Quick Answer

Permanent Establishment (PE) is a taxable business presence in a host country, usually tested through a fixed place of business or authority exercised by a dependent agent. For freelancers asking what is a permanent establishment, the practical move is to assign a risk label, then document contracts, work location, and revenue by country before scaling. Treaty wording and domestic law both affect the outcome, and unclear facts should be handled as active risk until confirmed.

Start Here With the PE Decision You Actually Need to Make#

Start with the decision that changes your next move: is PE risk active now, or are you still in monitor mode?

If you are asking what is a permanent establishment, the practical answer is simple. PE is a taxable business presence in another country that can shift you from planning to filing. That shift is commonly tested through facts you can document, such as whether there is a fixed place of business and whether someone in-country has authority to contract for you.

This is educational guidance for international tax decisions, not legal advice. Final treatment depends on domestic law where activity occurs and any bilateral tax treaty that applies. Thresholds are country-specific, and treaty terms can raise or lower local defaults. In the U.S. context, do not treat tests as interchangeable: being engaged in a U.S. trade or business can be broader than creating a U.S. PE.

Use this quick triage before you expand or renew anything:

- A fixed place of business can mean risk is active.

- Ongoing in-country authority to conclude contracts can mean risk is active.

- Unclear facts are not neutral facts. Treat unclear as active until verified.

Then assign one label and act on it:

Active now: pause expansion steps that increase local footprint, verify treaty and domestic-law treatment, and complete your evidence pack.Monitor: keep the same controls in place and set a clear recheck trigger tied to fact changes.Unclear: handle it as active now until you close the gap.

Before you choose between act now and monitor, keep a lean evidence pack that can survive review:

- Contracts showing who can and cannot bind terms.

- A dated log of where work was performed and by whom.

- Revenue records by country with service period context.

- Notes on domestic-law and treaty review.

Do not wait until year-end to organize this. The earlier you capture authority, location, and revenue facts, the easier it is to defend your position later. A common mistake is trying to reconstruct decisions after activity has already scaled.

By the end, you want three things: a risk label, an evidence pack, and an act-now-versus-monitor decision your team can follow without guessing. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2026.

What Permanent Establishment Means in Plain English#

Permanent Establishment, or PE, is the threshold that can let a host country tax business profits tied to activity there. Below that threshold, the host country often does not tax that foreign enterprise income. Cross it, and your posture often shifts from monitor to act now.

If you are still pinning down the concept, treat PE as a country-specific trigger rather than a permanent company status. You are testing facts in a place, at a time, under specific domestic law and treaty text.

| Party | What it applies to | Why you care |

|---|---|---|

| Home jurisdiction | Domestic tax rules in your residence country | It can remain relevant while host-country PE exposure is assessed |

| Source or host country | Domestic tax law on local business activity | It may assert taxing rights once PE conditions are met |

| Each contracting state under a treaty | Treaty wording and definitions | The same facts can be treated differently on each side |

Treaty language often follows OECD model wording, but outcomes are not uniform. Specific treaty text can include different thresholds or exceptions, and domestic law can apply the same facts differently.

In practice, two recurring pathways are a fixed place of business and a dependent agent. Do not assume PE exists only in a traditional office setup. Authorities may test arrangements beyond classic bricks-and-mortar facts.

Keep the PE question focused from day one: PE analysis asks when business profits become taxable in a source country based on the facts, domestic law, and treaty text.

For freelancers and consultants, this can affect pricing, contract terms, and cash planning. The decision is not just legal positioning. It can change how you draft authority clauses, who signs what, and how quickly you can expand into the next contract cycle.

Before cross-border work starts or renews, use this checkpoint:

- Save the relevant treaty article excerpt and your domestic-law interpretation note.

- Keep contract clauses showing who can and cannot bind commercial terms.

- Maintain a dated log of where services were delivered and by whom.

- Record the assumption you are using today and what fact change would force a recheck.

That last line matters because a documented assumption with a clear recheck trigger keeps monitor mode disciplined instead of passive.

The Two Triggers That Usually Create PE Risk#

A common PE risk framework uses two triggers: a fixed place of business in-country, or a dependent agent who habitually exercises authority to conclude contracts on your behalf there. When either trigger is a possible yes, risk is active enough to pause expansion and verify your position.

Trigger 1 is place-based. A fixed place through which your business is carried on can create exposure even if your entity is formed elsewhere. Document early how that place is actually used.

Trigger 2 is authority-based. Dependent agent permanent establishment risk can arise when someone in-country habitually exercises authority to conclude contracts for your business. Focus on actual behavior and authority, not just titles.

Use a pause-and-verify rule as soon as facts start repeating:

- If either trigger looks recurring, stop new in-country commitments until reviewed.

- Test your facts against applicable treaty language and domestic law.

- Compile records now: place and access evidence, contract authority terms, and who actually negotiated and finalized agreements.

To reduce ambiguity, add one operational check at each contract cycle: compare written authority to real conduct.

- Who was permitted to approve terms.

- Who actually approved terms.

- Where the approval happened.

When those three points diverge, treat that as a prompt for immediate review. Once either pattern is established, reporting, filing, and payment obligations in that country may follow. Escalate early when facts are unclear.

Treaty Rules and Local Law Can Point in Different Directions#

Start with treaty text, then test the same facts under domestic tax law in the relevant contracting state. That order helps reduce false confidence when risk is not clearly low.

Treaties often override, modify, or supplement local law, but not in the same way in every jurisdiction. Use the treaty as your starting point, then confirm how local law and local interpretation apply in practice.

| Step | What to check | Why it changes risk |

|---|---|---|

| 1 | Exact treaty article text and definitions | One definition can narrow or widen PE scope |

| 2 | Domestic tax law treatment in that country | Local rules can fill gaps or interpret terms differently |

| 3 | Match your facts to both | The outcome depends on treaty language and actual behavior |

Model conventions are orientation tools, not shortcuts. OECD model language and commentaries are often used as a default reference point, but wording can differ in U.S. model treaty language, and UN-model references show alternative approaches. Similar operating facts can produce different outcomes across treaties.

A practical U.S. example shows the split. Under an applicable treaty election, tax is generally limited to profits attributable to a U.S. PE, while domestic U.S. trade-or-business scope can be broader than PE. One test does not answer both questions, and IRS practice-unit summaries are guidance, not binding law.

A reliable way to run this review is to keep one two-column note per country:

- Column A: what the treaty text appears to permit or limit.

- Column B: how domestic law appears to apply to your same facts.

Then add a short mismatch line:

Aligned: both columns point to the same practical result.Mixed: the columns support different outcomes or use terms differently.Unknown: you cannot complete one column with current evidence.

Any result other than aligned should trigger escalation before expansion.

Use this verification checkpoint before signing new contracts or increasing activity:

- Save exact treaty article text and definitions relevant to PE and related tests.

- Keep a short note on how domestic tax law in that country interprets those terms.

- Map your facts in writing to both: key operating facts and which profits could be attributable.

- Recheck when facts change, not only at year-end.

A second safeguard helps in practice: date every interpretation note and name the owner. Undated notes can linger after facts change, which increases avoidable risk. If treaty language and local interpretation point in different directions, treat that as an escalation trigger before expansion.

Where Freelancers and Consultants Accidentally Cross the Line#

You can cross the line through repeat behavior, not one trip. Risk rises when in-country activity starts to look like ongoing local business operations, even if it began as temporary support.

A short client visit and recurring in-country deal closing do not carry the same risk profile. Repeated in-country deal closing by a representative is a clear review trigger.

Do not assume only formal office presence matters. You can face PE questions without opening a formal office because relevant presence is not limited to office space.

Subsidiary structures are another area where people over-assume. This grounding does not support a simple rule that a subsidiary alone creates or prevents PE, so do not rely on structure-only conclusions. Verify risk with formal review.

Day counts can help as an early warning signal, but they are not a complete answer. The 183-day benchmark is common, but not determinative on its own.

The usual failure mode is drift:

- A temporary local helper starts joining negotiation calls.

- Commercial urgency leads to ad hoc local approvals.

- Contract language stays narrow while behavior expands.

By the time someone asks for records, the timeline is hard to reconstruct.

Use this operating rule:

- If a local helper can bind contracts, treat it as potential PE exposure immediately.

- If that authority is used repeatedly, escalate for formal review rather than informal monitoring.

- If local premises are used repeatedly for core activity, classify that as a PE risk signal until checked.

- Keep dated records now: travel logs, contract redlines, approval emails, and monthly notes on who closed terms.

Add one monthly question that catches drift early: did actual authority this month match written authority? A single no is enough to reopen your PE screen. If authorities view your business as operating in-country, they may assert PE and related liabilities, including corporate tax exposure and other local obligations. In gray-zone facts, tighten documentation and escalate before you expand activity. Related: How to Create a Financial Safety Net as a Freelancer.

Use This Five Checkpoint Screen Before Entering a New Country#

Run this screen before you start selling in a new market. If checkpoint 1 or 2 is a clear yes, treat risk as active and pause expansion until your treaty and domestic-law position is documented.

| Checkpoint | What to review | Key details |

|---|---|---|

| Fixed place of business in the host country | Whether you control, or repeatedly use, a local place for core business activity | Dated records of where work happened, who had access, and which contracts were supported from that location |

| Dependent agent authority | Whether anyone in-country habitually concludes contracts for you, not just introduces leads | Who can present final terms, who can approve final terms, and who sends the acceptance that finalizes terms |

| Treaty position vs domestic tax law | The bilateral income tax treaty, then domestic tax law against the same facts | Treaty provision reviewed, domestic-law rule reviewed, current result, and known unknowns |

| Taxes in scope now vs later | Corporate income tax, payroll taxes, and other applicable taxes | One line for each tax type in your country note with owner and status |

| Evidence for source-country review | Whether the file has detailed records, proper registration status, and regular compliance reviews | Records with date, country, and responsible person visible without extra interpretation |

- Fixed place of business in the host country

Check whether you control, or repeatedly use, a local place for core business activity. Repeated use that looks like an operating base can be a risk signal under applicable rules. Keep dated records of where work happened, who had access, and which contracts were supported from that location.

Do not stop at yes or no. Capture the business relevance of that location:

- Which services were delivered from there.

- Which contracts were supported from there.

- Which months showed repeated use.

If your note cannot connect location to business activity, you will likely revisit the same question later with less clarity.

- Dependent agent authority

Check whether anyone in-country habitually concludes contracts for you, not just introduces leads. If someone can bind terms in practice, treat it as potential dependent-agent exposure and escalate early.

Match authority language to behavior:

- Who can present final terms.

- Who can approve final terms.

- Who sends the acceptance that finalizes terms.

The person doing the final step in practice is the key data point for this checkpoint.

- Treaty position vs domestic tax law

Review the bilateral income tax treaty, then test domestic tax law against the same facts. In the U.S. context, the threshold for a U.S. trade or business is broader than the threshold for creating a U.S. permanent establishment under treaty rules. When an applicable treaty position is claimed, U.S. tax is generally tied to profits attributable to a U.S. permanent establishment.

Keep this entry note short and explicit:

- Treaty provision reviewed.

- Domestic-law rule reviewed.

- Current result.

- Known unknowns.

Known unknowns are not a weakness. They show that uncertainty was identified and managed. Also note that the IRS practice unit often cited for this point is training material, not a binding legal pronouncement.

- Taxes in scope now vs later

Track tax workstreams separately from day one: corporate income tax, payroll taxes, and other applicable taxes. Do not assume one conclusion settles all tax types.

A practical step is to keep one line for each tax type in your country note with owner and status. It prevents PE activity from crowding out other obligations that can mature on different timelines.

- Evidence for source-country review

Plan for authorities to ask for proof, not just intent. Maintain a current file with detailed records, proper registration status, and regular compliance reviews, including contract-signature authority and work-location support. Late filing can create avoidable penalties.

Quality of evidence matters as much as quantity. For each record, make sure date, country, and responsible person are visible without extra interpretation. When facts are mixed, use a risk-first default: limit local contract authority, tighten location controls, and get formal advice before scaling in-country revenue.

A useful closeout for this screen is a one-page country decision note:

Go: evidence supports monitor posture with named recheck triggers.Conditional go: entry allowed with active controls and near-term review date.Hold: unresolved authority or location facts require escalation first.

That one page keeps commercial timing aligned with tax reality. You might also find this useful: A Guide to Gift Tax for US Expats.

Build a PE Evidence Pack Before You Need It#

If your five-checkpoint answers are mixed, build your PE file now. A clear record is easier to explain later, especially on operating facts and how profits were attributed at that time.

| File section | What to include | Key detail |

|---|---|---|

| Contract and authority records | Signed agreements, approval chains, and a signature-authority matrix by country and entity, where relevant | Who could conclude terms and when that authority changed |

| Operating evidence | Work-location logs and service-delivery records | Date key milestones and tie them to place |

| Legal and tax position file | The treaty article you relied on, your domestic-law analysis against the same facts, and OECD Model Tax Convention material as interpretive context alongside treaty text | Which version you reviewed when model commentary informs your interpretation, including updates that cover Commentary on Article 5 |

| Attribution questions | A memo when goods, services, or intangibles move between a PE and the home office | Link each allocation line to supporting records such as contract terms, delivery artifacts, or internal approvals |

Start with contract and authority records:

- Keep signed agreements and approval chains.

- Maintain a signature-authority matrix by country and entity, where relevant.

- For each setup, record who could conclude terms and when that authority changed.

Give each authority change a date and reason. Review is easier later when you can show when the old rule ended and when the new rule began.

Add operating evidence:

- Keep work-location logs and service-delivery records.

- Date key milestones and tie them to place.

- Make timeline shifts visible when material facts change across countries or entities.

Treat timeline quality as a control. If an event cannot be placed in time and country, flag it as incomplete rather than assuming it will be obvious later.

Keep a legal and tax position file:

- Save the treaty article you relied on and your domestic-law analysis against the same facts.

- Use OECD Model Tax Convention material as interpretive context alongside treaty text.

- Note which version you reviewed when model commentary informs your interpretation, including updates that cover Commentary on Article 5.

Document attribution questions separately:

- Create a memo when goods, services, or intangibles move between a PE and the home office.

- Link each allocation line to supporting records such as contract terms, delivery artifacts, or internal approvals.

To keep this practical, tie review to business events:

- Contract renewal cycle.

- New local representative.

- Scope expansion in a country.

- Changes in who can approve or conclude terms.

Use a simple status marker for each country file:

Current: no material fact change since last review.Update needed: fact change recorded, interpretation pending.Escalate: high-risk fact pattern or unresolved treaty and domestic-law conflict.

This turns the evidence pack from a year-end scramble into a living record that supports decisions while they are still reversible.

Red Flags That Should Trigger Professional Advice Immediately#

Get professional advice immediately when these signals appear, especially in combination. Do not treat them as routine recordkeeping issues.

| Red flag | Detail |

|---|---|

| Fixed place of business profile | You may have a fixed place of business profile in a host country tied to ongoing local activity |

| Dependent-agent behavior | A local representative functions like a dependent agent by habitually concluding contracts or playing the principal role leading to contract conclusion |

| Treaty and local-law mismatch | Your treaty-based view and local domestic-law interpretation are pulling in different directions |

| Double-taxation relief not confirmed | Your plan depends on double-taxation relief, but eligibility, method, or timing is not confirmed |

Treat these as decision risks, not admin tasks. PE risk can mean local authorities view your company as an ongoing in-country enterprise, with potential corporate tax exposure in that jurisdiction.

Do not rely on day-count shortcuts alone. There is no universal 30-to-183-day rule that automatically creates or avoids PE. Also, do not assume double-taxation relief applies automatically; some relief rules are context-specific. Confirm the exact mechanics before you call risk controlled.

When a red flag appears, take immediate containment steps:

- Pause contract changes that increase local authority.

- Preserve current records before they are edited or deleted.

- Set a clear owner and date for external review.

Quick containment does not resolve the legal question, but it preserves evidence quality while you resolve it.

Choose Your Risk Posture on Purpose, Not by Accident#

Choose your posture deliberately. For many freelancers and consultants, a conservative default is easier to defend when facts or local interpretation are unclear.

A conservative posture means documenting earlier and more consistently, so you are not rebuilding your position under pressure later. An aggressive posture can reduce near-term admin, but it can make disputes and cleanup harder if facts drift or your interpretation is challenged.

| Posture | Working assumption | Near-term burden | If you are wrong |

|---|---|---|---|

| Conservative | Local interpretation may be stricter than your first read | Higher admin now | You may over-document or do work earlier than strictly necessary |

| Aggressive | A narrow interpretation will hold if reviewed | Lower admin now | Retroactive defense can be harder if that interpretation is challenged |

Keep it intentional with one recurring checkpoint:

- Maintain a dated memo of your current position and assumptions.

- Keep contract authority and decision records current by country.

- Reconcile where work is performed with where revenue is earned.

- Trigger external review when your footprint, authority model, or country mix changes.

A practical way to choose posture is to score your own evidence quality first:

- Clear and current records by country support monitoring decisions.

- Partial or stale records support conservative handling until fixed.

- Contradictory records support immediate escalation.

Practical default: stay conservative unless your documented facts are clearly low risk and stable over time.

Turn Tax Concepts Into Daily Operating Controls#

Your posture is easier to defend when records make each tax judgment traceable. Treat PE review as an operating control, not a one-time legal memo.

When work spans countries, keep one country-level record tying together where work happened, who had authority, and where revenue was recognized. If those records sit in separate tools, your position is harder to defend under review.

Use U.S. treaty framing as a cautionary example, not a universal rule. In that context, treaty treatment can generally limit U.S. tax to profits attributable to a U.S. permanent establishment, while U.S. trade or business activity can still be broader than activity that creates PE. If you track only totals and not activity type, you can lose clarity on how effectively connected income is characterized.

Set a source hierarchy in every decision note: cite the bilateral income tax treaty and domestic tax law first, then label secondary guidance. An IRS practice unit like TRE/9450.06_02(2014) with last update 09/03/14 can support interpretation, but it explicitly says it is not an official pronouncement of law.

Build this into normal operations:

- Link each invoice and payout to country, contracting entity, and service period.

- Keep a live authority register by jurisdiction.

- Store location evidence for delivery and management activity in the same review trail.

- Save treaty and domestic-law position notes with date and owner.

- Reopen the PE screen before new market entry, a new local representative, or new contract authority.

Add a monthly close that keeps this practical:

- Confirm any change in who can approve or conclude terms.

- Reconcile location logs against contracts active that month.

- Update country notes where facts changed.

- Mark unresolved items for escalation before the next sales step.

If a trigger fires and the evidence file is incomplete, pause the scale step until the file is complete. The short-term cost is admin time. The larger risk is weaker support for your tax position if challenged.

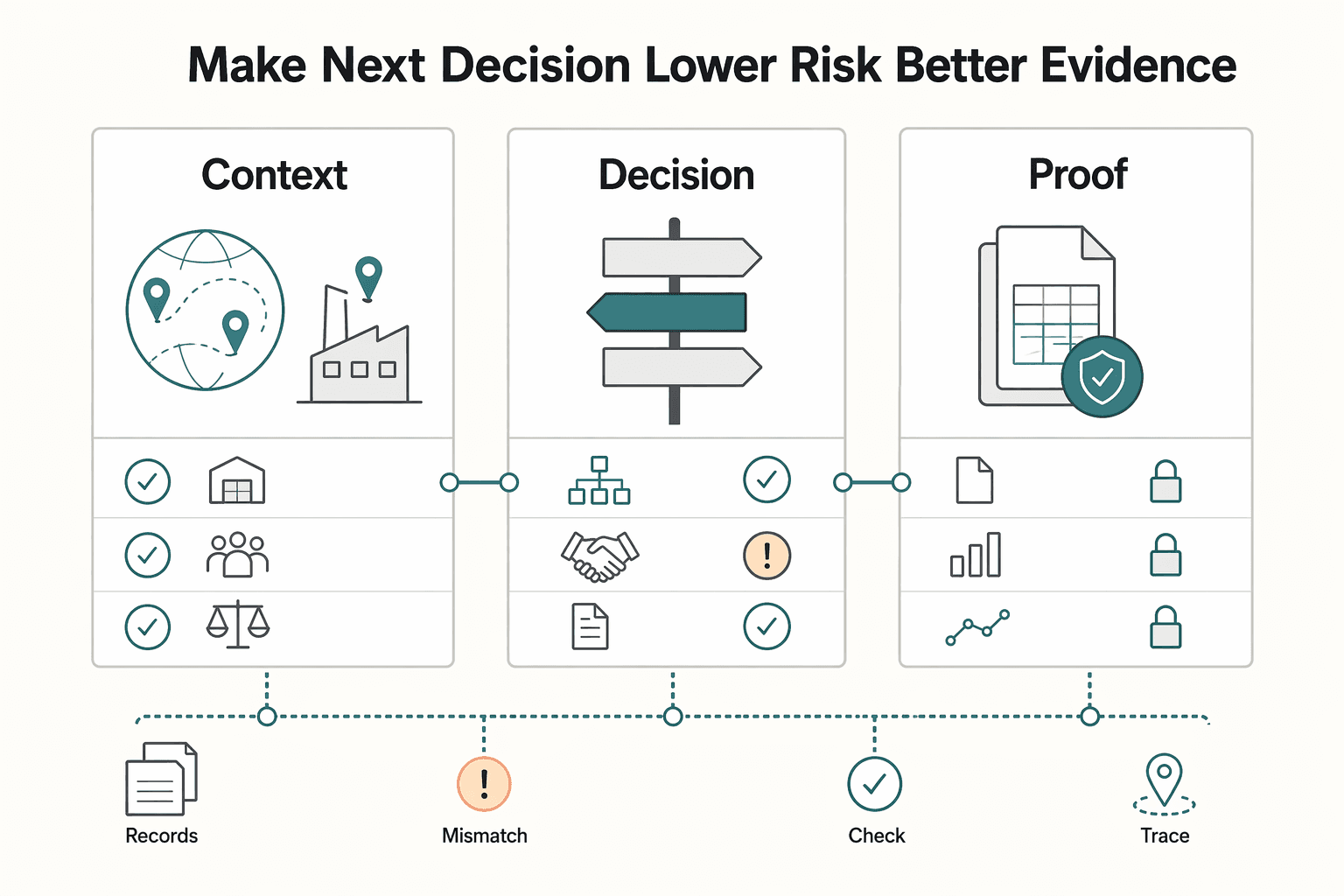

Make the Next Decision With Lower Risk and Better Evidence#

Treat the next move as a decision about presence, authority, and proof, not just a definition. When any one of those is unclear, assume risk is still live and slow expansion until your file is defensible.

Use these takeaways as a repeatable gate. Run the five-checkpoint screen before each market change. Compare the result with your last documented position, then update your position as facts change.

Keep one distinction clear in the U.S. example. In one IRS practice unit, a foreign company carrying on a U.S. trade or business is described as subject to U.S. tax on effectively connected income, while treaty election generally ties U.S. tax to profits attributable to a U.S. permanent establishment. Those tests are not always the same, so do not treat them as interchangeable.

For each country, confirm your position against applicable bilateral treaty text and domestic tax law first, then use interpretive materials as secondary context. That is a responsible way to scale when outcomes vary by jurisdiction and fact pattern.

Before your next expansion step, run this closeout sequence:

- Re-run the five-checkpoint screen and record pass or fail by country.

- Refresh your evidence pack with current contracts, authority records, work-location logs, and income mapping.

- Re-check that treaty assumptions still match current activity.

- Escalate quickly on red flags, especially unclear authority, mixed location evidence, or unresolved treaty interpretation.

- Pause launch if records cannot clearly show who acted, where, and how income was characterized.

One final discipline keeps decisions clean: attach a date, owner, and next review trigger to every country position. That turns a static memo into an active decision record and makes the next review faster and less error-prone. If you need cleaner cross-border records and audit-ready payment trails, use tools that keep exports traceable and reconciliation consistent.

Frequently Asked Questions

What creates a permanent establishment for a freelancer or consultant?

A permanent establishment is a taxable presence outside your company's state of residence. Common triggers include a fixed place of business or activity through a dependent agent. Authorities also assess activity patterns beyond a classic office-only test. A practical check is whether your facts show a fixed business location, dependent-agent activity, or in-country contract-concluding authority. If yes, PE risk may be active until treaty and domestic-law review clarifies treatment.

Can I create PE without opening an office?

Yes. PE risk is not limited to opening an office because authorities look beyond a strict bricks-and-mortar view. A representative office may or may not create PE depending on which activities are carried out through it. The safer approach is to document actual activity rather than rely on labels. What people did, where they did it, and who could conclude terms are key facts in the analysis.

Does using a local contractor or representative create dependent agent PE risk?

It can. Risk rises when in-country activity is involved in concluding contracts. If representative-office activity is combined with in-country contract-concluding activity, many countries would likely view PE as constituted. To manage this, compare contract language to actual conduct each cycle. If conduct is broader than the written role, escalate before renewing or expanding.

Does a subsidiary automatically mean I have PE in that country?

This grounding does not provide an automatic rule for subsidiaries. Whether PE exists still requires reviewing underlying activities and authority in that country. Treat subsidiary presence as a fact to evaluate, not a conclusion by itself. You still need activity records, authority records, and treaty and domestic-law testing.

Do tax treaties always protect me from local taxation?

No. Country thresholds vary, and treaties can raise or lower those thresholds rather than eliminate risk in every case. Review the specific bilateral treaty and local law before relying on protection. If your facts are not clearly mapped to treaty text and local interpretation, confidence is weaker even when treaty language looks favorable.

What is the difference between PE risk and VAT or GST registration?

This grounding defines PE as taxable presence outside the company residence state. It does not provide VAT or GST rule details. Do not treat a PE conclusion as a substitute for VAT or GST review. Keep separate decision notes for each tax type. That prevents a correct PE view from creating false comfort on indirect tax obligations.

When should I talk to a cross-border tax professional instead of handling this myself?

Escalate when your facts involve local representatives, contract-concluding activity, or unclear treaty effects across countries. Get advice when you cannot clearly map activities to treaty and domestic-law treatment. If your position is unclear, pause expansion decisions until the analysis is documented. Also escalate when your records are incomplete at the same time risk appears active. Professional review is easier before authority, location, and attribution evidence becomes fragmented.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

How to Create a Financial Safety Net as a Freelancer

Your **freelance financial safety net** is more than a savings balance. It is the set of controls that lets you cover fixed obligations on time when receipts are uneven, and it keeps invoiced revenue separate from cash you can actually spend. The goal is not to predict every slow month. The goal is to reduce the chance that one late client payment turns into missed bills, tax pressure, or borrowing.

Gift Tax for US Expats Without Filing Surprises

Keep filing season calmer by deciding early which lane each transfer belongs in: `Form 3520` or not reportable under these rules. For a U.S. person living abroad, the practical order is to get the U.S. filing lane right first, then sort the cross-border details that raise risk.