Quick Answer

Act fast: treat a wise account under review as a documented incident, not a guess. Log the exact in-app notice, check Home activity tasks, and verify whether the transfer’s estimated delivery window has actually elapsed on working-day timing. When that window is exceeded, stop repeating screen checks and request proof of payment showing sender and recipient details, date, amount, and currency. Keep screenshots, emails, and support replies in one record so every follow-up is consistent.

Start here if your Wise account is under review#

If your Wise account is under review and payments are affected, treat it as a cashflow problem first, not just a status label. Focus on what you can verify, document it, and keep operations moving while the review is active.

One scope limit matters up front: precise details about review triggers, timelines, blocked features, or required document flows may vary. Where details are unknown, this guide says so plainly.

Start with a clean record before you do anything else:

- Capture the exact notice shown in your account and when you saw it.

- Note your last successful account activity and any related email subject line or reference number.

- Separate urgent commitments in the next few business days from items that can wait.

- Save screenshots, emails, and support replies in one place so you can track one consistent timeline.

If you are already stressed, do not skip this logging step. A review gets harder to manage when the facts are spread across inboxes, chat messages, and half-remembered screen states. You want one timeline you can reuse in every reply instead of rebuilding the story each time someone asks what happened first.

For platform-specific action, rely on your in-account notices and the Wise Help Centre. If a detail is not confirmed there, do not treat it as confirmed. From there, decide whether the issue appears limited to a single transfer or broader account access.

You might also find this useful: A Guide to US Corporate Bank Account Options for Foreign Founders.

Identify your exact Wise status before you act#

Do not act on assumptions. Classify the issue by what you can prove in your account so your next step matches what is actually happening. Use these labels as working shorthand, not official Wise definitions:

- Transfer paused: one transfer appears delayed, pending, or under review.

- Account suspension: the issue appears account-level, not limited to one transfer.

- Account closure: the notice suggests the account relationship is ending.

| Working label | Plain-language meaning | What still works | What is blocked | Next required action |

|---|---|---|---|---|

| Transfer paused | One transfer is delayed, pending, or under review | Verify directly in-app | Do not assume account-wide impact | Start with that transfer record and the exact notice text |

| Account suspension | The issue appears to affect the account overall | Check each area in-product | Document every blocked action | Capture the exact notice language and follow in-app instructions |

| Account closure | The notice suggests Wise is ending the account relationship | Verify in-app | Verify in-app | Save the notice and proceed only from Wise-stated instructions |

Treat your label as provisional until you have the exact in-app notice language.

For verification, prefer concrete in-app checks over memory. One documented in-app path in the sources is Card tab -> Your spending limits. Wise also says View ATM fees shows your free allowance and reset timing. That does not define review status, but it gives you a reliable checkpoint for what you can currently access.

Avoid "testing" account health with extra paid actions. Wise says ATM costs depend on both withdrawal count and amount, including 2 free withdrawals or up to 200 EUR per calendar month, then a fixed fee from the third withdrawal onward. Wise also says fees can change over time.

If you are unsure whether the problem is broad or narrow, write down each function you actually tested and the result. "Card tab opens," "Your spending limits page loads," or "View ATM fees shows allowance/reset timing" is more useful than a vague note like "account seems blocked." You want a record of observed facts, not guesses about why they happened.

At this stage, keep the goal simple. Name the issue narrowly, verify only what you can confirm in-product, and log facts you can prove.

For a step-by-step walkthrough, see A Guide to Using Wise for Large International Money Transfers.

Run first-hour checks in the right order#

In the first hour, order matters more than speed. Check timing first, clear in-app tasks next, then verify sender-side details. If you skip the sequence, you will likely repeat checks that cannot change yet.

Check timing before you assume a hold#

Start with the transfer's estimated delivery time as your baseline. Confirm the send date and time, then count only working days, since Wise processes most transfers on working days and estimates use Monday to Friday.

| Item | What to check | Timing |

|---|---|---|

| Estimated delivery time | Use it as the baseline before assuming a hold | Confirm whether it has passed |

| Working days | Count working days only | Monday to Friday |

| Bank-transfer funding | Time to reach Wise | 1 to 4 working days |

| Outside-bank Swift or wire transfers | Time to reach Wise | 2 to 6 working days |

Use this order:

- Confirm the original send date and time.

- Count working days only.

- Check whether the estimate has actually passed.

- Only then move to deeper checks.

Keep the payment rail in mind while you do this. Wise says bank-transfer funding can take 1 to 4 working days to reach Wise, and outside-bank Swift or wire transfers can take 2 to 6 working days to reach Wise.

This check can rule out false alarms. If the estimate has not passed, you may not have a review problem yet. If it has passed, you now have a clear reason to move from watching to collecting evidence. Make a note of the exact time you concluded the estimate was exceeded so later follow-ups stay consistent.

Clear account-side prompts in Home first#

Once timing is clear, go to Home and check the activity list, pending tasks, and notifications. Wise says transfers may be paused while it asks for more information, so this is the first in-account checkpoint that can actually move the case forward.

Prioritize any identity prompt, extra security check, or source-of-funds request. Complete those before opening a new support thread. Wise also says extra security checks cannot be sped up through support. Also check for receiving-limit warnings. Wise states that if a payment goes over a limit, it may be refunded.

Do not clear one request and assume the case is moving. If there are multiple prompts, finish all of them and capture what you submitted. A simple screenshot before and after upload can save time later if you need to show that the request was completed.

Verify sender-side facts, not just "we sent it"#

If your side is clear, verify what the sender actually did. Ask whether they sent with Wise or from an outside bank.

If they used Wise, ask for the Tracking link so you can see where the transfer is. Then confirm the beneficiary details they used. Wrong details can cause rejection and return, and name typos can matter for some currencies, including JPY.

When you ask the sender for confirmation, ask for specifics in one message so you do not lose another day to back-and-forth. You want the amount, currency, send date, estimated delivery time, and payment route they used. "We sent it yesterday" is not enough to reconcile anything.

If the estimate has passed, switch to evidence collection#

If the estimated delivery time has passed after those checks, stop rechecking the same screens and collect Proof of payment. Ask the sender for a bank document that includes:

- sender's name and account details

- date and amount

- currency

This is the document Wise asks for to help trace missing funds.

At this point, your job changes from monitoring to documentation. Mark the transfer as "awaiting trace evidence" in your own log. Save the document when it arrives, and keep it attached to the same case timeline as the original notice and any Home prompts you completed.

For related context, see How to Determine the 'Maximum Value' of a Foreign Bank Account for the FBAR.

Build the document pack once and submit cleanly#

If follow-up is needed, send one complete packet in one thread instead of a series of partial updates. The sources here do not show a single universal review checklist, so use this as an organization method and prioritize any case-specific request shown in your Wise account or the Wise Help Centre.

A fragmented submission creates avoidable back-and-forth. Aim for one bundle that shows what happened and how each item ties to the same transfer or card event.

What to assemble before upload#

- Spending limits capture: in app, go to Card -> Your spending limits; on web, go to Card and open spending limits. Capture the view that shows daily and monthly ATM limits and refresh timing.

- ATM fees capture: select View ATM fees so the free withdrawal allowance and reset timing are visible.

- Transfer confirmation (if pricing or conversion is part of the issue): include the confirmation view that shows the upfront fee and exchange-rate breakdown.

- Any case-specific support request: include the exact message tied to your case, if one was provided.

For ATM limits and fees, do not assume one global threshold. Wise shows context-specific figures, and says exact fees depend on where your card was issued.

Common artifacts and purpose#

| Artifact type | What it helps clarify | Pre-send check |

|---|---|---|

| Spending limits screen | Current daily/monthly ATM limits and when they refresh | Captured from the Card spending-limits path |

| View ATM fees screen | Free withdrawal allowance and reset timing | Allowance and reset timing are visible |

| Transfer confirmation | Upfront fee and exchange-rate breakdown shown before confirmation | Fee and rate are visible in the same capture |

| Region/context note (if needed) | Why numeric limits can differ by account/location | Confirm the account/card-issuance context before applying thresholds |

Before sending, do a quick quality check so each file is readable and clearly mapped to the same case. Share only what is needed for that case.

If you later need to escalate, this same packet becomes your handoff bundle. That is why it is worth assembling carefully the first time instead of sending screenshots one by one as the stress rises. If you need background on identity checks, see KYC.

Understand what is blocked during suspension and closure#

If the issue moves to Account suspension, plan for meaningful limits on money movement while Wise performs its compliance check.

| Case | What Wise says | Timing |

|---|---|---|

| Suspension | Cannot add money to the account | During suspension |

| Suspension | Cannot receive money into the account | During suspension |

| Suspension | Cannot pay bills using Direct Debits; existing Direct Debits are cancelled | During suspension |

| Closure | Usually have 90 days from the first closure email to move money out | Before full closure |

| After full closure | Cannot log in; pending transfers are cancelled | After the account is fully closed |

| Cancelled transfer return: bank or wire | Return timing depends on the original payment rail | 2-3 working days |

| Cancelled transfer return: card | Return timing depends on the original payment rail | 3-10 working days |

| Cancelled transfer return: bank debit or ACH | Return timing depends on the original payment rail | Up to 90 working days while due diligence checks are carried out |

Move cashflow away from that account right away so incoming payments and auto-pulled bills do not fail. That means checking more than customer payments. Review any routine bill collections, subscriptions, or internal payment habits tied to that route so you are not surprised by a failed debit after you thought you had handled the main issue.

Account closure is different. Wise says it will email the date your account will be fully closed, and you usually have 90 days from the first closure email to move money out. After full closure, you cannot log in, and Wise says pending transfers are cancelled when it closes an account.

If pending transfers are cancelled, return timing depends on the original payment rail:

- 2-3 working days for bank or wire transfer

- 3-10 working days for card

- Up to 90 working days for bank debit or ACH while due diligence checks are carried out

Wise may not provide a specific closure reason, and support may not be able to view it. In practice, focus on the closure email details, your remaining balance, cancelled transfers, and any appeal deadline. An appeal does not automatically change the decision.

Related reading: Wise vs. Remitly: Which is Better for Sending Money to Family Abroad?.

Escalate and appeal without losing your position#

Escalate in sequence, not by volume. A review is easier for the next person to assess when your record is complete, consistent, and easy to follow.

The excerpts here do not confirm Wise's full escalation ladder, required attachments, or appeal timelines. If you already have an open support thread, answer open requests there before starting a new escalation. If a notice explicitly offers a reconsideration route, use it instead of opening a duplicate case.

When you escalate, make the handoff fast for the next reviewer. Include concise context such as:

- Case ID or reference number (if available)

- A short timeline of key dates and prior replies

- Relevant status screenshots or documents you already submitted

- One clear ask, such as confirming receipt or requesting a review

Keep the ask narrow. "Please confirm whether the uploaded document is sufficient for review" is easier to handle than a long message that mixes complaints, speculation, and three different requests. A concise escalation does not minimize the problem. It makes your file easier to move forward.

Treat appeal or reconsideration outcomes as uncertain. If direct support is exhausted and you are dealing with Wise US Inc., the BBB page shows a Submit a Complaint channel. Use it to document escalation, not to predict outcome, and keep in mind BBB notes that published complaint text may be incomplete.

Keep client cashflow moving while review is open#

When receipts are disrupted, the immediate job is cashflow control. Keep money moving in and out with a clear plan for the current period.

Build one live tracker with expected inflows, essential outflows, amounts, due dates, payment method, and status. Cashflow management works when you track and analyze all money in and out, and one common risk is a timing mismatch between delayed collections and scheduled payments.

A simple tracker is enough if it answers three questions quickly: what is due soon, what is already at risk, and what you can reroute now without creating reconciliation problems later. The point is not perfect forecasting. It is preventing avoidable missed payments while the review stays open.

Split actions into now and next#

Now#

- Pause new intake to the affected route if you cannot confirm normal receipt.

- Notify clients with open invoices before they send payment.

- Route urgent receivables to a backup route or account you already use and can reconcile.

Next#

- Update payment instructions only where routing actually changed.

- Reconcile payments already sent so you can separate late payments from missing ones.

- Keep one status log with payer, amount, invoice, payment method, send date, and payment proof or reference.

- Prefer electronic invoicing where possible, since it can reduce payment time versus paper invoicing.

A useful operational split is this: for invoices not yet paid, decide whether to reroute or pause; for payments already sent, investigate and document rather than changing instructions midstream. Mixing those two groups can make it harder to tell which money is delayed and which payments were redirected.

Tell clients what changed and what did not#

Keep client messages short and specific:

- What happened

- What is unchanged on your side, such as delivery plan and contact channel

- Whether to pay now with updated instructions or hold payment briefly

- When you will send the next status update

Example: "We are handling a temporary review on one payment collection route. Delivery and communication are unchanged. For invoice your invoice number, please use the updated payment details or hold payment until confirmation. I will send the next update by the agreed update time."

That structure can reduce back-and-forth by making the pay-now, hold, or update decision clear.

Avoid adding extra collection routes unless you can keep records and reconciliation clear in the same tracker.

If you want a deeper dive, read Canada's Digital Nomad Stream: How to Live and Work in Canada.

Reduce repeat reviews with cleaner account behavior#

The best prevention is clarity. Keep your account activity easy to understand, with consistent names, clear payment purpose, and records that match your stated account use.

A verified account helps, but it is not immunity from review. Reviews can still happen, and Wise may ask for more documents or restrict certain actions if activity looks unusual as part of ongoing AML controls.

Make verification checks easy to pass twice#

Repeat friction often comes from avoidable mismatches. Keep your profile name, invoice name, payer records, and submitted ID details consistent every time.

Before a new client pays, confirm:

- the exact payer name you expect

- the reference format you want used

- purpose wording that matches the invoice

Keep a standing document set ready for follow-up requests. Include:

- current government ID

- proof of address (if requested)

- short description of intended account use

- recent invoices or payment context

- business tax ID and payment information that match your books (if you operate as a business)

Think of this as reducing explainable confusion. If the payer name on the transfer, the invoice name in your records, and the identity details on file all line up, you have fewer moving parts to explain if questions come later.

Separate flows so your records tell one story#

Separate business and personal flows to reduce audit friction on your side. Cleaner books and cleaner naming can make activity easier to explain if a review happens.

Mixed records can create costly delays, especially when manual data entry is involved. Align account naming with bookkeeping categories, and keep the same verification discipline you use in vendor onboarding. That includes payment information and tax IDs before normal operations. If you need a deeper reset, read Separating Business and Personal Finances: A Important Step for LLCs.

A good test is whether an outsider could understand the purpose of a payment from your records without asking you for background. If not, the activity may still be legitimate, but it is harder to review quickly.

Recheck policy when your activity changes#

When your client mix or transfer pattern changes, recheck your account setup and documentation before the new pattern becomes routine.

You do not need constant review. You do need to revisit your records when your activity starts looking materially different from your earlier history or intended use. The tradeoff is straightforward: tighter documentation takes more admin time now, but it may cost less than another avoidable review later.

Use a weekly payment risk checklist before invoices go out#

A short weekly checklist is more useful than a rushed fix after funds go missing. Before you send high-priority invoices, make sure identity details, transfer details, and escalation steps are clear. If payer identity, recipient details, or transfer reference is unclear, pause and fix it first.

Check identities before you issue the invoice#

For priority invoices, confirm in one pass:

- the payer legal entity

- the intended recipient details

- the transfer reference format the client should use

In Wise's structure, Profile, Recipient, and Transfer are separate records. Keep your notes the same way so account ownership, beneficiary, and payment creation details do not get mixed together.

If you use a primary payment route and fallback route internally, define both before the due date and record who can approve a route change.

This matters most when a client pays through a team member who is not the contracting entity, or when the name you see in email differs from the name that should appear on the transfer. Resolve that mismatch before the invoice goes out, not after money is already in motion.

Build the investigation pack before anything goes wrong#

Pre-collect what you would need if funds do not arrive. Include:

- payer entity name and contact

- invoice number

- expected transfer reference

- tracking-link ownership path, if available, including who created it, who received it, and where it was shared

If a payment-related link arrives by email, verify it goes to a URL that starts with https://wise.com before anyone logs in. Wise notes a limited research exception for approved secure third-party websites. You can also use a secure communication code as an extra signal, but missing code alone is not definitive because some genuine Wise emails may not include it. If anyone clicked a suspicious link or shared sensitive data, contact Wise support immediately.

You are effectively prebuilding your first response. When a payment goes missing, response quality usually depends on whether these basic details were gathered before the invoice was sent.

Set trigger points now, not in a panic#

Define internal triggers now so your response stays consistent. Wise materials here do not provide exact thresholds or guaranteed review timelines for when to request proof of payment, open a case, or start a refund request, so treat these as internal policy choices:

- request Proof of payment when a client says funds were sent but you cannot match the transfer details

- open a case when available details still do not reconcile

- use a Refund request path when both sides agree the payment should be unwound instead of traced further

The goal is a fast, documented first response, not perfect prediction. Write these trigger points in the same place as your invoice process, not in a separate emergency note nobody checks. The right move should be obvious when the problem starts, especially if someone else may need to pick up the case.

This pairs well with our guide on How to Use Wise to Pay International Invoices with a US Credit Card.

If you want a backup rail ready before the next invoice cycle, review options such as Virtual Accounts.

Apply Gruv-style controls even if you are a team of one#

Even if you work solo, act like every payout or receipt may need to be explained later. Aim for one ledger view, one status history, and one retry record.

A practical model is to separate records from audit controls. Wisconsin Chapter 601 names 601.46 (records and reports), 601.85 (accounting, reports, and audits), 601.64 (enforcement procedure), and 601.935 (penalties), and it frames self-regulation as a purpose. This does not mean those insurance rules govern your Wise account. The point is simpler: if an event is important enough to move money, it should leave a clear trail.

Keep three lightweight artifacts#

You do not need heavy tooling. One lightweight approach is to keep these updated for each transfer event:

| Artifact | Keep in it | What it answers |

|---|---|---|

| Ledger export | date, payer, recipient, amount, currency, reference, rail, and current status | What should have happened |

| Status log | dated updates such as proof requested, sender confirmed, review notice received, or refund requested | What did happen |

| Retry log | what was retried, why, and what changed before the next attempt | What changed between attempts |

Use one quick test: can you trace a transfer from invoice to recipient to current status quickly without checking multiple apps? If not, your records are fragmented.

The value of these three artifacts is that each answers a different question. The ledger tells you what should have happened, the status log tells you what did happen, and the retry log tells you what changed between attempts. When those are mixed together, small delays become hard to explain.

Add policy gates before money gets sensitive#

Set one approval rule now, even if the approver is future-you. For example, require a second review for any new recipient, changed bank detail, unusually large payout, or rushed exception against the invoice, recipient record, and prior communication.

The common failure is not lack of effort. It is scattered evidence. During a provider follow-up or compliance review, fragmented screenshots and partial notes make routine payments harder to explain. If you grow into a small team, replace ad hoc chats with named approvals and one evidence pack per case: request notice, transaction details, submitted files, timestamps, and final approver.

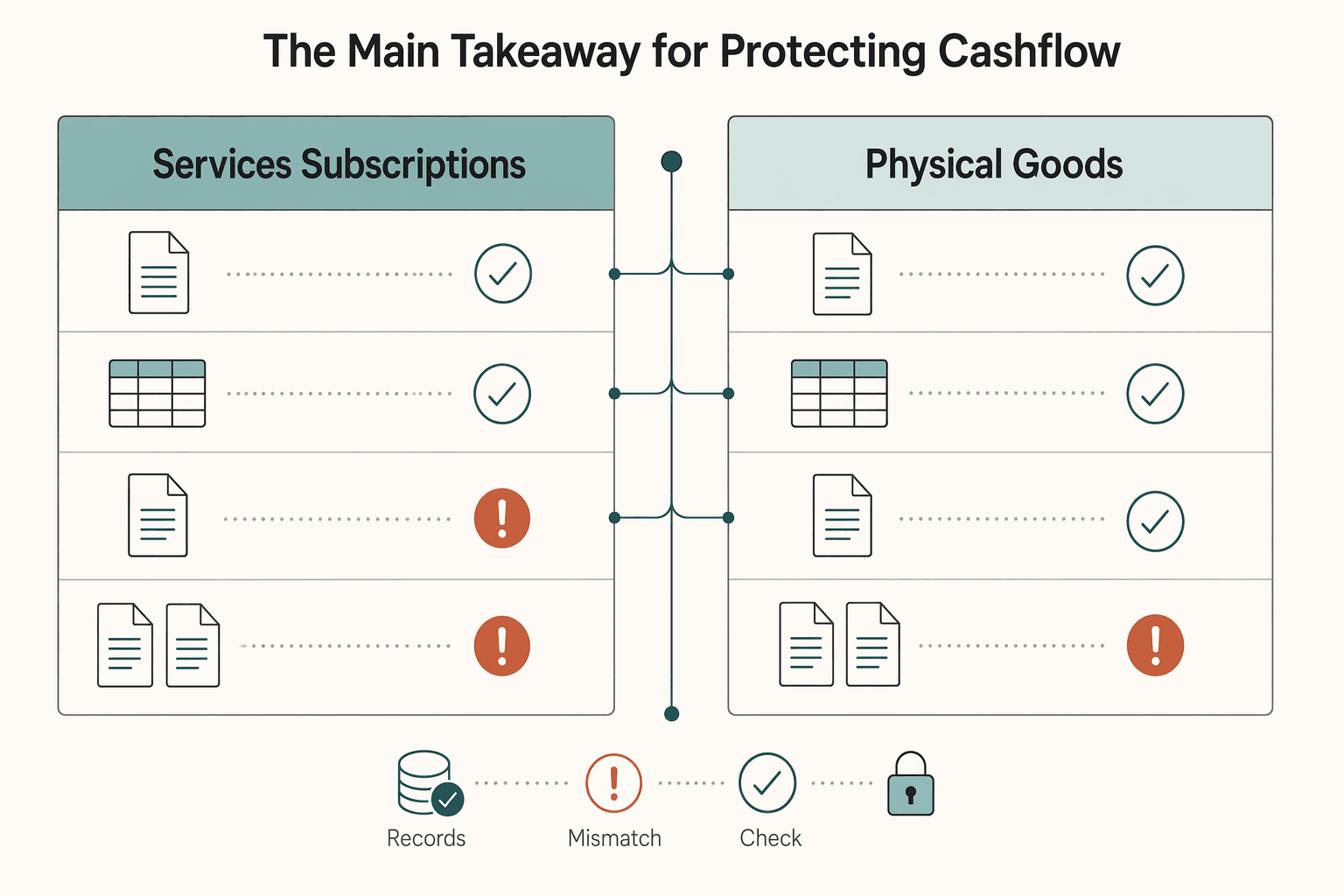

The main takeaway for protecting cashflow#

Speed helps, but sequence protects cashflow. When payments are disrupted, fall back to the same order every time: gather documents, validate payment details, verify goods received when relevant, and investigate discrepancies before payment.

Make this a repeatable operating habit, not a one-off crisis response. Use pre-payment reconciliation checks before money moves: does the invoice match your internal record, and do supplier details, including VAT and bank information, align across documents?

Use invoice reconciliation as your pre-payment control. It helps prevent overpayments and keeps the audit trail clear.

| Situation | Matching depth |

|---|---|

| Services or subscriptions | 2-way matching (Invoice + PO) |

| Physical goods or high-value items | 3-way matching (Invoice + PO + Delivery Note) |

Keep the core artifacts together every cycle: invoice, purchase order, and the bank statement entry once payment lands or goes out. If goods are involved, include the delivery note. If something does not line up, fix the mismatch before payment.

Manual reconciliation can work at low volume, but it becomes more error-prone as volume grows. Before your next invoice batch, implement a weekly checklist so reconciliation stays consistent as volume increases. Need the full breakdown? Read Transaction Monitoring for High-Risk Payments That Protects Cashflow. When this process becomes part of weekly operations, run disbursements with clearer status tracking and controls through Gruv Payouts.

Frequently Asked Questions

Why is my Wise account under review?

An account under review can mean Wise has paused a transfer to ask for more information, or that there is an account decision to review. It is not always an account-wide issue, because delays can also come from working-day timing, holidays, time zones, recipient-detail errors, receiving limits, or regulatory cancellation. Start by confirming whether you are dealing with a transfer delay or an account decision.

What should I check first in my Wise account?

Check your Home Activity list first for pending tasks or notifications. Then confirm timing basics like weekends, holidays, time zone differences, and whether the expected delivery window has actually passed. If money is incoming, also check whether a receiving limit may have triggered a refund.

What can I not do while my account is suspended?

The material here does not confirm a full feature-by-feature list of what is restricted during suspension. Use your in-app notice and Wise email as the source of truth for what is currently restricted on your account.

What document should I request from a sender when money has not arrived?

If the sender used Wise, ask for the tracking link first so you can see where the money is. If the estimated delivery time has passed, ask for proof of payment and share it with Wise. It should include sender and recipient details, plus the date, amount, and currency.

Can Wise close my account without giving a specific reason?

The provided Help Centre pages confirm Wise can close an account, be about to close it, or deny an application, and that these decisions can be appealed. They do not state that Wise will always give a detailed reason in every case. Keep the deactivation email and in-account notice as your main record.

Can I appeal a Wise suspension or closure?

Yes, for account decisions covered in Wise Help Centre. If Wise has closed your account, is about to close it, or denied your application, you can appeal through the in-account Appeal our decision link or the self-service appeals page. For Wise Business, only the account Owner can use self-service, and Wise says to reply to the deactivation email if self-service does not work.

How long does a Wise account review usually take?

Wise does not provide a standard or guaranteed review timeline in the material used here. Keep review timing separate from transfer-rail timing, since an outside-bank Swift or wire transfer can take 2-6 working days to reach Wise. If that window has passed, move to proof of payment and case details instead of waiting without new information.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- congress.gov/108/plaws/publ375/PLAW-108publ375.pdftrusted

- congress.gov/104/plaws/publ134/PLAW-104publ134.pdftrusted

- dcf.wisconsin.gov/files/cwportal/policy/pdf/access-ia-standard...trusted

- doas.ga.gov/sites/default/files/assets/State%20Purchasin...trusted

- docs.legis.wisconsin.gov/document/statutes/601.pdftrusted

- education.ky.gov/CTE/cter/Documents/22-23_CTE_POS.pdftrusted

- enisa.europa.eu/sites/default/files/2024-11/Remote%20ID%20Pr...trusted

- faa.gov/documentlibrary/media/advisory_circular/ac_6...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

Canada Digital Nomad Visa Planning for Visitor Status and Work Permits

The phrase `canada digital nomad visa` is useful for search, but misleading if you treat it like a legal category. It is shorthand for existing Canadian status options, mainly visitor status and work permit rules, not a standalone visa stream with its own fixed process. That difference is not just technical. It changes how you should plan the trip, describe your purpose at entry, and organize your records before you leave.

KYC KYB CIP Explained for Cross-Border Freelancers and Small Teams

Choose your onboarding lane first: **individual** or **entity**. Then keep your profile, invoice identity, and payout account in that same lane so checks can clear without avoidable follow-up.