Quick Answer

Treat it as an eligibility gate, not an automatic benefit. The limitation on benefits clause us tax treaty rules can block reduced withholding unless you satisfy a treaty-specific test and document it before payment. Confirm the exact treaty for your Contracting State, check whether it includes an LOB article, and choose the right form by income type (Form W-8BEN for income not from personal services, Form 8233 for personal-services income). Submit the claim to the withholding agent with treaty residence, beneficial-owner, and TIN support.

Start Here if You Want Treaty Benefits Without Surprises#

Treat the Limitation on Benefits, or LOB, article as an upfront eligibility gate, not post-signature fine print. In a U.S. income tax treaty, LOB is there to block treaty shopping. When a treaty includes it, benefits are available only if you satisfy one of that article's tests.

The safest first move is to stop treating tax residence as the full answer. Residence in a treaty country may be necessary, but it is not always enough to get reduced withholding. Confirm the exact treaty for your Contracting State, check whether it includes an LOB article, and then verify eligibility in the treaty text itself.

Use this quick decision sequence first#

| Step | What to do | Key detail |

|---|---|---|

| Confirm treaty and LOB article | Confirm the exact treaty for your Contracting State and whether it includes an LOB article | If the treaty has no LOB article, those additional tests are not required |

| Start with the simplest claimant path | If you are claiming as an individual resident of a Contracting State, check that lane first | IRS Table 4 lists code 01 for an individual, and individuals who are residents of a Contracting State are generally not affected by LOB |

| Match the form to the income type before payment | Use Form W-8BEN for income not earned from personal services and Form 8233 for income from personal services | Treaty-rate withholding claims also generally require a U.S. or foreign TIN plus certifications on treaty residence, beneficial ownership, and LOB satisfaction where applicable |

| Submit the claim to the right party | Give the claim to the payor of the income, the withholding agent | If the payor knows the claim is ineligible, it must not apply the treaty rate |

- Confirm the exact treaty and whether it has an LOB article.

Some U.S. treaties have an LOB article and some do not. If the treaty has no LOB article, those additional tests are not required. If it does, use that treaty's text, not a generic summary or a checklist borrowed from another treaty.

- Start with the simplest claimant path.

If you are claiming as an individual resident of a Contracting State, check that lane first. IRS Table 4 lists code 01 for an individual, and IRS guidance says individuals who are residents of a Contracting State are generally not affected by LOB. If you are claiming through an entity, expect a more involved analysis.

- Match the form to the income type before payment.

For income not earned from personal services, use Form W-8BEN. For income from personal services, use Form 8233. Treaty-rate withholding claims also generally require a U.S. or foreign TIN plus certifications on treaty residence, beneficial ownership, and LOB satisfaction where applicable.

- Submit the claim to the right party.

Give the claim to the payor of the income, the withholding agent. If the payor knows the claim is ineligible, it must not apply the treaty rate.

What your first evidence file should contain#

Keep the file lean but reviewable: the treaty article you rely on, the LOB article excerpt if there is one, documentation of treaty residence, your TIN, and the form you gave the withholding agent.

If you are not claiming as a direct individual, add documentation showing which LOB test you think applies. If you cannot point to the exact treaty text and the exact test, you are not ready to claim reduced withholding.

When to stop and escalate#

Slow down if your case appears to depend on Table 4 code 07 (ownership and base erosion), 09 (active trade or business), or 10 (discretionary determination). Those paths usually require tighter documentation before you certify anything.

The common failure mode is mismatch, not intent: wrong treaty article, wrong form, missing TIN, or certifications that do not align with the LOB position being claimed. If you hit any of those, pause before payment, fix the record, and then reassess whether the treaty claim is defensible.

Phase 1 Confirm Treaty Scope Before You Do Any Tax Math#

Start with source text before you do any rate, form, or withholding analysis. A common LOB mistake is relying on summaries instead of treaty text. Use this checklist in order:

- Identify the exact U.S. income tax treaty for your Contracting State.

Start with the treaty itself, because eligibility is treaty-specific and comes from the actual text.

- Confirm whether that treaty includes a Limitation on Benefits (LOB) article.

Not every U.S. treaty has one. If it does not, those additional tests are not required. If it does, read that article before you claim reduced withholding.

- Use IRS Table 4. Limitation on Benefits as a map, not a final determination.

Table 4 helps you orient to test categories and treaty or protocol references. For example: 01 (Individual), 07 (ownership and base erosion), 08 (derivative benefits), 09 (active trade or business), 10 (discretionary determination). It is still only a pointer. Final eligibility comes from the treaty's LOB text.

- Verify which LOB tests are actually available in your treaty text.

Do not assume every treaty includes the same set of tests.

If your notes rely on an old summary, a copied checklist from another country treaty, or generic LOB guidance, stop there. Keep three items in your file: the exact treaty excerpt, the LOB article excerpt, and the Table 4 code you think applies. If you cannot show those clearly, do not certify eligibility yet.

Phase 2 Map Your Likely LOB Path Before Filing Forms#

Before you file anything, map your facts to one likely LOB path: either an objective test you can prove now or an interpretation-heavy path you should escalate. If you cannot name the test, the likely disqualifier, and the documents that support your position, you are not ready to certify treaty eligibility. Treaty residence alone is not enough; you also need to satisfy at least one LOB test.

For most solo operators, start with routes that fit a business-of-one structure. Public-company routes, including subsidiary-style public-company routes where a treaty includes them, usually are not the first screen. They generally matter only if you have a listed entity in your ownership chain.

Start with the tests that usually screen fastest#

The ownership and base erosion path is often an early entity-based screen. It focuses on who owns the entity and whether too much income is paid out as deductible amounts to non-qualified persons. Clean ownership and ordinary expense flows can make this workable. Layered ownership or related-party charge patterns can push it into deeper analysis.

The active trade or business path can be strong if you can show real business activity in your treaty country and a clear connection to the income for which treaty benefits are claimed. Registration alone may not be enough. You need operating facts.

The derivative benefits path is treaty-specific and ownership-chain dependent. If your analysis relies on assumptions instead of documents and treaty text, treat it as interpretation-heavy.

Use this triage rule.

- Likely yes: you can point to an available treaty route and produce matching documents now.

- Needs interpretation: the route depends on treaty-specific conditions, layered ownership, or judgment calls you cannot prove cleanly from your file.

- Escalate: no objective test fits, and discretionary determination is your only plausible route.

If discretionary determination is your only lane, treat it as an adviser checkpoint, not a self-serve fallback.

Decision table

| Test path | Inputs to screen first | Common disqualifier | Evidence to have before filing |

|---|---|---|---|

| Ownership and base erosion | Legal ownership, qualified-person status, deductible payment flows | Unclear ownership chain or excessive deductible outflows to non-qualified persons | Formation records, shareholder or cap table records, org chart, ledger detail, related-party agreements |

| Active trade or business | Real operating activity in treaty country, link to income for which benefits are claimed | Thin local substance or weak connection to covered income | Contracts, invoices, operations records, payroll or contractor records, financial records |

| Derivative benefits | Treaty includes route, ownership chain can be mapped, owner status can be verified | Treaty-specific conditions not clearly provable | Full ownership chart, owner residency records, parent or entity records, treaty excerpt |

| Discretionary determination | No clean objective route, facts still non-abusive | You cannot explain and document why the structure is not treaty shopping | Written facts memo, structure diagram, commercial rationale, adviser-ready file |

| Public-company routes | Actual listed entity facts in the ownership chain | No listed entity in chain | Listing support, group structure records, ownership chart |

Run two checks before forms go out. Confirm the exact treaty wording again. LOB language can vary from the U.S. Model, so your available route may differ from what you saw in another treaty.

Then check current IRS Pub. 515 update notes before you rely on withholding guidance. In some suspended-treaty contexts, withholding agents may reject treaty claims. In practice, that can affect whether a withholding agent accepts your claim even if your LOB analysis looks strong.

Working rule: choose the most objective path you can prove with documents today. If your only defensible path is derivative benefits or discretionary relief, pause and escalate before filing.

For a step-by-step walkthrough, see A Deep Dive into the 'Services PE' Clause in Modern Tax Treaties.

Phase 3 Build an Evidence Pack Before You Claim Anything#

Build the file so a reviewer can verify your treaty claim end to end without guessing. Your evidence pack should connect three things clearly: the treaty text, the payee or entity facts, and the payment timeline tied to your chosen path.

Build the file around source text first#

Lead with the controlling treaty article excerpt, then add the treaty-specific technical explanation, if one exists, as support. Use the technical explanation as an official guide, not a substitute for the treaty text.

Keep that treaty limit in view. For example, the IRS technical explanation is for the U.S.-Canada convention. It is not a universal guide for every treaty, and it states that it is not a complete comparison to prior treaty text.

| File section | What to include | Why it matters |

|---|---|---|

| Treaty authority | Current treaty article excerpts, treaty-specific technical explanation | Shows the legal basis you are relying on |

| Payee and entity facts | Payee-identification notes, including flow-through/disregarded entity treatment, plus supporting entity records | Supports who is claiming and whether the payee is correctly identified |

| Claim chronology | W-8 or W-9 artifacts, payout records, withholding records, invoices or contracts, audit-trail exports | Shows what was collected, when, and which payments the claim relates to |

Document ownership and payment flows with payee identification in mind#

If your position depends on ownership and payment flows, map both: who owns the claimant and where related payments go. Publication 515 checkpoints are useful here because they explicitly call out Identifying the Payee and Flow-Through Entities. They also address disregarded entities.

Working rule: if your org chart, ledger flow, and tax form collection do not point to the same payee story, pause and fix the mismatch before you claim benefits.

Prove business activity with operating records, not registration alone#

If your path relies on business activity, build the file around operating evidence such as contracts, invoices, payroll or contractor records, expense support, and operating correspondence. Use registration and residency documents as supporting context, not the core proof.

If your argument depends on words like "substantial," label that point as interpretation and escalate rather than presenting it as a settled threshold.

Use Gruv records as chronology support, not standalone treaty proof#

Where enabled, include Gruv W-8 or W-9 artifacts, payout records, and audit-trail exports to anchor timing and payment linkage. These records strengthen chronology and traceability, but they do not establish treaty eligibility on their own.

Final pre-filing check: run the file against Publication 515 checkpoints, including payee identification and Forms 1042 and 1042-S reporting obligations. If those checkpoints are not cleanly supported, treat that as a documentation gap to resolve first.

Related reading: A Deep Dive into the 'Dividend' Article of the US-Germany Tax Treaty for LLC Owners.

Decision Rules for Simple Structures and Layered Structures#

Use a simple rule: if the payee, beneficial owner, and income-derivation story all line up on one clean set of facts, you may have a certifiable treaty claim. If they do not, treat it as an escalation case.

Start with the direct claimant path#

For a direct claim, confirm the basics first: the claimant is the beneficial owner, meets any applicable LOB requirement, and gives the correct form to the withholding agent, or payor.

For income not earned from personal services, use Form W-8BEN. For income earned from personal services, use Form 8233. For reduced withholding on Form W-8BEN or W-8BEN-E, a U.S. or foreign TIN is generally required, except in certain marketable securities cases.

Use these if-then checks before claiming treaty relief#

| If this applies | Then do this | Why it matters |

|---|---|---|

| The payment is direct and the claimant facts are clean | Keep the claim direct | Match the payee shown in your records and forms to the person claiming treaty benefits |

| An entity is involved | Treat entity certification as a decision gate | An entity claimant may need to certify it derives the income within Section 894 and is not fiscally transparent |

| Your facts suggest third-country benefit access | Pause | LOB provisions generally block third-country residents from obtaining treaty benefits |

| Your position relies on multiple legal assumptions at once | Escalate | When the claim depends on stacked interpretations, it is no longer a low-risk DIY filing |

- If the payment is direct and the claimant facts are clean, keep the claim direct.

Match the payee shown in your records and forms to the person claiming treaty benefits.

- If an entity is involved, treat entity certification as a decision gate.

An entity claimant may need to certify it derives the income within Section 894 and is not fiscally transparent. If that point is unclear, escalate before filing.

- If your facts suggest third-country benefit access, pause.

LOB provisions generally block third-country residents from obtaining treaty benefits.

- If your position relies on multiple legal assumptions at once, escalate.

When the claim depends on stacked interpretations, it is no longer a low-risk DIY filing.

What usually breaks in layered cases#

If the payor knows, or has reason to know, the owner is ineligible, it must not apply the treaty rate.

Also treat residency-position conflicts as a hard stop. If a nonresident alien elected U.S. resident treatment with a U.S. spouse, that person may not claim foreign-resident treaty benefits.

Sanity Checks Before You Claim Treaty Benefits#

Before you claim treaty benefits, make sure every related filing position tells the same story. Contradictions can undermine an otherwise workable claim.

Check for filing-position conflict first#

Ask one question first: does your treaty position align with the rest of your U.S. return posture? If one document takes a position that conflicts with another, pause and reconcile before filing.

Run that same consistency check across your return forms, workpapers, and entity records. You do not need to solve every edge case yourself here, but you do need one fact pattern across forms, workpapers, account records, and treaty notes.

Run the foreign-asset reporting cross-check#

Treaty eligibility does not replace foreign-asset reporting. If you are a specified person with specified foreign financial assets, Form 8938 may still apply. It must be attached to your annual return by that return's due date, including extensions, and state the correct calendar year or tax year.

- Confirm whether Form 8938 is in scope.

The IRS cites an aggregate-value threshold above $50,000 for certain U.S. taxpayers, notes higher thresholds for joint filers or taxpayers residing abroad, and includes certain specified domestic entities, with instructions citing $75,000 at any time during the tax year. If you do not have to file an income tax return for the year, Form 8938 is not required for that year.

- Keep Form 8938 and FBAR as separate checks.

Filing Form 8938 does not remove a separate FBAR requirement. If FinCEN Form 114 is otherwise required, you may need both.

- Reconcile documents before certification.

If your return workpapers, foreign account list, or Form 8938 draft conflicts with your treaty claim, pause. Align residency support, entity records, account reporting, and treaty memo first.

If you need a separate refresh on the saving clause, see How to Handle the 'Saving Clause' in US Tax Treaties.

Red Flags That Mean You Should Escalate Immediately#

Escalate immediately when your treaty position depends more on interpretation or assumptions than on a clean, treaty-specific evidence file.

1. You cannot prove the ownership chain and payment chain cleanly#

Escalate when ownership or payment flows are unclear. If you cannot show one consistent record of legal ownership, the income recipient, and downstream payments across entity records and withholding documentation, treat that as an escalation trigger.

2. Your answer turns on whether your activity is "substantial"#

If your result depends on interpreting "substantial," treat that as a professional-review case. You need the treaty text and its matching technical explanation in your file before taking a judgment-heavy position.

3. Your derivative benefits path depends on multi-country assumptions#

If eligibility depends on layered cross-border assumptions, escalate. Do not rely on copied logic from another treaty or old cross-era comparisons. Technical explanations are treaty-specific, protocol-amended, and can explicitly note that they are not complete comparisons to earlier conventions.

4. You are relying on discretionary relief without strong prior support#

If discretionary relief is your only path, escalate early. Do not proceed from a thin record. Weak governance or missing interpretive support are practical risk signals, especially in an environment of rising audit expectations.

Where LOB Fits Against Other Anti-Abuse Standards#

For a U.S. filing position, start with this rule: your controlling authority is the bilateral treaty you are claiming under, plus U.S. filing and disclosure requirements. If your notes mix standards, the treaty text should drive the filing position.

| Item | How the article frames it | Filing role |

|---|---|---|

| LOB provisions | Use objective criteria to determine who can claim treaty benefits | Show facts and records that match the treaty path you are relying on |

| PPT | A broader, purpose-focused concept in OECD treaty-abuse materials | It may help explain policy intent, but it is not a substitute for showing eligibility under the specific U.S. treaty provision you are using |

| BEPS Action 6 | Relevant background because it treats treaty shopping as a minimum-standard problem | Context only; it does not decide whether your U.S. treaty claim passes |

| Bilateral treaty text and U.S. filing requirements | The controlling authority for a U.S. filing position | Use the bilateral treaty you are claiming under and U.S. filing and disclosure requirements as the final authority |

Objective tests are not the same as a purpose-based screen#

LOB provisions use objective criteria to determine who can claim treaty benefits. Your file should show facts and records that match the treaty path you are relying on.

PPT is a broader, purpose-focused concept in OECD treaty-abuse materials. It may help explain policy intent, but it is not a substitute for showing eligibility under the specific U.S. treaty provision you are using.

BEPS Action 6 is context, not your filing authority#

BEPS Action 6 is relevant background because it treats treaty shopping as a minimum-standard problem. OECD also frames abuse risk as benefits being routed to third-jurisdiction residents or income being taxed contrary to treaty intent.

That background still does not decide whether your U.S. treaty claim passes. Do not treat non-U.S. treaty analysis as a replacement for the bilateral U.S. treaty text that governs your case.

Use treaty text and IRS checkpoints as the final authority#

Your outcome depends on the bilateral treaty in force for your case and U.S. filing requirements.

Use this working rule in your notes.

- Start with the exact bilateral treaty you are claiming under, and identify the eligibility article that applies (for example, an LOB provision where present).

- Confirm U.S. filing checkpoints, including whether you are taking a treaty-based position that reduces tax and whether you obtained the current treaty text (Pub. 901, 09/2024).

- Use OECD materials, including BEPS Action 6 and PPT discussions, as context unless your treaty text makes them directly relevant.

If concepts still conflict after that, escalate. For filing, a treaty-specific record is safer than a source-mixed memo.

How LOB Can Affect Dividend Tax Treatment#

LOB can matter in dividend work when your analysis depends on treaty eligibility. Passing LOB can be necessary for treaty benefits, but it does not by itself determine whether a dividend is qualified or whether an issuer is a qualified foreign corporation.

Use this quick check before you let treaty status drive your dividend conclusion.

- Confirm treaty status is actually part of your dividend analysis.

If your dividend conclusion does not depend on treaty eligibility, LOB may not control that step. If it does, read the actual treaty LOB article. IRS Table 4 is a starting map, not the final rule.

- Keep legal tests separate.

LOB is a treaty-access test. Dividend classification under other tax rules is a separate question. They can connect, but one does not automatically answer the other.

- Use the right withholding claim path for dividend-type income.

For income not from personal services, treaty-rate claims are generally documented through Form W-8BEN or the entity version, with beneficial-owner certification, a TIN, and LOB certification if applicable. If an entity is claiming treaty withholding, include the Section 894 derivation certification in your review.

Do not import service-income logic into dividend claims without checking the governing rules. The Form 8233 path is for personal services, so do not treat it as interchangeable with dividend withholding analysis. For freelancers, keep this section limited to actual dividend fact patterns. If the withholding agent knows, or reasonably should know, treaty eligibility is not met, treaty rates should not be applied.

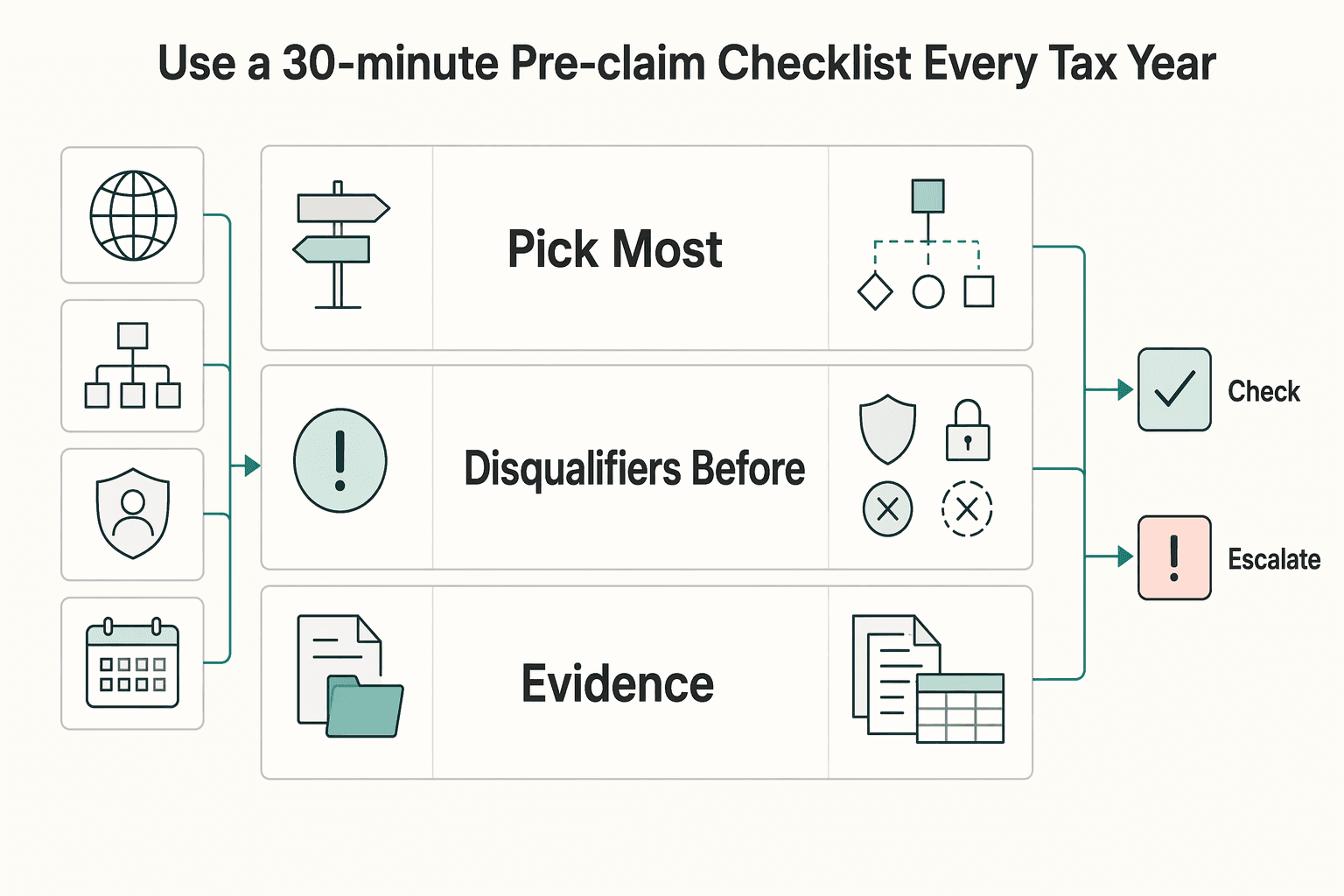

Use a 30-Minute Pre-Claim Checklist Every Tax Year#

If treaty access affects your withholding position, run this review each tax year before you sign forms or request a reduced rate. Pick your likely LOB path, confirm disqualifiers, map each key claim to a document, and make a clear go or no-go decision.

Start with four inputs: the current U.S. income tax treaty for your Contracting State, your current entity chart, your residency facts for the year, and your prior-year filing position. Use IRS Table 4. Limitation on Benefits as a map only. Final eligibility comes from the actual treaty Limitation on Benefits (LOB) article, because available tests can differ by treaty.

- Pick the most likely LOB path first.

Start with the path that fits your facts instead of testing everything at once. If you are an individual resident, treat "generally not affected" as a prompt to verify, not automatic clearance. For entities, identify the likely treaty path first, such as ownership and base erosion, derivative benefits, active trade or business, discretionary determination, or another treaty-specific route.

- Check disqualifiers before building paperwork.

First confirm whether the treaty has an LOB article. If it does not, those additional tests are not required. If it does, read the treaty article before relying on category codes such as 01, 07, 08, 09, 10, 11.

- Tie each key statement to a stored document.

Residency, ownership, and entity or payment facts should each map to supporting records. For entity treaty claims, confirm the treaty-claim fields you will use, including Form W-8BEN-E Line 14.

- Record unresolved issues immediately.

Keep a short escalation list for items that depend on interpretation or incomplete support so they are reviewed before filing.

Your outputs should be dated and review-ready: a go or no-go call, an escalation list, and an evidence file with the treaty excerpt, chosen LOB path, and supporting documents. Final checkpoint: do not file a claim unless every key statement maps to treaty text and a stored document.

Before you file, put your withholding documentation on a cleaner footing with the W-8 Form Generator.

The Main Takeaway for a Low-Stress Filing Position#

Treat the LOB article as a go or no-go checkpoint before you file, not a box to tick at the end. The lowest-stress position is one you can explain quickly using the current treaty text, the exact income type, and records that support each claim.

Start with treaty coverage before you focus on relief.

Ask this first: does this treaty cover this income type, and are you the kind of person it can help? Treaty relief varies by country and by item of income. If the treaty does not cover the income, or no treaty applies, standard U.S. nonresident tax treatment applies.

This is where filings can drift off course. It is easy to jump to a reduced rate before confirming the correct treaty version, the correct income article, and any later protocol updates. If treaty language is thin or unclear, use the Technical Explanation as the official guide to interpretation before you claim anything.

Build a file that proves your position.

You do not need a huge binder. You do need a clean evidence file where each key claim maps to a document.

- The current treaty article you rely on, plus relevant protocol language.

- The matching Technical Explanation excerpt when interpretation is needed.

- Residency records and any certification forms tied to the claim.

- A short note stating the income type and why the treaty article applies.

If a reviewer would have to guess what you are claiming, stop and tighten the file. Also separate general entitlement evidence from LOB proof: Form 8802 and Form 6166 can help when a foreign tax authority requests U.S. residency certification, but they do not replace meeting treaty terms.

Use hard escalation rules when facts are fuzzy.

Use a one-page test as an internal discipline: if you cannot explain your position in one page with treaty text, your facts, and your records, it is not ready for self-filed treatment. That is a quality check, not an IRS rule.

Escalate when either of these shows up: your facts do not cleanly fit the treaty article, or another part of your filing position conflicts with your claim. Common pressure points include state treatment, since some states honor treaty provisions and some do not, and status issues, since treaties generally do not reduce U.S. tax for U.S. citizens or U.S. treaty residents except in limited cases.

The working rule is simple: use the current treaty, confirm income coverage, rely on official treaty materials when interpretation is needed, and keep records that prove the claim without explanation gymnastics. If that is hard to do, pause and get professional review before filing.

If your LOB path still depends on judgment calls, use Contact Gruv to confirm what compliance and tax workflow support is available for your setup.

Frequently Asked Questions

What is a Limitation on Benefits clause in a U.S. tax treaty?

It is an anti-treaty-shopping rule in the treaty’s Limitation on Benefits (LOB) article. If a treaty includes an LOB article, benefits are available only if you satisfy at least one test in that article. If a treaty does not include an LOB article, those additional tests are not required.

Do I get treaty benefits automatically if I live in a treaty country?

No. Living in a treaty country is not automatically enough on its own. If the treaty has an LOB article, you still need to meet one of its tests, and a payor should not apply treaty rates if it knows or has reason to know you are not eligible.

Which LOB tests matter most for freelancers?

Start with the individual route if you are claiming directly as an individual. In IRS Table 4, that is 01, while entity routes include 07 (ownership and base erosion), 08 (derivative benefits), 09 (active trade or business), and 10 (discretionary determination). Use Table 4 as a map, then confirm the actual treaty text because available tests vary by treaty.

Why do people fail LOB even when their setup looks legitimate?

One failure point is treating a summary table as final authority instead of checking the treaty’s actual LOB article. Another is claiming a test without records that support it. Claims also fail when the payor has reason to know the owner is not eligible.

What should I do before claiming reduced withholding?

Run a treaty-specific checklist, pick one defensible LOB path, and build your evidence file before filing. Notify the withholding agent of your foreign status, use Form W-8BEN for income not earned from personal services, and use Form 8233 for personal-services income. For reduced treaty withholding rates on W-8 claims, provide a U.S. or foreign TIN, with a stated exception for certain marketable securities.

When should I talk to a tax professional?

Talk to one when you cannot clearly determine which treaty test applies or whether your documents actually support that test. Escalate if your position depends on interpretation rather than clear treaty text and evidence. If you cannot explain your claim with one treaty path and matching records, it is not a strong DIY filing case.

Is LOB the same thing as the saving clause?

No. They are separate treaty mechanisms and should be checked separately before relying on treaty benefits. Some treaties include saving-clause exceptions that may still allow certain U.S. residents to claim a treaty exemption. If that distinction affects your filing position, read How to Handle the 'Saving Clause' in US Tax Treaties before you file.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Tbilisi Digital Nomad Guide for 2026 Long Stays in Georgia

Start with sequence, not excitement. If your income depends on delivering work on schedule, secure your legal footing, assemble your documents, and keep month one reversible before you optimize comfort.

Handle the Saving Clause in US Tax Treaties Without Guesswork

Start with documents, not conclusions. Before you take any `saving clause us tax treaties` position, write down your residency facts, period-by-period status, and filing logic in plain language so someone else can follow your reasoning.