Quick Answer

Start by confirming whether the payee is U.S. or foreign, then request the matching form and keep payment setup incomplete until tax intake is done. If a client refuses to sign w-9 after clarification, move to formal escalation and apply backup withholding on affected reportable payments as required. Maintain one record trail of requests, replies, and notices, then complete reporting with verified information instead of filling gaps with assumptions.

A payee refusing to provide a Form W-9 can create immediate friction, especially when everything else in the engagement is moving smoothly. It is still manageable if you treat it as an operations issue, not a personal standoff. The goal is to stay clear, consistent, and compliant without turning a routine document request into a drawn-out dispute.

This three-phase approach moves from prevention to intervention to execution. Used consistently, it reduces confusion, protects your process, and leaves you with a clean record if the file is ever reviewed.

Phase 1: Prevention Through Bulletproof Onboarding#

Prevention starts with clear gates in onboarding: confirm payee status first, request the correct form second, and treat missing tax intake as incomplete setup until you resolve it. That helps keep a late-stage W-9 issue from turning into a payment problem.

Verify status before you request any form#

Do not send a W-9 by default. Start by classifying the payee, then request the form that matches that status.

Use a short intake checkpoint before you request any form:

- Legal name

- Individual or entity

- U.S. person or foreign person

- Country tied to tax status

Then compare that intake against the contract party name and payment beneficiary details. If those records do not line up, pause setup and resolve the classification before payment.

| Form | When you use it | Who should not receive it | Common misclassification risk | Requirement note |

|---|---|---|---|---|

| Form W-9 | Request a TIN from a U.S. person, including a resident alien | Foreign individuals and foreign entities | Treating a non-U.S. payee as U.S. and collecting the wrong form | Best practice: request after status verification |

| Form W-8BEN | Document foreign status for a foreign individual | U.S. persons and foreign entities | Sending it to a foreign company instead of an individual | Best practice: request after status verification |

| Form W-8BEN-E | Document foreign entity status | Individuals, including foreign individuals | Accepting it from an individual when it is for entities | Best practice: request after status verification |

Put the tax-document requirement in your agreement and onboarding flow#

This works best when the requirement shows up early and in the same places every time. Put it in your services agreement, onboarding checklist, and vendor setup communication so it feels routine rather than confrontational.

Use this checklist:

- State in your agreement that required tax and payment documents must be provided for invoice processing and reporting.

- After signature, run intake first and then request the correct tax form based on verified status.

- Do not finalize payee setup or payment readiness while required tax intake is incomplete.

- If intake is still incomplete, mark onboarding incomplete and escalate to your finance or compliance owner.

- If a TIN is missing on reportable payments subject to backup withholding, begin backup withholding immediately at the current rate of 24%.

Use a concrete onboarding sequence#

You do not need complicated tooling here. What matters is a sequence your team follows every time.

| Step | Action | Trigger or note |

|---|---|---|

| Intake form | Collect status fields first: U.S. versus foreign, individual versus entity, legal name, country, and payment contact | Do this before any form request |

| Secure document collection | Request and receive the correct form through a secure channel | The payee gives the form to you as payer or requester, not to the IRS |

| Follow-up trigger | Send a short reminder tied to payment readiness | Use it if the form is missing by the deadline |

| Escalation handoff | Hand the file off for a payment hold or classification decision | Do this before funds are released if it is still missing |

- Intake form

Collect status fields first: U.S. versus foreign, individual versus entity, legal name, country, and payment contact.

- Secure document collection

Request and receive the correct form through a secure channel. The payee gives the form to you as payer or requester, not to the IRS.

- Follow-up trigger

If the form is missing by the deadline, send a short reminder tied to payment readiness.

- Escalation handoff

If it is still missing, hand the file off for a payment hold or classification decision before funds are released.

Script you can adapt:

To complete vendor setup, we need to confirm your tax status and collect the correct tax form for our records. If you are a U.S. person, please return Form W-9. If you are a foreign individual, we will request Form W-8BEN, and if you are a foreign entity, Form W-8BEN-E. We cannot finalize payment setup until this step is complete.

Add one verification checkpoint before filing season#

For U.S. payees, check name and TIN consistency before filing season instead of waiting for downstream errors. If you are eligible to use it, IRS TIN Matching can serve as a preventive check before information returns are filed.

Keep a compact record for each onboarded payee: intake responses, agreement, received form, date received, and follow-up trail. That helps show you classified early, requested the right document, and handled missing information consistently.

Phase 2: Intervention With a De-escalation Playbook#

Once prevention fails, use a short, neutral sequence: clarify first, explain the compliance impact second, and send a final notice only if needed. Treat this as process management, not a negotiation about process steps.

| Tier | Objective | Channel | Message focus |

|---|---|---|---|

| Tier 1 | Resolve confusion and get the correct document request back on track | Written message in your normal onboarding thread | Confirm whether the payee is a U.S. person or a foreign payee so you can request the correct tax form |

| Tier 2 | Explain that missing tax intake can affect payment and reporting handling | Written follow-up, then an optional short call if they seem uncertain | This is a compliance step tied to payment and reporting, not a discretionary policy |

| Tier 3 | Give a clear last checkpoint and document your handling | Formal written notice in the primary contract or onboarding thread | State that completed tax intake is still needed and that you will proceed under the documented compliance process if it is not received by your stated deadline |

Pre-check: confirm payee type before escalation#

Before you escalate, confirm whether the payee is a U.S. person or a foreign payee. If they are foreign, pause the W-9 track and route them through your documented foreign-payee process so you do not keep requesting the wrong form.

Tier 1: Clarify misunderstanding#

Start by assuming the issue may be confusion, not refusal.

- Objective: resolve confusion and get the correct document request back on track.

- Recommended channel: written message in your normal onboarding thread.

- Message blueprint:

We may be solving the wrong problem. Please confirm whether you are a U.S. person or a foreign payee so we can request the correct tax form and complete setup.

Tier 2: Explain compliance consequences (neutral tone)#

If the first step does not resolve it, explain the operational consequence without sounding punitive.

- Objective: explain that missing tax intake can affect payment and reporting handling.

- Recommended channel: written follow-up, then an optional short call if they seem uncertain.

- Message blueprint:

This is a compliance step tied to payment and reporting, not a discretionary policy. If required tax details remain incomplete, we may need to apply our documented compliance process for reportable payments.

Keep the tone neutral. You are describing the process impact, not threatening the payee.

What to avoid saying:

- "We're punishing you."

- "This is negotiable if you pay fast."

- "We can ignore it this time."

- "Legal says you have no choice" (unless counsel-approved wording is verified).

Tier 3: Final compliance notice#

When the issue is still unresolved, send one clear final notice and make sure the file shows you handled it in good faith.

- Objective: give a clear last checkpoint and document your handling.

- Recommended channel: formal written notice in the primary contract or onboarding thread.

- Message blueprint:

Final notice: we still need completed tax intake to finalize compliant payment and reporting handling. If we do not receive it by your stated deadline, we will proceed under our documented compliance process.

Audit-ready documentation checklist#

At every tier, log the same core details:

- Date and time

- Sender

- Channel used

- Exact message text sent

- Client response, or no response

- Current status decision: continue, reroute, or escalate

Store records in one secure location used for compliance files, and handle sensitive information only through official, secure websites or other approved secure systems. Where possible, confirm receipt or acknowledgment through a reply, portal confirmation, or timestamped delivery record so your file shows what was sent, when, and whether it was received.

Related: The Complete Guide to Form W-9 for Independent Contractors.

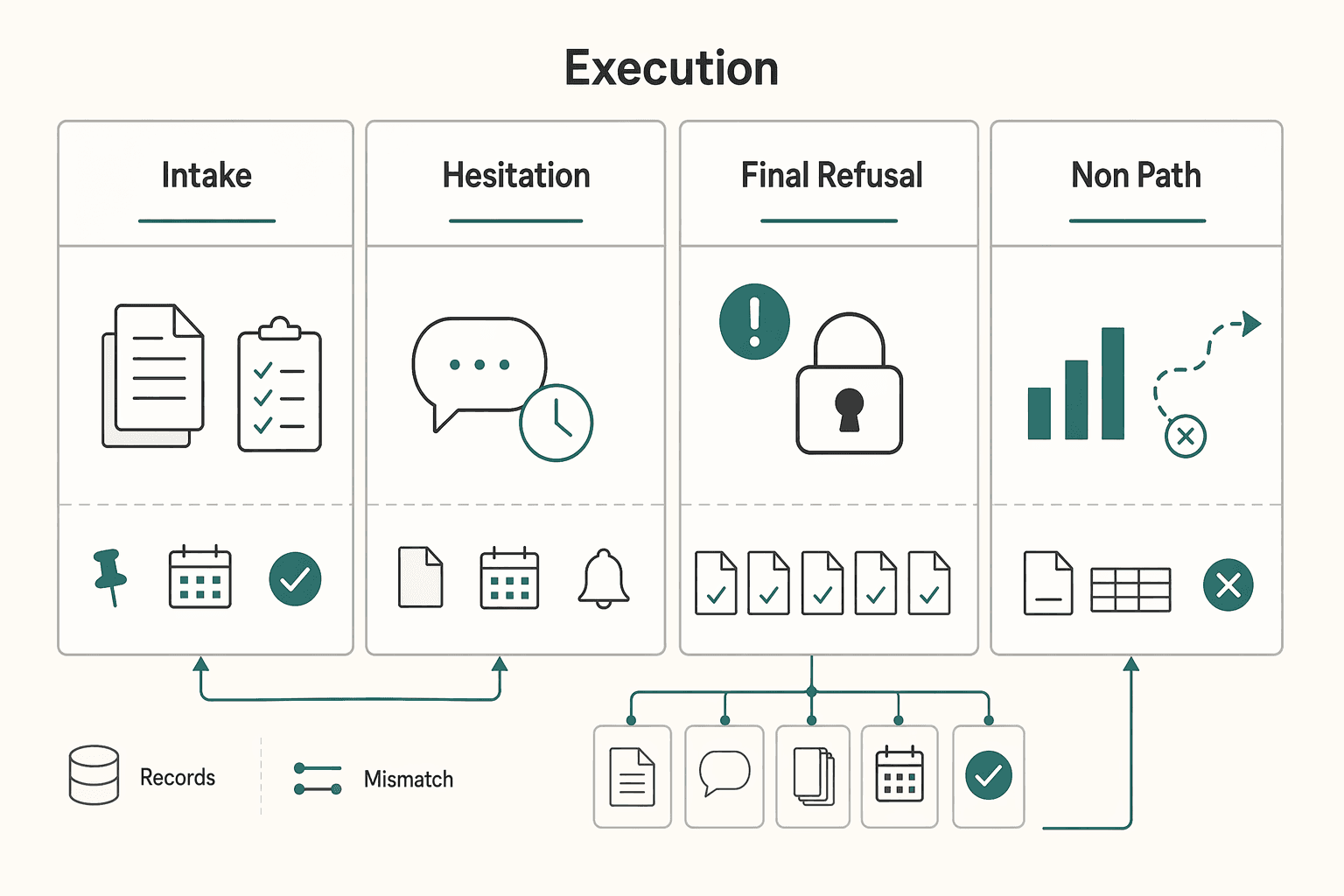

Phase 3: Execution of Your Final Compliance Duties#

Once the refusal is final, stop trying to persuade and start executing. The file should show four things clearly: what triggered the decision, how payments were handled, how reporting was handled, and what records you kept.

1) Trigger event: start the process immediately#

If the payee is a U.S. person and no TIN is provided, or the TIN is clearly incorrect, treat that as an immediate backup withholding trigger on reportable payments. Do not wait until year-end, and do not keep paying in full once the trigger is clear.

Before processing the next payment, confirm your file shows:

- Initial TIN solicitation at account opening or transaction time

- Follow-up solicitation history, including annual solicitations when required

- Any final notice you sent and the date sent

If a TIN is later provided but still looks questionable, run IRS TIN Matching when available for your filing setup. That can help prevent later mismatch notices such as CP2100 or CP2100A.

2) Payment handling: apply withholding consistently#

When withholding is required, consistency matters as much as timing. For each affected reportable payment, calculate from gross, withhold at the current IRS rate of 24%, and pay the net amount. Treat withheld funds as federal income tax withholding, not a fee adjustment.

Use one consistent status note in your vendor and invoice records, for example: TIN missing/invalid; backup withholding started the start date. That kind of consistency helps during internal review and at year-end.

| Scenario | Gross payment | Payment before trigger | Payment after trigger | What you do now | Common execution mistake |

|---|---|---|---|---|---|

| Final refusal before first payment | $1,000 | N/A | $1,000 less 24% | Start withholding on the first reportable payment and track withheld tax for reporting | Paying the full amount "just once" |

| Refusal after earlier full payments | $1,000 (future payment) | Earlier payments sent in full | $1,000 less 24% on future reportable payments | Start withholding from the trigger point forward and document when the trigger became clear | Quietly netting extra from later invoices without a documented basis |

| CP2100/CP2100A mismatch notice received later | $1,000 (next reportable payment) | May have been paid in full before notice | $1,000 less 24% if not already withholding | Follow the CP2100/CP2100A notice process, preserve notice records, and apply withholding when required | Treating the notice as clerical and continuing full payments |

3) Tax reporting: file complete returns with verified data#

Reporting should follow the facts you can support, not the facts you wish you had. If you withheld any federal income tax under backup withholding, file Form 1099-NEC for that payee regardless of payment amount. If no withholding occurred, verify the current filing trigger for that payment type and tax year before filing.

| Situation | Filing action | Note |

|---|---|---|

| You withheld federal income tax under backup withholding | File Form 1099-NEC for that payee | Do this regardless of payment amount |

| No withholding occurred | Verify the current filing trigger for that payment type and tax year before filing | Reporting should follow the facts you can support |

| TIN data is still missing at filing time | Follow the current IRS instructions for your payment type and tax year | Report only verified information you can support; do not invent placeholder TIN values unless your filing instructions explicitly allow your method |

| You withheld, or were required to withhold, federal income tax from nonpayroll payments | File Form 945 | Make sure the name and EIN on Form 945 match the name and EIN used on the related information returns |

If TIN data is still missing at filing time, follow the current IRS instructions for your payment type and tax year. Report only verified information you can support. Do not invent placeholder TIN values unless your filing instructions explicitly allow your method.

If you withheld, or were required to withhold, federal income tax from nonpayroll payments, file Form 945. Make sure the name and EIN on Form 945 match the name and EIN used on the related information returns.

4) Record retention: keep a single, audit-ready timeline#

At this stage, your best protection is a single, clean timeline. Keep W-9-related records in your files, not with the IRS, and keep them for four years based on IRS contractor guidance.

Your retained file should include:

- Initial solicitation record

- Annual solicitation records, if applicable

- Final notice

- Payment records showing gross, withheld, and net amounts

- Withholding start date evidence

- Filed return confirmations

Keep this in one secure timeline rather than scattering it across inboxes and chat threads. A chronological record is what shows good-faith compliance if your handling is reviewed later.

You might also find this useful: How to Fill Out Form W-8BEN for a Foreign Freelancer.

From Reactive Anxiety to Proactive Control#

If a payee refuses to provide a W-9, do not improvise. Run the same three-phase playbook every time: prevent avoidable errors, intervene with documented clarification, and execute a clear hold-and-escalate process when the file remains incomplete. That helps keep your records cleaner, reduce avoidable payment delays, and give you a defensible compliance trail.

Prevention#

The best time to control this issue is before anyone is waiting on money. Start with a status-first intake gate: confirm payee status in writing, send the matching document request under your policy, and log what you sent and when. This can reduce rework when status or entity details are challenged later.

Collect sensitive details only through secure channels. IRS training warns against sharing taxpayer-specific information in open channels, so avoid collecting SSNs, TINs, or similar data in casual email threads or open forms. Keep a timestamp, file copy, and confirmation record.

Intervention#

When documentation is missing or inconsistent, stop sending generic reminders. Ask one specific question at a time, capture each response in writing, and log the exact mismatch you are trying to resolve.

Escalate from education to your internal escalation path only when you have a documented issue summary, follow-up attempts on record, and an unresolved gap that blocks your payment or filing workflow.

Execution#

A final refusal is a process decision, not a debate. If the file is incomplete, stop advancement and move it to your defined escalation path.

Your evidence pack should include contract language, written status confirmation, document requests, reminder dates, and the internal approval note for the hold or next compliance action.

| Moment | Reactive behavior | Controlled behavior | Evidence trail | Business impact |

|---|---|---|---|---|

| Intake | You request forms late | You require written status confirmation before processing | Status confirmation and request log | Lower delay risk |

| Hesitation | You debate in long threads | You send one clear clarification request per issue | Follow-up messages and written replies | Lower dispute risk |

| Final refusal | You improvise case by case | You stop the file at your processability gate and escalate | Hold record and approval note | Defensible compliance steps |

| U.S. vs non-U.S. path | You send one default form | You verify status first, then follow the applicable certification path under your policy | Status record and form-request copy | Lower classification risk |

Use this checklist for the next refusal:

- Intake requirement: written status confirmation plus the applicable tax document request

- Scripted follow-up: initial request, correction request, escalation notice

- Escalation trigger: unresolved status or form mismatch after documented follow-up

- Final filing workflow: assemble the evidence pack, then verify the current withholding and reporting rules before filing

Frequently Asked Questions

I sent a W-9, but the payee says they are foreign. Is that a refusal?

Not necessarily. A W-9 is a request for taxpayer identification number and certification. If the payee says they are foreign, pause W-9 follow-up and get written status clarification before deciding what documentation to request next. Next action: document their written statement and confirm the next form request with your tax preparer or counsel.

The W-9 came back, but the LLC details do not make sense. What should I check?

Check line 1, line 2, and line 3a first. For a disregarded entity, the owner name should be on line 1, the disregarded entity name on line 2, and line 3a should reflect the owner's tax classification. Line 3b also matters: you may generally rely on it unless you know it is incorrect, and known issues can create downstream reporting work. Next action: request a corrected form and log the exact mismatch you found.

Can I make tax documentation a contract requirement?

Yes, as a business rule. Use language like "required tax documentation" or "applicable tax forms" so your process can adapt without naming only one form. Next action: update your contract and onboarding language to require the applicable form based on documented facts and current IRS instructions.

Do I still have reporting or withholding duties if the form never arrives?

Possibly, but you should not infer a filing threshold or withholding rate from refusal alone. Obligations can depend on the facts and current IRS instructions, including updates on IRS.gov/FormW9. Next action: verify what you know, review current instructions, and escalate unclear cases to your tax preparer or counsel.

Can I accept an e-signed W-9?

Use caution. IRS e-signature guidance is specific to Forms 8878 and 8879 in an ERO e-file context, so it is not blanket approval for every W-9 process. If you collect forms electronically, keep defensible evidence such as a signed image, timestamp, and remote IP metadata when available. Next action: confirm your method with your filing provider or counsel before relying on it.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Germany Freelance Visa Application Path for Freiberufler and Gewerbe

Choose your track before you collect documents. That first decision determines what your file needs to prove and which label should appear everywhere: `Freiberufler` for liberal-profession services, or `Selbständiger/Gewerbetreibender` for business and trade activity.

Form W-9 for Freelancers Working Across Borders

Treat **Form W-9** as an onboarding control point, not an admin afterthought. Before you sign, confirm the identity record you are certifying. This form gives your correct TIN to the person who may need to file an information return with the IRS.

How to Fill Out Form W-8BEN for a Foreign Freelancer

For many global professionals, Form W-8BEN is the first real point of friction in a U.S. client relationship. It often gets treated like routine paperwork. That is the wrong frame. If you run a business of one, this form is an early operating decision that affects cash flow, onboarding speed, and how much confidence a client has in your setup.