Quick Answer

Choose the best travel insurance for digital nomads by locking your order of decisions: visa paperwork fit first, country-to-country continuity second, cost third. In this shortlist, SafetyWing is noted for buy-before-or-during-travel timing and 180+ country positioning, while World Nomads is framed for US-resident trip coverage. Genki is presented as a two-track choice (Traveler vs Native). Final selection should come from policy documents and certificate wording, not roundup rank position.

The Best Travel Insurance for Digital Nomads in 2026#

The best travel insurance for digital nomads in 2026 is not the plan that tops a roundup. It is the one that clears your paperwork and still works when your route changes. For long stays, keep the order simple: paperwork first, continuity second, price third. Eligibility is part of that first check, because a cheap plan you cannot actually use is not a bargain.

Most online advice answers only part of the problem. Community threads are good for finding names fast. Provider pages show how a company positions the product. Editorial rankings help you compare slices of the market. None of those sources, on its own, tells you whether your insurance proof will hold up in a visa file or whether the plan still fits once a short trip turns into a move. Rankings help you discover options. They do not submit your packet for you.

- Set the decision order before you compare brands. For long stays, hold the sequence steady: paperwork first, continuity second, cost third. If the documentation is weak, a lower monthly price is usually false savings.

- Check movement fit using the details that are actually stated. One nomad-focused provider says it covers 180+ countries, treats US coverage as an extra, and allows purchase before departure or while you are already abroad. That matters when dates slip or the route changes after you have already left.

- Look for extension and underwriting signals early. Another option is described as allowing mid-trip extensions, and it is reported as being underwritten by Nationwide Insurance. That combination can matter when a planned trip quietly becomes a longer stay.

That is why this guide keeps returning to documents and continuity. If approval depends on proof, the homepage is not the product. The certificate is.

| Option | What is clearly visible | Why people shortlist it | What to verify before you buy |

|---|---|---|---|

| SafetyWing | 180+ country positioning, buy before or during travel, sample price shown as USD 62.72 per 4 weeks for ages 18-39 | Flexible timing for people already abroad | Exact exclusions, US add-on impact, and whether certificate wording matches your visa portal requirements |

| World Nomads | Mid-trip extension is reported; underwriting by Nationwide Insurance is reported | Useful for trips that may lengthen | Renewal terms, destination limits, and document format for visa submission |

| Other shortlist names, including Genki, Faye, and Insured Nomads | Often appear in nomad discussions and list pages | Useful for keeping the longlist honest | Plan-level terms, claims steps, and visa-document output quality, requested in writing |

Keep one red flag in view: some rankings are advertiser-backed. One major guide says it receives compensation from listed companies. It also cites a large method set, 25 companies reviewed, 2,250 quotes, and 1,000 surveyed policyholders across 36 rating factors. That is useful context, but it is still only input. A serious methodology can still miss your exact visa process or move pattern.

Once you have a workable shortlist, the job shifts from discovery to fit. If your visa file is next, pair this list with your application document checklist in How to Apply for a Digital Nomad Visa: A Step-by-Step Walkthrough.

How to Choose the Right Policy for Your Move#

Most bad picks happen before anyone reads the policy wording. People compare monthly prices, or chase the brand they have seen most often, before checking whether the plan can even be issued from their country of residence or whether the certificate wording will support the move. The right policy is the one that passes your visa document check and still holds together if dates or countries change.

In practice, the cleanest decision usually comes from removing unworkable options early, not from obsessing over small differences at the end. That means getting the order right before you compare quotes.

- Confirm residency eligibility first. Some providers cover residents of many countries, but you still need to confirm your own country-of-residence rules and start conditions. Some plans look global until you get to those start rules. If you miss this step, everything that follows, price, benefits, even brand reputation, is just noise.

- Match the policy to your trip pattern. Short travel loops and long-stay relocation are not the same use case. If your timeline is flexible, check whether you can buy after departure and whether mid-trip extension is available. Flexibility only helps if the policy still works once dates slip and the move no longer looks like a short trip.

- Pick coverage scope on purpose. Decide between medical-only coverage and broader travel insurance based on what you actually need covered. The label matters because travel insurance and longer-term medical coverage solve related but different problems. If cancellation flexibility matters, verify whether Cancel For Any Reason is optional and separately priced, and check the plan limits. For example, World Nomads states fear of travel is not a valid cancellation reason.

- Use paperwork as the tie-breaker. If approval depends on insurance proof, request sample documents before purchase and confirm the insured name format, dates, and continuity wording. A small price gap is rarely worth much if the certificate does not match what the visa process is asking for. A single emergency bill can be expensive, so weak documents and weak coverage are a costly combination. Paperwork often settles the decision faster than another hour of reading reviews.

Also keep the layer question straight. Travel insurance is not always a full replacement for domestic health insurance. If you need broader local healthcare access and long-term stability, treat travel coverage as one layer, then confirm country requirements before you buy using The 2025 Global Digital Nomad Visa Index: 50+ Countries Compared. That is the setup for the next table.

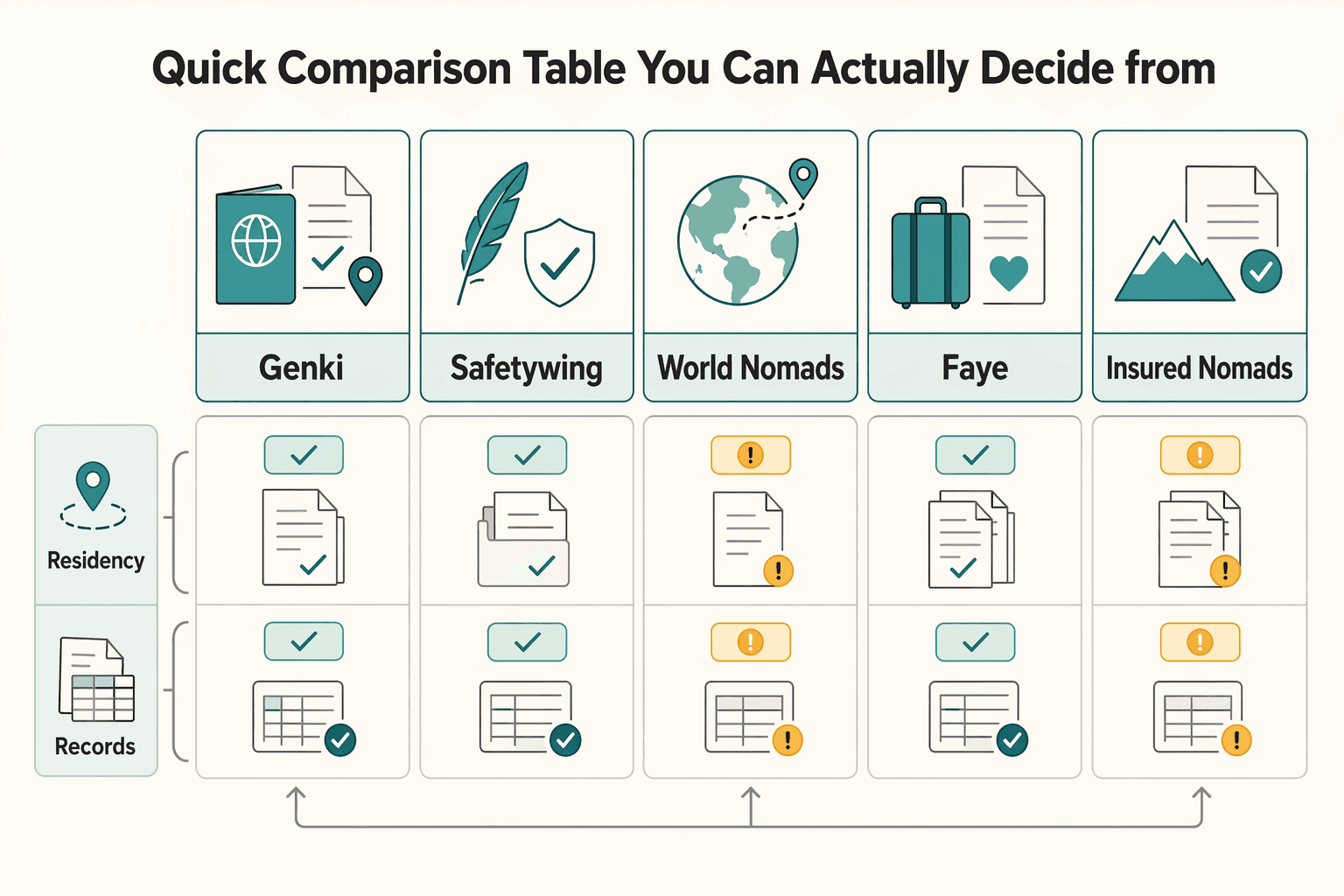

Quick Comparison Table You Can Actually Decide From#

Compare evidence quality before you compare slogans. When your visa paperwork is time-sensitive, an unknown cell is not neutral. It is a real risk.

Use this table as a discipline tool. It keeps you from rewarding the loudest marketing while ignoring the provider that simply gives you cleaner facts. The point is not to crown a winner. It is to show where the record is solid and where you still need written confirmation.

| Provider | Best-for profile | Visible strengths | Visible caveats | Unknowns from available evidence | Visa-proof readiness | Claims process clarity | Source context label |

|---|---|---|---|---|---|---|---|

| Genki | People first choosing between travel health and international health tracks | Own guide clearly maps Traveler and Native | Plan-level features are not established in the available excerpts | Residency eligibility, extension terms, cancellation rules, document format | Not verifiable from current excerpts | Not verifiable from current excerpts | Provider guide plus review excerpts |

| SafetyWing | People who may need to buy before departure or while already abroad | 180+ country positioning, signup before or during travel, sample price visible | US coverage is an extra; favorable summaries can be affiliate-backed | Coverage triggers, renewal mechanics, exclusions, certificate wording | Not verifiable from current excerpts | Partial signal only; provider support claims are visible, but at least one personal review reports friction | Provider page, listicle, or community anecdote |

| World Nomads | Travelers prioritizing broad residency access and mid-trip flexibility | Reported coverage for residents of many countries; reported mid-trip extension; reported no pandemic exclusion | Fear of travel is reported as not a valid cancellation reason | Exact document format by visa portal and country-level acceptance | Partial signal only; confirm documents directly before purchase | Partial signal only; process steps are not fully detailed here | Editorial summary |

| Faye | People widening the shortlist beyond the usual names | Strong homepage rating is visible | Plan-level features are not established in this review set | Eligibility, extension rules, exclusions, claims path | Not verifiable from current excerpts | Partial signal only; one reviewer describes straightforward but cumbersome claims | Listicle or review excerpt |

| Insured Nomads | Longlist only until better documents are available | Useful to keep in wider consideration | Current excerpts do not provide enough transparent plan detail | Policy terms, limits, renewal conditions, document output | Not verifiable from current excerpts | Not verifiable from current excerpts | Listicle or sponsored-placement context |

Use two quick checks as you score. If a page says compensation can affect product order, treat rank position as a lead, not a verdict. Also check freshness. One major editorial page flags potential staleness in part of its card information, which is reason enough to put dates and plan details back on your confirmation list. Card summaries are exactly where small terms tend to drift first.

If two options remain close, pick the one that can produce clear visa-ready proof faster. Reviews can surface patterns and failure modes, but they should not outrank documentation readiness, extension terms, and cancellation limits. With that frame in place, the provider sections below are mostly about where the evidence is strong and where it is still thin.

Genki#

Genki is easiest to evaluate when you first need to separate trip-style coverage from longer-term international health coverage.

Its own guide says it offers two options made for digital nomads, expats, and traveling families: Genki Traveler as travel health insurance and Genki Native as international health insurance. The page is set up as a side-by-side chooser and is dated Jun 1, 2025. Use it as a product map, not as a substitute for checking the current policy wording.

That split is genuinely useful early in the process. It forces the first question most buyers skip: are you buying travel health for movement, or international health for longer-term medical support abroad? Based on the material here, Genki gives you clearer product structure than some alternatives. But it does not give you, in this review set, enough plan-level detail to stop there.

A practical screen looks like this:

- Start with track fit. Decide whether your move fits Traveler or Native before you compare anything else. If you skip that first split, you can spend a lot of time comparing the wrong class of product.

- Treat review recency carefully. Third-party reviews are context, not contract language. A review title with 2026 tells you the article is recent; it does not prove the terms.

- Read social proof with the right filter. Trustpilot shows a 4.0 TrustScore in this excerpt, but Trustpilot also says reviewer opinions are their own and claims are not fact-checked by default.

- Strip affiliate bias out of comparisons. At least one comparison page is explicitly affiliate-monetized, so use those lists to build questions and then answer them in provider documents.

Genki can stay on the sheet without becoming the default. That is a sensible place for it based on the material here. If it remains on your final shortlist, the next move is simple: pull the certificate and full policy wording and match them against your visa needs and relocation pattern, not against review-site confidence.

SafetyWing#

SafetyWing deserves a serious look if your timing is fluid. The ability to buy before departure or while already abroad, plus broad country positioning, speaks directly to the way many nomad moves actually happen. It is one of the few options available where the timing and movement mechanics are visible on the page. Even so, keep it in a verify-first category until you have the policy wording and visa documents in hand.

SafetyWing positions Nomad Insurance for nomads and remote workers abroad. It says you can sign up before departure or while already traveling, and it states coverage across 180+ countries, with US coverage handled as an extra. Those are meaningful signals if dates slip or the route changes after you have left, but they are still starting signals, not final proof for your exact case.

Use four checks here, in this order:

- Mobility fit comes first. Treat the 180+ countries scope and the US carveout as a fast route check, not full itinerary proof. For nomads, that matters more than a glossy benefit summary. It is useful if you expect country changes, but you still need the written terms that explain how those changes are handled.

- Use price as a planning anchor, not a promise. The page shows 62.72 per 4 weeks for ages 18-39 and says signup can happen while abroad. That is helpful for rough planning and for late-moving timelines. Late signup is a real differentiator only if the rest of the terms still fit.

- Balance provider promises against user friction. SafetyWing advertises a simple claims path, 24/7 human support, and fast live chat response. Claims experience is where glossy positioning meets reality. At the same time, at least one personal review reports denied claims and difficult support. In practice, that means you should treat support messaging as a claim to test, not as settled fact.

- Be stricter on visa readiness than on marketing. Some favorable coverage is affiliate-backed, including one article written in collaboration with SafetyWing. If a visa deadline depends on insurance proof, request document samples in writing and confirm names, dates, and continuity wording before payment. This is a common place for avoidable resubmissions.

If the choice comes down to this plan and Genki, use one plain tie-breaker: pick the one that gives you clearer written terms for country changes, even if it is not the cheapest monthly quote. Do not let the monthly anchor decide by itself. If your move still looks more like travel than relocation, World Nomads is the next useful contrast. For budget planning alongside insurance decisions, How to Manage Your Finances While Traveling Long-Term can help.

World Nomads#

World Nomads makes the most sense when your move still looks a lot like travel, especially for US-resident travelers. It is less reassuring if you need long-stay continuity or visa-ready proof and cannot confirm those details in the certificate.

Three details matter most:

- The public wording is travel-first. The digital nomad page says US residents can get coverage for medical emergencies and unexpected incidents while on a trip. It also asks for your country of residence to show relevant information. That is a clear audience signal. It is not the same as proving long-stay continuity or document fit for a relocation file. Trip language can be perfectly fine for emergencies and still be vague for relocation paperwork.

- The trust signal is useful, but limited. The USA page presents four plans and shows a Trustpilot score of 4.3 out of 5 based on 5,000+ reviews. That helps with quick screening. Ratings tell you people used the product; they do not tell you what their document packet looked like, how claims will go in your case, or whether a visa process will accept the paperwork without extra back and forth.

- Third-party experience is mixed enough to force a document check. Independent reviews conflict: one writer says they stopped recommending World Nomads in 2022, while another reports reimbursement of more than $600 but flags missing Trip Protection clauses and a 180-day term limit in their case. Conflicting reviews do not prove the plan is wrong. They do remove any reason to rely on momentum from older recommendations. Read the current policy wording yourself, especially on duration and benefit details for longer stays.

Before you sign, put the exact policy certificate next to your visa insurance requirements and keep it side by side with Genki, SafetyWing, and Faye until one option is clearly cleaner on documentation. That same side-by-side discipline becomes even more important once the evidence gets thinner, which is where the next two names land.

Faye and Insured Nomads#

Faye and Insured Nomads should stay on your table as evaluate further, not final picks, until you have plan documents in hand. The deciding issue here is not brand familiarity. It is evidence depth.

Faye has enough visible signal to justify a closer look. Its homepage shows 4.8/5 stars, and one long-form reviewer says they relied on World Nomads for eight years before switching. That helps with discovery. Ratings tell you there was enough customer experience to produce sentiment. They do not tell you whether the terms are clean for your use case. On the material here, Faye still does not outrank a better-documented alternative when you are planning a relocation.

There is also a practical warning attached to Faye. That same reviewer describes claims as straightforward but cumbersome, with heavy documentation and long reimbursement waits. Treat that as a pre-purchase checkpoint: ask exactly which claim documents are required and how reimbursement is handled during long stays abroad. If the answer is vague, do not fill the gap with optimism.

Insured Nomads is harder to rank from the material on hand. The current excerpts do not provide enough transparent plan-level detail to compare it with the leading alternatives. One DigitalNomads.world excerpt is mostly cookie-consent text, and another prominent list context includes sponsored or partner-placement framing. At that point, ranking it confidently would mean inventing certainty the material does not support.

Hard rule for both names: if most of the support is ratings, affiliate content, or sponsored placement, stop ranking and request the same document packet from every finalist. On a Digital Nomad Visa path, paperwork usability matters more than brand preference or a small price difference. That is why the document step deserves its own checklist.

The Documentation Checklist Most Lists Skip#

This is the part most roundups skip, and it is often where the best-looking option either becomes usable or falls apart. The safer choice is usually the policy with clearer documents and a clean claims entry path, not the one with better marketing. This is where a decent shortlist turns into a decision you can actually use.

| Stage | What to do | Why it matters |

|---|---|---|

| Pre-application | Classify travel insurance and nomad insurance before comparing | Separating them keeps you from comparing unlike policies |

| Pre-application | Request policy confirmation, certificate wording, full policy terms, and claim-start steps | If you only get summary copy, keep the option in "needs verification" |

| Before departure | Read the fine print and the claim-start steps side by side | If either part is vague, treat that as a practical risk |

| After arrival | Re-check renewal timing and coverage continuity if your country changes | What worked for the first country on your route may not be enough for the next |

| When using reviews | Time-stamp what you read and note possible commissions | Reviews can surface useful questions, but final decisions should still come from current policy wording |

Use a simple sequence:

- Pre-application: classify each option before you compare it. Common failure mode: treating travel insurance and nomad insurance as if they are interchangeable labels. In your notes, separate them so you are not comparing unlike policies. If you mix them together, the comparison gets blurry fast. One is typically framed around cancellations and unexpected medical costs abroad, while the other is framed as broader coverage that can include health, travel, and equipment.

- Pre-application: build one document packet per finalist. Ask for downloadable policy confirmation, certificate wording, full policy terms, and claim-start steps. If you only get summary copy, keep that option in a "needs verification" category until full documents are available. The point is to make every finalist answer the same document request, not to let each provider define the comparison on its own terms.

- Before departure: verify claims mechanics, not just coverage promises. Read the fine print and the claim-start steps side by side. If either part is vague, treat that as a practical risk instead of assuming the missing detail will work in your favor. The goal is not to imagine best-case service. It is to know the first move when something goes wrong.

- After arrival: re-check continuity details if your country changes. Do not assume renewal timing or coverage continuity stays the same across moves. What worked for the first country on your route may not be enough for the next. Confirm the current terms in your own policy documents.

- When using reviews: treat them as context, not proof. Time-stamp what you read and note disclosures like possible commissions. Date matters because terms, pricing, and product pages move. Personal experience can surface useful questions and common failure modes, but final decisions should still come from current policy wording.

If two options still look similar after that, choose the one with clearer document output and the simpler first step for opening a claim. Once you have that packet, the remaining questions are usually about scope and continuity, which the FAQ tackles directly.

Pick Insurance Like a Relocator, Not a Browser#

If you treat this like ordinary online shopping, you will overvalue brand and undervalue paperwork. Insurance for a real move is closer to relocation planning than to browsing a top-10 list. A browser shops for the lowest visible price. A relocator shops for something they can prove, renew, and actually use. Use the same sequence from the start of this guide, just expanded: eligibility first, document fit second, how the plan works after departure third, brand preference last.

- Eligibility first. Start with policy type and travel-pattern fit. Long-term travelers may not qualify for standard travel insurance, and some home-country health plans can lapse after extended time abroad. If your plan looks more like relocation than a short trip, start with expat-style or broader nomad coverage, then narrow providers. This alone strips out a lot of noise.

- Document fit second. Once eligibility looks plausible, check whether the insurer can produce clear policy documents on your timeline. Run the same document check across top options instead of relying on rankings or summary pages. Document fit is often the real bottleneck. This is where a popular plan often drops out.

- How it works after departure third. Then test the practical details. One provider says you can sign up before departure or while abroad, states coverage across 180+ countries with US coverage as an extra, and describes reimbursement within a few days in its claims flow. Useful, yes, but only after you confirm the wording that makes those details relevant to your route. Treat them as specifics to confirm, not as guarantees.

- Brand preference last. Use ratings and list placement for discovery, not final selection. Third-party summaries can conflict on country scope, ratings snapshots, and price anchors like 62.72 per 4 weeks for ages 18 to 39. That is normal. Those summaries are not written for your exact move.

If two options still look close, use one final checkpoint: choose the one with clearer eligibility language, cleaner paperwork output, and fewer unknowns in claims handling. Popular plans are easy to find. Usable ones are the plans you can document and keep.

Frequently Asked Questions

What is the best travel insurance for digital nomads?

There is no single winner for everyone. Some nomad-focused guidance explicitly says insurance is not one size fits all and depends on both origin and destination countries. A practical pick is the one that fits trip length, medical risk, and eligibility needs.

Is travel insurance enough for long-term nomads?

Often not on its own. Travel insurance is usually built for unforeseen travel events, including emergency medical issues during a trip, while international health insurance is aimed at longer-term medical support abroad. One common approach is combining both layers.

What documents do I need for Digital Nomad Visa insurance proof?

There is no universal packet for every country. Start with official visa requirements, then request insurer documents that match those requirements and your residency status.

Can I keep coverage while moving between countries?

It depends on the policy. Country changes can affect eligibility and how coverage applies, and guidance in this area warns against broad assumptions across origin and destination pairs. Verify continuity terms in writing before each move.

What should I verify before buying a nomad insurance plan?

Confirm policy type first: travel insurance versus broader nomad coverage that may include health, travel, and equipment. Next, check claim initiation steps and required documents. Also remember home medical coverage may not carry over abroad.

How should I compare Genki, SafetyWing, and World Nomads when details are incomplete?

Use confidence-based comparison, not popularity. If one provider gives clearer eligibility and trip-use language, such as coverage for US residents during trips with medical emergencies and unexpected incidents, score that as stronger evidence than vague claims. For missing details, keep options in a verify-before-ranking state and request the same policy and claims documents from each provider.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 5 external sources outside the trusted-domain allowlist.

- digitalnomads.world/tips/faye-travel-insurance-reviewexternal

- helenabradbury.com/blog-1/best-travel-insurance-for-digital-nomadsexternal

- novo-monde.com/en/comparison-travel-insurance-for-digital-n...external

- theroamingrenegades.com/best-travel-insurance-for-digital-nomadsexternal

- worldnomads.com/usa/travel-insurance/whats-covered/digital-n...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Apply for a Digital Nomad Visa: A Step-by-Step Walkthrough

Use a country-specific sequence, not a generic checklist. If you want fewer surprises, use this order. Core requirements often overlap, but each country can add its own rules, and some filing locations add extra instructions. Stale guidance is a common source of delay.

The 2026 Global Digital Nomad Visa Index for 50+ Countries

Start with legal fit, not lifestyle filters. The practical order is simple: choose a route you can actually document, then decide where you want to live. That single change cuts a lot of wasted comparison work and stops you from falling in love with places that were never a real filing option.

Manage Finances While Traveling Long-Term Without Cashflow Gaps

If you are funding travel from live client payments, the real job is continuity, not chasing the lowest visible cost. You need spending access and incoming cashflow that can keep working through separate failures in separate systems.