Quick Answer

Pay owner services through payroll first, then set shareholder distributions only after you can defend the wage amount with role-based support. For s-corp reasonable salary, IRS Fact Sheet FS-2008-25 uses a facts-and-circumstances standard, so 50/50 and 60/40 splits are only rough checks. Build support with one chosen method, comparable data such as BLS or PayScale benchmarks, and records showing the wage actually ran as employee compensation.

Start here if you want an IRS-defensible salary without guesswork#

Start with this rule: if you actively work in your S corporation and receive, or are entitled to receive, payment for those services, that compensation is generally treated as wages. For federal employment tax purposes, corporate officers, including S corporation officers, are employees, and service payments should be handled as wages rather than distributions or shareholder loans.

Use that as your default in an owner-run S corporation. Wages come first. Then document why the amount is reasonable. Do not begin from a distribution-first setup when officer services are clearly being performed.

There is no IRS safe-harbor percentage for reasonable compensation. The IRS position is based on facts and circumstances, so "50/50" or "pay yourself X%" shortcuts are not a reliable compliance method.

What you should expect from this guide#

This guide gives you a decision sequence, an evidence checklist, and clear escalation points for situations that need professional review. The goal is an explainable, defensible position, not a shortcut ratio.

What this is, and what it is not#

This is practical compliance guidance tied to IRS expectations for wage classification and reasonable compensation in an S corporation. It is not universal legal or tax advice for every state, fact pattern, or jurisdiction.

Global readers need a second checklist#

Keep these as separate tracks:

- S corporation wage treatment for owner services

- Cross-border reporting duties, when applicable

If foreign financial assets are in scope, Form 8938 is filed with your annual return by that return's due date, including extensions. Thresholds vary by filing status and residency context. In some cases, including certain joint filers and some taxpayers residing abroad, the thresholds are higher. A baseline $50,000 trigger applies in certain cases.

Keep this separate too: filing Form 8938 does not replace FBAR, FinCEN Form 114. FATCA is part of this reporting framework, and it is separate from the wage-classification rules for S corporation officer services. Related: Calculating Reasonable Salary for an S-Corp Under IRS Rules.

What reasonable compensation means in plain English#

Reasonable compensation means paying wages for the work you actually do in the S corporation, rather than treating service pay as non-wage payments.

The IRS applies a facts-and-circumstances test, not a fixed percentage or universal formula in the Code or Regulations. IRS Fact Sheet FS-2008-25 (August 2008) states that payments to a corporate officer for services must be treated as wages to the extent they are reasonable compensation.

Keep the payment types separate:

- Wages are employee pay for services rendered.

- Shareholder distributions are non-wage owner payments that come after reasonable compensation is addressed.

- If service pay is labeled as distributions or shareholder loans, the IRS can reclassify those amounts as wages.

Your number should be defensible based on the services you perform and the overall facts and circumstances. Reducing payroll taxes, by itself, is not enough to support a low wage amount.

Also, paying some wages does not automatically make the amount reasonable. In Watson (668 F.3d 1008 (8th Cir. 2012)), $24,000 per year in wages with large distributions was still litigated. The lesson is simple: the salary still has to fit the services rendered.

We covered this in detail in A Guide to the 'Reasonable Compensation' Test for C-Corps.

Why salary comes before distributions#

If you perform services for your S corporation, pay yourself through payroll first and treat distributions as what comes after salary and expenses.

That sequencing matters because owner pay runs through two channels with different tax treatment, and they are not interchangeable. Salary is wage compensation for your work and runs through payroll, including the 15.3% employment tax for Social Security and Medicare. Distributions are the remaining profit after salary and expenses, not a substitute for wage pay when your labor drives the business.

A common failure pattern is taking little or no wage pay while pulling cash as distributions, even when those payments are effectively for services. That can create reclassification risk, back taxes, and penalties. If your work is what generates revenue, the IRS expects a reasonable salary through payroll.

Use a simple checkpoint: wage compensation should look like wage compensation in your records. You should be able to produce payroll reports and year-end Forms W-2 and W-3, not just owner transfers and journal entries. For 2024, IRS substitute-form specifications for W-2 and W-3 provide a concrete documentation checkpoint. Wages should run through payroll documentation first, then distributions. Related: How to Handle Shareholder Distributions in an S-Corp.

Why 50/50 and 60/40 shortcuts can backfire#

Treat common 50/50 and 60/40 S-corp salary shortcuts as rough smell tests, not final support. A fixed split can look tidy while ignoring what changed in your work, time allocation, and business performance from year to year.

A low-margin year and a high-margin year should not default to the same ratio if your role intensity and market-rate context changed. If you reuse last year's percentage without rechecking the facts, the math may stay clean while the reasoning gets weaker.

Use this checkpoint: if a shortcut output conflicts with the role-based comparables you gathered, rely on the comparables. Document why the role match is stronger than a generic split.

Ratio shortcuts are only as strong as the documentation behind them. If the evidence in your file does not directly address officer compensation, treat the ratio as unproven and keep your written rationale anchored to role-specific support.

Related: A Guide to Converting an LLC to an S-Corp.

Pick a salary method and document your choice#

Pick one recognized method, use it as your primary support, and document why it fits your facts. The IRS does not provide a strict formula, so defensibility comes from a logical, well-documented method tied to market value.

If your work maps to a clear role, start with the market approach. If you perform multiple roles in a small business, the cost approach is often a practical fit. The income approach is also recognized.

How the methods compare#

Reasonable compensation is what like enterprises would ordinarily pay for similar services under similar circumstances. Use that standard to match your actual duties, not a convenient label.

| Method | Best fit | Data needed | Common failure mode | Audit defensibility signal |

|---|---|---|---|---|

| Market approach | Clearly defined role or industry benchmark | Comparable wages from BLS, PayScale, Glassdoor, ZipRecruiter; role-match notes | Choosing a title that does not match real duties; keeping comparables without role-match rationale | Sources align with duties, level, and market, and you can explain the match |

| Cost approach | Small business owner wearing multiple hats | Role list, comparable wages by role, and business context | Missing major duties or weak documentation of how roles were evaluated | Method reflects how the business actually runs |

| Income approach | Cases where business context is central to the analysis | Clear written method explanation plus business context, for example, gross receipts and total assets | Using undocumented math or a shortcut as a formula | File shows a recognized method and explains why the context supports the amount |

Use comparables like evidence#

Comparables are useful only if they show a real role match. Pull BLS benchmarks, cross-check them with PayScale, Glassdoor, and ZipRecruiter, and record why your selected role matches what you actually do.

Document that role-match logic in plain language: core duties, level, and relevant business context. Keep that explanation with the year files so you do not have to recreate it later.

Sequence to follow each year#

A practical sequence each year is:

- Choose one primary method.

- Consider one secondary check with another recognized method.

- Document any differences in a short memo saved with your year files.

If your support diverges, revisit role selection and business context before finalizing. Also avoid fixed heuristics like a 50/50 split as final support. If reasonable compensation is not paid, the IRS may recharacterize distributions as wages.

Related reading: A Deep Dive into the 'At-Risk' Rules for S-Corp Losses.

Build an evidence file the IRS can follow in five minutes#

Once you pick a salary method, make the file easy to verify from start to finish. The point is simple: show that a shareholder-employee who performed services was paid reasonable compensation before non-wage distributions, and make that logic traceable in your records.

That alignment matters because IRS guidance ties officer payments to wage treatment to the extent they are compensation for services. Payroll-tax failures can trigger tax due plus additions tied to payroll deposits and returns.

Build the minimum pack, not a scrapbook#

Keep the file lean but complete. A practical five-document baseline can work. It is a control set, not an IRS-issued checklist:

- Role description: what the owner actually did during the year.

- Time allocation record: how time was split across the duties used in your method.

- Compensation memo: method selected, why it fits, comparables used, and the final approved wage.

- Comparable wage support: the market-analysis materials you relied on, plus short role-match notes.

- Owner-approval note or minutes: annual approval record for the wage decision.

Tie the file to what you actually filed#

A concrete checkpoint is consistency across the evidence file, Form 1120-S workpapers, and payroll records. If your memo and payroll records tell different stories, treat that as a filing issue and reconcile it before you file.

Do a three-way tie-out before the return goes out:

- Approved annual wage in the memo.

- Wages actually processed through payroll.

- Officer wage treatment reflected in return workpapers.

If your wage rationale changed but the documentation did not, treat that as a compliance defect and fix it before filing.

Use a document table so nothing goes stale#

| Document | Owner | Storage location | Refresh cadence | Reviewer |

|---|---|---|---|---|

| Role description | Owner-operator | Tax folder, annual compensation subfolder | Annually or when duties change | Owner and tax preparer |

| Time allocation record | Owner-operator | Tax folder, supporting schedules | Monthly, quarterly, or year-end reconstruction | Owner |

| Compensation memo | Owner or preparer | Tax folder, annual compensation subfolder | Annually before filing | Tax preparer |

| Comparable wage support | Owner or preparer | Tax folder, source exhibits | Annually and when role or market context changes | Owner |

| Owner-approval note or minutes | Owner-operator | Corporate records folder | Annually | Owner and preparer |

| Payroll summary and tie-out workpaper | Payroll provider or owner | Payroll folder plus tax workpapers | At least at year-end before filing | Owner and preparer |

Treat stale documentation as a filing defect#

Potential misses include reusing last year's memo after role changes, changing methods without updating time-allocation support, or increasing distributions while payroll support stays unchanged. Update the memo, refresh comparables, revise time records as needed, and confirm payroll and Form 1120-S workpapers still match.

The downside is real: in a challenged compensation case discussed by practitioners, the IRS assessed a payroll tax deficiency of $9,560 plus $3,605 in additions to tax. Build a file that is deliberate, consistent, and quick to verify.

Use this checklist as your baseline. Then keep your compensation memo, payroll records, and any cross-border tasks on one repeatable schedule.

Run payroll correctly and keep owner pay streams separate#

To keep the record defensible, run owner wages through payroll and keep distributions and other payment types in separate lanes with clear labels.

Put each payment type in its own lane#

Do this as a standard operating pattern:

| Payment type | How to handle it | Record cue |

|---|---|---|

| Compensation for your services | Run through a formal payroll process | Payroll handles gross pay, taxes, and deductions |

| Shareholder distributions | Record outside payroll after salary | Profit taken after salary |

| Contractor payments | Keep outside payroll | Use their own invoice and payment trail |

| Other non-payroll payments | Keep separate from wages | Document them clearly |

This separation is operational, not cosmetic. Payroll is where gross pay, taxes, and deductions are handled, while distributions are profit taken after salary.

Check tax handling, not just cash movement#

A bank transfer by itself is not enough. Check that payroll reports show the owner wage stream handling income tax withholding and FICA, with regular pay cycles and quarterly payroll filings.

As a practical FICA check, the source material describes 7.65% withheld on the employee side, split into 6.2% Social Security and 1.45% Medicare, with an additional 7.65% employer share. You do not need to memorize the percentages, but you should see those tax components in payroll reports instead of bypassing payroll with ad hoc transfers.

Before each quarter closes:

- Confirm each salary payment ran through payroll.

- Review payroll reports for withholding and payroll-tax entries.

- Confirm distributions are booked separately and not netted against wages.

Avoid mixed transfers that are hard to reconstruct#

Do not blur wages, distributions, and contractor payments into one stream. Keeping each payment type distinct makes the trail easier to follow.

Use distinct labels and source documents for each stream. If you cannot match a bank line quickly to its supporting record, clean it up now.

Reconcile before quarter-end, not after year-end#

Before quarter-end, verify wages and payroll-tax entries match payroll reports and the general ledger, and check that distributions were not posted to wage accounts.

Fix mismatches while the details are still fresh. That helps keep the payroll and owner-pay record consistent through year-end.

Handle edge cases before they become audit problems#

Clean payroll lanes are necessary, but they do not solve everything. If business facts change and your wage logic does not, the risk of distributions being challenged as wages goes up.

| Situation | What to do | Why it matters |

|---|---|---|

| Profitability, role scope, or time commitment changes | Revisit the compensation rationale during the year instead of reusing last year's number | A stale split can become harder to defend when the economics shift |

| Mixed-role owner work | Break duties into practical buckets such as delivery, business development, management, and admin | Assess pay against what you would pay someone else to do that work |

| Cash-tight or low-profit year | Document constraints and timing decisions instead of skipping compensation analysis | Very low wages with continuing distributions can draw recharacterization scrutiny |

| Transition from sole proprietorship to S corporation | Start a new compensation file, confirm shareholder payroll is running, and align the written rationale with actual payments | Do not carry sole-prop draw habits into the S corporation year |

Rework the number when income swings#

If profitability, role scope, or time commitment changes, revisit your compensation rationale during the year instead of reusing last year's number by habit. Wages and distributions are treated differently for employment taxes, so a stale split can become harder to defend when the economics shift.

Use a simple check: does your current-year pay memo still match the work you actually did? If not, update it before year-end.

Split mixed-role work into real duties#

Many owner-shareholders are both employees and investors, so your records should reflect the work actually performed. You can break duties into practical buckets, for example delivery, business development, management, and admin, and assess pay against what you would pay someone else to do that work.

Keep this practical, not overly technical. A dated role summary, rough time allocation, and short pay rationale are often more credible than a vague title.

Low profit does not mean no analysis#

A cash-tight year is a reason to document decisions more clearly, not to skip compensation analysis. Wage income is subject to employment tax, while distributions are not, so the pressure to minimize salary is real.

Document constraints and timing decisions as they happen. If wages remain very low while distributions continue, that pattern can draw recharacterization scrutiny.

Reset when you move from sole proprietorship to S corporation#

Do not carry sole-prop draw habits into your S corporation year. Once you elect S corporation treatment, owner pay needs a fresh wage-versus-distribution rationale tied to the new entity setup.

Start a new compensation file for the transition year, confirm shareholder payroll is actually running, and align the written rationale with how money is really being paid.

If you want a deeper dive, read Sole Proprietorship vs. LLC: The Definitive Guide for Global Freelancers.

Cross-border checkpoints for globally mobile S-corp owners#

Once foreign accounts are involved, correct S-corp payroll is only part of compliance. You can run wages correctly and still have separate foreign-asset reporting obligations.

Keep payroll compliance separate from foreign asset reporting#

Form 8938 and FBAR are separate filings, not substitutes. Filing Form 8938 does not remove the FinCEN Form 114 (FBAR) requirement.

Form 8938 is attached to your annual return and filed by that return's due date, including extensions. It applies when specified foreign financial assets exceed the relevant thresholds, and those thresholds are not one-size-fits-all. The IRS notes a $50,000 base threshold for certain U.S. taxpayers, with higher thresholds for some joint filers and taxpayers residing abroad.

Do not assume every S-corp owner files Form 8938, or that the entity always does. Filing depends on whether the filer is a specified person or specified domestic entity and whether thresholds are met. If you are not required to file an income tax return for the year, you do not file Form 8938.

Make the records tell one story#

If you use foreign accounts, keep the records organized so the filings are internally consistent. Anyone reviewing the file later should be able to follow key account changes during the year without guesswork.

Keep the evidence pack broader than payroll#

Form 8938 itself shows what to track. It asks whether foreign deposit or custodial accounts were closed during the tax year, and it includes maximum-value fields for foreign deposit accounts. That means year-end balances alone are not enough when accounts changed during the year.

For a cleaner cross-border file, keep:

- foreign account statements across the year, not only year-end statements

- account opening or closure records when relevant

- records that support the maximum account values reported during the year

- your filed return package, including Form 8938 when applicable

If you are unsure whether a filing obligation sits with you personally, with the S corporation, or potentially both, escalate to a qualified tax professional before filing.

For a step-by-step walkthrough, see The S-Corp Election for LLCs: A Tax-Saving Strategy for High-Earning Freelancers.

Know exactly when to escalate to a tax professional#

Escalate before filing when cross-border filing obligations are unclear or threshold application is uncertain.

| Issue | Article checkpoint | Escalate if unclear |

|---|---|---|

| Form 8938 filer status | Filing depends on whether the filer is a specified person or specified domestic entity | Whether you are a specified person for Form 8938 purposes |

| Form 8938 and FBAR | Form 8938 does not replace FBAR | Whether Form 8938, FBAR, or both apply |

| Form 8938 thresholds | For certain specified domestic entities, instructions point to filing when specified foreign financial assets exceed $50,000 at year-end or $75,000 at any time during the tax year | Whether the applicable Form 8938 threshold is met |

| Excluded accounts | Excluded accounts may change what must be reported | Whether excluded accounts change what must be reported |

| Income tax return filing | If you are not required to file an income tax return for the year, Form 8938 is not required | Whether that rule changes your Form 8938 filing obligation |

Use these triggers:

- You are unsure whether you are a specified person for Form 8938 purposes (specified individual or specified domestic entity).

- Foreign accounts or other specified foreign financial assets are involved and you are unsure whether Form 8938, FinCEN Form 114 (FBAR), or both apply.

- You are unsure whether the applicable Form 8938 threshold is met for your filer status or entity type.

- You are not sure whether excluded accounts (for example, accounts maintained by a U.S. payer) change what must be reported.

For cross-border issues, keep these hard checkpoints in view:

- Form 8938 does not replace FBAR.

- Form 8938 filing depends on filer status and applicable thresholds.

- For certain specified domestic entities, Form 8938 instructions point to filing when specified foreign financial assets exceed $50,000 at year-end or $75,000 at any time during the tax year.

- Form 8938 is attached to the annual return and filed by that return's due date, including extensions, and it must identify the applicable tax year or calendar year.

- If you are not required to file an income tax return for the year, Form 8938 is not required.

Keep the escalation focused so you get usable answers quickly:

- your evidence pack: foreign account records, other foreign asset records, and draft return materials

- your method memo: your filer status, which year the filing relates to, and where threshold application is uncertain

- your unresolved questions: whether Form 8938 applies, whether FBAR also applies, and whether any accounts are excluded

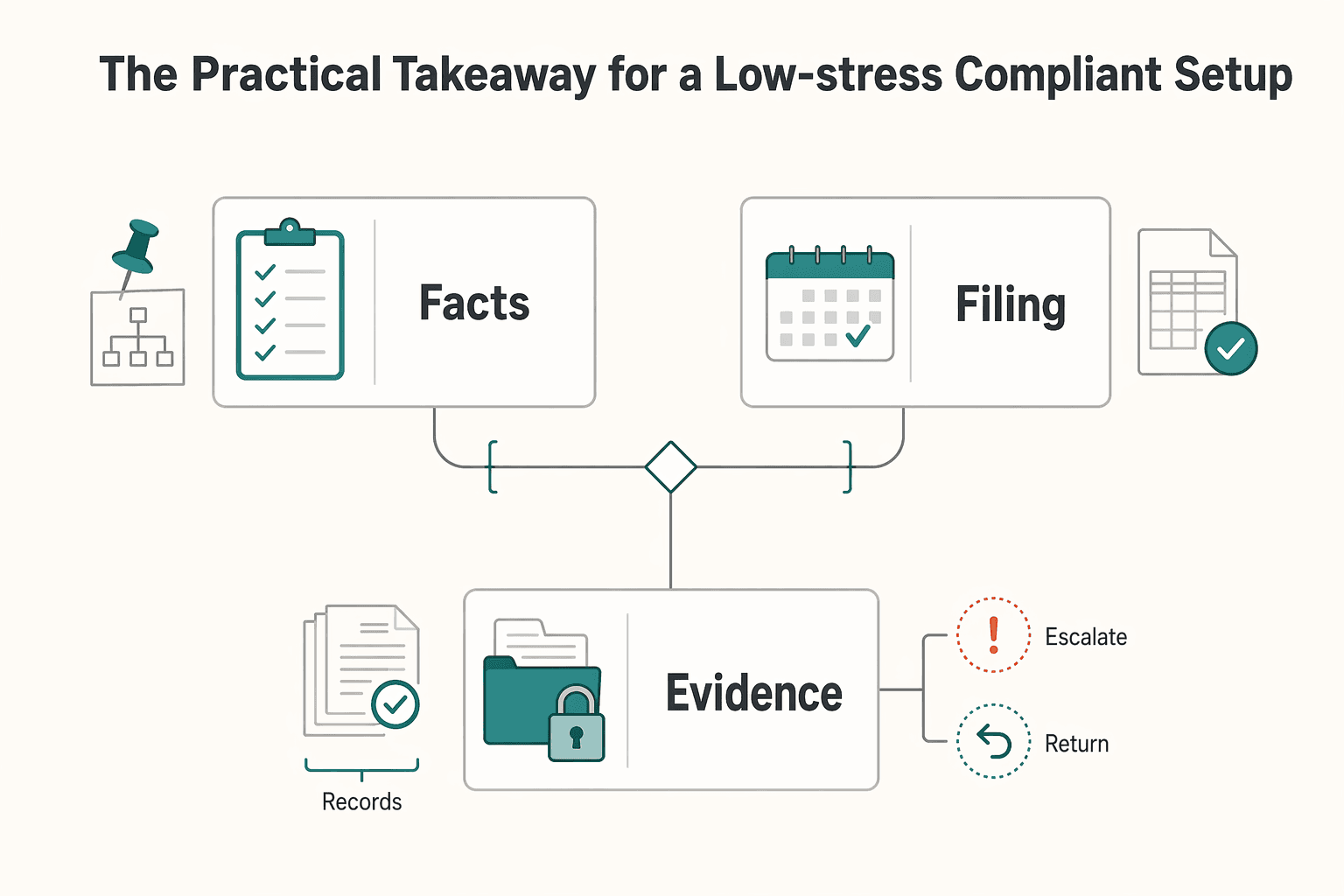

The practical takeaway for a low-stress compliant setup#

The lowest-stress way to handle this is to treat your S-corp salary decision as a repeatable operating process, not a year-end tax move. Use the same sequence each time: define the role, choose the method, gather comparables, run payroll, and keep one evidence file that explains the number.

- Define the role you actually perform

Document real duties, not just your title.

- Choose one primary method and apply it consistently

Use method-backed analysis tied to your work instead of chasing a lower number.

- Gather and save comparable pay support

Keep the market analysis you relied on and why it matches your duties.

- Pay fair-market compensation before distributions

If you perform substantial services, treat wages first and distributions after.

- Keep a clean evidence file

At minimum, keep your market analysis, approval note or minutes, and time records together.

Ratio shortcuts, including fixed splits like 60/40, are weak inputs, not final answers. If salary is set too low and distributions are high, distributions can be reclassified as wages, with potential back taxes, penalties, and interest.

Recheck the number when facts change materially, not just at filing season. If duties, payouts, or business conditions shift and the support gets harder to defend, escalate early with organized records so compliance stays straightforward.

Need the full breakdown? Read How Much Should a Freelancer Save for Taxes? A Simple Formula.

If your setup now includes distributions and payroll, get a second set of eyes before filing.

Frequently Asked Questions

Is there an IRS formula for setting S-corp reasonable salary?

No. IRS Fact Sheet FS-2008-25 (August 2008) says there are no specific Code or Regulation guidelines, and courts decide based on each case's facts and circumstances. For s-corp reasonable salary, that means the number needs a defensible, role-based rationale, not a fixed-percentage shortcut.

Can I take only shareholder distributions and no salary from my S corporation?

Usually no if you perform services as a shareholder-employee. IRS guidance says those payments are treated as wages, and reasonable compensation must be paid before non-wage distributions. If service pay is labeled as distributions, the IRS can still treat it as wages and apply employment taxes.

Are 50/50 and 60/40 required rules or just rough heuristics?

They are not IRS requirements. Guidance describes 50/50 as a common misconception, and fixed splits like 60/40 are not a substitute for a facts-and-circumstances analysis. If a split does not match your actual services and compensation facts, treat that as a warning sign.

What documents best support my compensation number in an IRS review?

Keep a clear file showing how you reached the number using IRS guidance, industry pay data, and company financial context, including gross receipts and total assets. Also keep payroll and distribution records consistent with that analysis, since IRS guidance focuses on whether payments for services should be treated as wages. The goal is one coherent story, not disconnected records.

Which salary method should I use first for a one-owner consulting business?

There is no universal first method for every one-owner consulting business. If you perform multiple roles, practitioner guidance says the cost approach, the "many hats" approach, is suited to that setup. Use it as a starting structure, then check that the result still aligns with market pay for comparable work.

What should I do if my income drops or spikes mid-year?

Reassess compensation when the business facts change materially. Update the analysis to reflect current services and financial context, then confirm wages and distributions still make sense together. If the new facts make the position hard to defend, reassess the approach before filing.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- congress.gov/114/plaws/publ113/PLAW-114publ113.htmtrusted

- docs.house.gov/billsthisweek/20250519/BILL-TO-BILL_BILLS-11...trusted

- energy.gov/sites/default/files/2025-12/NPC_Permitting_r...trusted

- gao.gov/assets/a299526.htmltrusted

- in.gov/dwd/files/Employer_Handbook.pdftrusted

- irs.gov/businesses/corporations/do-i-need-to-file-fo...trusted

- irs.gov/businesses/small-businesses-self-employed/s-...trusted

- leginfo.legislature.ca.gov/faces/billNavClient.xhtmltrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sole Proprietorship vs LLC for Global Freelancers in 2026

For most freelancers in 2026, the practical default is still simple: use the simplest structure you can run cleanly, then formalize when risk actually rises. If your work is still in validation mode and the downside is contained, a sole proprietorship is often the practical starting point. When contract exposure, delivery stakes, or dispute risk starts climbing, forming an LLC deserves earlier attention.

How to Handle Shareholder Distributions in an S-Corp

Start with one rule: classify each owner transfer clearly, then keep enough records to test distribution taxability against **[stock basis](https://www.irs.gov/businesses/small-businesses-self-employed/s-corporation-stock-and-debt-basis)** later. In an S corporation, income, loss, deductions, and credits flow through to shareholders and are taxed on shareholders' personal returns. Whether a non-dividend distribution is taxable depends on stock basis, not debt basis. `Schedule K-1` reports the non-dividend distribution amount, but it does not tell you the taxable amount.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.