Quick Answer

Start with the IRS Substantial Presence Test, not a single 183-day shortcut: meet 31 current-year days and the weighted three-year formula in IRS Publication 519 before drawing a federal conclusion. Then run each state separately. Minnesota can treat you as resident through domicile or statutory residency, where a permanent abode plus presence on any part of a day can matter. A clean federal result does not automatically close state filing exposure.

Introduction Stop Treating 183 Days Like a Magic Number#

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

At the federal level, the Internal Revenue Service uses the Substantial Presence Test to determine U.S. tax residency. It is not a same-year shortcut. You generally need at least 31 days in the current year and a combined 183 days across the current year and prior two years under IRS counting rules. The IRS example of 120 + 40 + 20 = 180 shows why this matters.

Many filing mistakes start when you do a raw current-year count, decide you are safely under a headline number, and stop there. That skips the weighted lookback and ignores that federal status is its own classification exercise.

Day counting is more technical than most people expect. For this federal test, being physically present at any time during a day generally counts, with specific exceptions such as certain transit days under 24 hours. The right question is not "How many nights was I there?" It is "Which days count, which days are excluded, and what does the three-year calculation produce?"

Rules outside this federal test can differ, and you need to evaluate them separately. You can satisfy one test and still need to assess another. A one-number shortcut can miss those differences, especially when another jurisdiction uses its own day-count method or looks beyond the calendar.

This guide gives you three things:

- A two-layer decision path so you run the federal substantial presence calculation first, then evaluate any other relevant residency rules separately.

- A documentation checklist focused on records that support your day count and residency position before return prep starts.

- Clear escalation triggers for close thresholds, excluded-day questions, or conflicting facts.

If you remember one rule before filing season, run the federal calculation first, then evaluate each other relevant jurisdiction on its own terms.

The Mental Model You Need Before You Count Days#

Use a two-layer check, not a single day total: federal status first, then state residency. If you blend those layers, you can end up with the wrong filing position.

At the federal layer, IRS Publication 519 classifies aliens as either resident alien or nonresident alien, and that classification drives income scope. Resident aliens are generally taxed on worldwide income, while nonresident aliens are taxed on U.S.-source income and certain connected income. So the federal answer is not just a label on a form. It changes what income enters the return in the first place.

At the state layer, the rules can still differ. California says residency is a facts-and-circumstances determination, allows part-year treatment, and does not issue written opinions confirming residency for a specific period. So being under 183 in one place is not, by itself, a complete residency answer. A year can contain different periods, and your file needs to show when the status changed and why.

Use this quick decision tree before you file:

- Jurisdiction in scope: list federal plus each state where you lived, worked, or had relevant ties.

- Test type: classify federal status, then identify each state's own residency standard.

- Day-count method: apply each jurisdiction's counting approach separately.

- Tie-break conditions: check additional residency facts, including part-year facts.

- Filing consequence checkpoint: confirm whether income is treated as worldwide, U.S.-source, or state-source for that filing position.

That order matters because it forces you to finish one layer before you jump to the next. It also keeps your calendar work separate from your tie-fact analysis. A common problem is getting comfortable with a day count and assuming the same answer must work everywhere else. This checklist is meant to stop that shortcut.

It also helps to do this in a worksheet instead of in your head. Give each jurisdiction its own line. Record the dates in scope, the rule you are applying, the day-count method, any fact-sensitive issues, and the filing consequence you think follows. If you later need to explain the position, that worksheet becomes the backbone of your file.

If your layers point in different directions, pause and escalate before filing. For a deeper contrast on residence rules versus other tax concepts, see Tax Residency vs. Citizenship-Based Taxation: The US Anomaly. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

How the U.S. Federal Test Actually Works in Practice#

At the federal layer, you are classifying status, not just counting days. The IRS uses the Substantial Presence Test to determine whether you are a U.S. resident or nonresident alien, and that result sets your filing posture.

| Period | Days | Weight | Weighted days |

|---|---|---|---|

| Current year (2025) | 120 | 1 | 120 |

| First prior year (2024) | 120 | 1/3 | 40 |

| Second prior year (2023) | 120 | 1/6 | 20 |

The test is not a simple same-year count. You must meet both gates:

- At least 31 days of U.S. presence in the current year.

- At least 183 days on a weighted three-year formula: all current-year days, plus 1/3 of the first prior year, plus 1/6 of the second prior year.

Treat those as gates in order. First confirm the current-year presence requirement. Then run the weighted three-year formula. If you skip the first step or treat the whole thing as a same-year tally, you are not really applying the federal test.

IRS example logic shows why the weighting matters: 120 days in 2023, 120 in 2024, and 120 in 2025 gives 120 + 40 + 20 = 180, so it does not meet the test for 2025. That is the simplest reminder that several years of meaningful U.S. presence can still fail the federal test once the prior years are discounted.

Also, under this test, being in the U.S. at any time during a day generally counts, though listed exclusions apply. In practice, a day ledger based only on nights, client meetings, or memory can drift away from the legal count. If you are present at any time during the day, you usually start from the assumption that the day counts and then test whether an exclusion applies.

Use this checkpoint before you finalize federal status:

- Build a three-year worksheet with raw days by year, then apply 1, 1/3, and 1/6.

- Remove excluded-day categories before final totals.

- Confirm the output: U.S. resident or nonresident alien.

- Tie that output to filing consequences immediately.

Keep the raw day total and the adjusted total separate in your file. That makes later review much easier. If the number changes, you want to know whether the facts changed or the exclusion analysis changed.

Do not let the federal worksheet sit as a math exercise with no filing note attached. Once you have the classification, write down the filing posture it supports. That prevents a common operational failure: the day-count worksheet says one thing, but the return gets prepared as if the opposite status applied.

If your weighted total is near the line, or your visa history includes categories such as F-1 visa, escalate before filing. Close-call years are where misunderstandings about excluded days get expensive. For a quick next step, try the tax residency day counter.

Why State Rules Can Trigger Residency Even When Federal Status Does Not#

Federal nonresident status does not automatically prevent state residency treatment. In Minnesota, residency can be triggered through either domicile or statutory residency, so a federal day-count result alone can miss the state filing position.

That is why you should treat the federal answer as the first layer, not the final one. A clean federal result can still sit next to a messy state question if the state uses different criteria or asks about living arrangements and intent.

For statutory residency, you need both pieces: a permanent abode in Minnesota, meaning a residence with kitchen and bathing facilities, and presence in the state on all or part of more than half the days. Partial days count, so overnight-only tracking can understate presence. A calendar that only tells you where you slept is not enough if the rule counts any part of a day.

In practice, test the abode issue and the day-count issue together. Mark the dates when the residence was available to you, then compare that period with the days you were present. If those two records live in different places, reconcile them before you decide the filing position.

Domicile uses a different lens: where you intend your permanent home to be, tested against your actions. When facts are mixed, relying on a narrow calendar story can raise audit exposure. If your stated intent points one way but your living pattern points another, that is not a routine filing decision anymore.

| Checkpoint | What to verify |

|---|---|

| Statutory residency | Permanent abode status plus presence counted as all or part of a day |

| Domicile | Stated intent and observable actions align |

| Filing consequence | Whether your resident vs nonresident position changes state reporting |

A useful internal test is whether you can state your position in a single sentence and support each piece of that sentence from your records. If your federal result is clear but the state facts are close, reconcile day records, abode access, and intent evidence before filing. Related: Spain Tax Residency: More Than Just Counting Days.

The Four Mistakes That Cause Expensive Residency Problems#

Most costly residency problems come from execution shortcuts, not obscure rules. The pattern is usually ordinary: the wrong layer, the wrong count, or the right answer with no file behind it.

- Using one rule for everything. IRS federal status, meaning resident alien vs. nonresident alien, is a separate analysis, and those statuses are taxed differently. A state can apply its own residency framework and income-scope treatment in the same year. This usually starts when you let a same-year calendar total become the answer for every return. The fix is simple: classify the federal year first, then test each state separately.

- Counting overnights instead of counted days. Under the substantial presence test, being in the United States at any time during a day generally counts as a day, with explicit exceptions. If you only track nights, your count can be wrong. That is why a usable day ledger needs arrivals and departures, not just where you slept.

- Treating day totals as the whole story. Connection facts can still matter; in the IRS context, permanent home location and where a spouse or minor child lives are explicit signals. When those facts conflict with your day log, treat that as a red flag. A neat spreadsheet will not overcome a home-tie story that points somewhere else.

- Waiting for an inquiry before organizing proof. California says residency is determined from all facts and circumstances, and FTB does not issue written residency opinions for a specific period. Part-year treatment can split income scope between resident and nonresident periods, so build dated records before filing. By the time an inquiry arrives, it is much harder to reconstruct why you treated one date range one way and another date range differently.

Use this pre-filing checkpoint to avoid all four mistakes:

- Confirm federal classification first, then test each state separately.

- Recalculate day counts with the correct method and exceptions.

- Reconcile connection facts, including home and family, with your day narrative.

- Save dated evidence before filing, not after agency contact.

Add a brief note when you correct a count or resolve a conflict in the records. Those notes help show that the final filing position came from a deliberate process rather than a guess made under deadline pressure.

If any checkpoint conflicts, escalate before you file.

Build an Audit Ready Evidence Pack Before You Need It#

Build one audit-ready evidence pack before filing season and keep it current all year. The goal is simple: your residency story, account records, and tax filings should agree before you file, not after someone asks questions.

Think of it as one controlled file, not a pile of loose documents gathered after the fact. A strong file lets someone move from the calendar to the workpaper to the filed return without guessing what happened in between. If you would need to rely on memory to explain a key judgment call, the file is not ready yet.

Use one working file with dated records for:

- Travel log with entry and exit proof for each border movement, organized so the count can be followed in date order.

- Home tie records, including leases, utility records, and abode access periods.

- Personal tie facts for disputed periods, for example spouse or household location.

- Prior and current filing copies, plus workpapers that show how you reached status conclusions.

- Foreign account and asset inventory mapped to each reporting track.

- Form 8938 support file showing included assets and your inclusion logic.

- FBAR support file aligned with FinCEN Form 114 inputs.

Each item has a job. The travel log supports the day count. The home-tie and personal-tie records support the narrative about where you were actually based. The workpapers show how the legal conclusion was reached. The foreign-asset files show that reporting decisions were made from a consistent asset population rather than from memory at the end of the year.

For disputed periods, keep the evidence tied to the dates that matter. A vague annual note is less useful than a dated file that shows what was true during the exact period your filing position depends on.

For federal coordination, treat Form 8938 as a threshold-based check, not a default filing. It is used to report specified foreign financial assets when value exceeds the applicable threshold, and it is attached to the annual income tax return. Thresholds vary by filer type, with higher thresholds for some joint filers and some taxpayers living abroad. If no income tax return is required, Form 8938 is not required for that year.

The practical point is to make the Form 8938 decision from the right starting place. Start with filer classification, return-filing status, and the asset population you are actually testing. Then document why items were included or excluded. That way, if the form is needed, you already have the support file. If it is not needed, you still have a record of how that decision was reached.

Treat FBAR and FATCA as related but separate checks, then reconcile them on a cadence:

- Monthly: collect and date supporting records.

- Quarterly: reconcile account and asset populations across FBAR and Form 8938 tracks, and document intentional differences.

- Annually: lock the final dossier before filing.

A simple way to do this is to keep one master asset list and mark how each item is treated on each track. If the populations differ, write down the reason while the facts are still fresh. That is much easier than trying to recreate the logic at year end.

If records conflict across systems, resolve the conflict before you file rather than hoping to explain it later. An after-the-fact explanation is weaker than a dated file that already shows how you counted days, how you handled abode periods, and how you reconciled FBAR and Form 8938 decisions.

Clear Escalation Triggers for When to Talk to a Tax Pro#

Talk to a tax pro before filing when your Form 8938 decision depends on filer classification, threshold interpretation, or uncertain return-filing status. The earlier you escalate, the narrower the question usually is, and the easier the review is to document.

| Trigger | Why it needs review | What to confirm before filing |

|---|---|---|

| You are near a Form 8938 threshold | The commonly cited $50,000 threshold is not universal | Confirm whether higher thresholds apply based on joint filing or living abroad |

| Your filer category is unclear | Form 8938 applies to specified persons, including specified individuals and some specified domestic entities | Confirm whether you are filing as a specified individual or a specified domestic entity |

| You are unsure whether you must file an income tax return | Form 8938 must be attached to an annual income tax return, and is not required for years when no return is required | Confirm return-filing obligation first, then Form 8938 obligation |

| Your asset list is ambiguous | Some financial accounts are excluded from Form 8938 reporting | Reconcile included vs excluded accounts before preparing the form |

| A domestic corporation, partnership, or trust is involved | Certain domestic entities formed or used to hold specified foreign financial assets may have Form 8938 obligations | Confirm entity treatment and filing requirements for the relevant tax year |

Before that review, prepare a short note showing the filing position you expected to take, the exact point that makes the answer uncertain, and the records that bear on that question. That turns a vague request into a focused technical review.

Common failure modes are treating one threshold as a universal rule or preparing Form 8938 before confirming return status and filer classification. Another is letting the asset population drift between your workpapers and your actual forms. If your facts are close to a threshold or your classification is unclear, pay for pre-filing advice early and document the filing position in writing.

Keep that written position with the same evidence pack used for the return. If the question comes up later, you want the technical conclusion and the supporting file in the same place.

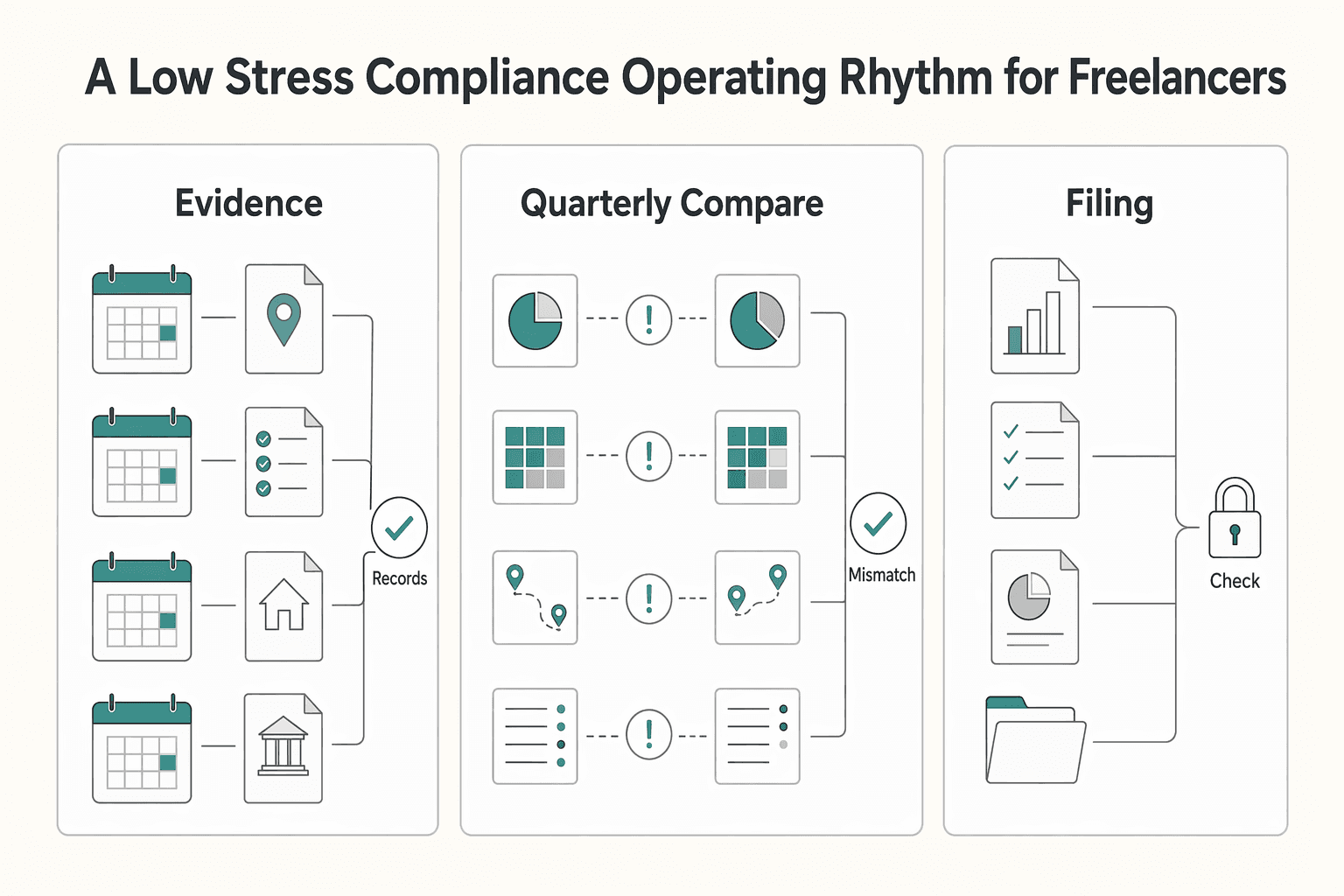

A Low Stress Compliance Operating Rhythm for Freelancers#

Use a simple monthly-quarterly-pre-filing rhythm so compliance decisions are made before deadline pressure. The goal is to catch small record mismatches early, while they are still easy to fix.

Think of this as an operating rhythm, not a filing-season scramble. If you close each month with a current ledger and supporting records, you avoid having to reconstruct movement, living patterns, and asset scope all at once.

Keep one dated ledger per active jurisdiction and update it monthly. Track days present, likely residency signals, and material changes in living patterns. If travel logs, lease periods, and account activity conflict for the same month, resolve the conflict and note what changed.

- Monthly: refresh day counts, residency signals, and evidence status by jurisdiction.

- Quarterly: compare federal and state assumptions, and flag drift for review.

- Pre-filing: lock a status memo, evidence index, and reporting checklist before return prep, including FBAR, FATCA-related items, and Form 8938 where applicable.

The monthly step prevents most future stress. Close the month while travel and living arrangements are still fresh in your mind. Attach the relevant proof, update the ledger, and write a short correction note if something did not match on the first pass.

The quarterly step is where you compare layers. Does the federal worksheet still point the same way as the state review? Do your day counts still align with your abode or domicile story? If not, flag it while there is still time to resolve it calmly.

For pre-filing, make Form 8938 decisions explicitly. Confirm which threshold applies to your filing status and living situation, and verify whether an income tax return is required, since Form 8938 is attached to that return and is not required when no return is required. Document excluded accounts so your asset scope is clear.

Two common errors create avoidable risk: treating one number, like $50,000, as a universal rule, and treating FBAR and Form 8938 as interchangeable. Both errors come from collapsing separate checks into one answer. If a correction may depend on non-willful conduct standards, weak documentation makes your position harder to support.

If you use Gruv records, export payment and payout data with timestamps and stable transaction IDs where supported, then map those exports to the same evidence index used for residency and foreign-asset checks. That way your operating records and your tax file can be reviewed together instead of as separate systems.

Conclusion Use a Two Layer Test and Document as You Go#

The core takeaway is simple: residency is a two-layer decision, not a one-number shortcut. Assuming one day count settles federal and state outcomes is where avoidable errors start.

Start with the federal layer. IRS Publication 519 separates resident-alien and nonresident-alien status and addresses the Substantial Presence Test as a distinct analysis. That structure matters because the federal analysis starts with status.

Then run the state layer on its own terms. State tax exposure is not a copy of federal status. A general state principle is that residents are taxed on worldwide income while nonresidents are taxed on state-sourced income. Domicile is also a facts-and-circumstances call, and a person can have only one domicile at a time.

Use this pre-filing sequence every year:

- Run the federal decision path first and record assumptions.

- Run each state decision path separately, including domicile and other residency evidence where relevant.

- Reconcile both layers, then lock your evidence pack and escalation triggers before return prep starts.

By the time return prep begins, your file should already show what counted, what was excluded, and why the filing position follows from those facts. That is what makes a position defensible. A reviewer should be able to trace the conclusion from your calendar to your workpapers to the filed return without filling gaps from memory.

Documentation quality is what keeps positions defensible. Keep records of movement, home ties, and the reasons behind each status call. If a third party could not reproduce your conclusion quickly from your file, the file is not ready.

Final point: stay jurisdiction specific and verify locally. Rules vary by jurisdiction, and outcomes are driven by facts, not shorthand. One reported state example showed about $1 billion collected from residency audits over 2013 to 2017, with a 52% win rate across 15,122 audits. The practical message is straightforward: early decisions and clean records are cheaper than late defense.

Frequently Asked Questions

Is the 183-Day Rule the same thing as the federal Substantial Presence Test?

No. Minnesota's 183-day rule and federal residency tests are separate frameworks run by different authorities. Treat federal and state residency analysis as separate decisions in the same year.

Can I still be treated as a state resident if I am not a federal U.S. resident?

Yes. Under Minnesota's 183-day rule, you may still be treated as a resident even if you have permanent residency in another state, as long as the rule's conditions are met. If gross income meets the filing minimum, including the published $14,950 figure for 2025, a filing obligation may still apply.

Does part of a day count toward residency under state rules like Minnesota?

Under that state's 183-day rule, any part of a day counts as a full day. A full overnight is not required.

What is the practical difference between U.S. resident and nonresident alien for filing?

Status changes filing posture and can change how the same calendar year is taxed. One example is IRS first-year choice, which can treat you as a U.S. resident for part of the year and dual-status for that year. Because that election has specific presence tests, treat it as a technical decision.

When do tax reciprocity agreements change how a state applies residency rules?

For Minnesota's 183-day rule, reciprocity is explicitly relevant for North Dakota and Michigan residents. Do not assume reciprocity applies beyond listed states without checking current state guidance.

What records should I keep to defend my day count and abode position?

Keep a dated day ledger, travel evidence, and documents showing when an abode was available to you. For this rule, abode means a residence suitable for year-round use with its own cooking and bathing facilities. Keep correction notes when documents conflict.

When should I escalate to a professional instead of deciding residency myself?

Escalate when facts are near thresholds, records conflict, or federal and state outcomes do not align. Escalate faster if you are considering IRS first-year choice. The 31-day consecutive presence condition, the 75% test, and exempt-individual day exclusions require careful counting.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Tax Residency vs. Citizenship-Based Taxation: The US Anomaly

You're not choosing one tax identity and discarding the other. In cross-border life, you're usually operating two systems at the same time: a status-driven filing layer and a place-driven residency layer. Stop asking which one wins and start running one operating flow that covers exposure, obligations, paperwork, and proof.

Spain Tax Residency for Mobile Freelancers Who Need Defensible Records

Decide early, while the facts are still clean. Once you hit a year where Spain could plausibly challenge your position, it gets much harder to rebuild a consistent story from old emails, half-complete calendars, and missing receipts.