Quick Answer

Remitly is usually the better first check for family transfers when recipient access matters, especially cash pickup or country-specific home delivery, while Wise is strong for bank deposits when you want to compare the exact amount delivered. To compare fairly, use the same send country, receive country, amount, funding method, and payout type on both services before choosing.

The Quick Answer: A Consumer-Level Comparison#

For personal transfers, start by comparing Wise and Remitly with the exact same inputs. If your recipient can accept a bank deposit, check which quote delivers more. If recipient access matters more than pure pricing, Remitly is often the better first check, especially for cash pickup or country-specific home delivery.

To compare them fairly, use the same send country, receive country, amount, funding method, and payout type on both services. The total delivered amount can change when you switch from bank transfer to debit or credit card funding, or from bank deposit to cash pickup. Confirm the current policy by corridor.

A few terms are worth keeping straight. The mid-market exchange rate is the rate banks and transfer services use to trade currencies with each other. A rate markup means a provider uses its own exchange rate and adds a margin instead of using that mid-market rate. An upfront fee is the fee shown before you confirm. A delivery estimate is the expected arrival time for the recipient account.

| Decision input | Wise | Remitly | What you should verify |

|---|---|---|---|

| Total delivered amount | Explains the mid-market rate and shows the fee upfront. Fees vary by how you pay, amount, and exchange rate. | Cost depends on amount, payment method, and delivery option. Displayed rates can change. | Compare the exact "recipient gets" result, not just the send fee. Confirm current policy by corridor. |

| Funding method impact | Wise says send fees vary by payment method. | Remitly says cost varies by payment method too. | Run the quote twice if needed, for example bank transfer vs debit card. |

| Delivery path reliability | Wise gives an arrival estimate when you make a transfer. It also states 74% arrive in under 20 seconds and 95% in a day. | Remitly shows total cost and delivery time before sending and advertises an on-time delivery promise with fee refund if late. | Check the quoted arrival time for your exact route, not homepage speed claims alone. |

| Recipient access needs | Use bank-deposit receiving as the baseline comparison on Wise. | Bank deposit, cash pickup, and country-dependent options. Home delivery is specifically listed for the Dominican Republic, Philippines, and Vietnam. | Make sure the recipient actually has the account or ID needed for pickup. |

| Support responsiveness | Wise says phone support is available 24/7. | Remitly advertises 24/7 help in English via chat and phone. | Support exists on both sides, but do not assume the same response time or resolution speed. |

If you're sending personal support, use this quick rule set:

- Maximize recipient amount to a bank account: run Wise and Remitly quotes with identical inputs, then compare the exact delivered amount.

- Speed matters more than fee math: check delivery-time quotes on both services first, then choose the faster corridor-specific route.

- Recipient needs cash pickup or courier delivery: Remitly is usually the more relevant first check.

One practical red flag: do not compare a Wise bank-deposit quote with a Remitly cash-pickup quote and treat that as a clean price test. Save a screenshot of the fee, exchange rate, and delivery estimate before you send, since rates and options can shift.

That consumer lens is useful, but it only answers the personal-transfer question. Once client revenue enters the picture, convenience stops being the main standard and cashflow risk takes over. If you want a deeper dive, read The Best Way to Send Money to the Philippines from the US. If you want a quick next step, try the free invoice generator.

A Professional Risk Assessment: Can They Handle Your Business?#

For client revenue, start with risk, not convenience: treat Wise Business as your default for inbound business payments, and treat Remitly primarily as a remittance or outbound payout option unless you verify an inbound business path for your exact corridor and account type. A high-value client payment tests four things: account type fit, transaction pattern fit, verification readiness, and cashflow impact if funds are paused.

| Pre-payment check | What to confirm |

|---|---|

| Account type fit | If funds come from a business bank account, Wise says you need a Wise Business account; business-funded payments to a personal Wise profile can be rejected. |

| Transaction pattern fit | Confirm the product is documented for receiving business payments, not only sending payouts. |

| Verification readiness | Be ready to provide identity/business documents quickly if the transfer is reviewed. |

| Interruption impact | Decide now what happens if funds are delayed and your payroll, rent, tax set-asides, or contractor payments are due. |

When a new overseas client is paying a large invoice, check these in order before you share payment details:

- Account type fit: If funds come from a business bank account, Wise says you need a Wise Business account; business-funded payments to a personal Wise profile can be rejected.

- Transaction pattern fit: Confirm the product is documented for receiving business payments, not only sending payouts.

- Verification readiness: Be ready to provide identity or business documents quickly if the transfer is reviewed.

- Interruption impact: Decide now what happens if funds are delayed and your payroll, rent, tax set-asides, or contractor payments are due.

The AP test that actually matters#

If your client uses accounts payable (AP), execution risk often shows up first in payee setup and reconciliation details.

| AP criterion | Wise Business | Remitly |

|---|---|---|

| Legal payee matching | Requires the funding bank-account name to match your Wise profile or registered business name. | Has a business signup path and business agreement language, but you should verify inbound legal-payee handling for your corridor before you rely on it for client revenue. |

| Invoice/reference handling | Provides a specific invoice-payment rule: use either invoice number or payment reference number (not both) so funds can be matched. | No equivalent inbound invoice-matching guidance was supported in this section's sources; verify what reference data carries into your records. |

| Receiving-account structure | Documents local account details so customers can pay into your Wise account; states acceptance in 18+ currencies. | Sourced business docs here are send-side (fund and send). Do not assume equivalent multi-currency inbound receiving details without product-level confirmation. |

| Escalation when paused | Transfers can pause during verification; some cancellation flows auto-cancel/refund if requested information is not provided within 2 working days. | Offers 24/7 English support, but timing still depends on review and partner availability; requested information not provided within three days can lead to cancellation. |

Built for business versus adapted for it#

The real distinction here is inbound capability. Wise Business is documented for collecting customer payments through local account details, then converting from the same account across 40+ currencies. Remitly should not be labeled consumer-only, but the supported evidence here describes business sending and outbound coverage, including 100+ local currencies and over 170 countries, not a clearly documented primary inbound setup for collecting client revenue. If you plan to use it for inbound revenue, verify the terms and workflow first.

| Attribute | Wise Business | Remitly |

|---|---|---|

| Collecting customer payments | Collecting customer payments through local account details | Not a clearly documented primary inbound setup for collecting client revenue |

| From the same account | Converting from the same account across 40+ currencies | Business sending/outbound coverage |

| Coverage cited here | 40+ currencies | 100+ local currencies and over 170 countries |

Reconciliation risk is still payment risk#

Payment risk does not end at receipt. You also need records that reconcile cleanly. Wise documents statement exports for up to a 365-day period per file, accounting connections, and QuickBooks sync behavior that separates bank-feed sync from bill reconciliation. It also notes that accounting-data sharing authorizations can expire after 90-180 days, so you should build reauthorization into your finance ops routine.

Use a simple rule: personal remittance rails for family-support transfers; business-ready receiving rails for client revenue collection, especially when a 5-14 working day verification delay would strain cashflow. Related: Using Wise for Large Transfers Without Cashflow Surprises.

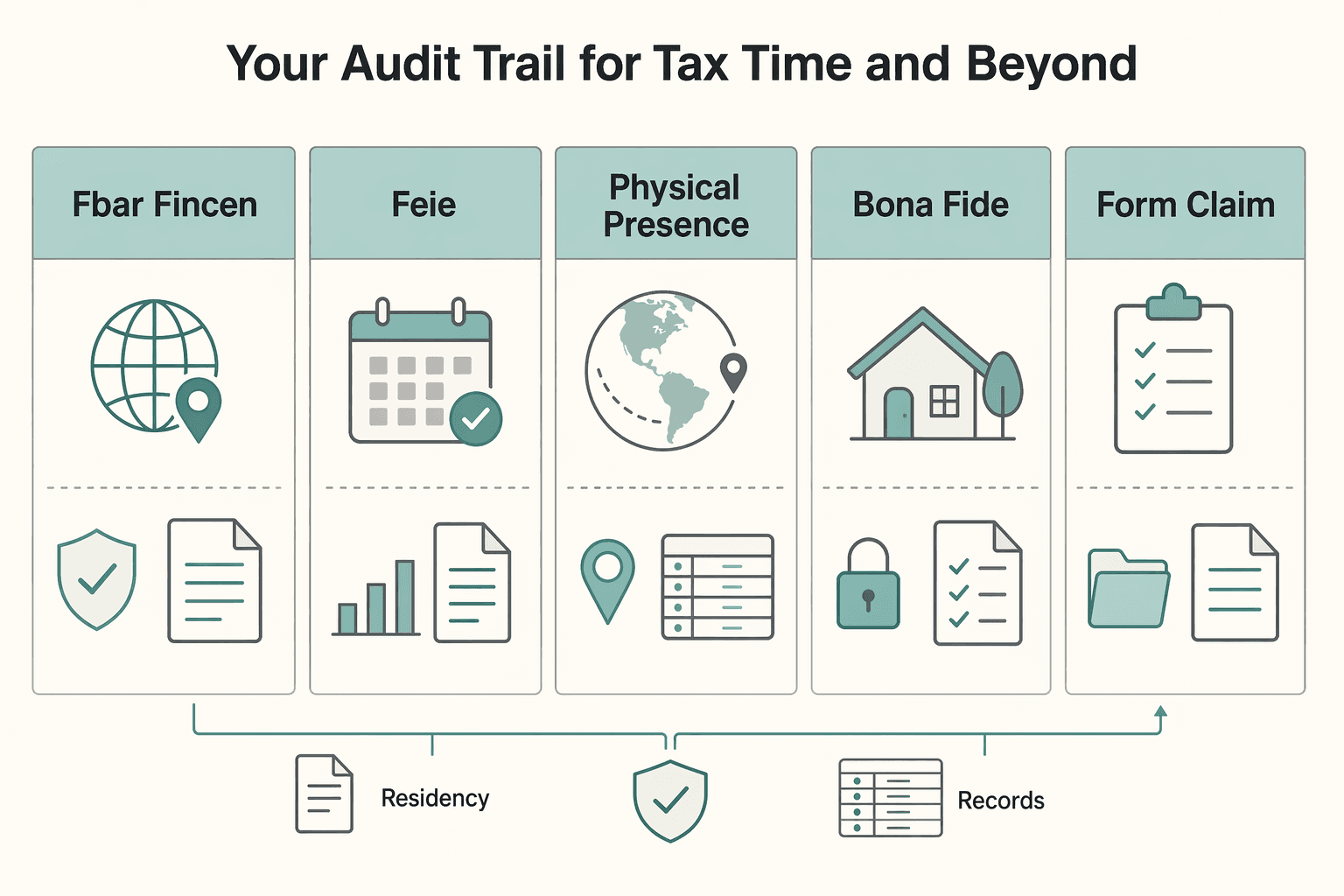

Compliance Readiness: Your Audit Trail for Tax Time & Beyond#

If you need records that hold up at tax time or during professional review, Wise is usually the stronger fit; Remitly is more useful as personal remittance history.

| U.S. term | What the article says | Key rule |

|---|---|---|

| FBAR (FinCEN Form 114) | Annual report of certain foreign financial accounts filed with Treasury through FinCEN | Trigger: verify the current aggregate-value threshold before relying on it. |

| FEIE | Potential exclusion if IRS requirements are met | Qualification paths include the physical presence test and bona fide residence test. |

| Physical presence test | 330 full days in foreign country/countries | During any 12 consecutive months. |

| Bona fide residence test | Foreign residence for an uninterrupted period | Includes an entire tax year. |

| Form to claim FEIE | Form 2555 | Attach to Form 1040 or 1040X. |

| Recordkeeping check | Wise | Remitly |

|---|---|---|

| Statement completeness | Monthly PDF statements can be auto-created on the 1st of each month, if enabled, and you can generate custom statements. | You can download transfer history by year, including transfers sent in that year across receiving countries. |

| Export range and handoff speed | Transfer lists can be exported for up to a 365-day period. Custom generated statements stay available for 30 days, so archive quickly. | You select year and file format, then download. Remitly states only the last few years are available. |

| Transaction metadata | Export filters include date, recipient, transfer type, status, direction, card, category, and currency. | History includes core fields such as transfer date, recipient name, and amount sent. |

| Fee visibility | Accounting statements can show fees separately. | No grounded source here confirms an equivalent fee breakout in exports. |

| Fit for business documentation | Generally stronger for accountant handoff and reconciliation. | Better framed as remittance records; Remitly says it is designed for family and friends, not paying for goods and services. |

Neither platform replaces tax or compliance advice. Wise says it cannot advise on your personal tax situation and tells you to speak with a qualified professional; Remitly also publishes non-advisory legal and tax language.

Platform role vs your responsibility

| Platform role | Your responsibility |

|---|---|

| Process transfers and provide transaction records or statement exports. | Determine filing triggers, keep residency evidence, aggregate accounts correctly, and file required forms on time. |

For U.S. cross-border compliance, keep the definitions tight:

- FBAR (FinCEN Form 114): Annual report of certain foreign financial accounts filed with Treasury through FinCEN. Trigger: verify the current aggregate-value threshold before relying on it.

- FEIE: Potential exclusion if IRS requirements are met; qualification paths include the physical presence test and bona fide residence test.

- Physical presence test: 330 full days in foreign country/countries during any 12 consecutive months.

- Bona fide residence test: Foreign residence for an uninterrupted period that includes an entire tax year.

- Form to claim FEIE: Attach Form 2555 to Form 1040 or 1040X.

For proof-of-income workflows such as underwriting, visa, or financing, Wise records are often easier to package because you get recurring statements, fee visibility, and structured export fields. Remitly receipts and annual history downloads can still help, but they read more like send-side remittance evidence than a primary operating-account trail.

Use this operating cadence:

- Monthly: download and archive statements and exports, and label transfers so your bookkeeper can separate income, owner draw, and family support.

- Quarterly: review possible FBAR, residency, and foreign-income filing exposure; track key deadlines, for example April 15 and the automatic FBAR extension to October 15.

- Escalate early: if your structure or cross-border activity gets more complex, involve a qualified tax professional before filing season.

For a step-by-step walkthrough, see Mercury vs. Brex: Which is Better for a Bootstrapped SaaS Business?.

The Verdict: Choosing a Utility vs. Building an Operation#

Use Remitly for personal family support, and use Wise Business when your money flow is business revenue and business records. That remains the practical split even after Remitly's U.S. business launch.

A utility is just money movement from sender to recipient. An operation includes payment intake, reconciliation, export quality, permissions, and clear separation between personal and business activity.

| Your primary job | Better fit now | Why |

|---|---|---|

| Family support transfer | Remitly (consumer) | Remitly's consumer product is centered on sending money to loved ones and remittance delivery options. |

| Client revenue collection | Wise Business | Wise Business is positioned for sending, receiving, and spending for business activity, including invoice/payment-link/card intake flows. |

| Mixed personal + business use | Separate setups | Keep accounts and controls separate. Remitly Business already enforces separation from personal profiles with a different email. |

Do not treat one transfer app as your full payment infrastructure. Transfers can be delayed by review or verification, and records may have scope limits. For example, Wise statements only include Wise currency-account transactions, so you may also need a transfer-list export, up to a 365-day window, for complete documentation. For teams, audit report download is permissioned to Admin or Admin/Owner.

Use this next-step checklist:

- Keep the tool that matches today's job: Remitly for personal support, Wise Business for business intake and records.

- Verify before relying on it: sender-country eligibility, business vs. consumer terms, verification timing, and export/report scope.

- Expand to a broader payments stack when you need repeatable intake and reconciliation, team permissions, and audit-ready documentation.

If mixed use is your pain point, read Separating Business and Personal Finances: An Important Step for LLCs. If you pay invoices through Wise, see How to Use Wise to Pay International Invoices with a US Credit Card. To confirm current coverage by country/program, Talk to Gruv.

Frequently Asked Questions

Is Wise or Remitly better for receiving large client payments?

Wise is often the better fit for receiving large client payments. It gives you local account details so a client can pay you directly from their bank. Confirm current inbound support and feature availability by region and account type before relying on it.

Which is safer for freelancers, Wise or Remitly?

The safer choice is the one that matches your real use case. If you invoice clients, use a provider with an explicit business product for paying or receiving business funds. If you mainly send family support, a remittance-focused service can fit better.

Do Wise or Remitly help with tax reporting?

No. They are payment tools, not filing systems, and they do not file for you or advise you personally. Keep documented account and transfer records, and verify any filing trigger with the current IRS or FinCEN threshold instead of a remembered app number.

Can I use Remitly for business invoices?

Yes, but only through the business product and only where your sender country and account are eligible. Use Remitly Business for paying freelancers, contractors, vendors, or teams if its corridor coverage works for your outbound payments. Do not assume a consumer Remitly account is suitable for goods or services.

What are the main differences between a Wise Business and a personal account?

The main difference is operational fit. Wise Business is for business onboarding and accounting connections, including direct setup with Xero and QuickBooks from within Wise. Business support is country-dependent, and some features vary by region.

Are there alternatives to Wise and Remitly designed specifically for freelancers?

Yes, but evaluate alternatives by job fit rather than by name. Check receiving rails, invoicing fit, reconciliation workflow, and compliance burden. If you mainly send family support, prioritize corridor-specific delivery methods such as bank deposit or cash and verify those options for your destination.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- bsaefiling.fincen.gov/resources/FinCENFBARHelp.pdftrusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- wise.com/help/articles/2960247/connecting-your-wise-a...trusted

- wise.com/help/articles/2736049/how-do-i-download-a-st...trusted

- remitly.com/us/en/landing/businessexternal

- remitly.com/us/en/help/article/receiving-money-optionsexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

The Best Way to Send Money to the Philippines from the US

If you need to **send money to philippines from us** on any regular basis, start with one number: how many Philippine pesos actually reach the recipient. The visible transfer fee matters, but it is only part of the cost. The World Bank is clear that remittance pricing is hard to compare because both fees and exchange rate margin shape the final result.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.