Quick Answer

Start by automating invoice sends, reminders, and status updates, then keep manual approval for term changes, disputed items, and high-risk exceptions. A practical setup uses one invoice hub, a small set of payment rails like ACH or PayPal, and a weekly checkpoint that traces one invoice from send date to reconciled record. This lets you automate freelance finances without treating uncertain payment statuses as spendable cash.

Automate freelance finances without losing control of cashflow#

You can automate freelance finances and still keep control over key cash decisions. The practical target is simple: automate repetitive admin, then keep human approval for higher-risk exceptions.

This is built for freelancers, creators, and small teams that depend on client invoices. The point is not just cleaner bookkeeping. It is about reducing reactive money decisions through repeatable workflows and clear visibility into available cash. Think about it this way: automation should speed up admin, not replace judgment. Sending invoices, nudging reminders, and moving status updates are admin tasks. Setting terms, approving exceptions, and deciding whether money is safe to spend are control tasks. Use this three-part setup:

- Invoicing automation with hard term controls

Set recurring invoices, reminders, and status updates to run automatically because manual tracking gets error-prone and draining as workload grows. Keep term choices manual before each client starts: due date, accepted payment methods, and any upfront requirement. Key differentiator: automation handles timing, while you approve terms that define risk.

In practice, your signed agreement and invoice template should match before the first invoice goes out. If a client wants a different due date or a different rail, change the underlying record first, then let reminders run from that record. Do not let scattered messages become the real source of payment terms.

- Exception alerts tied to expense tracking

Automate status alerts so payment issues surface quickly, then map confirmed payments into records for expense tracking and planning. Key differentiator: alerts support faster response and earlier planning, but only confirmed funds enter your spend plan.

Keep status labels clear enough that you can tell whether an alert means activity happened or cash is actually available. An invoice being sent is not the same as a payment being confirmed, and a payment event is not the same as money you should allocate. When in doubt, slow the spending decision, not the recordkeeping trail.

- Weekly control checks with escalation rules

Run one weekly review of open invoices, overdue balances, and unresolved payment issues. If a payment stalls, escalate in a fixed order: reminder, direct follow-up, then service pause when terms allow. Key differentiator: each stalled invoice follows the same path instead of ad hoc reactions.

The review should move in the same order each time: open invoices, overdue items, payment exceptions, then bank-confirmed cash. That sequence matters because it keeps you from building a spending plan on top of records that still need verification.

Use this checkpoint each week: trace one invoice from send date to settlement to booked record. If that trail breaks, narrow the automations before adding new ones. A common failure mode is treating early payment statuses as usable cash. Keep a short incident file for each exception with invoice copy, payment-attempt history, and client messages.

If the trail breaks at a specific handoff, fix that handoff first. Do not stack another tool on top of a missing status or a broken field mapping. A lean setup with one clear exception queue is usually better than a clever setup that needs manual detective work every week.

Who this list is for and the criteria used to rank options#

This list is for freelancers, creators, and small teams that invoice repeatedly, use a business bank account, and collect through ACH, PayPal, Venmo, or Apple Pay. If you need enterprise ERP behavior or deep custom engineering on day one, skip this list and move straight to an API-led build.

If that description fits, choose the stack you can explain, verify, and repair without a long rebuild. Use this ranking order:

- Payment collection fit for your client base

Start with the rails your clients already use, then keep only the smallest set that still gets invoices paid on time. Higher rank goes to setups that reduce payment friction without treating every rail as the same risk.

If most clients already pay the same way, simplicity should rank higher than feature breadth. A rail that looks flexible but adds confusion, slower follow-up, or extra exception handling is not a better fit just because it offers more options.

- Fee transparency by market, not assumptions

For PayPal, use the right market context: domestic and international are defined by whether sender and receiver are in the same or different markets, and consumer and merchant fee pages are separate. Higher rank requires checking the right market page and reviewing policy updates before you enable or change a rail.

The ranking favors setups where this check happens before rollout, not after invoices are already live. Your internal note should be specific enough that you or a bookkeeper can see which page you used, which market it applied to, and why the rail was approved.

- Exception handling for disputes and payment holds

Collection reliability includes what happens when payments are disputed, charged back, or held, not just what succeeds. Higher rank goes to stacks where exception states are explicit before funds are treated as spendable.

If a tool makes dispute or hold states hard to see, it should rank lower even if routine payments look smooth. Reliable collection is not just the happy path. It is whether you can see trouble early and respond without guessing.

- Reconciliation quality and maintenance effort in QuickBooks or QuickBooks Solopreneur

The invoice-to-payment-to-reconciled path should be easy to trace without constant fixes. If you cannot explain that path in under two minutes, the stack is too complex for your current stage.

The more often you have to rename, reclassify, or hunt for missing fields, the lower the setup should score. Easy traceability beats extra automation if the extra automation creates cleanup every week.

Red flag: carrying a fee assumption from one market into another. Keep a short decision note for each rail with market, fee page used, and last verification date. That note saves time when you revisit a rail, compare options, or hand the work to a bookkeeper. Related: The Best Business Bank Accounts for Freelancers.

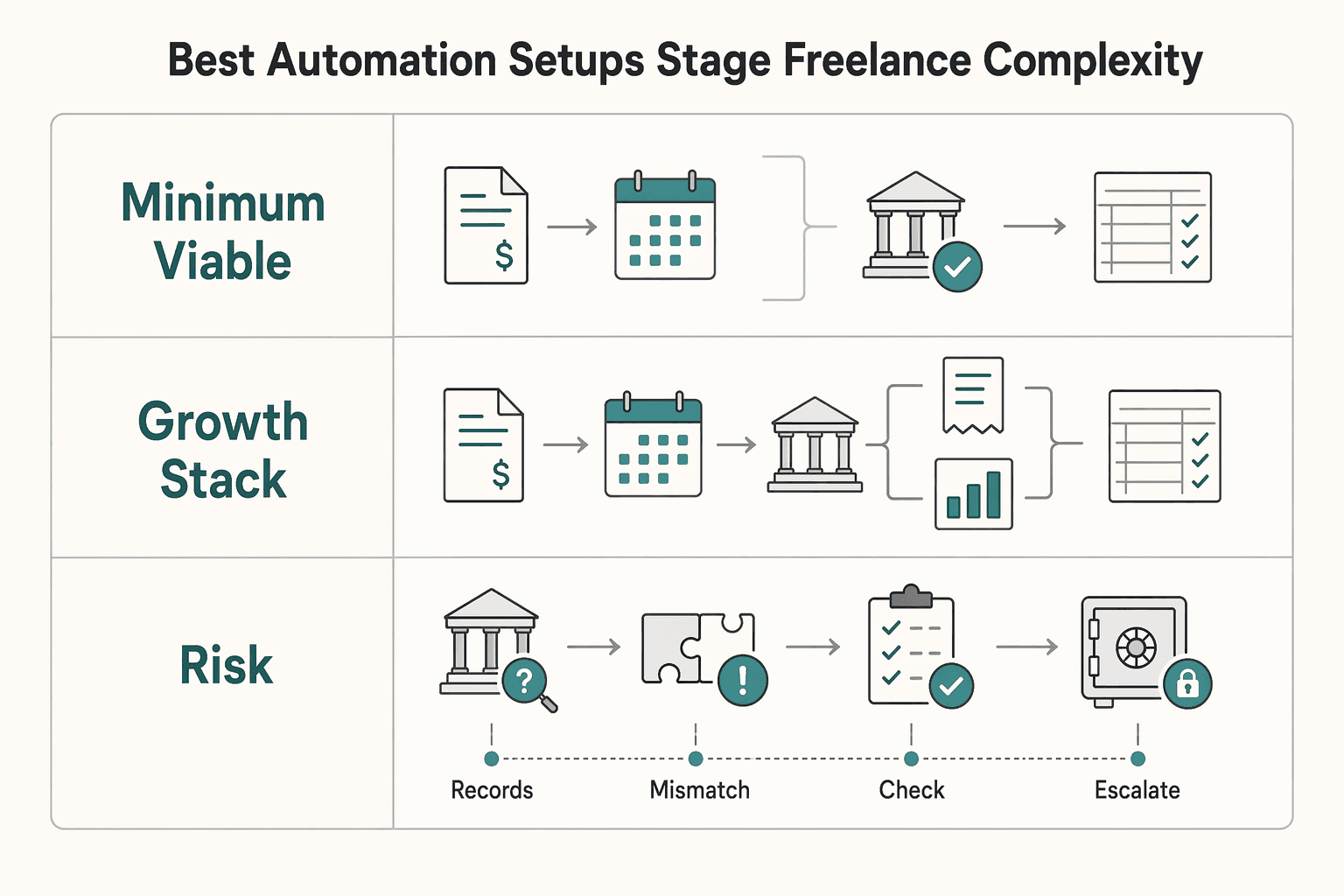

The best automation setups by stage of freelance complexity#

Use the lightest setup that still protects cash decisions, then add controls only when reconciliation or risk events show a real gap. Most freelancers do not need the most advanced stack first. They need the cleanest setup they can operate consistently.

| Stage | Best for | Core setup | Key differentiator |

|---|---|---|---|

| Minimum viable stack | Solo freelancers with a simple client mix and recurring ACH retainers | QuickBooks as the record base; automate invoice sends and reminders; review cleared deposits against the business bank account | Fast launch with low setup drag while keeping the invoice-to-reconciled path easy to explain |

| Growth stack | Clients who need more than one payment method, such as PayPal plus Apple Pay, while reporting still lands in QuickBooks | Improve invoicing automation and follow-up timing; keep a market note per rail | More collection flexibility without losing visibility |

| Risk-sensitive stack | High-ticket or cross-border work where holds and disputes can disrupt cashflow | Capture status changes automatically; require manual approval before treating funds as available for payout or spending | Explicit exception control over speed |

- Minimum viable stack

Best for solo freelancers with a simple client mix and recurring ACH retainers. Keep QuickBooks as your record base, automate invoice sends and reminders, and review cleared deposits against your business bank account. Key differentiator: fast launch with low setup drag while keeping the invoice-to-reconciled path easy to explain.

This works best when most invoices follow the same pattern. You send from one place, use the same core rail mix, and treat the bank match as the reality check. If you can explain how an invoice becomes a reconciled record without opening multiple tools, stay at this stage longer.

- Growth stack

Best when clients need more than one payment method, such as PayPal plus Apple Pay, while reporting still lands in QuickBooks. This stage improves invoicing automation and follow-up timing, but adds more policy checks and moving parts. Key differentiator: more collection flexibility without losing visibility. Keep a market note per rail. PayPal defines domestic and international by market, and update timing can differ by region (US page: February 19, 2026; MU page: 21, April 2025).

The main risk here is invisible complexity. Another rail gets added, another policy note gets skipped, and exceptions start living in messages instead of the record system. Add one rail or one automation at a time, then run a full invoice lifecycle before making it standard across clients.

- Risk-sensitive stack

Best for high-ticket or cross-border work where holds and disputes can disrupt cashflow. Capture status changes automatically, then require manual approval before treating funds as available for payout or spending. Key differentiator: explicit exception control over speed. PayPal merchant documentation includes invoicing transaction and chargeback fee categories. Policy changes are posted on a Policy Updates page, and exchange rates or bank/card issuer fees may still apply even when temporary waivers exist for specific corridors.

At this stage, speed matters less than protecting your judgment about available cash. Let automation gather status changes, trigger alerts, and tee up the records, but keep the approval step with the person who owns delivery or spending decisions.

If you rely on Zapier or n8n, keep high-risk events out of full auto. Route low-risk status updates automatically, and require human confirmation for unusual amounts, cross-border events, or disputed payments. In practice, the automation can gather the event and create the task, but the release decision should stay manual.

A good test is simple: if a disputed or unusual payment can move through your automations without anyone noticing until the weekly review, the scope is too wide. Tighten it until risky events create visibility instead of false confidence. If you want a deeper dive, read The Best Invoicing Software for Freelancers. Want a quick next step? Try the free invoice generator.

Best tools and rails for each finance job#

Best results come from one invoice hub, one automation connector, a small set of payment rails, and a weekly cash-allocation review. The fewer duplicate roles you assign across tools, the easier it is to troubleshoot when something looks wrong.

| Finance job | Options | Primary use | Control note |

|---|---|---|---|

| Invoicing and collection hub | QuickBooks or QuickBooks Solopreneur | Invoice issuance, follow-up, and status tracking from one home base | Keep the invoice path traceable from sent to paid to reconciled |

| Automation glue | Zapier or n8n | Move paid-invoice events into the tracking sheet and follow-up queue | Keep scope tight: auto-route low-risk updates and require manual confirmation for unusual amounts, disputes, or cross-border events |

| Payment rails | ACH, PayPal, Venmo, Apple Pay | Offer a limited mix that balances client convenience and reconciliation control | For PayPal, verify by market and page type before changing terms |

| Budget control layer | Profit First plus operating expense account discipline | Move cleared payments into predefined buckets and review transfers weekly against bank activity | Treat incoming cash as allocations, not one spendable balance |

- Invoicing and collection hub (QuickBooks or QuickBooks Solopreneur)

Use one home base for invoice issuance, follow-up, and status tracking so the same fields flow through reporting. The goal is fast traceability: sent to paid to reconciled without hunting across tools.

Use the same status language, due-date logic, and client identifiers every time. That consistency keeps reminders predictable and makes it easier to answer a basic question quickly: was this invoice sent, paid, pending, or simply updated?

- Automation glue (Zapier or n8n)

Automate repetitive handoffs, like moving paid-invoice events into your tracking sheet and follow-up queue. Keep scope tight: auto-route low-risk updates, and require manual confirmation for unusual amounts, disputes, or cross-border events.

Name your automations so the trigger and destination are obvious. If one breaks, you should know whether the gap affects follow-up, tracking, or reconciliation before you even open the workflow. That makes weekly checks faster and repair work less guessy.

- Payment rails (ACH, PayPal, Venmo, Apple Pay)

Offer a limited mix that balances client convenience and reconciliation control. For PayPal decisions, verify by market and page type before changing terms. The merchant fees page includes sections for invoicing transaction rates, alternative payment method rates, and dispute fees. Consumer pages define domestic (same market) vs international (different markets), and update dates can differ (US: February 19, 2026; MU: 21, April 2025). Log which market page you used and recheck the Policy Updates page before rollout.

Each added rail creates another terms check, another status path, and another place where client expectations can drift from your records. That is why a smaller, well-documented mix often works better than offering every option by default.

- Budget control layer (Profit First plus operating expense account discipline)

Treat incoming cash as allocations, not one spendable balance. Move cleared payments into predefined buckets and review transfers weekly against bank activity to reduce surprises from pending or disputed funds.

The discipline here is timing. Allocate from cleared activity, then compare the transfer plan to actual bank movement so you do not build your spending plan on top of money that is still unsettled or under review.

If a rail decision depends on fees you cannot verify by market and date, pause and keep the setup simple until you can confirm. Simplicity is not a step backward if it preserves traceability. For a broader system view, see Financial Management for Freelancers: Budgeting, Saving for Taxes, and Retirement.

All-in-one app versus DIY AI finance stack comparison#

Choose an all-in-one setup first, and move to a DIY stack only when you can point to at least three recurring automations that materially cut recurring work. Most freelancers overestimate the benefit of flexibility and underestimate the cost of maintaining it.

| Option | Best for | Pros | Cons | Failure mode to watch |

|---|---|---|---|---|

| All-in-one in QuickBooks / QuickBooks Solopreneur | Solo operators who want speed and clear ownership | Fewer moving parts, faster onboarding, easier bookkeeping handoff | Less custom logic as edge cases grow | Exceptions get forced into default fields and stay hidden until review |

| DIY AI finance stack with Zapier or n8n | Builders with repeat exceptions and clear integration goals | Flexible triggers and tailored workflows | Higher maintenance, more testing, more breakpoints after app/auth changes | A background automation fails silently and leaves paid invoices unreconciled |

| Hybrid setup | Growing freelancers with mixed complexity | Core records stay centralized while targeted tasks are automated | Requires strict ownership and naming discipline | Duplicate records across tools create conflicting totals |

The real tradeoff is not whether you can automate. It is how many places a status can drift before anyone notices. All-in-one tools constrain you, which is often useful early. DIY stacks let you route information exactly where you want it, but every extra handoff creates another place where a changed field, expired auth, or hidden error can break the chain.

Recent 2026 roundups compare multiple tools by business stage rather than declaring one universal winner, so fit and integration should drive the choice. Use compatibility as a hard filter: if a tool does not integrate cleanly with your existing systems, skip it.

Decision rule: choose all-in-one first unless you can document three automations that each remove recurring work and have a clear owner. Write those automations down in plain language. If you cannot describe what triggers them, what record they change, and who checks failures, you are not ready for the maintenance load.

Verification checkpoint: run one full invoice end to end before broader rollout, and confirm send date, payment confirmation, ledger entry, and reconciliation result all match without repeated patching. If the first test still creates cleanup work, stop there. The goal is fewer interventions, not faster creation of new ones.

Client onboarding checklist that prevents late pay and bad terms#

Use one onboarding checklist for every client, and lock terms before work starts so payment handling stays consistent. Late pay often starts well before the overdue date. It starts when terms live in scattered places or when one client gets custom handling which no one remembers later.

- Set written payment terms before kickoff

Put due dates, accepted payment rails (ACH, PayPal, Venmo, Apple Pay), and late-payment handling in the signed agreement, not chat. Add a clear pause-work condition for overdue invoices.

Treat the signed agreement as the control document. Before kickoff, compare those terms to the invoice template you will actually use so the first invoice does not create a mismatch. If a client wants a different rail or different timing later, update the signed terms and the template together.

- Standardize invoice fields in QuickBooks

Use one invoice template with consistent fields (client name, project ID, issue date, due date, payment rail, status). Avoid client-specific labels that force manual cleanup during reconciliation.

Consistency matters more than aesthetics here. The fields should let you filter, follow up, and reconcile without guessing which label means what. If a client wants different wording on the front end, keep the same underlying structure in your records.

- Require a first-payment milestone before net terms

For new clients, collect an initial milestone payment before offering longer payment windows. This gives an early signal on payment behavior before larger balances build.

This is less about being strict for its own sake and more about getting an early operational signal. A clean first payment shows that the client can use the agreed rail and follow the agreed process. If that first milestone is messy, fix the process before a larger balance builds.

- Assign a client risk tag and handling rules

Tag clients as low, medium, or high risk, then tie each tag to reminder cadence, manual review, and allowed payment methods. For higher-risk clients, confirm funds before treating them as available.

The tag only helps if it changes behavior. A higher-risk tag should change reminder cadence, approval steps, and what counts as confirmed funds. Keep the rules simple enough that you will actually follow them every time.

Keep one verification note in each client file: contract version, accepted rails, and last PayPal fee-policy check date. PayPal's US consumer fees page shows a last-updated date (February 19, 2026) and points to a Policy Updates Page. The merchant fees page includes invoicing, dispute, and chargeback fee categories. That note becomes useful later when a client asks for a change and you need to confirm what was originally approved.

If a client asks to change payment terms after kickoff, pause delivery until the change is signed and reflected in your invoice template. The clean handoff is simple: signed terms, matching invoice template, first invoice, risk tag, then work. If that sequence gets loose, payment problems usually show up later in reconciliation rather than at kickoff.

What to do when payments fail, get held, or trigger disputes#

When a payment goes sideways, treat it as a controlled exception, not a one-off judgment call. Keep routine collection automated, then follow a fixed escalation path. The worst time to invent a process is after money is already stuck.

- Escalation ladder with 4 fixed steps

Use the same sequence every time: reminder, direct follow-up, service pause, then formal collections handoff. Start with your invoicing workflow, request a confirmed payment date and method, and pause service if that commitment does not happen. Do not improvise once collection has failed.

Keep the language and ownership consistent. The reminder should reference the invoice and current status. The direct follow-up should ask for a confirmed payment date and method. The service pause should be applied the same way whenever your terms allow. The formal handoff should use the same incident packet instead of rebuilding the story from memory.

- Four payment states that drive action

Keep pending, failed, disputed, and resolved as separate operational states with different actions. Do not treat pending or held funds as spendable. Only move work forward when payment status is confirmed in your source system.

These states stop wishful thinking. pending means monitor. failed means follow up and confirm next action. disputed means stop automatic progress and gather evidence. resolved means the exception is closed and the normal workflow can continue.

- Manual override on 2 risk triggers

Pause auto-fulfillment when either trigger is true: the amount is high for your business, or the client has weak payment history. Require manual confirmation of invoice and ledger status before delivery resumes. This adds friction, but usually reduces downside risk.

The automation can still create alerts, tasks, or notes, but it should not release delivery by itself when either risk trigger is present. That keeps a high-risk case from being treated like a normal invoice just because the workflow fired.

- Evidence packet with core records

Maintain one incident packet per case with invoice copy, payment-attempt history, client messages, and ledger/reconciliation notes. If you need to escalate, this gives you a clear timeline and ownership trail instead of a fragmented account.

Keep the packet in one place and in order. Start with the invoice copy, then the payment-attempt history, the client messages, then ledger or reconciliation notes. The goal is a short, defensible timeline, not a pile of disconnected screenshots.

Weekly finance checklist that keeps automation honest#

The goal is simple: run one repeatable loop that verifies what is real in your books, your automations, and your client files. If misses continue for two cycles, simplify the system before adding anything new. This checklist matters because it catches small problems before they become month-end confusion.

- Monday: reconcile outcomes to deposits

Match prior-week invoice outcomes in QuickBooks against deposits in your business bank account, then flag anything still pending or unresolved. Do not plan around money that is not fully available.

Start with what changed, not with what you hope is true. Compare invoice status, payment confirmation, and bank activity for the prior week. If something is marked paid but not clearly supported by a matching bank movement, leave it out of cash planning and open an exception note.

- Midweek: check automation health

Review every Zapier or n8n workflow for failed runs, stale credentials, and broken field mappings. Fix root causes, then run an end-to-end test so proposals, agreements, payments, and reconciliation still connect cleanly.

Do not stop at clearing the visible error. Confirm that the same trigger still writes to the right fields and does not create duplicate or partial records. Then run a simple end-to-end check so the whole path still works the way you expect.

- Friday: review spending drift

Check expense-tracking drift, subscription creep, and Profit First transfers into the operating expense account. Compare booked expenses against what actually cleared the bank.

This is where "booked" and "cleared" often drift apart. Look for recurring subscriptions that no longer matter, transfers that did not match the plan, and expenses that hit the bank without clean categorization. Cleaning this up here makes the next week easier.

- Monthly: audit each client file

Confirm each client file has current terms, a complete invoice trail, message history, and a clear non-payment path. Verify that cleanup and handoff habits are being followed.

Use the monthly audit to confirm that client files still support the way you are operating now, not just the way you set them up at kickoff. Terms, accepted rails, invoice trail, and notes about what happens next should still agree with each other.

- Two-cycle miss rule

If reconciliation misses continue for two cycles, reduce automation scope and simplify the tool chain before adding new features.

Treat a repeated miss as a system problem, not a one-off. If the same mismatch survives the normal weekly review twice, something in the workflow is too fragile for the current level of automation.

Build a get-paid system you can trust#

Trust comes from consistency: automate repeatable admin, keep human approval at cash-risk points, and run the same onboarding checklist for every client.

- Keep automation in the admin lane, keep judgment at cash-risk points

Automate recurring invoicing, reminders, and ledger updates, then require manual review for disputes, unusual requests, or signed-term changes so exceptions have clear ownership.

That boundary is what preserves cash control when volume rises. Speed is helpful, but only when the system still makes it obvious who approves the risky decisions.

- Expand in phases only after proof, not optimism

Roll out to one client segment first, reconcile on a fixed cadence, and expand only after exception handling is stable in your own records.

Proof means you can show the full trail in your own system, from invoice to payment status to reconciliation, without repeated patching.

- Filter ideas from public content before you adopt them

Use public "AI finance stack" posts as idea inputs, not proof, especially when key details are behind member-only posts. Keep only changes that improve reconciliation without increasing exception work.

If an idea sounds clever but makes your weekly checks harder or your incident notes longer, it is not an upgrade for your stage.

- Tie growth context to margin discipline

Growth headlines can be directionally useful, but operational decisions should follow verified net cash after payment processing costs and unresolved incidents. One industry article cites $1.5 trillion in 2024 earned on Upwork. That is context, not your control metric.

Your control metric is still the cash that clears, reconciles, and remains usable after the real frictions in your own process.

If you need deeper controls for collections, payouts, and traceable processes, review Gruv options where supported and confirm coverage for your market and program before rollout.

Frequently Asked Questions

What should I automate first in freelance finances?

Start with invoice creation, payment reminders, and ledger updates because they are repetitive and easy to verify against bank deposits. Keep client terms, dispute handling, and release decisions manual until records stay clean for at least two reconciliation cycles.

Can I automate invoicing without losing control of cashflow?

Yes. Separate payment states and treat only resolved funds as spendable. Keep human review for pending, failed, or disputed items before delivery or payout decisions.

Is QuickBooks Solopreneur enough, or do I need extra tools?

It can be enough when your invoice-to-reconciliation path is simple and exception volume is low. Add extra tools only when you can name a recurring gap that shows up in weekly checks.

When should I use Zapier or n8n instead of an all-in-one app?

Use them when you need cross-app triggers your core setup cannot handle reliably, such as routing payment events into task tracking and follow-up queues. Start narrow and expand only after repeated end-to-end tests pass.

How do I reduce chargebacks and payment holds in an automated setup?

Keep an incident packet for every dispute: invoice copy, payment-attempt history, client messages, and reconciliation notes. In merchant docs, review sections for Invoicing Transaction Rates, Chargeback Fees, and Dispute Fees before setting response rules.

Which payment methods should I offer first: ACH, PayPal, Venmo, or Apple Pay?

Offer the methods your clients already use, but document accepted rails in the signed agreement and invoice template. For PayPal, check whether a payment is domestic (same market) or international (different markets) for that market, and review the Policy Updates Page. The US consumer fees page shows a last-updated date of February 19, 2026.

How often should I reconcile automated transactions?

Run a weekly reconciliation pass and a monthly documentation checkpoint across active clients. If misses continue for two cycles, reduce automation scope before adding new connections.

Watch

Automate Your Freelance Finances

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- childcarenj.gov/ChildCareNJ/media/media_library/CCDF_State_P...trusted

- tiffin.edu/wp-content/uploads/AI-Tools-with-Description...trusted

- crofils.com/2025/05/18/from-cash-flow-chaos-to-calm-with...external

- mercury.com/blog/personal-finance-automation-toolsexternal

- solofinancehub.com/blog/how-to-automate-freelance-financesexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Best Invoicing Software for Freelancers in 2026

If you're picking [invoicing software](https://www.helcim.com/guides/best-invoicing-software-for-freelancers), optimize for billing reliability first, not invoice design. This guide groups tools into three practical lanes so you can shortlist fast, then confirm your choice with one real end-to-end invoice test before you migrate clients. If you're building a broader workflow, not just invoices, pair this with [Automating Your Freelance Finances: A Guide to Tools and Workflows](/blog/automating-freelance-finances).

The Best Business Bank Accounts for Freelancers

APY can break a tie. It should not drive your shortlist. If you are comparing the best business bank accounts for freelancers, start with the setup that keeps money moving, records clean, and month-end work manageable.

Freelance Financial Management That Protects Cashflow First

Stabilize cash timing first. Perfect budgeting can wait. When payments arrive unevenly, the immediate win is a repeatable way to see what came in, what needs to be set aside, and what is actually safe to spend this week.