Quick Answer

Start by checking IRS status and sorting your case into processing, under review, or refund sent. If the return is still within the live processing window, document updates and avoid premature escalation. Once you are outside that window, gather your filed return, notices, and payment proof before contacting the IRS. If the system shows a mailed payment was issued but not received, move into the official payment-trace path for missing refunds.

A delayed tax refund is more than a nuisance. For a professional running a business-of-one, it signals that something in your tax process, recordkeeping, or filing controls needs attention. If you treat it that way, you stop waiting passively and start fixing the issue at its source.

This guide uses a three-phase plan. First, handle the immediate delay. Then identify the weakness that caused it and put controls in place so the same problem is less likely to happen again.

Phase 1: The Immediate Triage Protocol#

Classify the case first, then act. If you are still inside the current IRS processing window, wait and document. If you are outside it, gather records. If the IRS shows Refund Sent and a mailed refund check has not arrived, start a payment trace with Form 3911 when IRS trace criteria are met.

Classify the status before you escalate#

Start with IRS Where's My Refund?. Enter your SSN or ITIN, filing status, and the exact whole-dollar refund amount from your return. Check no more than once per day. The IRS updates the tool daily, and repeated checks do not speed anything up. Use these definitions to sort your case:

| Status | What it means | Key detail |

|---|---|---|

| Processing | The IRS is still handling your return through review and approval | A personalized refund date may not be available yet |

| Under review | A hold state where the IRS needs more time to verify return items | Items may include income, withholding, credits, or business income |

| Refund sent | The IRS has moved your refund to sent status | This is one of the official tracker stages |

| Payment trace | The IRS investigates a refund that was already issued but not received | This is typically done using Form 3911 |

When you log the case, use the tracker language exactly as shown so you do not blur a processing delay into a missing-payment case.

Follow the if/then path#

Start with the right timing window, then follow this path:

| Scenario | Timing or trigger | Action |

|---|---|---|

| Current-year e-filed return | Check status after 24 hours | Start with Where's My Refund? |

| Prior-year e-filed return | Check status after 3 or 4 days | Start with Where's My Refund? |

| Paper return | Check status after 4 weeks | Start with Where's My Refund? |

| Still inside the live IRS processing window | The current IRS processing page still shows you are within the window | Wait, save screenshots, and log dates |

| CP05 or CP05B-type review notice | CP05 guidance says to wait 60 days from the notice date before calling again | Follow the notice instructions |

| Refund Sent but mailed check not received | More than 28 days since the IRS mailed your refund | Initiate a Form 3911 payment trace |

- Check status at the right starting point

- Current-year e-filed return: after 24 hours - Prior-year e-filed return: after 3 or 4 days - Paper return: after 4 weeks

- Verify the live IRS processing window

- Confirm the current IRS processing page before you rely on a general timeline. - If you are still in that window, wait, save screenshots, and log dates.

- If you are outside the live window

- Pull your filed return, proof of filing, refund method details, and any IRS notices. - If you received a CP05/CP05B-type review notice, follow the notice instructions. CP05 guidance says to wait 60 days from the notice date before calling again.

- If status is Refund Sent but you did not receive a mailed check

- If it has been more than 28 days since the IRS mailed your refund, initiate a Form 3911 payment trace. - If the check was cashed, Bureau of the Fiscal Service review can take up to six weeks. - If the check was not cashed, the IRS can issue a replacement after the original check is canceled.

Capture the tracker result exactly as shown, with date and time. That screenshot, plus your filed return and any notice number, is the minimum evidence pack you want ready for a call or trace follow-up.

Run the business-of-one screen#

Before you call, run a quick mismatch screen and pull the documents you will actually need:

| Trigger | What to verify | Pull this document |

|---|---|---|

| Income mismatch | Do return amounts match third-party income reporting, for example Forms 1099/W-2? | Filed return plus each income form used |

| Estimated-payment mismatch | Do estimated payments on your return match what the IRS posted? | Payment confirmations, bank records, and any CP23 notice |

| Deduction or treaty review | Did claimed deductions or treaty benefits trigger review? | Schedule A or treaty support, plus any CP07 notice |

The real risk is not complexity by itself. It is complexity without a clean paper trail. If you cannot tie a number to a source document quickly, fix that before you contact the IRS. Then move to the next phase to diagnose an IRS refund delay. For a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

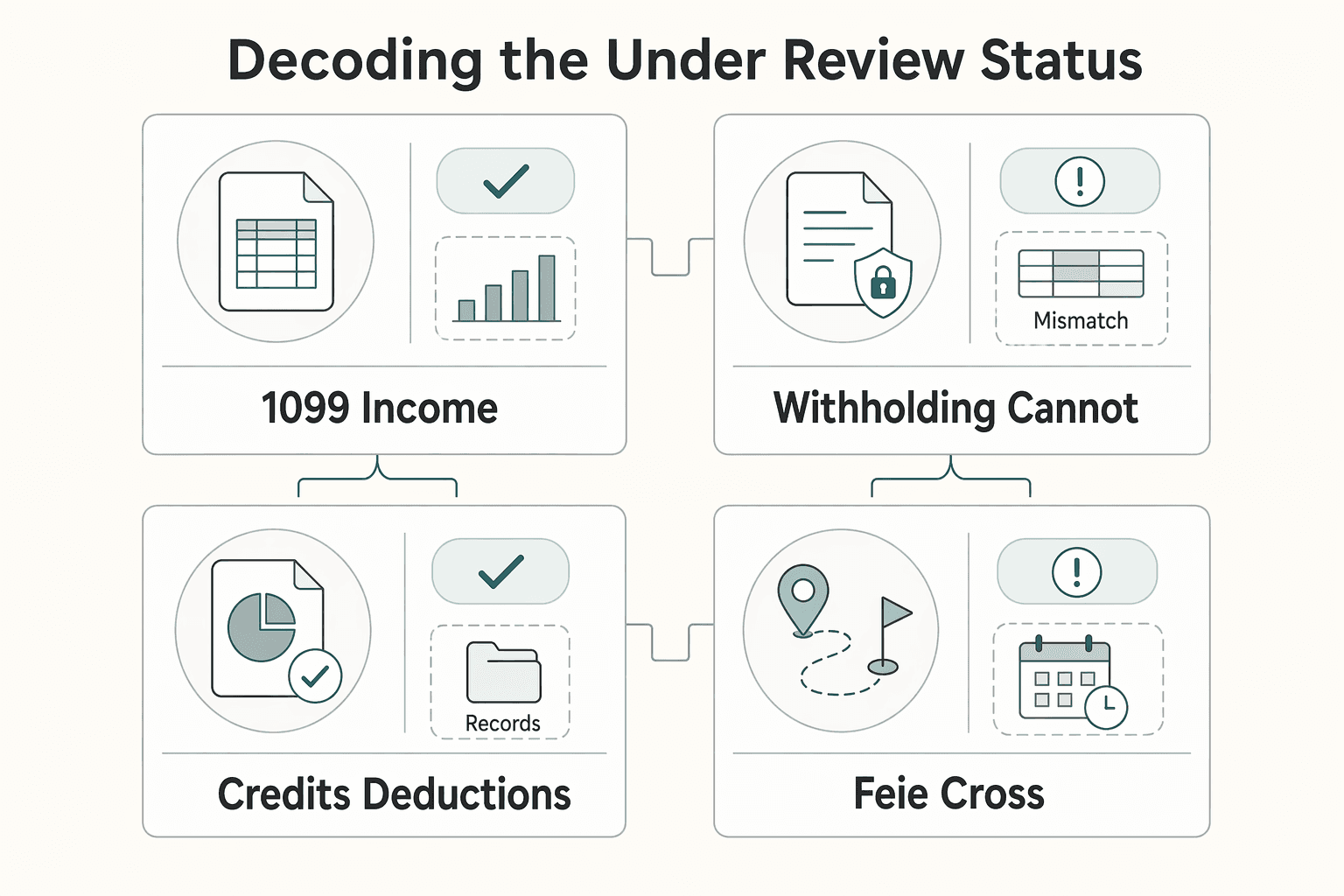

Decoding the "Under Review" Status#

A common Phase 1 outcome is an under review status. Treat that as a verification process, not an automatic audit. A review is the IRS checking whether income, expenses, credits, and withholding were reported accurately. A refund hold is the pause on payment while that verification happens. An audit is a separate examination process, and the IRS says audits start by mail, not by phone.

Use this routing path so you respond to the notice you actually received, not the stress of the delay:

- No IRS notice yet: Monitor Where's My Refund and save dated screenshots.

- CP05: Monitor and wait. IRS guidance says no immediate action and to allow up to 60 days before reaching out.

- CP05A or CP05B: Read the notice carefully and follow the stated instructions; if it asks for documents, reply by the due date with the exact items requested.

- Refund Sent but funds not received: Shift to a refund trace using Form 3911.

- You cannot reconcile the issue cleanly: Escalate to a qualified tax professional before replying.

| Trigger pattern | Why it gets flagged | Verify this record | Corrective action before responding |

|---|---|---|---|

| W-2/1099 income does not match the return | Third-party income reporting does not match filed amounts | Each payer form against the filed return | Build a line-by-line reconciliation and organize proof for each mismatch |

| Withholding cannot be verified | IRS needs support for withholding before issuing the refund | W-2/1099 withholding entries and return figures | Pull the records that support each withholding amount claimed |

| Credits, deductions, or other return items need verification | IRS may verify return items before release | Relevant schedules plus underlying records | Tie each claimed figure to a source document before you respond |

| FEIE or cross-border income positions | Foreign income and exclusion claims require support | Form 2555, travel-day records, foreign income records, tax-home evidence | Confirm FEIE support and worldwide income reporting are consistent before replying |

For international filers, validate FEIE evidence first. If you claimed FEIE, confirm Form 2555 is attached. Confirm your tax home was in a foreign country during the qualifying period, and confirm your records support either bona fide residence or the 330 full days in 12 months physical presence test. Keep travel logs, entry and exit evidence, and foreign income documentation together in one packet.

Before you respond, run a simple checklist. Create one response file for the case. Log every IRS letter and contact. Verify return-to-record consistency line by line, and keep copies of everything you send. If you cannot substantiate a cross-border position or explain a mismatch from your records, get professional review before you submit a response.

We covered this in detail in How to Handle a Tax Audit When Your Income is Paid Through Deel or Remote.

Phase 2: Diagnosing the System Failure#

If your refund is delayed, treat that as a symptom, not the root cause. IRS notes delays can happen when a return has errors, is incomplete, or is affected by identity theft or fraud. In this phase, your job is to find which part of your recordkeeping or pre-filing process made the return harder to verify.

Name the weak point clearly#

Compliance debt is a working term, not an IRS legal term. It means unresolved filing or record errors that pile up and later create delay and rework risk. IRS guidance is clear that errors can delay return processing.

Source of truth is your recordkeeping setup that clearly shows income and expenses and includes a summary of business transactions. If payments, invoices, and receipts live across disconnected tools, you do not have one.

Reconciliation cadence is also a working term, not an IRS legal term. It means your recurring check to confirm records are complete and accurate before filing. The standard is simple: file only after you verify the return is correct and complete.

Audit the records you actually use#

Refund delays can come from records that are hard to verify, not just from one obviously wrong number.

| Current state | Risk created | Fix to implement now |

|---|---|---|

| Income tracked across payment apps, email, and bank feeds with no master log | What you report may not match payer information returns, including Form 1099-NEC | Keep one income log tied to payer, invoice, payment date, amount, and deposit record |

| Receipts are scattered or missing | Deductions or credits cannot be supported | Store support docs in one organized place and link each document to the booked expense |

| Bank and card accounts are not reconciled consistently | Missing, duplicate, or misclassified transactions stay hidden until filing | Reconcile each account against your books on a recurring schedule you can maintain |

| Return prepared from memory plus year-end exports | Incomplete entries, missed forms, and data-entry errors become more likely | Run a pre-filing tie-out of books, statements, and all tax forms received |

Run a four-part self-assessment#

Start with income, then work outward:

| Review area | What to compare | What to flag |

|---|---|---|

| Income capture | Payer forms, including 1099-NEC, against invoices and deposits | Missing payers, duplicated entries, or timing mismatches |

| Expense documentation | Claimed deductions and credits against receipts, invoices, canceled checks, card records, or equivalent proof | Items that cannot be traced back to source records |

| Account reconciliation | Books to bank and card statements line by line | Uncategorized deposits, duplicate expenses, transfers booked as income, and personal-business mixing |

| Pre-filing review | Filed return against final books, payer forms, and payment details | Incomplete or error-filled returns, direct-deposit input errors, and unresolved identity-verification letters |

- Income capture

Pull payer forms first, including 1099-NEC, then compare them against invoices and deposits. Look for missing payers, duplicated entries, or timing mismatches. When you find them, they usually point to intake or recordkeeping gaps you can fix.

- Expense documentation

Check that claimed deductions and credits map to support documents such as receipts, invoices, canceled checks, card records, or equivalent proof. If you cannot trace items back to source records, your document retention process is the failure point.

- Account reconciliation

Compare books to bank and card statements line by line. Flag uncategorized deposits, duplicate expenses, transfers booked as income, and personal-business mixing. These patterns usually point to weak in-year reconciliation, not just a tax prep mistake.

- Pre-filing review

Confirm the filed return was checked against final books, payer forms, and payment details. IRS flags incomplete or error-filled returns as delay triggers, and direct-deposit input errors can create delays when a bank rejects and returns the deposit. Also check for unresolved identity-verification letters, which can block processing until you respond.

Save the exact records you used at filing time. If your books, filed return, and payer-reported amounts differ later, you need that filing-time evidence pack to explain the gap quickly.

Repeated calls will not speed up processing. Isolate the mismatch pattern, then fix the process that created it.

Hand off cleanly into Phase 3#

Before you move on to Phase 3, write down:

- Your top 1 to 3 process failures, for example weak income capture, missing deduction support, no reconciliation rhythm, or no pre-filing tie-out

- One owner for each fix: you

- Your recurring bookkeeping and review routine, stated in plain terms and on a schedule you can actually maintain

Related: Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

Phase 3: The 'Never Again' Protocol for Financial Resilience#

Lock in these three controls and run them year-round. The goal is simple: keep one defensible record set, reserve tax cash on purpose, and file only when key numbers tie back to evidence.

This is a control issue, not a motivation issue. National Taxpayer Advocate reporting highlights delays tied to amended returns, delayed or inadequate responses to records requests, and severe compliance burdens for taxpayers living abroad. Build a process that does not depend on fast document retrieval, paper-heavy workflows, or memory.

Pillar 1: Keep one source of truth you can defend#

Your source of truth is the ledger and document set you would use to explain any number on the filed return. Keep these artifacts in one place:

- One bookkeeping ledger for all business income and expenses

- One master income log linking payer, invoice, payment date, amount, and deposit record

- One cloud document folder organized by tax year

You still own this setup even if a preparer files the return. Keep one cloud location with year-based folders such as 2026/Income Forms, 2026/Bank Statements, 2026/Receipts, and 2026/Filed Return.

Why this can lower delay risk: records access can be slow, so having a complete, defensible record set before filing makes follow-up easier if it is needed. If you cannot trace a return number back to supporting records, stop and fix the books before the next filing cycle.

Pillar 2: Build a withholding workflow, not a guess#

For this protocol, withholding means your own rule for moving tax cash out of operating funds as income arrives. Choose your account structure first:

- Operating account plus separate tax-reserve account

- One account with clearly separated subaccounts or vaults

- For multi-country or multi-currency flows, anchor the rule to where funds first land so the trail stays reconcilable

Then choose one transfer trigger you will actually follow:

- Every client payment

- Daily sweep

- Weekly scheduled transfer

Document the rule in writing and in your bank automation notes. The important part is consistency, not inventing a percentage on the fly.

Why this can lower delay risk: it is designed to reduce last-minute cash pressure and create a clearer trail of reserve transfers tied to your payment records.

Pillar 3: Reconcile before filing, not after a delay#

Before you file, build a year-specific evidence pack for the exact return version you submit. If you later amend, keep the original pack and create a separate amended-return pack. Use this control table:

| Check | Required evidence | Escalation action if mismatched |

|---|---|---|

| Income reported vs payer records | Payer-issued forms, income log, invoices, and matching deposits | Request correction from issuer first. If unresolved, document outreach and involve a tax professional before filing. |

| Estimated tax payments claimed | Payment confirmations, bank debits, and payment log | Pause filing, rebuild the payment log from records, and escalate if gaps remain. |

| Major deductions/credits claimed | Receipts or invoices, proof of payment, and business-purpose notes where needed | Remove unsupported items or escalate for professional review if the impact is meaningful. |

| Final return totals vs books | Final return draft, year-end reports, and reconciliation notes | Do not file until numbers tie out or you have a written, supportable explanation. |

Escalate early when complexity persists#

Bring in a tax professional when any of these apply:

- Cross-border facts, foreign tax issues, multi-country filing exposure, or state-residency complexity, especially when international withholding-relief processes are already delayed

- Unresolved issuer mismatch after you compare forms, invoices, and deposits

- Reconciliation gaps that persist after a serious cleanup pass

- Planned amended return with changes that affect core return positions

Treat these as hard handoff criteria, not optional upgrades.

You might also find this useful: Malta's Tax Refund System for Foreign Companies Without Guesswork.

Before your next filing cycle, centralize your travel-day and residency evidence in one place with the Tax Residency Tracker.

Conclusion: From Anxious Wait to Empowered CEO#

Treat a delayed refund as a control signal, not background noise. Finish triage, document the cause, and tighten the process before the next filing cycle.

The practical outcome can be cleaner records and fewer filing surprises. Use Where's My Refund? with your SSN or ITIN, filing status, and exact whole dollar amount, and check status on the correct timeline for your filing method. If status shows Refund Sent and a mailed payment is still missing, move to a refund trace and follow IRS instructions, including Form 3911 when directed.

- Complete triage now. Confirm the current status and whether this is still normal processing or a missing-payment case. If a mailed check is missing and it has been more than 28 days since mailing, escalate to a replacement claim or trace.

- Log the root cause. Keep the records that support your return, including income and payment documentation, so you can resolve notices and identify what failed.

- Install prevention before next filing. Reconcile income and payments before filing so issues are found early, not after refund delays.

If you are globally mobile, keep the same mindset around compliance risk. U.S. reporting on worldwide income still applies, and cross-border residency questions can add real complexity. If your case involves dual-status or treaty-residency conflicts, escalate early to a qualified tax professional.

For immediate status action, start with How to Check the Status of Your Federal Tax Refund. That is your checkpoint: verify status, document the cause, and tighten execution before the next return.

For a step-by-step walkthrough, see Handling Tax Residency During a Crisis When You're Stuck Abroad.

If you want to tighten your compliance workflow after resolving this refund issue, review Gruv Tools.

Frequently Asked Questions

I haven’t received my tax refund. What should you do first?

Start by checking status, not guessing. Use Where’s My Refund only after the IRS timing windows apply: within 24 hours after e-filing a current-year return, about 3 or 4 days after e-filing a prior-year return, and 4 weeks after filing a paper return. If the tracker is still moving through Return Received, Refund Approved, or Refund Sent, keep a dated log and wait for the next status change.

What do “processing delay” and “manual review” actually mean?

A processing delay means your refund is taking longer because the return needs corrections or additional review. A manual review means the case is out of the normal automated flow and has to be handled by IRS staff. In practice, your next move is to document filing dates, tracker messages, and any IRS letters before taking additional steps.

What if the tracker says my refund was sent, but I never got the money?

At that point, stop refreshing the same page and move to trace or replacement steps. If a mailed check is missing, the IRS says you can file an online replacement claim after more than 28 days from the mailing date. A payment trace is the process used to track that missing payment, and it can start through official IRS channels, including 800-829-1954. If you filed married filing jointly, automated trace initiation is not available, so be ready to use Form 3911 if directed.

Could my refund be reduced to pay another debt?

Yes. That is an offset. Treasury can reduce your refund through the Treasury Offset Program (TOP) to pay eligible debts. Your next step is to document the BFS notice and contact the debt agency listed there first. Do not assume the IRS is always the first dispute channel in an offset case.

Is this a processing delay, a manual review, or an audit?

A refund delay and an audit are not the same thing, so classify the situation before you react. An audit is a formal examination of your books, accounts, and records, and IRS audit contact starts by mail, not by phone. | Situation | What it is | How you’ll know | What you should do next | Likely outcome | |---|---|---|---|---| | Processing delay | A refund hold tied to corrections or additional review | Tracker status slows or changes while no audit notice has arrived | Monitor and keep records of each status update | Outcome depends on review; refund may be released, adjusted, or held for more review | | Manual review | Your case requires IRS staff handling instead of standard automation | IRS indicates additional review, and processing takes longer than normal | Document dates, notices, and requested records | Slower processing, then release or adjustment | | Audit | A formal review of return accuracy and records | IRS notifies you by mail | Escalate carefully, verify the letter, and prepare records | No change, adjustment, or a formal dispute path |

When should you talk to a tax professional?

Talk to a pro when the delay involves cross-border facts or an amended claim tied to foreign tax credits. That is a clear point to escalate because special refund-claim rules can apply. If that is your case, stop improvising and get a documented strategy before you respond.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

How to Check the Status of Your Federal Tax Refund

Your refund is your own cash coming back, not a bonus. If you freelance or consult, treat that money like a receivable you manage closely, because it can affect both business obligations and personal draw.