Quick Answer

Yes - willful blindness in the FBAR context means you had warning signs of a filing duty, had a reasonable way to verify, and still filed without checking. The practical way to reduce that risk is to document what you verified before filing: track accounts against the $10,000 aggregate trigger, ask account-specific questions, and keep written follow-ups. Then make sure your return and FinCEN Form 114 align so your file shows diligence instead of conscious avoidance.

More Than an FBAR Mistake: Are You at Risk of 'Willful Blindness'?#

Treat this as a records-quality check first. Based on the material available here, the immediate risk is relying on a source you cannot fully open or verify. Use this quick snapshot to decide if this applies to you:

- The source opens to a file-download landing page rather than substantive guidance text.

- The download does not start automatically on your first attempt.

- You have not saved the final document you relied on, with date and context notes.

One practical control matters right away. If a source only opens as a download page or access is partial, use the manual retry link, then save the final document you relied on with the date and your context notes.

The first consequence is operational. If you cannot access the underlying document, your analysis is harder to verify later. This section is focused on building usable evidence: the final source file, when you accessed it, and what decision it informed.

Related: Missed an FBAR Filing? When Delinquent FBAR Procedures Fit and When They Do Not.

What 'Willful Blindness' Actually Means for Your Business-of-One#

As a practical risk screen (not a legal test), concern rises when a possible FBAR duty is flagged, you have a reasonable way to verify it, and you do not verify. Whether conduct is willful still depends on the full facts.

In the FBAR civil penalty context, willfulness matters because a willful failure to file a timely and accurate FBAR may lead to significant penalties. But one bad fact alone does not automatically settle willfulness. A source example makes that point: a taxpayer making $300,000 as an independent contractor reported that income on a tax return but did not file an FBAR reporting a foreign account's $200,000 maximum balance, and those initial facts alone were not sufficient by themselves to indicate willfulness.

Quick self-test for conscious avoidance#

- A possible FBAR signal appeared.

A return question, account detail, or other prompt put the issue on your radar.

- A verification path existed.

You had a reasonable way to confirm filing duties before filing.

- You chose not to verify.

You filed without confirming despite the unresolved signal.

If all three are true, treat this as a higher-risk pattern worth prompt review. If you followed up and kept records of what you verified, your facts may support a stronger position.

Practical behavior spectrum (working guide, not legal advice)#

| Scenario | What it looks like in practice | What the record shows |

|---|---|---|

| Initial hypothetical facts | Income is reported on the tax return, but no FBAR is filed reporting the foreign account's maximum balance. | Serious facts, but not sufficient by themselves to indicate willfulness. |

| Additional facts are developed | More context is added beyond the initial snapshot. | Additional facts can change the willfulness outcome. |

A common failure mode is assuming income reporting covers everything. It does not. The source example specifically separates income reporting from FBAR reporting of maximum account balance.

Penalty comparison checkpoint#

The source describes willful FBAR exposure with a higher-of structure: 50% of the unreported account balance at the time of the violation, or $100,000 adjusted for inflation. Do not treat that dollar figure as current without year-specific verification.

- Current civil penalty amounts: Non-willful and willful penalty amounts can be year-specific, so confirm the applicable figures for the year at issue before relying on them.

The practical takeaway is simple: document what you checked and keep complete account records so your fact pattern is clear if questioned.

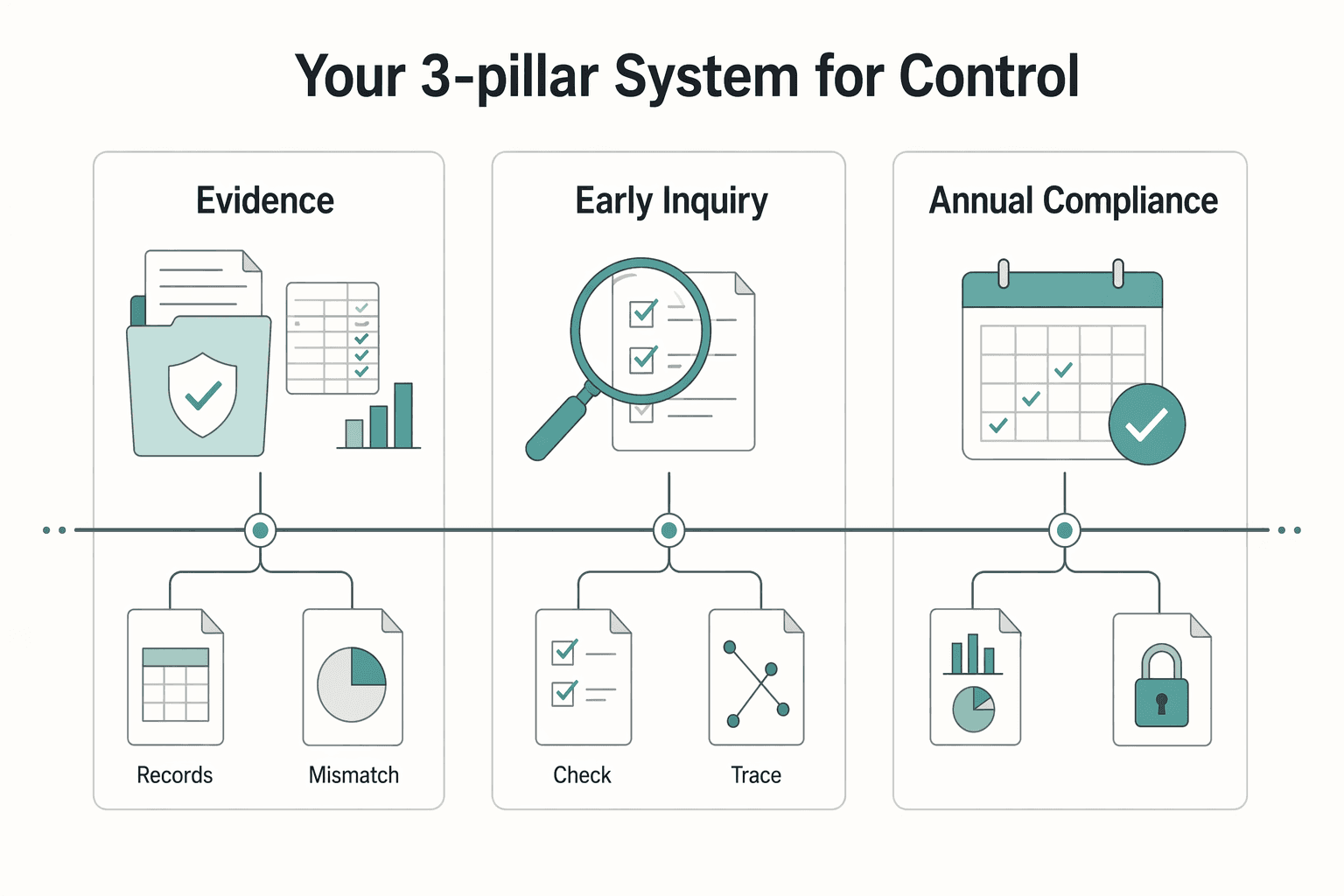

The Willful Blindness Defense Framework: Your 3-Pillar System for Control#

Use this as a prevention system, not a post-problem defense. To lower risk, you need documented habits that show you verified facts before you signed or filed.

Each pillar turns intent into evidence a reviewer can inspect. That matters because civil FBAR willfulness can include knowing, reckless, and willful-blind conduct, and the burden is a preponderance of the evidence.

| Pillar | Primary objective | Proof artifact |

|---|---|---|

| 1. System of record | Identify every foreign account that may count toward annual FBAR reporting | Account ledger, statements, account name/number (or other designation) details |

| 2. Early inquiry | Resolve open issues instead of guessing | Dated emails, meeting notes, documented follow-up questions |

| 3. Annual compliance review | Confirm year-end filings match the underlying facts | Review checklist, Schedule B Part III check, filed FBAR copy |

Two plain-language working labels help here, and they are not formal IRS or FinCEN legal definitions. A contemporaneous record can mean a document made when something happened, or immediately after, such as an updated account tracker, saved statement, or follow-up email after advisor guidance. A diligence record can mean documentation that you investigated uncertainty instead of assuming income reporting alone was enough or skipping unclear prompts.

You can also verify a few baseline requirements:

- FBAR is annual for each year the foreign-account relationship exists.

- The filing trigger is aggregate foreign-account value exceeding $10,000 at any time during the calendar year.

- Required records include identifying account details, including name and number or other designation, and must be retained for 5 years and kept available for inspection.

Decision outcomes by pillar are straightforward:

- Pillar 1: reduces omission risk; action is a complete account inventory; evidence is a full, current account record.

- Pillar 2: reduces conscious-avoidance risk; action is asking and documenting unresolved questions; evidence is a dated inquiry trail.

- Pillar 3: reduces sign-off risk; action is a year-end filing check, including Schedule B Part III and FBAR timing of April 15 with automatic extension to October 15; evidence is a completed review package.

Implement these in sequence: build the record, document inquiries, then run the annual review. Treat current reporting requirements as a separate verification step before relying on the review package. For a step-by-step walkthrough, see Do I Need to File an FBAR for a Company Account I Have Signature Authority Over?.

Pillar 1: Build Your System of Record - The Antidote to Chaos#

Start with one master ledger. It is not an IRS-required format, but it is a practical control that helps show you tracked facts instead of guessing.

FBAR filing risk is driven by foreign account status, your financial interest or signature/other authority, and aggregate value, not by whether an account produced taxable income. The trigger is when aggregate foreign-account value exceeds $10,000 at any point in the year, so omissions often start with scattered records.

What goes into the ledger#

Use the ledger as your single source of truth for every account you own, co-own, or control through signature or other authority. Start broad, then classify.

| Account/example | Treatment |

|---|---|

| Foreign bank accounts | Include for review and classification |

| Foreign brokerage accounts | Include for review and classification |

| Mutual fund or similar pooled fund accounts | Include for review and classification |

| Fintech wallets or payment platforms | Include for review and classification if balances are held at a foreign financial institution |

| Any foreign account where you have signature authority or other authority | Include for review and classification |

| Certain cash-value insurance, annuities with cash surrender value, and commodity futures/options accounts | Include for review and classification |

| Correspondent/Nostro accounts | Needs case-specific review before exclusion |

| Certain IRAs | Needs case-specific review before exclusion |

| Certain retirement plans | Needs case-specific review before exclusion |

| A foreign account holding only virtual currency | Needs year-specific review before exclusion |

Include these for review and classification:

- Foreign bank accounts

- Foreign brokerage accounts

- Mutual fund or similar pooled fund accounts

- Fintech wallets or payment platforms, if balances are held at a foreign financial institution

- Any foreign account where you have signature authority or other authority

- Other foreign financial products identified in IRS materials, including certain cash-value insurance, annuities with cash surrender value, and commodity futures/options accounts

Items that need case-specific review before exclusion:

- Correspondent/Nostro accounts

- Certain IRAs

- Certain retirement plans

- A foreign account holding only virtual currency (IRS Publication 5569 example)

Do not rely on income documents alone. An account can still matter for FBAR even with little or no taxable income.

Your recurring review routine#

Review on a fixed cadence, such as monthly, and again at year-end before filing. Use a recurring calendar trigger so the process does not depend on memory.

For each account, do an account-by-account scan and record:

- Highest balance visible for the review period

- Open or closed status, plus any status change

- Any change in ownership, signature authority, or other authority

If an account was opened, closed, or authority changed, log the date, or the best document-supported date. Keep the evidence from each cycle, not just the ledger row: balance snapshots, export files or statements, and short notes on changes. This builds a consistent diligence trail and supports required FBAR recordkeeping. Keep required records for 5 years from the FBAR due date.

Minimum ledger fields#

| Field name | Why it matters |

|---|---|

| Institution name and address | Required record element for reportable accounts |

| Country of institution | Helps confirm foreign location |

| Name on account and account number | Required identifier for each reportable account |

| Account type | Required record element |

| Ownership / signature authority / other authority | Tracks control, not just title |

| Native currency | Keeps value tracking consistent |

| Maximum value during the year | Required record element and core FBAR input |

| Opened / closed status and date | Helps prevent missed new or legacy accounts |

| Review date and reviewer note | Creates contemporaneous diligence evidence |

| Aggregate threshold flag | Internal trigger: aggregate value exceeded $10,000 at any time during the year |

If you are unsure about reportability, add the account to the ledger first and classify it second. That default keeps uncertainty from turning into omission.

Pillar 2: Master the Proactive Inquiry Protocol - Create Your Audit Trail of Diligence#

A clean ledger is not enough if your file shows you ignored open questions. This pillar is about proving that, when facts were unclear, you asked, verified, and corrected course instead of guessing.

The line you need to hold#

Use this practical distinction:

| Conduct bucket | What it looks like in practice | What your file should show |

|---|---|---|

| Non-willful error | You made a mistake, but you made a real effort to classify accounts correctly | Dated questions, shared documents, and clear follow-up |

| Willful blindness | You saw warning signs and did not follow up on obvious FBAR questions | Gaps, vague asks, or unresolved uncertainty left untested |

| Knowing or reckless noncompliance | Facts indicate you knew the duty, or ignored a high risk it applied | Repeated disregard after clear warning signs |

An examiner evaluates facts and circumstances, not your intent statement alone. Civil willfulness can include willful blindness and reckless conduct, and the record is judged on a preponderance of the evidence. Schedule B foreign-account answers are one checkpoint in that record, alongside your ledger and your FinCEN Form 114 filing position.

Ask questions that match the trigger#

Do not ask, "Do I need an FBAR?" Ask account-specific questions that force a classification. The filing trigger is aggregate foreign-account value above $10,000 at any time during the year, and scope can include financial interest, signature authority, or other authority.

| Trigger situation | Question to ask advisor | Record to save |

|---|---|---|

| You hold a foreign bank, brokerage, or mutual fund account | "Please confirm whether this account is reportable on FinCEN Form 114 and how you want maximum value documented." | Statement or export showing highest balance, plus written advisor response |

| You use a platform account that may hold funds outside the U.S. | "Please review whether this platform account is reportable for FBAR in my facts, and what documents support that conclusion." | Terms or location screenshots, balance history, and written classification |

| You can direct movement of funds in a business, client, or family account | "I have signature or other authority but not ownership. Does this create an FBAR obligation?" | Authority documents, access evidence, and written response |

| An account had no income or low activity | "Please confirm whether no income changes FBAR reporting for this account." | Year statement and written answer |

| An account opened or closed during the year | "How should we treat this account for FBAR, and what date evidence should I keep?" | Opening or closing confirmations, statements, and filing note |

If your advisor does not get full facts, you do not get a reliable classification. Send your ledger, flag uncertain accounts, and request a written position.

Run the follow-up email protocol after every substantive advisor discussion#

Send a short confirmation email promptly after each substantive discussion. Use this four-step structure every time, then save both your message and any reply in the same annual folder as the supporting account records:

| Step | What to confirm |

|---|---|

| 1. Facts provided | Accounts, authority, balances, and opens or closes |

| 2. Filing position | Whether FBAR is required for each unclear item |

| 3. Next actions and timing | The FBAR April 15 due date and automatic extension to October 15 if relevant |

| 4. Correction request | "Please reply if I misunderstood anything." |

- Confirm the facts you provided, including accounts, authority, balances, and opens or closes.

- Confirm the filing position, including whether FBAR is required for each unclear item.

- Confirm next actions and timing, including the FBAR April 15 due date and automatic extension to October 15 if relevant.

- Ask for correction: "Please reply if I misunderstood anything."

Research selectively and keep evidence clean#

Use high-signal primary materials tied to your exact question, then save only what supports your decision trail. Keep a dated copy with the visible URL and a one-line note, such as threshold check, record-retention check, or authority-scope check. A small, labeled file set is stronger than a large folder of unsourced screenshots and forum noise.

When to escalate to a qualified cross-border tax professional#

Escalate when ownership, control, or filing scope is unclear and that uncertainty could change whether an account belongs on FinCEN Form 114. Common escalation cases include signature or other authority without title, mixed business-personal control, platform classifications that are not straightforward, or conclusions given without document review.

Use this rule: if you cannot explain, in one short paragraph with attached documents, why an account is in or out of your FBAR population, escalate before filing.

Pillar 3: Conduct Your Annual Compliance Review - A CEO's Final Check#

This is your final pre-filing quality-control step. Your return, your records, and your FinCEN Form 114 should tell the same story. For each check below, decide clearly: proceed, pause, or escalate.

| Check | Proceed | Pause | Escalate |

|---|---|---|---|

| Check Schedule B for factual consistency | Schedule B answers are consistent with your ledger and your FBAR decision. | Any account or authority fact in your records is missing or inconsistent in your return package. | You cannot explain, in one short written note, why Schedule B, your ledger, and your FBAR position align. |

| Reconcile your ledger to the draft FBAR | Draft FBAR matches the ledger and supporting records. | Any unresolved mismatch remains. | Ownership, authority, or platform classification is still unclear after document review. |

| Save filing proof like an audit-ready record set | Submitted copy, confirmation page, acknowledgement trail, and supporting records are stored together. | You filed but did not preserve the core artifacts. | No acknowledgement appears and status is still unclear after BSA E-Filing status lookup. |

1. Check Schedule B for factual consistency#

Action: Review Schedule B Part III against your actual foreign-account facts, including financial interest, signature or other authority, and your FBAR filing position.

- Proceed: Schedule B answers are consistent with your ledger and your FBAR decision.

- Pause: Any account or authority fact in your records is missing or inconsistent in your return package.

- Escalate: You cannot explain, in one short written note, why Schedule B, your ledger, and your FBAR position align.

Before filing, confirm your trigger note is resolved: FBAR filing is required if the aggregate value of foreign financial accounts exceeds $10,000 at any time during the year. Schedule B asks whether you are required to file FinCEN Form 114, and IRS guidance treats a wrong or blank Schedule B box as a significant fact in willful-blindness analysis.

2. Reconcile your ledger to the draft FBAR#

Action: Compare your master ledger to the draft FinCEN Form 114 line by line.

| Record source | What must match | If mismatch, do this |

|---|---|---|

| Master account ledger | Account population, ownership or authority status, account name, account number or designation, account type | Correct the ledger or draft FBAR, then recheck all related entries |

| Statements or platform exports | Maximum value used for each account | Recalculate from source records and save the supporting file |

| Draft FinCEN Form 114 | Every reportable account from the ledger, with the same maximum-value basis | Pause submission until resolved or escalated |

- Proceed: Draft FBAR matches the ledger and supporting records.

- Pause: Any unresolved mismatch remains.

- Escalate: Ownership, authority, or platform classification is still unclear after document review.

3. Save filing proof like an audit-ready record set#

Action: After filing through BSA E-Filing, save the confirmation page and download the read-only submitted FBAR copy. Then track acknowledgement email status. FinCEN says accepted individual submissions are acknowledged in about 2 business days.

Use one consistent folder you can reliably retrieve later for your own records, such as Tax/<tax-year>/FBAR/, and one consistent naming pattern, such as <tax-year>-FBAR-SubmittedCopy.pdf, <tax-year>-FBAR-ConfirmationPage.pdf, and <tax-year>-FBAR-AcknowledgementEmail.pdf. Keep supporting account records with account name, account number or designation, account type, and maximum value. Required records must be retained for 5 years and kept available for inspection.

- Proceed: Submitted copy, confirmation page, acknowledgement trail, and supporting records are stored together.

- Pause: You filed but did not preserve the core artifacts.

- Escalate: No acknowledgement appears and status is still unclear after BSA E-Filing status lookup.

Keep deadline control in view: FBAR is due April 15, with an automatic extension to October 15. Use extension time to resolve facts, not to file on assumptions.

Before you finalize your annual review, run a quick threshold sanity check with the FBAR calculator and save the result in your compliance folder.

The Red Flags: How the IRS Spots Willful Blindness#

If you want to know whether your controls are strong enough, look at the file the way an examiner would. In a civil FBAR exam, a key issue can be whether your facts look like good-faith checking or conscious avoidance. Per the IRS Chief Counsel memorandum dated May 23, 2018, civil willfulness can include knowing violations, willful blindness, and reckless violations, and the burden is a preponderance of the evidence.

That means willfulness can be evaluated from the available evidence, not only from a direct admission. Because the statute and regulations do not define willfulness, inconsistencies, missing support, and unresolved contradictions may carry weight if your file does not show a clear process of inquiry and follow-through.

Practical comparison#

| File risk pattern | What triggers concern | What record from your three-pillar system can help |

|---|---|---|

| Annual FBAR reporting is missing or unclear | You had foreign account interest or authority, but the file does not clearly show annual FBAR treatment | Pillar 1 account ledger and filing records tied to each account and authority relationship |

| Reported account details are not supported | FBAR account information, including high-balance figures, cannot be traced to underlying records | Pillar 1 statements/exports and saved calculation workpapers for each reported account |

| Evidence can be read as knowing, willfully blind, or reckless conduct | Filing questions were left unresolved or follow-through is not documented | Pillar 2 dated question logs, follow-up messages, and resolution notes kept with the filing file |

| Willful vs non-willful treatment is not well supported | The file does not clearly explain facts, decisions, and final reporting position | Pillar 3 reconciliation notes that tie records, analysis, and final FBAR treatment before filing |

The practical line is simple: good-faith compliance leaves a traceable record, while conscious avoidance can leave avoidable gaps.

Penalty exposure is why this matters. The memorandum states a maximum penalty of $10,000 for a non-willful violation and, for a willful violation, the greater of $100,000 or 50% of the account balance. For a deeper breakdown, see The Difference Between 'Willful' and 'Non-Willful' FBAR Penalties.

Pause and escalate#

Pause self-filing and get qualified cross-border tax review before filing or amending if any of these apply:

- Your records do not clearly establish annual FBAR reporting treatment.

- You cannot reconstruct account details, including high-balance support, from records.

- The available facts could be read as knowing conduct, willful blindness, or recklessness.

From Compliance Anxiety to Professional Confidence#

Your goal is not to sound persuasive after the fact. It is to keep a file that makes your decisions verifiable before filing. In practice, that means being able to confirm three outcomes each year: complete records, a documented inquiry trail, and a final pre-filing review that catches mismatches early.

Run this like an annual control process for a business of one, not a one-time stress event. Keep your account ledger and statements current, save written Q&A with your preparer or platform, and do a final tie-out before you submit.

| Area | Before system adoption | After system adoption |

|---|---|---|

| Decision clarity | You rely on memory and assumptions | You can point to records behind each decision |

| Documentation quality | Explanations are reconstructed later | Explanations are documented as you go |

| Error prevention | Conflicts surface after filing | Final review catches gaps before submission |

Keep an evidence pack, not just a narrative: statements, balance support, filed returns, working notes, and saved written inquiries. Also preserve timing evidence when official notices arrive. The National Taxpayer Advocate's 2023 Purple Book presents taxpayer-rights and tax-administration recommendations, including that certain math error notices be sent by certified mail and explain a 60-day window to request abatement.

Do not assume that reporting in one place automatically resolves overlapping obligations, especially where duplicative BSA/FATCA reporting burdens can exist. If your records are incomplete or your facts conflict across filings, pause and get qualified cross-border tax review before you submit.

Related reading: Tax Residency vs. Citizenship-Based Taxation: The US Anomaly.

If you want this diligence workflow backed by policy gates and audit-ready records, talk with Gruv to confirm what is supported for your setup.

Frequently Asked Questions

What is the difference between a willful and non-willful FBAR violation?

The civil penalty framework depends on whether a violation is treated as willful or non-willful, and the willful side is much harsher. The excerpt does not provide a full legal test for classifying conduct, so if your facts are unclear or contradictory, escalate to a cross-border tax professional instead of self-labeling. | Distinction | Willful violation | Non-willful violation | | --- | --- | --- | | Classification basis | Treated as willful under applicable law | Treated as non-willful under applicable law | | Civil penalty framework (from the excerpt) | Up to 50% of the maximum account balance during the year (or, if greater, $100,000 adjusted for inflation per violation) | Maximum penalty stated as $10,000 (adjusted for inflation) | | Relief notes | Not covered in this excerpt | No penalty may be imposed if all account income was reported and reasonable cause existed | | Decision rule | Escalate to cross-border tax professional | Self-handle or document and monitor only when facts are simple and well documented |

Is simply forgetting to file an FBAR considered willful blindness?

The excerpt does not provide a direct legal definition of "willful blindness," so do not assume forgetting is automatically non-willful. Classification depends on the full facts. If the issue spans multiple years or your records are inconsistent, escalate.

How can you show your issue was non-willful?

Show it with contemporaneous records, not just a later explanation. Keep account balance support, filed-return records, and written notes showing how you identified and corrected the issue. If you cannot document the facts clearly, escalate.

If you reported all the income, are you automatically fine on the FBAR side?

No. Reporting all account income helps, and reasonable-cause relief for non-willful cases is tied to reported income plus reasonable cause, but relief is not automatic. If either element is weak, escalate for professional review.

What are clear freelancer examples of good-faith inquiry versus conscious avoidance?

The excerpt does not define these terms in detail. As a practical approach, keep written records of how you checked whether your accounts were reportable and what corrective steps you took. If your file includes unresolved contradictions or repeated misses, escalate.

What should you do if you realize you should have filed FBARs in prior years?

Treat this as time-sensitive risk control: stop repeat errors, gather records, and get a professional eligibility review for Delinquent FBAR Submission Procedures or Streamlined Filing Compliance Procedures. Timing is critical because the cited relief paths depend on correcting before IRS contact, and taxpayers contacted first are ineligible for those procedures.

Does the FBAR requirement apply to Wise, Revolut, or platform accounts?

Do not assume the brand name determines treatment. Confirm whether you hold a foreign financial account and apply the aggregate test against $10,000 during the year. If classification is unclear, escalate before filing.

Can you self-handle a current-year issue, or should you always get help?

Self-handle only when the facts are simple, records are complete, and classification is clear. Escalate when exposure is multi-year, records are missing, account status is uncertain, or facts could be treated as willful.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaefiling.fincen.gov/helptrusted

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- fincen.gov/system/files/shared/FBAR%20Line%20Item%20Fil...trusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- irs.gov/pub/lanoa/pmta_2018_13.pdftrusted

- taxpayeradvocate.irs.gov/wp-content/uploads/2023/02/PurpleBook_2023_F...trusted

- taxpayeradvocate.irs.gov/news/nta-blog/nta-blog-chapter-61-foreign-in...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Portugal NHR vs Spain Beckham Law for High-Earning US Expats in 2026

Start with documentation, not tax projections. In the portugal nhr vs spain beckham law decision, the safer first move is to choose the path you can prove from end to end before you optimize for headline outcomes.

The Difference Between 'Willful' and 'Non-Willful' FBAR Penalties

For modern global professionals, FinCEN Form 114, or the FBAR, creates a familiar kind of stress. You use platforms like Wise, Deel, and Revolut because they make your work easier and your finances more flexible. That flexibility is useful, but it also creates compliance complexity and, with it, the risk of a serious mistake. The line between an honest error and a willful violation can feel uncomfortably thin, and the penalties are not something to take lightly.

A Freelancer's Guide to the Statute of Limitations on Tax Audits

**Treat the statute of limitations question as an operations issue, not a loophole hunt.** If you run a freelance business across borders, you do not need tax folklore. You need a repeatable process that keeps compliance clean when facts get messy across tax years.