complaint within the allowed time. That sort of detail matters because a strong claim can still lose momentum over avoidable service problems.

| Contract check | Why it matters for practicality |

|---|---|

| Governing Law | Helps you assess whether court process is clear enough to proceed now |

| Jurisdiction | Helps you avoid avoidable venue disputes and delays |

| Dispute Resolution | Clarifies whether court is available now or only after another step |

| Monetary claim + records | Aligns with small-claims money-judgment posture |

Do not stop there. Read Termination, Limitation of Liability, and Indemnification too. They can change how the dispute is argued, so flag unclear language before filing. In practice, those clauses matter most when the other side tries to turn a straightforward nonpayment issue into a broader fight over scope, exit, or responsibility.

That move is common enough that you should plan for it. A client who owes a simple invoice may respond by reframing the whole engagement as a service failure, a scope mismatch, or a disagreement over what was approved. If your contract documents and approvals are clean, that tactic is easier to contain. If they are messy, a simple collection claim can become a wider argument that eats time and weakens your confidence even if the payment is still due.

Use this pre-filing file check:

- Signed contract and amendments.

- Change orders or written scope approvals.

- Invoice trail, including dates, amounts, and due terms.

- Acceptance evidence, such as delivery or approval messages.

- Final demand letter and delivery proof.

These documents do two jobs at once. They prove the money claim, and they help keep a scope dispute from swallowing a simple collection case. The cleaner the file, the less room the other side has to turn procedure into leverage.

A useful if-then rule follows. If Jurisdiction and Governing Law are unclear in a cross-border dispute, agency-first is often the more practical opening move, then file once forum risk is clearer. That does not mean court is off the table. It means you do not want your first big spend of time and attention to go toward fighting over where the dispute belongs.

Once the contract screen is clear, the decision gets much simpler. You are no longer choosing between two abstract tools. You are choosing the route that best fits the claim, the forum, and the quality of your evidence.

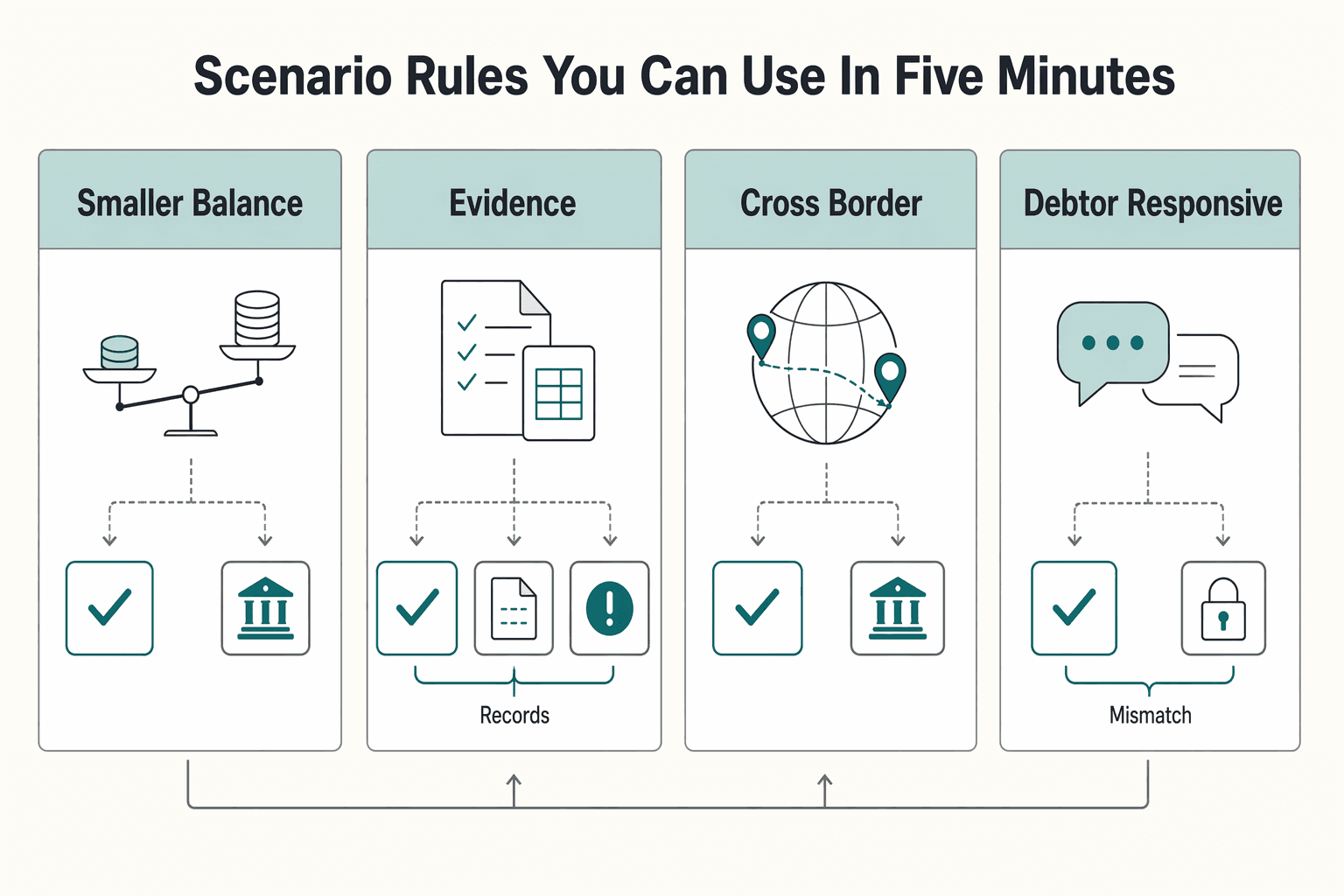

Scenario rules you can use in five minutes#

You do not need a perfect model to make a sound first move. You need a short rule set that accounts for the amount, the quality of your records, the clarity of venue, and how much owner time you can realistically spare. The goal is not theoretical precision. The goal is to get to action without ignoring the obvious risks.

Use the table below as a decision shortcut when you do not want to re-argue the whole issue every time an invoice goes bad.

| Scenario signal | First move | Verification checkpoint | Main failure mode | Switch trigger |

|---|---|---|---|---|

| Smaller balance, limited billable time | Start with a debt collection agency | Written fee terms, reporting cadence, and escalation steps are explicit | Unclear escalation creates drift and weak follow-through | Move to small claims only after outreach and payment-plan attempts fail |

| Larger balance, strong records, defendant details are clear | Prepare a small-claims filing path | Contract, invoice trail, and acceptance evidence are organized before filing | Filing before the file is court-ready | If service or documentation breaks, pause and fix the record first |

| Cross-border counterparty and weak jurisdiction or dispute terms | Prioritize negotiated settlement, then agency pressure | Settlement terms, payment dates, and default consequences are in writing | Spending early on forum fights instead of payment resolution | File only after forum risk is mapped and enforcement is still practical |

| Debtor is responsive but keeps stalling | Send a final demand letter with a short deadline, then choose one path | Delivery proof, exact amount due, and deadline timestamp are documented | Repeated extensions weaken enforcement signal | If no payment or signed plan by deadline, escalate once and move |

Those rules work because they force the decision back to the real variables. Smaller balances are often more sensitive to your time cost, so outsourcing some of the pursuit may make sense. Larger balances with clean proof can justify the effort of filing, but only if the file is truly ready. Cross-border disputes punish casual assumptions about venue, so settlement pressure is often the smarter first step. And when a debtor is responsive but consistently stalls, your problem is usually not lack of communication. It is lack of consequence.

One discipline matters across all four scenarios: set one final deadline, then take one escalation path without repeating soft resets. Repeated extensions are a common failure mode because they dilute urgency, consume owner attention, and make later enforcement look less credible than it should. If you say the next missed date triggers escalation, treat that as a real trigger.

This is where many freelancers talk themselves into avoidable delay. A client sounds sincere. They ask for one more week. They make a partial promise without signing anything. Then another week passes, and the file is now older, messier, and harder to move. The problem is not kindness. The problem is giving time away without buying certainty in return.

If you start with agency pressure, keep the language disciplined. Before any legal-threat wording in agency-first cases, add a compliance check on debt age. Debt Collection Rule guidance discusses a prohibition on legal action, or threats of legal action, to collect time-barred debt. Do not let tone outrun what the file and the law actually support.

A good five-minute decision is not casual. It is just compressed. You are checking for amount, evidence quality, venue clarity, debtor behavior, and your own capacity to follow through. Once those are clear, the first move is usually obvious. The bigger risk is not choosing imperfectly. It is staying in comparison mode so long that the claim gets harder to collect.

Execution checklist before and after you choose#

Once you choose a path, execution matters more than rhetoric. Start only after you have two things in writing: your evidence pack and your stop-loss limit for added time and spend.

Those two guardrails do more than keep you organized. They protect you from the most common operational failure, which is pouring disproportionate effort into a claim because frustration has replaced judgment.

| Checkpoint | Debt collection agency path | Small claims court path |

|---|---|---|

| Before you start | Confirm counterparty identity, amount due, signed contract, unpaid invoice trail, delivery proof, reminder history, and final demand letter proof | Use the same evidence pack, confirm where your court provides forms, and confirm the filing and service process in that court |

| Cost controls | Confirm contingency terms, escalation steps, and reporting cadence before outreach starts | Confirm filing and service process, hearing document format, and likely total effort before filing |

| Compliance and risk | Verify the agency can operate in your jurisdiction and avoid unsupported legal-threat language | Track deadlines from the court notice date and plan for possible post-judgment collection work |

| After action starts | Log every contact, offer, and response to support settlement decisions | Keep the same log for hearing credibility and post-judgment follow-through |

Keep your file in one clear sequence: contract, scope or change approvals, invoice terms and dates, delivery or acceptance proof, reminders, and demand-letter proof. That order makes settlement review easier, gives you a cleaner story at hearing, and keeps later follow-through from turning into a scavenger hunt. It also shows that you tried to resolve the matter before filing, which matters both practically and reputationally.

For agency use, the operational risk is usually not that the agency does nothing. It is that you sign vague terms, hand over an incomplete file, and then allow the account to drift without a clear escalation trigger. That is why written fee terms, reporting cadence, and next-step rules matter before outreach begins, not once you are already frustrated.

For court, the trap is different. Many freelancers prepare for the hearing and forget to prepare for everything around it. Service, filing accuracy, deadlines, document formatting, and post-ruling follow-through all matter. A hearing date feels like the center of gravity, but the result often turns on the quieter procedural steps around it.

If you choose court, include post-trial execution in your plan. In California, the Notice of Entry of Judgment (SC-130) includes a date that drives appeal and collection deadlines, and a plaintiff cannot appeal the decision on the plaintiff's own claim. That is a useful reminder that the hearing is not the whole job. Dates and form mechanics continue to matter after the ruling.

If payment is made after judgment, close it correctly. California uses the Acknowledgment of Satisfaction of Judgment (SC-290), and local guidance says that after a written request to file it, the defendant has 14 days to comply. Again, the broader lesson is procedural discipline. Closing steps are part of collection too, so verify local court rules before acting.

The contact log is worth more than it looks. In an agency path, it helps you decide whether a payment proposal is serious or just another delay tactic. In a court path, it supports your timeline, your credibility, and any later follow-through if payment does not arrive promptly. Keep one log, one chronology, and one evidence pack so you are not rebuilding the story every time the dispute changes shape.

Use one stop-loss checkpoint as a final control: set a maximum additional spend or time cap, then reassess at that threshold. If your log shows repeated promises without payment movement, switch path once and document why. That keeps the decision disciplined instead of emotional.

If you want to reduce how often disputes get to this point, strengthen the paperwork on the front end. Try the SOW generator.

Conclusion#

The right move is the one with the best expected take-home and the cleanest execution, not the one that looks toughest on paper. A strong headline can still be a weak business decision if you do not have the time, venue fit, or follow-through to finish the job.

If you read this decision through one lens, use this one: compare both paths on the same standards. What will it cost directly? What will it cost in owner time? How collectible is the debt in reality, not in theory? And what happens after the first apparent win, whether that is a settlement agreement or a judgment?

Treat timing as a real risk variable, not a convenience issue. In many debt-collection contexts, collectability falls as debt ages, so avoid drift, set a decision date, and escalate once your file can support the next step. Delay is not neutral. It often makes both options worse.

Keep process realism front and center. Litigation can be necessary, but it is not automatic payment. Agency terms vary by provider and case, and court spend varies by venue and procedure. The decision improves when you stop asking which path sounds stronger and start asking which one you can execute cleanly with the records you actually have.

Use this closeout sequence before escalation:

- Recheck contract terms, jurisdiction, and dispute path for conflicts.

- Finalize one evidence pack: contract, unpaid invoice trail, delivery proof, reminders, and final demand letter proof.

- Set a stop-loss cap for additional spend and time.

- If using a debt collection agency, confirm coverage for your filing area, escalation cadence, and reporting terms in writing.

- If using small claims court, confirm local form process, hearing requirements, and realistic post-judgment collection steps.

- If bankruptcy protection is involved, consult legal counsel before further collection activity.

- Escalate once, then stay on that route unless a defined trigger is met.

Final rule: if venue terms are clear and your file is complete, act now. If venue terms are weak, tighten documentation and run one structured settlement attempt, then escalate on deadline.

Frequently Asked Questions

Is small claims court always cheaper than a debt collection agency?

No. Costs can vary by jurisdiction, case details, and your agreement terms. Agency pricing can be contingency-based, while court-related expenses can also add up.

Can I still fail to collect after winning a legal judgment?

Yes. Even after judgment, separate enforcement steps may still be needed before money is recovered. Plan for post-judgment enforcement from the start.

When should a freelancer use a debt collection agency first?

Agency-first can make sense if you want collection pressure before filing in court and accept that fee structures vary by agency. Before signing, confirm scope, escalation steps, and whether terms affect later court options.

What changes if the client is in another state or a cross-border dispute?

Procedure risk rises because local court rules vary and can change. Do not assume one venue's process maps cleanly to another. In these cases, it can be worth trying settlement pressure before larger court spend.

Do I need a final demand letter before filing a small claims lawsuit?

Requirements can differ by jurisdiction, so check local rules before filing. A clear final demand with a short deadline and delivery proof can still strengthen your position. If helpful, use How to Write a Final Demand Letter Before Legal Action.

What contract terms matter most before I pick a path?

Focus first on the terms that control dispute process and payment obligations, then confirm any limits that could affect recovery.

Can I switch from agency efforts to court later if payment arrangement attempts fail?

It can be possible, depending on your agency agreement and whether collection rights were assigned. Keep one log of contacts, offers, responses, and missed deadlines, and confirm who has standing to sue.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- courts.michigan.gov/4ac33d/siteassets/reports/special-initiative...trusted

- files.consumerfinance.gov/f/documents/cfpb_debt-collection_small-entit...trusted

- nycourts.gov/courthelp/pdfs/smallclaimshandbook.pdftrusted

- sanbenito.courts.ca.gov/system/files/general/dca-small-claims-court-...trusted

- sanmateo.courts.ca.gov/self-help/small-claims-self-help/what-happen...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Freelancers Collect Overdue Invoices When Clients Stop Paying

If "client won't pay freelancer" describes your situation, do not treat it as a personality conflict. Treat it as a collections process with dated records, clear decision gates, and one next action at a time.

Small Claims Court for Freelancers With Unpaid Invoices

Small claims court can be a practical path for unpaid invoices, but only if you treat it like a process that rewards clean records and punishes shortcuts. It is usually less formal than full litigation, and [freelancers can often represent themselves](https://blog.freelancersunion.org/2014/04/01/what-all-freelancers-should-know-about-small-claims-court), but that easier access does not reduce the need for evidence, correct party details, and the right filing path.

How to Write a Final Demand Letter Before Legal Action

Send a final demand letter when informal resolution has already failed and you still want a documented, settlement-first path before legal action. It is not a threat. It is a clear, factual request that matches your records and the next step you are actually prepared to take.